With all the executive orders, CFIUS edicts, and additional sanctions placed on Chinese tech companies by the US, it’s hard to see where these companies - and by extension the Chinese Internet - can expand to. Certainly, China’s own economy will continue to grow, providing a meaningful amount of business and opportunities. But that won’t be enough to satisfy either the investors’ need for growth or the companies’ own raw ambitions.

So where can the Chinese Internet go to expand?

We can find some clues from the major Chinese cloud providers’ expansion plans, particularly Alibaba and Tencent. I’m focusing on cloud expansion as an indicator, because it is capital intensive (e.g. building data centers) and longer-lasting (you can’t just pack up and abandon a data center when things don’t work out -- it’s commercial real estate!). Cloud infrastructure is also a good proxy for the Internet as a whole, because all online services will eventually be run on the cloud, one way or another.

Alibaba and Tencent Cloud

Alibaba and Tencent Cloud are not only the two leading public cloud providers in China, they also have meaningful market shares around the world.

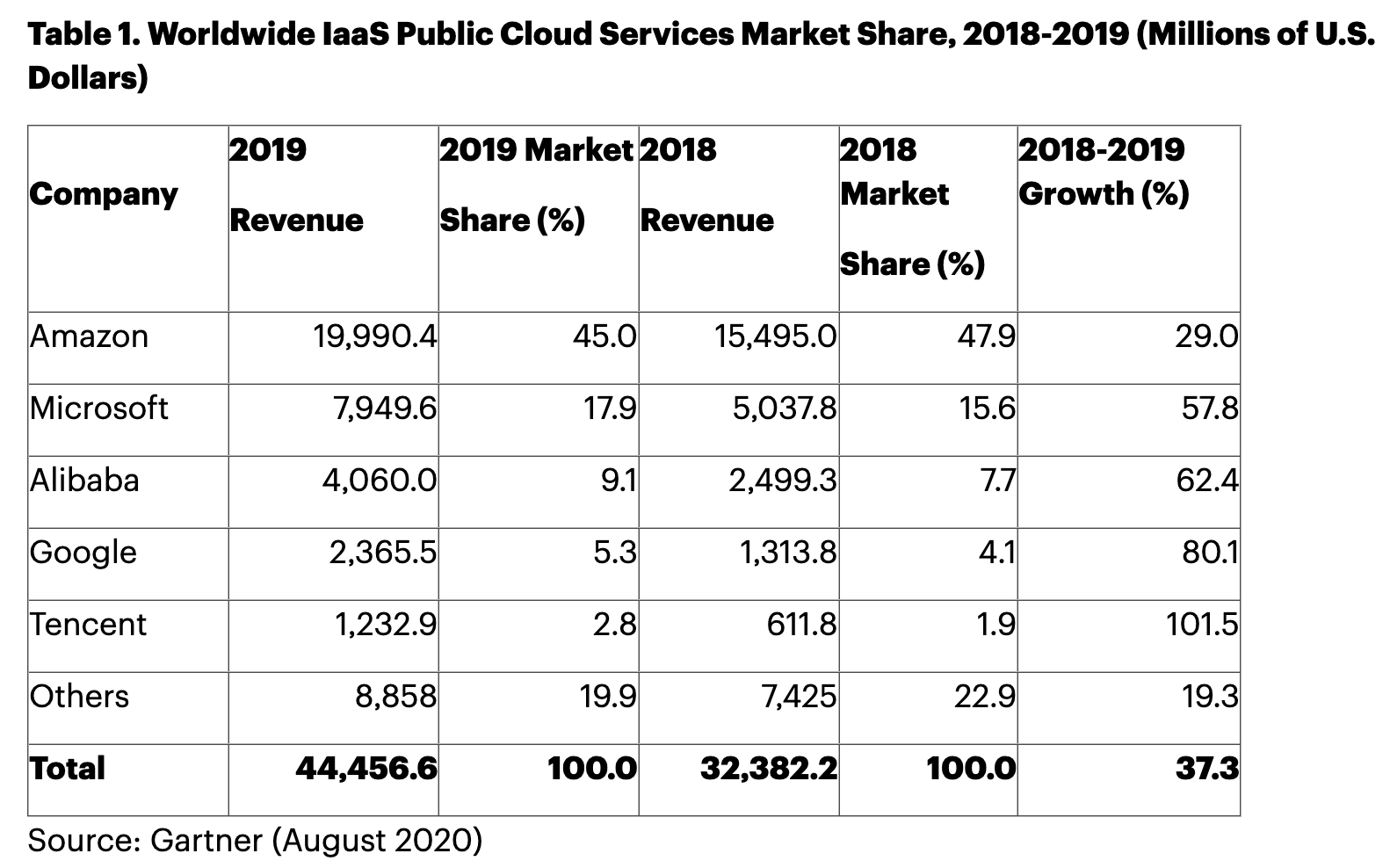

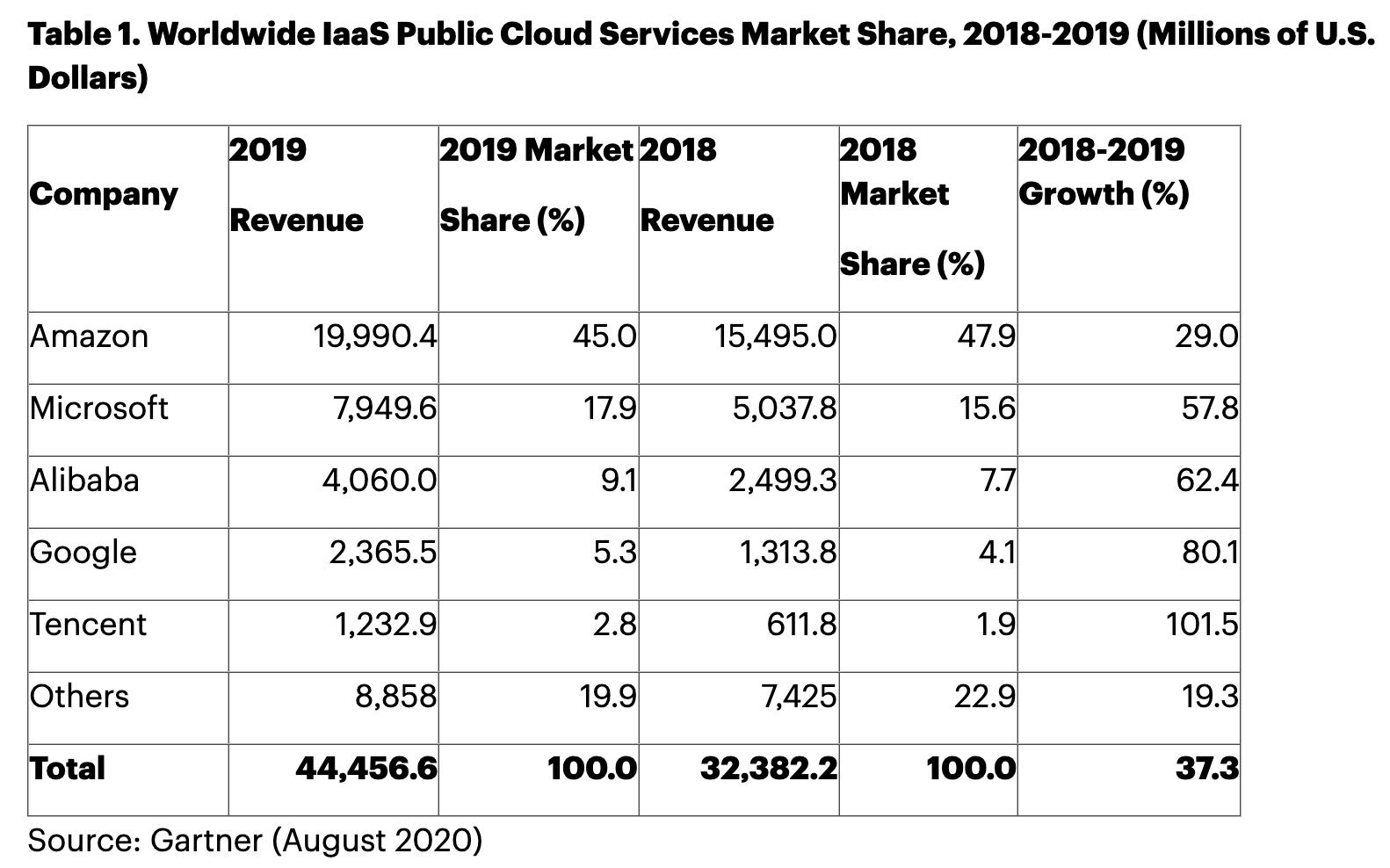

In Gartner’s newly released worldwide Infrastructure-as-a-Service (IaaS) market share report earlier this month, the top five are:

- AWS

- Azure

- Alibaba

- Tencent

Alibaba is the clear number 3, while Tencent made the cut at number 5. Notably, Tencent’s IaaS revenue grew by over 100% from 2018 to 2019, albeit from a small base. Other providers who may have bigger brand names, like IBM Cloud and Oracle Cloud, do not have big enough market shares to deserve their own rows in the spreadsheet.

According to Gartner, if we combine IaaS with Platform-as-a-Service (PaaS), Alibaba would still be at number 3 globally, while Tencent and Oracle would be in a virtual tie at number 5.

(These cloud acronyms can get confusing, so here’s a plain term definition of IaaS and PaaS. IaaS is data center hardware for rent; think raw server, storage, and networking capacity, maybe with a layer of virtualization on the bare metal machines. PaaS is the layer above IaaS, where the cloud vendors provide common building blocks for applications for rent: think containers, databases, logging, etc. I’m glad Gartner will combine these two categories in future analysis, because the line is basically indistinguishable and somewhat meaningless.)

With this current state of play in mind, let’s look at the massive amounts of investment both Alibaba and Tencent plan to make in their cloud unit. Back in April, Alibaba announced it plans to spend $28.2 billion USD to expand its cloud infrastructure in the next three years, which I explored in-depth in “Alibaba vs IBM: Fighting for Third Place in Cloud”. Not to be outdone, Tencent announced in May that it’ll invest $70 billion USD in the next five years to do the same.

Let’s put these eye-popping numbers in context. IBM’s acquisition of Red Hat two years ago, a pure cloud play to expand IBM’s hybrid cloud capabilities, was $34 billion USD, which was a 63% premium of Red Hat’s pre-acquisition valuation of roughly $21 billion USD. This was one of the largest acquisitions in tech history. Alibaba basically plans to build another Red Hat. Tencent plans to build two. And if you take Gartner’s analysis at face value, both are already materially ahead of IBM Cloud.

