ChatGPT has set off an AI arms race – and this arms race is global. Even though the seemingly ubiquitous chatbot is blocked in China, Baidu is set to release its own ChatGPT-like bot in March. Most of the reporting so far, in both English and Chinese business media, frame the announcement as a tactic to boost its core search business. This angle shows a glaring lack of understanding of the business value of a ChatGPT-like bot, and the years of technology progression that must be accumulated to make that business value real.

It’s true that Baidu is glomming on to the ChatGPT-induced frenzy to boost its relevance, just like Google with its $300 million investment into Anthropic (an OpenAI competitor) and every startup with cash left to pivot in Silicon Valley. However, Baidu has been an active participant in this so-called “AI arms race” for at least a decade. Its ChatGPT-like bot, named Ernie (or 文心 in Chinese) is an application derived from PaddlePaddle – a homegrown deep learning framework that began its development as early as 2013 and open sourced on GitHub in 2016. (PaddlePaddle is analogous to Google’s Tensorflow and Facebook’s PyTorch.)

So Ernie didn’t come from nowhere, nor is it a “copycat” knock-off of ChatGPT, like some lazy reporting suggested. If Ernie does catapult this otherwise anemic Chinese tech company to a new level of growth, Baidu more than deserves it. And this transformation would not come from Search, but two other smaller but more AI-natural product lines – Cloud (launched in 2013) and Apollo (self-driving project launched in 2016).

Search is “Dead”

Before we discuss the rationale behind why Ernie is geared to boost Baidu’s Cloud unit and Apollo project, let’s first understand why it is not meant to boost Search.

Search, as a user behavior, is effectively dead. Not “dead” as in no one will use a search engine. Of course not. But “dead” as in this behavior will no longer grow meaningfully, thus nor will Search as a product.

This massive user behavior change was ushered in by the other “B” in China Tech – ByteDance. The key insight that ByteDance productionized, first with Jinri Toutiao in 2012 (its news app), then with Douyin and TikTok in 2016, is that the act of “searching” is unnecessary when a recommendation engine can know, within seconds, what you want simply by showing you a few things first, collect some data, then quickly adjust to serve up what you are looking for. You no longer have to form a query about exactly what you are looking for anymore – the prerequisite for Search.

ByteDance, having first productionized and commercialized this “post-Search” user experience, has been eating Baidu’s lunch for years. Their relative market caps reflect this difference. As of today, Baidu’s market cap is roughly $50 billion USD, which includes the post-ChatGPT-bot announcement bump. ByteDance’s most recently reported market cap sits at $240 billion USD, which prices in the ever-present specter of TikTok getting banned in the US. Granted, ByteDance is a private company and its stocks are not trading publicly, so this comparison is not exactly apples-to-apples. Nevertheless, the post-Search company is worth at least 4-5x more than the Search company, because younger generations of Internet users simply don’t “search” anymore.

This does not mean incorporating Ernie, or other elements of PaddlePaddle, won’t improve Baidu’s search experience. I’m sure when Ernie debuts in March (or whenever Baidu decides to do it), it will spark a rush of usage, novelty, and attention to boost search revenue temporarily. Deep learning systems, as Google has shown over the years, also have shown to be able to improve search results (and digital ads targeting). I would be shocked if parts of PaddlePaddle are not in Baidu’s search engine already.

Sadly, these improvements in search won’t move the needle much for Baidu’s bottom line when search – a stable and shrinking market – is effectively “dead”.

Baidu AI Cloud

A more natural and higher-potential business for Ernie to make a real dent is Baidu’s cloud unit. Dubbed the “Baidu AI Cloud”, it has always sought to differentiate itself with AI, similar to Alphabet’s Google Cloud Platform’s market positioning.

The rationale is quite straightforward. We (Baidu) build an AI framework (PaddlePaddle) and applications (image generation, natural language processing, conversational bot like Ernie, etc.), and we make these technologies available as APIs on our cloud platform. Whether customers use our applications directly, or use our APIs to build their own AI applications, we charge them for consuming our cloud computing resources and make money either way.

