It has been more than 440 days since Jack Ma’s infamous speech at the 2020 Bund Finance Summit. (We have the full speech translated in English, Chinese, and Japanese. It’s worth a read.)

Since the speech, Alibaba’s stock tumbled by more than 50% over the course of 2021. Many other Chinese tech companies’ stocks fell with a similar velocity and magnitude. The entire technology and investment ecosystem in China got tossed into a whirlwind of regulatory crackdowns and policy changes, much of which is still ongoing.

I’ve been hearing a common sentiment from many investors: “China is uninvestable.” Yet, one (dare I say) pretty good investor begs to differ – Charlie Munger. The investment portfolio of Daily Journal, of which Munger is the chairman, began buying Alibaba shares during H2 of 2021. During Q4 of 2021, its Alibaba position effectively doubled. $BABA is now the Daily Journal’s third-largest holding after Bank of America and Wells Fargo, at a reported price of $118.79.

Anyone who follows the investment career of the Buffett-Munger duo knows they don’t trade stocks for short-term gains; they are long-term, multi-year holders. Thus, whatever the now 98-year-old Munger saw in Alibaba, he has determined that this investment will be worthwhile well beyond his 100th birthday.

What did “Poor Charlie” see in Alibaba, or more likely what did his China-focused protege and confidante, Li Lu, help him see, we may never know. What we can deduce from this investment is that China is far from being “uninvestable”.

I share a similar sentiment, which I articulated in a previous post “Removing China’s ‘Startup Debt’”. 2021 has been a painful but necessary year to clean up 40-plus-years of “startup debt” that the Chinese economy has accumulated since “opening and reform”. Alibaba, being the country’s largest tech company, probably has the most “debt” to clean up.

Whether you are a tech company or a country, “removing startup debt” generally creates a more sustainable foundation to grow for the long term. In the short term, you have to slow down your pace of shipping new features and improving your products, but you can never completely stop.

Despite a tumultuous 2021, Alibaba has not stopped shipping. Most of the analysis on Alibaba is focused on its e-commerce, food delivery, and other consumer-facing products – all of which are low-margin businesses that are slowing down. Alibaba’s long-term moat, growth, and profitability lie in its cloud platform, B2B enterprise businesses, and more “hardcore” technical innovations. That’s where I suspect Munger found Alibaba appealing, otherwise he would have invested in the company many years ago, not 2021 of all years. That’s also where I have seen the most ''ships'' and improvements. Let’s dig into what they are.