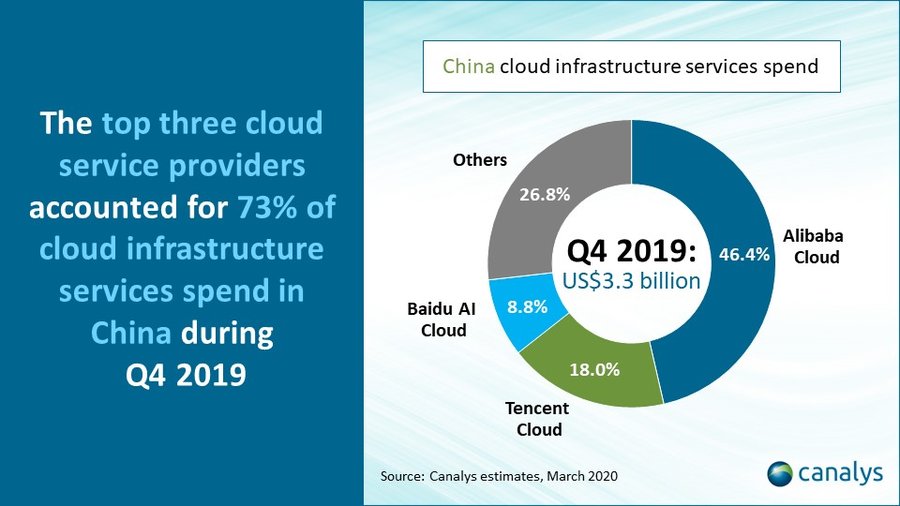

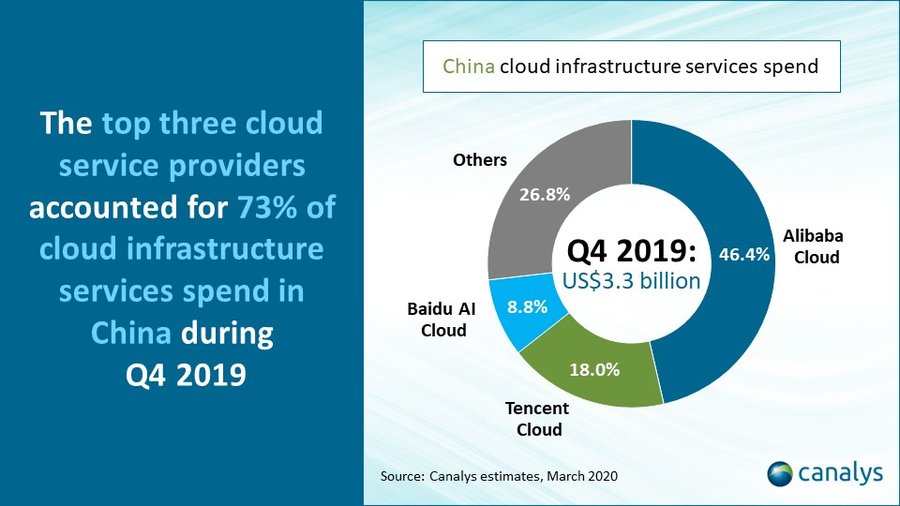

I understand that this comparison with Red Hat’s acquisition is a bit crude, but I hope it illustrates the pure magnitude of Alibaba and Tencent’s cloud investments. A big portion of these investments will go into China’s own rapidly growing cloud market. According to Canalys, China’s cloud infrastructure spending grew by 66.9% in Q4 of 2019 and by 63.7% for the entire year to exceed $10.7 billion USD, making it the second-largest cloud market in the world.

Given how closed China’s Internet economy is to outside players (AWS is the only non-Chinese cloud provider with a foothold), this growth will only benefit domestic companies.

Both Alibaba and Tencent Cloud already have many data centers outside of China. The new investments will likely be global. The only other Chinese cloud vendor that has a decent global presence is Huawei Cloud. However, considering the late-breaking new round of sanctions earlier this week that targeted all of its overseas cloud and R&D units, including the ones in Southeast Asia, Latin American, Europe, and Africa, Huawei will be in survival mode, not expansion mode, for the foreseeable future.

Southeast Asia, Latin America, Middle East

I chose Southeast Asia, Latin America, and the Middle East, because of their long-term economic potential and Alibaba and Tencent Cloud’s existing presence there, making them probable expansion destinations, even with all the geopolitical tensions swirling around us. I’m leaving out India -- an otherwise great expansion target -- because of its recent banning of many Chinese apps and intense animosity towards Chinese tech.

There are the data center maps of Alibaba and Tencent Cloud, respectively, as they stand today:

It’s important to look at cloud services longitudinally (or vertically) on a map, because time zone differences combined with geographical distance matter a lot for performance, user experience, and delivering timely customer support.

To illustrate this more concretely, data centers in North America plus customer successes teams can reasonably serve users in Latin America. Indeed, many American cloud providers do exactly that, until market traction is big enough in Latin America to justify building local data centers. The same can be said for data centers in Europe serving Africa, or data centers in India serving the Middle East.

Southeast Asia: as I described in detail in “Southeast Asia and the Pacific Light Cable Network”, the ASEAN region has a vibrant and burgeoning digital economy. There is a data center construction boom in Singapore. Some regional Internet giants started using Chinese cloud providers from the get-go -- Shopee on Tencent, Tokopedia on Alibaba (and later added GCP). Other major players use the leading American counterparts -- Gojek on GCP, Grab on AWS and Azure. Because the digital economy there is young, most of these startups are cloud-native to begin with. Given the existing inroads that Alibaba and Tencent have already made in the region, with strategic investments, acquisitions, and product expansion, Southeast Asia is a natural and relatively mature target to expand their cloud units further. Both existing cloud capacities in China and data centers in Southeast Asia can serve customers. Alibaba has also announced its plan to add a 3rd data center in Indonesia in 2021.

