Hello Interconnected Readers:

I had a busy week last week that was mostly self-created. While still doing volunteer work at the Reno campaign office (work doesn’t stop when Election Day is over) and continuing my day job as an investor (doing calls with founders, helping with recruiting), I took it upon myself to produce an English version of Jack Ma’s Bund Finance Summit speech and focused my weekly deep dive on providing additional context and nuances to the speech. (You can read them here and here.)

[If you’d like to skip ahead to the six news stories and commentaries – three from English language sources, three from Chinese language sources -- here are this issue’s items:

- “The unsigned Op-Eds that foreshadowed Ant Group IPO suspension” (English Source: TechNode)

- “China draws up first antitrust rules to curb power of tech companies” (English Source: Financial Times)

- “U.S. Backs Down on TikTok” (English Source: Wall Street Journal)

- “10 days after IPO suspension, Ant Group appoints Li Chen as head of compliance” (Chinese Source: Sina Finance)

- “Rumor: Huawei plans to sell Honor product line for 100 billion yuan, Digital China and others will take over” (Chinese Source: CN Beta)

- “A Li Xueqin personal livestream sales event filled with bots: 3.11 million views, less than 110,000 are real humans” (Chinese Source: Deep Net)]

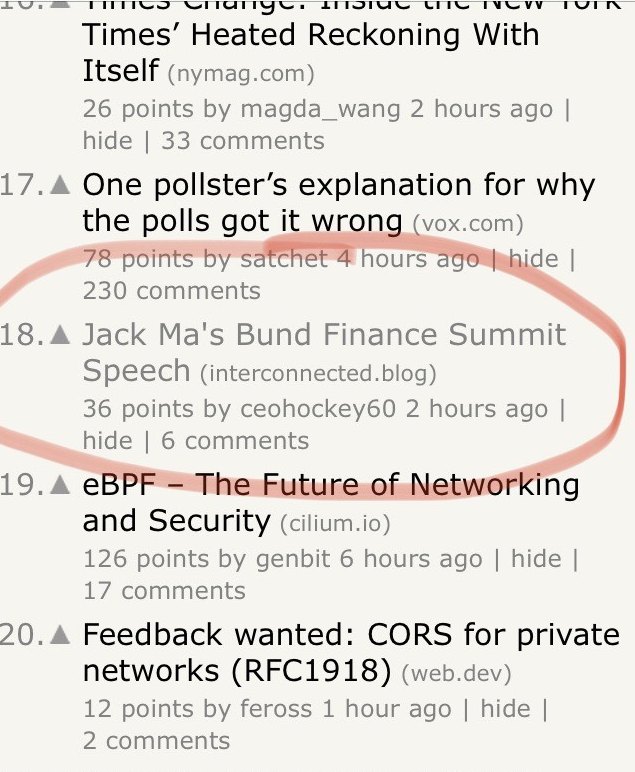

Both pieces received a lot of positive reactions. The speech made it onto Hacker News front page. The deep dive analysis was shared and referenced.

Counterpoint: "Jack Ma, by speaking up in public, focused all the regulatory attention on Ant Group as the example to look at. The speech…gained Ant a seat at the table…He knew what he was doing and got what he wanted."@kevinsxu https://t.co/YEMSD7Nezp

— Jonathan Cheng (@JChengWSJ) November 12, 2020

I’m obviously happy that people found my work useful, but last week’s experience also illuminated something deeper that caught me by surprise: the lag in information flow between the Chinese language and the English language world.

Jack Ma gave his speech on October 24. I didn’t watch it until November 4, because I was busy with the election. I didn’t decide to translate it until November 9, when I watched it for a second time and thought it was compelling enough to be worth translating -- something I rarely do because Interconnected is focused on original work. In the period between Ma giving the speech and my translating the speech -- 16 days -- it appears that there was no other published English version of it. And if I got lazy and didn’t do it, perhaps we still won’t have one?

Maybe this is my personal bias as someone obsessed with speechwriting, but I think a good, consequential speech should be watched, listened to, and read in its entirety in order to be fully understood. Regardless of which side of this issue you are on, we can all agree that Ma’s speech was consequential. Its impact may not have been obvious initially, but surely became obvious when Ant’s IPO was suspended on November 3.

I will continue to do my little part by continuing to write Interconnected. But I hope more people produce bilingual content and contribute to the information flow between the English and Chinese language world, so we don’t depend on the free time of some random person on the Internet like me -- 16 days after something big happened.

Real improvement in US-China relations depends on it.

Kevin

The summary below covers the period between November 9 - 15, 2020 of six news stories – three from English language sources, three from Chinese language sources. Disclaimer: all translated article titles are done by me, not official translations from the media outlets.