This is the same logic that underpins Microsoft Azure’s symbiotic relationship with OpenAI – whether you use ChatGPT directly or use OpenAI APIs to make your own chatbot, Azure makes money either way. That’s why last month, riding on the buzz of ChatGPT, Microsoft announced that all of OpenAI’s latest and greatest APIs and frameworks – GPT-3.5, Codex, DALLE 2 – will be generally available for Azure customers. Baidu is fully aware of this playbook and has been executing along the same direction – various AI models labeled Ernie (or 文心) have been available as APIs on Baidu AI Cloud for quite some time (see screenshot below).

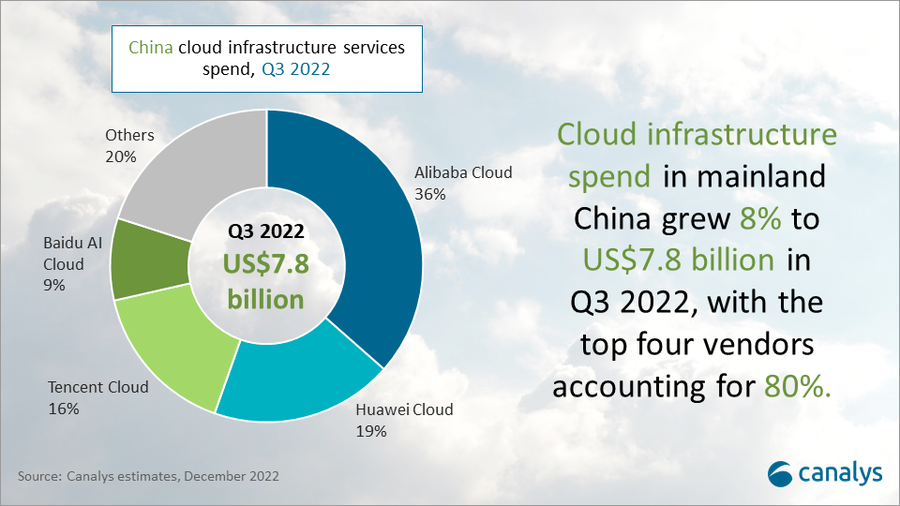

However, this playbook is easier said than done for Baidu. According to Canalys’s latest estimates of China’s cloud market, as of Q3 2022, Baidu’s market share is a mere 9%, trailing Alibaba, Huawei, and Tencent.

If you read last year’s cloud industry whitepaper published by the China Academy of Information and Communications Technology (CAICT) – a think tank affiliated with the Ministry of Industry and Information Technology – you will only see Baidu marginally mentioned in the PaaS category. (For interested readers, I wrote a deep dive on this whitepaper a few months ago.)

In short, Baidu AI Cloud is a laggard in China, which is already quite competitive with incumbents (AliCloud), state-owned telecoms (China Telecom’s CTyun), and new entrants (ByteDance Cloud) all vying for a piece of the same pie. This unfortunate position, of course, makes the release of Ernie all the more compelling.

If Ernie the chatbot takes off like ChatGPT, whether a company wants to use Ernie directly or build its own Ernie, the eventual big winner should be Baidu AI Cloud.

Self-Driving Apollo Robotaxis: Ernie-Style

The other high-potential unit that lends itself well to Ernie is Apollo, but the revenue relationship is more subtle and multi-dimensional.