Latin America: Chinese tech firms, like ridesharing platform Didi Chuxing, have gained traction in Latin America, where local political and cultural resistance is not as strong as in the US. The continent’s overall cloud market is also projected to grow 38.3% CAGR between 2018-2023, according to IDC. Tencent already has a colocation presence in Sao Paulo, where most of the continent’s cloud data centers are situated. Both Alibaba and Tencent have an assortment of data centers in the US that probably have idle capacity to serve Latin American customers, because they are effectively shut out of the US market. Latin America also has an emerging digital economy with marquee players like Brazil’s Nubank, one of the largest neobanks (or pure digital banks) in the world. (Worth noting that Tencent has also been building its own neobank, WeBank.) I would not be surprised to see announcements by either Alibaba, Tencent, or both, building their first dedicated cloud data center in Latin America in the next two to three years.

Middle East: in terms of GDP per capita, the Middle East is roughly at the same level as Latin America. Israel has a very active tech scene with seven unicorns to date. Careem, the super app that combines ridesharing, payment, and delivery, spans most markets in the Arab world and was acquired last year by Uber for $3.1 billion USD. Zomato, the India-based food delivery service backed by Ant Financials, also has significant market presence in the Middle East. Alibaba has been eyeing the region for quite some time with a Dubai data center that came online in 2016. It entered the Turkish market with a partnership in 2018. Even though the Indian market’s sentiments have turned sour in the last few months, the two giants’ cloud capacities in India can serve its Middle Eastern customers just fine. As far as geopolitics is concerned, there is perhaps no single region (generalizing of course) that has more misgivings towards the US than the Middle East. The enemy of my enemy is my friend (and customer).