Before you go on, please check out last week's deep dive post: "Jack Ma, P2P Lending, Responsibility, Legacy"

“The unsigned Op-Eds that foreshadowed Ant Group IPO suspension” (English Source: TechNode)

My Thoughts: This is one of the best pieces of reporting on Ant’s suspended IPO, which combs through the impact and implications of the various unsigned Op-Eds published in response to Jack Ma’s speech from official publications run by key regulatory authorities, like the People’s Bank of China. These essays are important primary sources to pay attention to, if you want to read the tea leaves and anticipate any Chinese government actions on, well, everything! Understanding their substance, as well as the rumored identities of who these “senior scholars” really are, is just as valuable as parsing through an official communique. Highly recommend this article.

“China draws up first antitrust rules to curb power of tech companies” (English Source: Financial Times)

My Thoughts: China’s antitrust actions have been rumored for quite sometime -- I made a brief comment on it back in August. Like many parts of China’s economy, antitrust as a regulatory realm is young and without many precedents; the only one I can think of was the Tencent vs. Qihoo360 case (or the “3Q War”) back in 2010. By comparison, the current US antitrust regime was formed more than 100 years ago, based primarily on the Sherman Act of 1890, the Clayton Act of 1914, and the Federal Trade Commission Act of 1914. There is a lot of updating the US antitrust system needs to cope effectively with the rise of Big Tech; the traditional definitions of monopoly power, market power, and predatory pricing don’t really work when tech products are effectively deflationary. As for China, I hope the regulators take a more first-principle, sui generis approach to drafting these rules. Regulating Alibaba cannot be the same as regulating Amazon, but the experiences from both sides can be useful for each other.

“U.S. Backs Down on TikTok” (English Source: Wall Street Journal)

My Thoughts: Still remember the TikTok “ban”? I almost forgot myself, even though I wrote plenty of articles about it just two months ago. It seems like the Trump administration forgot about it too. As I’ve written before, I’m not opposed to a ban, if there is evidence, not just speculation, that products like TikTok and WeChat are being used as tools for foreign influence campaigns or to steal American people’s data. We just had an election. We should have real data to investigate now. But will we have serious regulators who would do their job?

“10 days after IPO suspension, Ant Group appoints Li Chen as head of compliance” (Chinese Source: Sina Finance)

My thoughts: Li Chen may be the person to watch, as we wait for not just Ant Group’s IPO to resume at some point, but also how new regulations on fintech will impact how companies will behave and comply -- something that Tencent, JD, Meituan, Xiaomi, etc. will all have to figure out. There’s not much information available on Li Chen, except that he appears to be an Ant veteran, having held executive positions in Ant’s division in Chongqing as well as the company's blockchain and cloud divisions.

“Rumor: Huawei plans to sell Honor product line for 100 billion yuan, Digital China and others will take over” (Chinese Source: CN Beta)

My thoughts: This sale could become official as early as this Sunday, likely before you get around to reading this weekly issue. I discussed this impending sale back in October, and it appears that Digital China (a key Huawei distributor and partner) along with a group of investors connected to the Shenzhen municipal government (where Huawei is headquartered) will be the buyers. There is rumor that the Honor unit may IPO in three years as an independent company after this sale. I maintain my previous opinion that this move is intended to keep its higher-end product, Mate, alive and competitive by consolidating internal resources and R&D focus. Veteran executive Gordon Orr of McKinsey also believes this sale is a "park and hold for me" strategy, rather than a "sell and move on." Only when the details of the sale is public, which may come soon, will we have a better sense of the bigger strategic intention behind the sale, if any.

“A Li Xueqin personal livestream sales event filled with bots: 3.11 million views, less than 110,000 are real humans” (Chinese Source: Deep Net)

My thoughts: Livestream e-commerce in China has been so huge for so long that young startups trying to replicate it in the US are fetching big funding rounds at a massive valuation. The latest example is Popshop, a two-year-old product that raised at a 100 million pre-money valuation from Benchmark, even though the app just came out of private beta and has ~3000 daily active users. This article on a recent Singles’ Day shopping livestream featuring Li Xueqin, a livestream star and comedian, reveals how many fake bots are behind the raw viewers and engagement metrics that people see on the surface. It also uncovers the overall frothiness of the livestream e-commerce industry, where streamers routinely buy fake engagement to generate buzz and, hopefully, sales. It’s an uncomfortable truth that US entrepreneurs, and the investors who fund them, should pay attention to.

(To close out on a lighter note, Li Xueqin happens to be my favorite Chinese comedian. Here’s one of my favorite routines of hers. Let me know if you like/dislike her humor and why!)