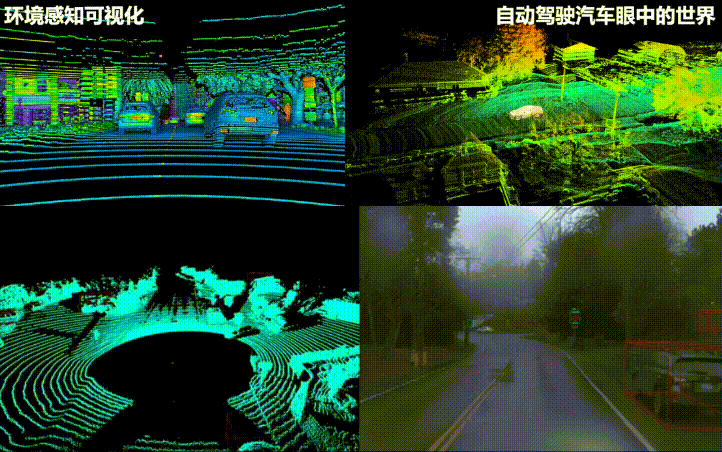

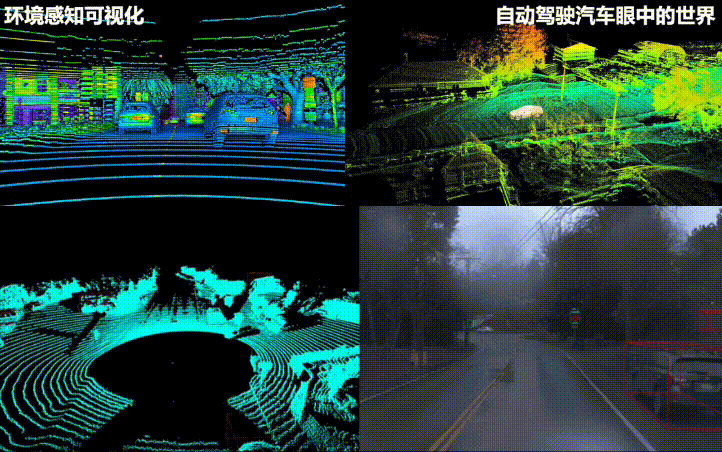

For background, Apollo is Baidu’s self-driving software and hardware stack. It was launched and open sourced back in 2017. The ambition around Apollo is to become the operating system for other self-driving carmakers, as well as the technology powering Baidu’s own brand of robotaxis. Not surprisingly, there is already some overlap between the Apollo project and the PaddlePaddle project – the two teams have collaborated to build a 3D computer vision and detection system to enhance self-driving. Thus, integrating Ernie into Apollo should not be difficult.

I have discussed Apollo in previous posts as a leading open source project out of China that has global potential. Because of its permissive licensing scheme (Apache 2.0), Apollo has the prospect of becoming the “Android of self-driving” for many carmakers, with Tesla being the Apple/iOS corollary.

With Ernie, Apollo could become that much more attractive. Ironically, an Ernie-enabled Apollo is the one scenario where a search-oriented, conversation-based user behavior both makes sense and could continue to make sense for years to come. No matter how reliable self-driving becomes, at least for the foreseeable future, passengers will likely still prefer to keep their eyes on the road and be ready for emergencies or malfunctions, which lends itself better to asking questions (or voice search) to a chatbot, not staring and clicking on a screen.

Baidu’s Apollo robotaxis network has already started charging passengers for rides during the 2021 Winter Olympics at its Shougang Park test location in Beijing to prove out the business model. It has ambitions to roll out this service in 65 cities by 2025.

If Ernie makes Apollo more “sticky” with passengers, these robotaxis will directly generate more revenue from these passengers. If Ernie makes Apollo more attractive as an operating system to other carmakers, there will be more self-driving cars running on Apollo, which will indirectly funnel a good chunk of computation workloads to Baidu AI Cloud.

These are all big “if’s” right now, with Ernie as a centerpiece of this multi-dimensional maneuver to revive Baidu’s relevance. With a decade worth of AI technology accumulation in PaddlePaddle, another decade-old platform in its Cloud unit, and a growing ecosystem around Apollo, Baidu has all the supporting pieces and is as well-positioned as any company to capitalize on the “ChatGPT frenzy”.

Baidu earned this opportunity, but the outcome is far from certain.

ChatGPT能让百度再次崛起吗?