Land Grab Now, Profit (Much) Later

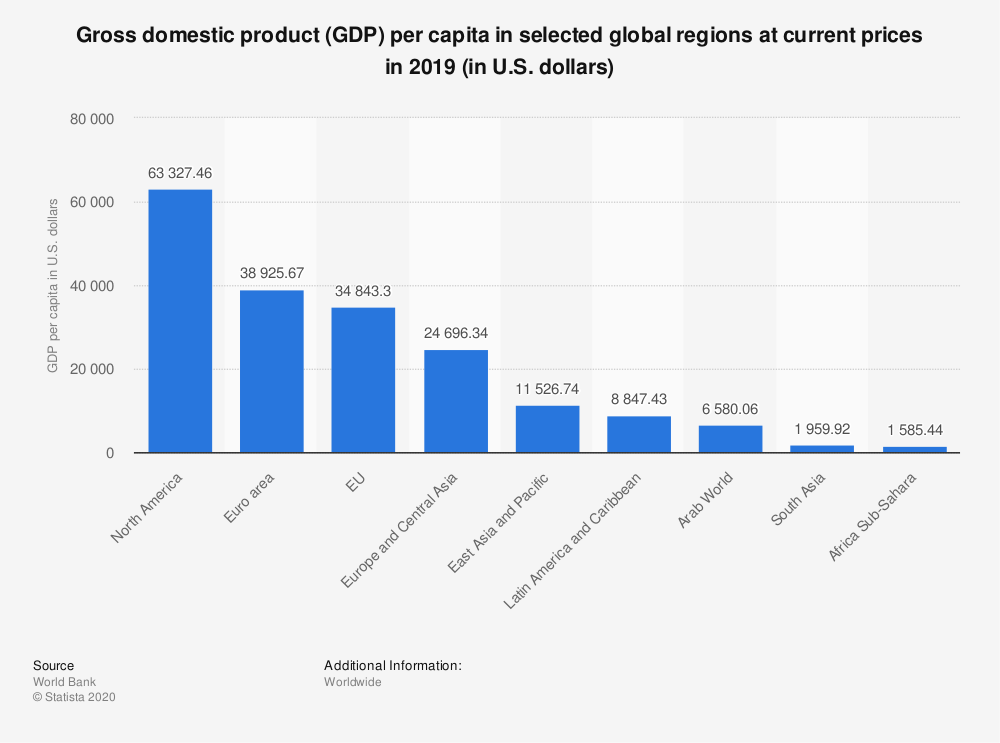

So far I’ve painted a fairly rosy picture of expansion opportunities. But the harsh reality is all these destinations are still quite poor, where meaningful revenue will not be generated for a long time. As shown in this chart of GDP per capita by regions, all areas of Asia, Latin America, and the Middle East trail the US and EU by a wide margin.

Although GDP per capita is typically a proxy for consumer spending, it can also serve as a signal for enterprise spending, since much of it is dictated by meeting consumer demands anyways.

For what it’s worth, the vast majority of the cloud industry is still in “land grabbing” mode, not “profit taking” mode. Everyone is focused on building out physical infrastructures and grabbing market share for now. That’s why most of the major cloud vendors, including Microsoft, Google, Oracle, IBM, and certainly Alibaba and Tencent, do not disclose any operating income (i.e. profit) that directly attributes to their cloud businesses. Instead, they report rough topline revenue numbers or just growth rates within dubious, non-standardized categories: “Commercial Cloud” (Microsoft), “Google Cloud” (Google), “Cloud & Cognitive Software” (IBM), and “Cloud Services and License Support” (Oracle). They are all likely losing a lot of money and will continue losing money in the foreseeable future.

The only exception is AWS, who reported a whopping $9.2 billion USD of operating income for its fiscal year 2019, where North America accounts for more than 75% of that income.

To “land grab”, offering bulk discounts of up to 80% in exchange for signing long-term (3+ years) deals is common in the cloud industry. An even more extreme example: according to Reuters, in 2017, Tencent apparently offered to complete a cloud project for the Fujian provincial government for a grand total of 0.01 yuan. Getting workload is the name of the game; revenue and profit must wait.

Thus, the Chinese Internet led by Alibaba and Tencent still have room to expand around the world. Smaller Chinese startups, who are in either Alibaba or Tencent’s orbit, can also expand on the backs of their cloud infrastructures to gain users and market share. But none of them will be making serious money from those expansions any time soon. Being shut out of the most lucrative markets of North America and parts of Europe hurts. A lot.

The big question is now (repackage a John Maynard Keynes saying): can geopolitics remain irrational longer than you can remain profitless?

If you like what you've read, please SUBSCRIBE to the Interconnected email list. New posts will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

中国互联网还能去哪里?

随着美国对中国科技公司的各种施压:行政命令、CFIUS法令和新的制裁,很难想象这些公司,以及整个中国互联网,还能扩张到哪里。当然,中国自身的经济将继续增长,提供新的商业机会。但这些巨头们不仅需要满足股东们对增长的需求,也要满足它们自己对全球化的雄心壮志。

那么中国互联网到底还可以去哪里扩大呢?

我们可以从中国领头的云厂家的扩张计划中找到一些线索,尤其是阿里和腾讯。我把重点放在云的扩展上是因为它需要巨大的资本投入(例如,建立数据中心),而且长期影响很大(不能业务一不顺利就随时打包放弃数据中心——那可是商业地产!)。云基础设施也是整个互联网的一个很好的抽象,因为所有的在线服务最终都会以某种方式在云上运行。

阿里和腾讯云

阿里和腾讯云不仅是在中国是领先的两家公有云,它们在全球也拥有可观的市场份额。

在Gartner本月早期发布的全球基础设施即服务(IaaS)市场份额报告中,排名前五的是:

- AWS

- Azure

- 阿里云

- 谷歌云

- 腾讯云

阿里云的市场份额舒舒服服的让它排在第三,腾讯云第一次打进前五。值得注意的是,从2018到2019年,腾讯的IaaS收入增长率超过100%,尽管基数较小。其他更有名的大牌云厂商,如IBM Cloud和Oracle Cloud,没有足够大的份额,不足以单独列出来。