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

Hello 《互联》读者们:

我上周很忙,但主要是自找的。一直还在Reno的大选办公室做志愿者工作(虽然选举日过去了,但事情并没有忙完),还在继续我作为投资人的工作(与创业者交流,帮忙招聘),我又自发地把马云在外滩金融峰会的演讲翻译成了英文,上周的深度分析文章也是围绕这套演讲的大背景和细节。(您可以在这里和这里看。)

【如果您想直接跳到本期的六条新闻总结和评论,三条原文是英文,三条原文是中文,以下是本期的文章标题:

- “未署名的评论文章,预示了蚂蚁集团IPO的暂停”(英文来源: TechNode)

- “中国制定首套反垄断规则,遏制科技公司的势力”(英文来源: 英国金融时报)

- “美国收敛对TikTok的禁令’”(英文来源: 华尔街日报)

- “IPO暂缓10天后 蚂蚁集团已任命李臣为合规负责人” (中文来源: 新浪财经)

- “传华为计划1000亿元出售荣耀,神州数码等接手” (中文来源: CN Beta)

- “一场李雪琴亲历的直播带货造假现场:311万观众真实数不到11万” (中文来源: 深网)】

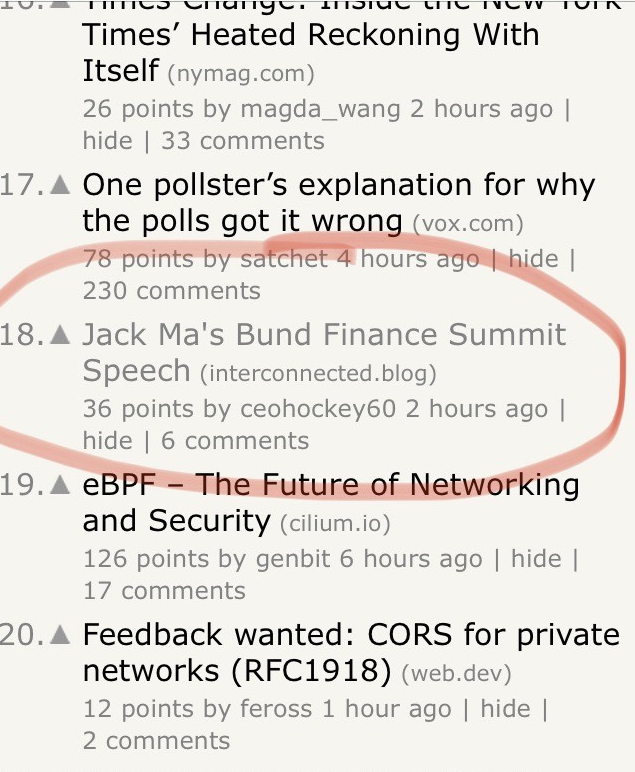

这两篇文章都得到了很多积极正面的反响。演讲那篇上了Hacker News的头条。深度分析的那篇也有被广泛分享和参考。

Counterpoint: "Jack Ma, by speaking up in public, focused all the regulatory attention on Ant Group as the example to look at. The speech…gained Ant a seat at the table…He knew what he was doing and got what he wanted."@kevinsxu https://t.co/YEMSD7Nezp

— Jonathan Cheng (@JChengWSJ) November 12, 2020

我当然很高兴读者觉得我写的东西有用,但上周的经历也照亮了一个更深的问题,让我有点吃惊:中文与英文世界之间信息交流的缓慢程度。

10月24日,马云发表了演讲。因为忙于大选,我直到11月4日才看了演讲。直到11月9日,我看了第二遍以后,才觉得它很有价值,值得翻译 -- 翻译是我很少做的事情,因为《互联》专注于原创作品。在马云发表演讲和我翻译他的演讲之间 -- 一共16天 -- 似乎没有其他的英文版本在网上出版。而如果我偷了个懒的话,也许现在还是不会有英文版?

也许这只是我做为一个痴迷于演讲稿写作的人的个人偏见,但我认为,一个好的、有影响力的演讲应该被完整地看、听、和读完才能被充分彻底地理解。无论您站在整个问题的哪一边,我们都可以在一点上达成一致:马云的演讲是有影响力的。它的影响一开始可能并不明显,但在11月3日蚂蚁IPO暂停时就非常明显了。

我将继续写《互联》来尽我的一份小贡献。但我希望会有更多的人写双语内容,为中英文世界的信息流通做出贡献,这样我们就不会在某些大事发生后16天,依赖像我这个互联网上的无名氏了。

中美关系如果要真正改善,有赖于此。

Kevin

本期《每周互联》的新闻总结概括的时间段是:2020年11月9日至15日,包括本作者挑选的六条新闻:三条原文是英文,三条原文是中文。声明:所有翻译的文章标题都是我做的翻译,不是官方翻译。

还希望大家有空看看我上周最新的深度分析文章:《马云,P2P借贷,责任,留给社会的遗产》

“未署名的评论文章,预示了蚂蚁集团IPO的暂停”(英文来源: TechNode)