ChatGPT已经掀起了一场全球性的AI大战。尽管看似无处不在的ChatGPT在国内还不能(合法)使用,但百度已确认将在3月发布自研的chatbot。到目前为止,英文媒体和中文商业媒体的大部分报道都将这一消息归结为激进其核心搜索业务的策略。这个角度显示出对类似于ChatGPT的AI产品的商业价值明显缺乏了解,以及要实现该商业价值的背后所必须积累的多年技术沉淀。

诚然,百度的计划是在赤裸裸的抓住被ChatGPT掀起的热点,来提高对自己的关注度。这种举动与谷歌大笔投资Anthropic(OpenAI的竞争对手)三个亿没什么区别。所有在硅谷还有现金可以pivot的创业公司也都在努力蹭AI的热点。然而,在这场所谓的 "AI军备竞赛" (AI arms race)中,百度已经积极参与了至少十年。其类似ChatGPT的chatbot,文心(文心),是一个源自飞桨的app。飞桨则是百度内部自研的一款深度学习框架,早在2013年就开始研发,2016年在GitHub上开源。(飞桨好比谷歌的Tensorflow和Facebook的PyTorch。)

因此,文心并不是凭空出现的,也不是像一些懒惰的报道所说的那样,是ChatGPT的 "山寨版”。如果文心真的能帮这家近几年发展平淡的科技巨头重返辉煌,成果也是应得的,因为百度确实在AI上付出了很多血汗和金钱。而这种转变不会来自搜索业务,而是来自另外两个规模较小但更符合人工智能业务价值的产品线 – 云(2013年推出)和阿波罗(2016年推出的自动驾驶项目)。

搜索已经“死”了

在讨论文心会怎么促进百度云和Apollo的商业逻辑之前,让我们先聊聊为什么它会促进搜索业务。

搜索,作为一种用户行为,实际上已经“死”去了。不是说没有人会用搜索引擎,当然不是。但这种"死"是指此行为将不会大幅度地增长,因此搜索作为一款产品也不会增长多少。

这种用户行为的“巨变”是由BAT的另一个 "B" – 字节跳动 – 激起的。字节在2012年推出的今日头条,之后在2016年推出的抖音和TikTok,产品其中的关键“秘方”是,当一个推荐引擎可以在几秒钟内知道你想要什么,只需先向你展示一些内容,收集一些数据,然后快速调整推荐的内容,就可以锁定用户真正在找什么,"搜索" 也就并是不必要了。用户不再需要对自己正在寻找的东西要想出一条查询的句子或问题 – 这是搜索的先决条件。

字节率先把 "搜索后" 的时代成功的产品化和商业化,多年来一直在“肯”百度的市场份额。两家公司的相对市值也反映了这种差异。截至目前,百度的市值约为500亿美元,其中还包括蹭ChatGPT热点后的股价增长。字节最近被报道的市值为2,400亿美元,其中还包括TikTok在美国被禁的阴影。当然,字节还没有上市,其股票没有公开交易,所以这种比较并不完全准确和公平。然而,一家“搜索后”公司的价值至少是“搜索”公司的4-5倍,很说明问题。年轻一代的互联网用户根本不 "搜索" 了。

这并不意味着文心,以及飞桨的其他元素,不会改善百度的搜索体验。我相信,当文心在3月首次亮相时,它将引起很多应用尝试、新奇的用法和新的热点,以暂时提高搜索业务的收入。深度学习系统,正如谷歌多年来已经证明的那样,确实能够提高搜索结果的质量(以及打广告的定位准确度)。飞桨的一些模型也应该已经融入到百度搜索引擎中了。

可悲的是,当搜索 – 一个稳定且开始萎缩的市场 – 实际上已经 "死" 了时,搜索的提高和进步不会对百度的底线有多大影响。

百度智能云

对文心来说,一个更自然、更有潜力的业务是百度的云计算平台。被称为 "百度智能云",它一直在寻求以AI来在市场中区分自己,类似于Alphabet的谷歌云平台(GCP)的市场定位。

其商业逻辑很清晰。我们(百度)研究出了一款人工智能框架(飞桨)和一套应用程序(图像生成、自然语言处理、像文心这样的对话机器人,等等),我们在“智能云”上将这些技术作为API提供给客户。无论客户是直接使用我们的AI应用程序,还是使用我们的API来构建他们自己的AI应用程序,都需要消耗我们的云计算资源,所以最终百度智能云总是可以赚钱。