根据Gartner的分析,如果我们将IaaS与平台化服务(PaaS)结合在一起,阿里云仍是全球第三,而腾讯和Oracle则并列第五。

(这些云行业内的缩写并不易懂,这里帮大家给IaaS和PaaS简单明了的做个定义。IaaS就是出租数据中心里的硬件;如服务器、存储盘和网络容量,也许在裸机上再加一层虚拟化。PaaS是IaaS之上的一层,云厂商在这一层提供出租各种通用的产品构建块:比如容器、数据库、日志等。我很高兴Gartner在未来的分析中将这两个类别结合,因为实际区别已经不大,也没什么意义。)

考虑到这一现状,让我们看看阿里和腾讯计划在其云部门未来的巨额投资。早在今年4月,阿里就宣布在未来三年内投入282亿美元扩展云基础设施,我在《阿里巴巴vs IBM:争夺云市场第三》那篇文章中做了些深度分析。腾讯也不甘示弱,5月份宣布将在未来5年内在云上投资700亿美元。

让我们把这两个惊人的数字换个方式理解一下。IBM两年前收购Red Hat,目的纯碎是为了云,扩展IBM的混合云产品服务,交易价为340亿美元,比Red Hat被收购时的约210亿美元市值溢价63%。这是科技史上最大的收购之一。阿里基本上准备再建一个Red Hat。腾讯准备建两个。如果我们相信Gartner的分析,两者已经遥遥领先IBM Cloud。

我承认,与Red Hat的收购做比较有点粗旷,但我希望它能更好的刻画出阿里和腾讯对云的投资的规模。这两笔投资很大一部分将是针对中国本身正在快速增长的云市场。Canalys的数据显示,2019年第四季度,中国云基础设施支出增长66.9%,全年增长63.7%,总体超过107亿美元,成为全球第二大云市场。

考虑到中国互联网经济对外企的封闭程度(AWS是唯一一家在中国有些生意的外企云厂商),增长总体只会让如国内厂商受益。

阿里和腾讯云已经在海外搭建了许多数据中心。新的投资也应该会是全球性的。另外一家在海外还有些业务和基础设施的国产云是华为云。但考虑到本周早些针对华为的新一组制裁,尤其针对它在海外的云和研发部门(包括东南亚、拉美、欧洲和非洲),华为在短期的未来将处于生死挣扎状态,而不是扩张状态。

东南亚、拉丁美洲、中东

我选择东南亚、拉丁美洲和中东三个地区,因为它们都有长期经济增长潜力,而且阿里和腾讯云已经在那里有基础,它们是最合理的扩张目的地,即使目前各地的地缘政治关系都更加紧张。我把印度排除在外,因为最近对中国apps的禁令和对中国科技总体的强烈敌意。要不然印度其实是很好的扩张目标。

这是阿里云和腾讯云的目前全球的数据中心地图:

在地图上纵向(或垂直)观察分析云服务是很重要的,因为时区差异和地理距离对性能、用户体验和及时提供客服都非常重要。

更具体地说明这一点:位于北美的数据中心结合客服团队可以很好的服务拉丁美洲的用户。事实上,许多美国公有云已经在这么做,直到拉美市场有足够大的体量来证明在当地建设数据中心是值得的。同样,在欧洲的数据中心可以为非洲服务,在印度的数据中心可以为中东服务。

东南亚:正如我在《东南亚与太平洋光缆网》中描述的那样,东盟地区拥有一个充满活力的数字化经济。新加坡是许多新数据中心的所在地。当地的一些互联网巨头早就开始用中国公司提供的云服务,比如Shopee在用腾讯云,Tokopedia在用阿里云(后来有加了谷歌云)。其他大互联网公司也一直在用美国公司提供的云服务,比如Gojek在用谷歌云,Grab在用AWS和Azure。因为当地整体的数字化经济还很年轻,所以大多数互联网公司都是“云原生”的。阿里和腾讯已经在东南亚有各种进展,包括战略投资、收购和产品扩张,所以是个很自然也相对成熟的目标去进一步扩大其云业务。在中国本土现有的和东南亚当地的数据中心都可以很好的为客户提供服务。阿里也已经宣布,计划在2021年在印尼增设第三个数据中心。