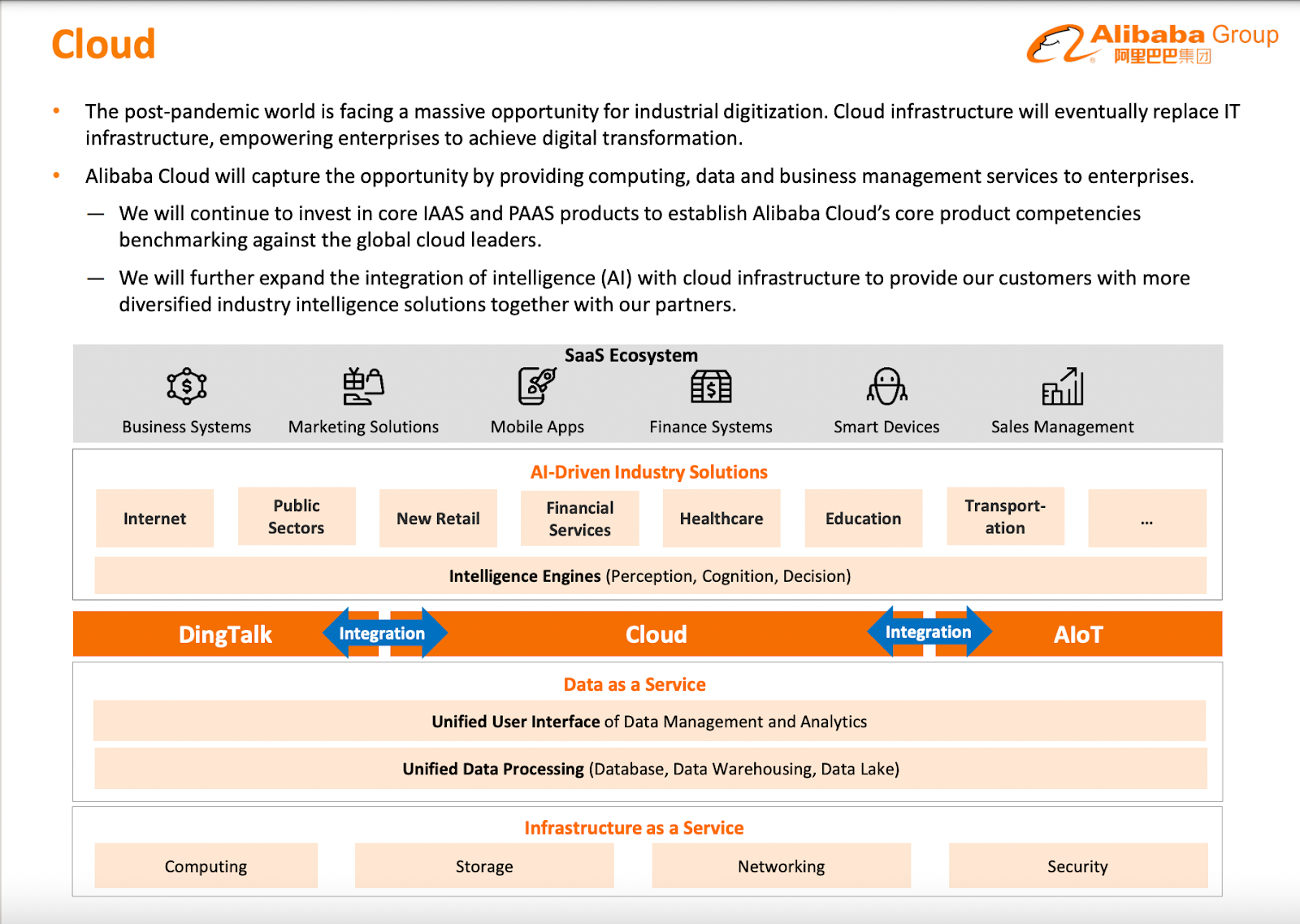

AliCloud: A Profitable Cloud

Alibaba has built its cloud platform, AliCloud, into a profitable business. The division has been profitable (on adjusted-EBITA basis) for the last four quarters.

Building a profitable cloud is a rare feat. It takes an incredible amount of forward planning, discipline, operational efficiency, and hedgehog-like execution. It’s a level few in tech has achieved. Actually not few, just one: AWS.

Amazon’s AWS has been profitable since 2015. But Google’s GCP is still bleeding money ($644 million loss in its most recent quarter). Microsoft does not share Azure’s profitability status, so no one really knows. Thus, AliCloud is the only other profitable cloud of comparable size. (To be clear, there are other smaller profitable clouds like Digital Ocean, but their sizes and market shares pale in comparison to the Big Tech’s clouds.)

Granted, AliCloud’s share of Alibaba’s total business is still small – no more than 10%. The business unit also had many things working against it in 2021. It lost a huge customer (rumored to be ByteDance) possibly due to geopolitical tension. It incorporated DingTalk into the unit in April 2021, which is Alibaba’s workplace SaaS product that is still young and mostly given out for free to drive adoption, thus hurting profitability.

What will be worth watching when Alibaba publishes its next earnings results is if AliCloud was able to maintain profitability for the entirety of a rough 2021. If so, then a consistently profitable AliCloud, especially during lean times, can serve as the long-term foundation for global expansion of Alibaba’s enterprise business and more “hardcore” technical innovation – both of which take a long time to pay off and both of which are already underway.

APAC-Wide B2B Expansion

With the antitrust regulatory landscape in China still in-flux, it's hard to predict how much Big Tech’s like Alibaba are allowed to grow domestically. Thus, overseas expansion beyond China has become a higher priority. Expansion also aligns better with the government’s overall objective to keep growing China's overall influence.

While the US market is effectively off-limit for AliCloud, other emerging markets are wide open spaces. In a previous post, “Where Can the Chinese Internet Go?”, I've identified Southeast Asia, Latin America, and the Middle East as three top regions where AliCloud (and other Chinese cloud platforms) can grow. But cloud expansion is an expensive endeavor, so having an already profitable business that can sustainably make investments is crucial.

AliCloud seems to be doing exactly that, particularly in the APAC region. In the last two years, it has announced new data centers in South Korea, Thailand, the Philippines, and Indonesia. It is building small businesses, startups, and developer ecosystems around AliCloud, targeting the Philippines, Thailand, and South Korea. It won an official partnership to provide cloud computing services for the Malaysian government (along with Telekom Malaysia, Amazon, Google, and Microsoft, so the deal is not exclusive), while announcing the opening of its first-ever non-China-based innovation center to be located in Kuala Lumpur. (These “innovation centers” are often used as “sweeteners” to lock in a government contract in emerging markets.)