这同样也是微软Azure与OpenAI共生的逻辑 – 无论你是直接使用ChatGPT还是使用OpenAI的API来做自己的聊天机器人,Azure都能赚钱。这也就是为什么上个月,乘着ChatGPT的热潮,微软宣布所有OpenAI最新,最好的API和框架 – GPT-3.5、Codex、DALLE 2 – 都会在Azure上提供给客户使用。百度完全了解这一玩法,并也一直沿着同样的方向布局。各种标记为文心(或ERNIE)的AI模型已经被包装成API在百度智能云上有段时间了(见以下截图)。

然而,对百度来说,这套玩法说起来容易,做起来难。根据Canalys对中国云计算市场的最新分析,截至2022年第三季度,百度的市场份额仅9%,落后于阿里、华为和腾讯。

如果您读了中国信息通信研究院(一家隶属于工业和信息化部的智囊机构)去年发布的云计算产业白皮书,会发现百度仅在PaaS类别中被小小提到。(对于感兴趣的读者,我在几个月前写了一篇关于此白皮书的深度分析文章。)

简而言之,百度智能云在国内云市场中还是很落后的,无论是领头羊(阿里云)、国企(中天云)还是新玩家(字节的火山引擎)都在激烈争夺同一块馅饼。当然,百度智能云的落后也使得文心的发布更加引人注目。

如果文心能像ChatGPT一样腾飞,无论是公司想直接用文心还是造自己的文心,最终的大赢家都应该是百度智能云。

文心风格的阿波罗自动驾驶

另一个很适合文心的高潜力产品线是阿波罗,但收入关系更加微妙和多维。

先介绍一下阿波罗项目的背景。阿波罗是百度自研的自动驾驶软件和硬件栈。它早在2017年就开源了。阿波罗的野心是成为其他无人驾驶汽车制造商的操作系统,同时作为百度自己品牌的无人驾驶出租车产品(robotaxis)的基础技术。毫不奇怪,阿波罗项目和飞桨项目之间已经有一些重叠 – 这两个团队已经合作搭建了一款3D计算机视觉和检测系统,以加强自动驾驶能力。因此,将文心整合到阿波罗中应该不难。

我在之前的文章中讨论过阿波罗,作为中国的一个领先的开源项目,还是很具有全球发展潜力的。由于它决定使用一项很开放的许可制度(Apache 2.0),阿波罗有可能成为许多汽车制造商的 "自动驾驶的安卓"(而特斯拉则更像苹果的iOS)。

有了文心,阿波罗可能会变得更有吸引力,更有 "粘性"。有意思的是,用文心的阿波罗以对话做搜索是少有适合“搜索”的用户行为情况,并且这种用户行为还会持续很多年。无论自动驾驶变得多么成熟可靠,至少在可预见的未来,乘客可能仍然觉得眼睛盯在路上更放心些,准备好应对紧急情况或故障,更习惯向机器人提问(所谓语音搜索),而不是盯着屏幕点击。

百度的阿波罗robotaxis网络已经开始在2021年冬奥会期间在北京首钢公园的测试点开始向乘客收费,以证明其商业模式。它有野心在2025年前在65个城市推出这项服务。

如果文心能使阿波罗在乘客体验中更有 "粘性",这些robotaxis能直接从乘客的口袋中产生更多的收入。如果文心让阿波罗作为一款操作系统对其他汽车制造商更有吸引力,将会有更多的无人车在阿波罗上运行,这将间接地将很大一部分计算工作负载输送到百度智能云上。

当前而言,这些都是 "如果",而文心则是这些“如果”中的核心。能否重振百度,还是个未知数。凭借飞桨十年的AI技术积累,其云计算部门这另一组有十年左右成熟度的平台,以及围绕阿波罗的生态,百度拥有所有的棋子来赢由ChatGPT激起的这盘全球AI棋。

百度付出了心血,也配的上这个千载难逢的机遇,但结果还远未确定。