拉美:中国科技公司,如滴滴出行,已经在拉丁市场有些成绩。当地的政治和文化阻力也没有在美国那么强烈。据IDC预测,2018-2023年间,拉美的整体云市场的复合年增长率将达到38.3%。腾讯已经在圣保罗拥有一个共享数据中心,整个州的大部分云数据中心都在那里。阿里和腾讯在美国已经搭建了一些数据中心,现在应该有闲置容量来服务拉美客户,因为两家实际上已经被美国市场排除在外。拉美也有自己新兴的数字化经济和巨头,像巴西的Nubank,世界上最大的纯数字化银行(所谓的neobank)之一。(值得一提的是,腾讯也一直在做自己的neobank,既微众银行。)如果在未来的两三年听到阿里、腾讯或两家都宣布在拉美建立首个自己专用的云数据中心,我不会感到惊讶。

中东:按人均国内生产总值来比较,中东与拉美大体相当。到目前为止,以色列已经有七家独角兽,在整个科技领域里非常活跃。Careem是一款集共享乘车、支付和外卖于一体的super app,横跨阿拉伯世界的大部分国家,去年被优步以31亿美元的价格收购了。总部位于印度的外卖配送公司Zomato(蚂蚁金服投了它),在中东也有可观的市场份额。阿里已经盯着中东有段时间了,在迪拜的第一个数据中心早在2016年就上线了。阿里在2018年也以合作伙伴的方式进入土耳其市场。尽管印度市场最近的状况很不好,但这两家巨头位于印度的云计算容量可以很好地服务其中东客户。就地缘政治而言,也许没有哪个地区(概括地说)比中东对美国的意见更大了。敌人的敌人就是朋友(和客户)。

先抢地,再赚钱

我虽然描述了一幅比较乐观的扩张前景,但严峻的现实是,所有这些目的地仍然很穷,在很长一段时间内,都不会产生有规模的收入。正如这张按地区划分的人均GDP图表所示,亚洲、拉美和中东的所有地区都还远远落后于美国和欧盟。

尽管人均GDP通常是用来预测老百姓的消费能力,但也可以用来估算企业开销能力,毕竟企业支出的决策很大一部分是为了满足消费者需求。

目前来说,绝大多数云厂商仍处于“抢地”模式,而不是“收割”模式。每家都在专注于建设基础设施,抢占市场份额。这也就是为什么大多数云厂商,包括微软、谷歌、甲骨文、IBM,当然也有阿里和腾讯,都不披露任何直接归属于自己云业务的营业收入(即利润)。它们的财报一般只宣布一个收入数字甚至只公布增长率,而且还划分到一些莫名其妙,非标准化的类别中:“商业云”(Microsoft)、“谷歌云”(Google)、“云和智能软件”(IBM)和“云服务和License支持”(Oracle)。每家都亏损很多,而且在短期还会继续亏损。

唯一的例外是AWS,它在2019财年的营业收入高达92亿美元,北美地区占该收入的75%以上。

为了“抢地”,提供高达80%的批量折扣以换取长期订单(3年以上),这在行内很常见。一个更极端的例子:据路透社报道,在2017年,腾讯为了抢福建省政府的一个云项目只收了一分钱。搞到工作负担是最重要的,赚钱还要慢慢来。

因此,以阿里和腾讯为首的中国互联网仍有向全球扩张的空间。规模较小的创业公司,无论是阿里系的还是腾讯系的,也都可以借助其云设施进行扩张,获得海外用户和市场份额。但这些扩张一时半会儿都赚不到什么大钱。被挤出最有钱的北美和部份欧洲市场仍是很痛苦的。

当前最大的问题是(重新包装 John Maynard Keynes 的一句话):在地缘政治不合理的时间内,你能坚持多长时间不赚钱?

如果您喜欢所读的内容,请用email订阅加入“互联”。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,与我交流互动!