AliCloud has not stopped making moves, though mostly under the radar, devoid of major media attention. (Western mainstream media prefer to write non-stop about "where is Jack Ma".)

Targeting APAC as AliCloud’s next B2B growth vector makes sense due to three factors:

1. The region’s proximity to China and its sphere of influence;

2. Alibaba’s existing e-commerce traction in most APAC markets;

3. A macro trend that APAC has the largest and fastest-growing developer community – a prerequisite to cloud business growth.

Factor #3 is a reality that most American tech companies have yet to grasp or invest in heavily, leaving a wide-open space for AliCloud to execute against.

“Hardcore” Tech and Open Source

In addition to market expansion overseas, a lot of “hardcore” technology innovation is happening within AliCloud. I’m calling these innovations “hardcore”, because they are both difficult to achieve technically and mostly related to hardware. Here are a few made public in 2021 that are worth highlighting, spanning all layers of the stack from chips and processor, to operating system and database:

Yitian processor: in its September 2021 quarterly earnings report, Alibaba announced its home-grown Yitian 5nm processor, which it plans to deploy into its own proprietary servers inside AliCloud’s many and growing data centers. Building your own cloud server processor is no joking matter. AliCloud engineers appear up to the task. Yitian is supposedly the fastest Arm processor on the market. While replacing processors, in this case probably Intel’s, with your own won’t yield much business impact overnight, deploying Yitian is key to increasing AliCloud’s profit margin over time, not to mention reducing dependency on an American supplier that may get caught up in future sanctions.

Xuantie: this is Alibaba’s own semiconductor design, which leverages RISC-V, the dominant open-source instruction-set architecture. It is still a young project. What’s telling is Alibaba’s willingness to open source it so early in its development, showing that the company recognizes the value of open source in its long-term strategy and the positioning it could gain among proprietary chip architectures, like Intel’s x86 and Arm.

AnolisOS: this is a home-grown operating system that has apparently been in development for 10 years and serves as the OS for the system that makes Singles Day possible. The newsworthy thing is AliCloud decided to open source AnolisOS last year and made it compatible with CentOS, a popular Linux operating system distribution. Linux still dominates the cloud computing server market – even Azure runs more Linux servers than Windows servers. I don’t see Anolis taking any meaningful market share away from Linux. What this news does show is the AliCloud engineering team’s confidence in their own product and, again, their willingness to embrace open source, create an ecosystem around Anolis, and eventually make AliCloud’s stack more home-grown.

PolarDB-X: this is AliCloud’s main distributed database offering and the combined product of previously two separate database units, called PolarDB and X-DB (thus the PolarDB-X name). Similar to Anolis, this database has been in development for a few years now, but the newsworthy element last year was, again, the announcement to open source PolarDB-X. A highly performant and reliable distributed database is extremely hard to build. Yet, every cloud needs its own flagship distributed database offering to be successful. For AWS, it is Aurora. For Azure, it is Cosmos. For GCP, it is Spanner. For AliCloud, it is PolarDB-X. Interestingly, only PolarDB-X is open-sourced.

One pattern you’ve probably observed at this point is that AliCloud’s “hardcore” technology development is increasingly intertwined with its willingness to open source them, as a way to gain market share versus competitors and pave the way for long-term profitability. As long-time readers of Interconnected know, we’ve written many posts about the intricacies of open source, both as a technology development model and an important element of an overall business strategy. In short, it takes a long time for open source to pay off, but once it starts paying, it pays in spades. Given its current profitability, AliCloud is well-positioned to reap the fruits of its own innovation via open source in the long run.

Does Charlie Munger understand or care about the specifics of any of these “hardcore” tech or the intricacies of how open-sourcing them can contribute to Alibaba’s overall growth? Probably not. But what Alibaba has been doing during a rough 2021 was continuing to invest, expand, ship, and build its moat on the back of a profitable AliCloud – that much Munger definitely understands. And as Alibaba and China as a whole continue to remove their “startup debt”, he, along with Daily Journal shareholders, stands to benefit from it all for years to come.

Disclosure: I do not own any BABA shares. I did during most of 2020 and 2021, but sold them all recently to fund other projects. Maybe Munger bought them. That’s why I’m not as good of an investor as he is; very few people are.