我的想法: 这是我读到的关于蚂蚁暂停IPO事件最好的一篇报道,梳理了央行等主要监管部门主管的官方刊物针对马云的演讲发表的各种未署名专栏文章的影响和意义。如果您想揣测领导层的意向,预测政府对一切事情的未来行动,这些文章是很重要的原始资料,值得关注。了解这些文章的内容,以及传闻中这些 "资深学者 "背后的真正身份,和解析官方文献一样有价值。强烈推荐此文。

“中国制定首套反垄断规则,遏制科技公司的势力”(英文来源: 英国金融时报)

我的想法: 中国反垄断的政策出炉传闻已经出现一阵子了 -- 我在8月份的时候对此做了一个简短的评论。与中国经济的许多领域一样,反垄断作为一个监管概念还很年轻,没有太多先例;我唯一能想到的是2010年的腾讯和奇虎360的官司(俗称 "3Q大战")。相比之下,美国的反垄断监管制度形成于100多年前,核心的法律基础是1890年的《Sherman Act》、1914年的《Clayton Act》和1914年的《Federal Trade Commission Act》。为了有效地应对和制约科技巨头们的势力,美国反垄断制度的许多地方需要更新,当科技产品的本质是通货紧缩的时候,传统定义的垄断力、掠夺性定价就不太适用了。至于中国,我希望监管机构在起草这些规则时采取更多的第一原则、自成原创的思考方式。监管阿里的方式不能和监管亚马逊一样,但两边的经验是可以互相借鉴的。

“美国收敛对TikTok的禁令’”(英文来源: 华尔街日报)

我的想法: 还记得TikTok的 “禁令” 吗?我自己都差点忘了,尽管两个月前我还写了很多关于这个话题的文章。看来特朗普政府也忘了。我在以前的文章里表过态,如果有证据,不仅仅是猜测,能证明像TikTok和微信这样的产品被用作外国煽动影响活动的工具,或者窃取美国人民的数据,我不反对禁令。刚刚举行了一次选举,现在应该有真实的数据来做调查。但会有认真的监管者来做他们该做的工作吗?

“IPO暂缓10天后 蚂蚁集团已任命李臣为合规负责人” (中文来源: 新浪财经)

我的想法: 李臣会是个值得关注的人,因为我们等待的不仅仅是蚂蚁集团在未来的什么时候重启IPO,而是监管金融科技的新规则宣布后将如何影响各个企业的行为和合规。 这是腾讯、京东、美团、小米等等都要弄清楚的。关于李臣的信息并不多,只知道他应该是蚂蚁的老将之一,曾在蚂蚁在重庆的小额贷款有限公司,以及集团的区块链和云部门担任过高管职位。

“传华为计划1000亿元出售荣耀,神州数码等接手” (中文来源: CN Beta)

我的想法: 荣耀的出售最早可能在本周日就被宣布,很可能在您读到本周刊之前。我上个月评论过当时关于出售的传言,看来神州数码(华为的重要分销商和合作伙伴)以及与深圳市政府(华为总部所在地)有关的一批投资机构会是买家。还有传言称,此次出售后,荣耀部门可能会在三年内以独立公司的形式上市。我维持之前的观点,此举是为了通过整合内部资源和研发重点,来保持其高端产品Mate的竞争力。资深高管麦肯锡的Gordon Orr还认为,这次出售是一种 "先帮我临时持有"的策略,而不是 "完全卖掉,勇往直前"。只有当出售的细节公开后(可能很快就会揭晓),我们才能更好地了解出售荣耀背后更大的战略意图(如果真有任何战略意图的话)。

“一场李雪琴亲历的直播带货造假现场:311万观众真实数不到11万” (中文来源: 深网)

我的想法: 直播电商在中国已经发展了很久,以至于试图在美国复制它的年轻创业公司都能以昂贵的估值融到大笔资金。最新的例子是Popshop,是个才成立两年的产品,以1亿美元的预估价从Benchmark那里融到了钱,尽管产品才刚从测试beta版出来,日活跃用户约3000人。这篇文章分析了由直播网红加脱口秀明星李雪琴出镜的最近一次双十一的直播带货,揭示了直播互动的背后其实很多都是机器bots做的,大家在表面上看到的浏览量和互动指数远远没有那么简单。它还揭露了直播带货行业的整体泡沫,直播大V们经常购买流量和互动来炒作,希望能带更多货。这是一个令人不舒服的事实,在美国的创业者,以及投他们的VC,也都应该注意。

(这一期来点轻松收尾:李雪琴恰好是我最喜欢的中国脱口秀演员。这是我最喜欢的一段表演,不妨看看?无论您喜欢还是不喜欢她的幽默,请告诉我为什么哈!)

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,和我交流互动!