芒格的新宠:阿里巴巴

自从马云在2020年外滩金融峰会上发表的那次重磅演讲以来,已经过去440多天了(我们发表了英文、中文和日文的演讲全文翻译,非常值得一读)。

自演讲以来,阿里的股价在2021年期间暴跌了50%以上,许多其他国内科技公司的股价也以类似的速度和幅度下跌。中国的整个科技和投资生态都被扔进了监管打击和政策变化的旋风中,很多仍在进行当中。

我从许多投资人那里听到一个共同的观点就是:"中国不可投。" 然而,一位(我敢说)成绩相当优秀的投资人却不敢苟同,他就是查理·芒格。芒格担任主席的Daily Journal 在2021年下半年开始狂买阿里股票。在2021年第四季度,其阿里的持股总数翻了倍。$BABA现在是 Daily Journal 继美国银行和富国银行之后的第三大持股,报告价格为118.79美元。

任何关注巴菲特和芒格二人投资生涯的人都知道,他们从不以短期炒股收益,而有着长期的、多年的投资风格。因此,无论现年98岁的芒格从阿里身上看到了什么,他已经确定这项投资的价值将远远超过他个人的一百岁生日。

作为旁观者也许永远不会知道 "穷查理" 在阿里身上看到了什么,或者更可能的是李录帮他看到了什么。但我们可以从这笔投资中推断出的是,中国远非 "不可投"。

我也有类似的观点,曾在之前的一篇文章《清除中国的"创业债"》中阐述了这一点。2021年是痛苦但必要的一年,以清理中国经济自 "改革开放" 以来积累的40多年的 "创业债"。阿里作为中国最大的科技公司,需要清理的"债" 也可能最多。

无论你是一家科技公司还是一个国家,"清除创业债" 后一般都能为长期发展创造一个更可持续的基础。在短期内,你必须放慢创造新功能和改进产品的步伐,但永远不能完全停止。

尽管2021年很动荡,阿里并没有停止创新改进。对阿里的分析大多集中在其电商、外卖配送和其他to C消费者的产品上 —— 这些都是薄利的业务,增长正在放缓。阿里的长期护城河、增长点和盈利能力在于其云平台、B2B企业业务和更多的 "硬核" 技术革新。这就是我怀疑芒格发现阿里吸引人的地方,否则他多年前就会投它了,而不是等到2021年。这也是我看到最多创新和改进的业务方面,让我们来看看创新改进的都是什么。

阿里云: 一个盈利的云

阿里已经将其云平台 —— 阿里云 —— 打造成为了一个盈利的业务,该部门在过去四个季度里一直在盈利(按调整后的EBITA计算)。

做出一个盈利的云是件罕见的壮举,需要大量的长远规划、纪律、运营效率和“刺猬般”的执行能力。这是一个科技界很少有公司达到的水平。不,不是少数,其实只有一个平台达到了这一水准:AWS。

亚马逊的AWS自2015年以来开始盈利;但谷歌的GCP仍在流血(最近一个季度亏损6.44亿美元);微软不公布Azure的盈利状况,所以没有人真正知道情况。因此,阿里云是唯一一个规模相当的“盈利云”(当然,还有其他规模较小的盈利的云厂商,如Digital Ocean,但它们的规模和市场份额与科技巨头的云规模相比微不足道)。

诚然,阿里云在阿里总业务中的份额仍然很小 —— 还没超过10%;该业务部门在2021年也不走运,失去了个大客户(据传是字节),可能是因为地缘政治紧张的关系。阿里云在2021年4月还将钉钉纳入该部门,一个还很年轻的产品,大部分是免费送客户来推动使用,因此是亏损的。

当阿里公布其下一份财报时,值得关注的是阿里云是否能够在艰难的2021年中一整年保持盈利。如果是的话,那能够持续盈利的阿里云,可以作为阿里企业业务全球扩张和更多 "硬核" 技术创新的坚实后盾和长期基础 —— 这两者的回报都需要很长时间,而它们也都已经在进行中。

亚太地区的B2B扩张

由于中国的反垄断监管状况仍不明朗,很难预测像阿里这种大厂以后在国内的发展空间还有多少。因此,出海扩张应更加优先,出海也与政府期望国家整体影响力扩大的大目标更加一致。

虽然阿里云杀入美国市场基本没戏,但在其他新兴市场扩张的空间还是很大的。在之前的一篇文章《中国互联网还能去哪里?》中,我提到东南亚、拉美和中东是阿里云(和其他中国云平台)三大可以大显身手的地域。但云平台扩张很昂贵,因此拥有一个已经盈利的业务、能够持续进行投资是至关重要的。

阿里云似乎已经在这样做了,特别是在亚太区域。近两年,它已经宣布在韩国、泰国、菲律宾和印度尼西亚建立新的数据中心,也正在围绕阿里云建立小型企业、创业公司和开发者的各种生态,主要目标是菲律宾、泰国和韩国。它还赢得了为马来西亚政府提供云计算服务的官方合作(同时还有马来西亚电信、亚马逊、谷歌和微软,所以并不是独家),同时宣布在吉隆坡开设其有史以来第一个在中国境外的创新中心(这些“创新中心”通常被用作 "甜头",以锁定与新兴市场的政府的合同)。

阿里云一直没停,尽管大多都很低调,没有什么媒体关注(西方主流媒体更喜欢不停地写“马云在哪儿”)。

将亚太地区作为阿里云的下一个B2B增长点很合理,其中有三个因素:

1. 该地区靠近中国的影响范围

2. 阿里在大多数亚太市场已经有不小的电商业务

3. 亚太地区拥有最大和增长最快的开发者社区这一宏观趋势 —— 这是云计算业务增长的先决条件。

这第3个因素是大多数美国科技公司尚未掌握或大力投入的,为阿里云留下了一个广阔的发展空间去操作。

"硬核"技术与开源

除了海外市场的拓展,阿里云内部也在进行大量的 "硬核" 技术革新。我称这些创新为 "硬核",是因为它们既在技术落实上难度很高,又大多与硬件有关。以下是2021年公布的几个值得关注的创新,横跨从芯片和处理器,到操作系统和数据库的整个技术栈。

倚天处理器:在2021年9月的季度财报中,阿里公布了其自制的倚天5nm处理器,它计划将其部署在阿里云众多且不断增长的数据中心内的专有服务器中。打造自己的云服务器处理器不是开玩笑的事,阿里云的工程师们似乎完全可以胜任。据称,倚天是市场上最快的Arm处理器。虽然用自制的处理器取代买的处理器(可能是英特尔的)在短期不会给业务带来多大收获,但部署倚天是长期增加阿里云利润率的关键,更不用说还可以减少对可能陷入未来制裁的美国供应商的依赖性。

玄铁:它是阿里自制的半导体设计,利用RISC-V这一主流的开源指令集架构。玄铁仍然是一个很年轻的项目。值得注意的是,阿里在此项目的开发初期就愿意将其开源,表明公司认识到开源在其长期战略中的价值,以及它在英特尔的x86和Arm等专有芯片架构中可以争取到的定位。

AnolisOS:这是一套自产的操作系统,显然已经开发了10年,作为运作“双十一”的系统的OS。有新闻价值的点是阿里云去年决定将AnolisOS开源,并使其与Linux操作系统发行版CentOS兼容。Linux仍是云计算服务器OS份额的最大一块 —— 就连在Azure上运行的Linux都比Windows要多。我不认为Anolis会从Linux手中夺走任何有意义的市场份额,但AnolisOS开源这一消息显示的是阿里云工程团队对自己产品的信心,以及他们的意愿去拥抱开源,围绕Anolis打造生态,并最终使阿里云的技术堆栈能使用更多自制的产品。

PolarDB-X:这是阿里云的主打分布式数据库产品,是以前两个独立的数据库团队的合并产品,当时分别称为PolarDB和X-DB(因此称为PolarDB-X)。与Anolis类似,这个数据库已经开发了好几年,同时有新闻价值的点是去年也宣布将PolarDB-X开源。一个高性能、可靠的分布式数据库是很难做好的。然而,每一个云平台都需要自己的旗舰分布式数据库产品才能成功。对于AWS来说,那是Aurora。对于Azure来说,那是Cosmos。对于GCP来说,那是Spanner。对于阿里云来说,那就是PolarDB-X。而只有PolarDB-X是开源的。

您可能已经察觉到了一个规律,那就是阿里云的 "硬核" 技术开发与它拥抱开源的意愿日益交织在一起,以此从竞争对手那里抢到市场份额,并为长期盈利铺平道路。《互联》的长期读者都知道,我们写了很多分析开源方方面面的文章,它既是一种技术开发模式,也是一套商业战略的重要元素。简而言之,开源需要很长的时间才能得到回报,但一旦回报开始,成绩是显赫的。鉴于其目前的盈利能力,阿里云可以通过对开源的投资而从自己的创新中长期受益。

查理·芒格了解或关心这些 "硬核" 技术的具体细节,或开源会如何促进阿里的整体增长的复杂关系吗?应该不的。但是阿里在艰难的2021年中仍在继续投资、扩张、出新产品,并在盈利的阿里云内继续挖自己的护城河,这一点芒格是很清楚的。随着阿里和整个中国继续清除其 "创业债",他和Daily Journal的股东们将是未来多年的受益者。

披露:我不持有任何阿里的股票。在2020和2021年的大部分时间里,我确实持有一些,但最近都卖掉了,以资助其他项目。也许芒格把我持的股买了。这也许就是为什么我没有他的投资水平高;很少人有。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周一篇新文章送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!