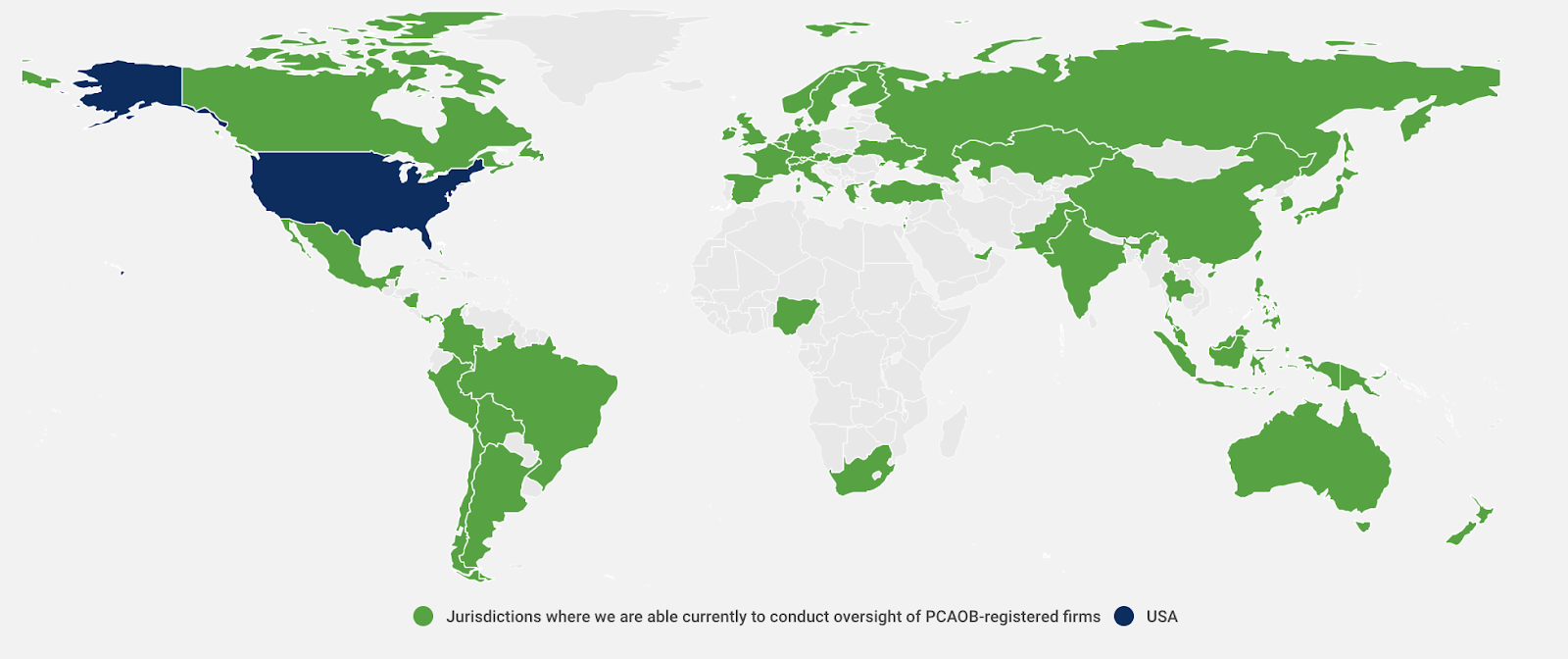

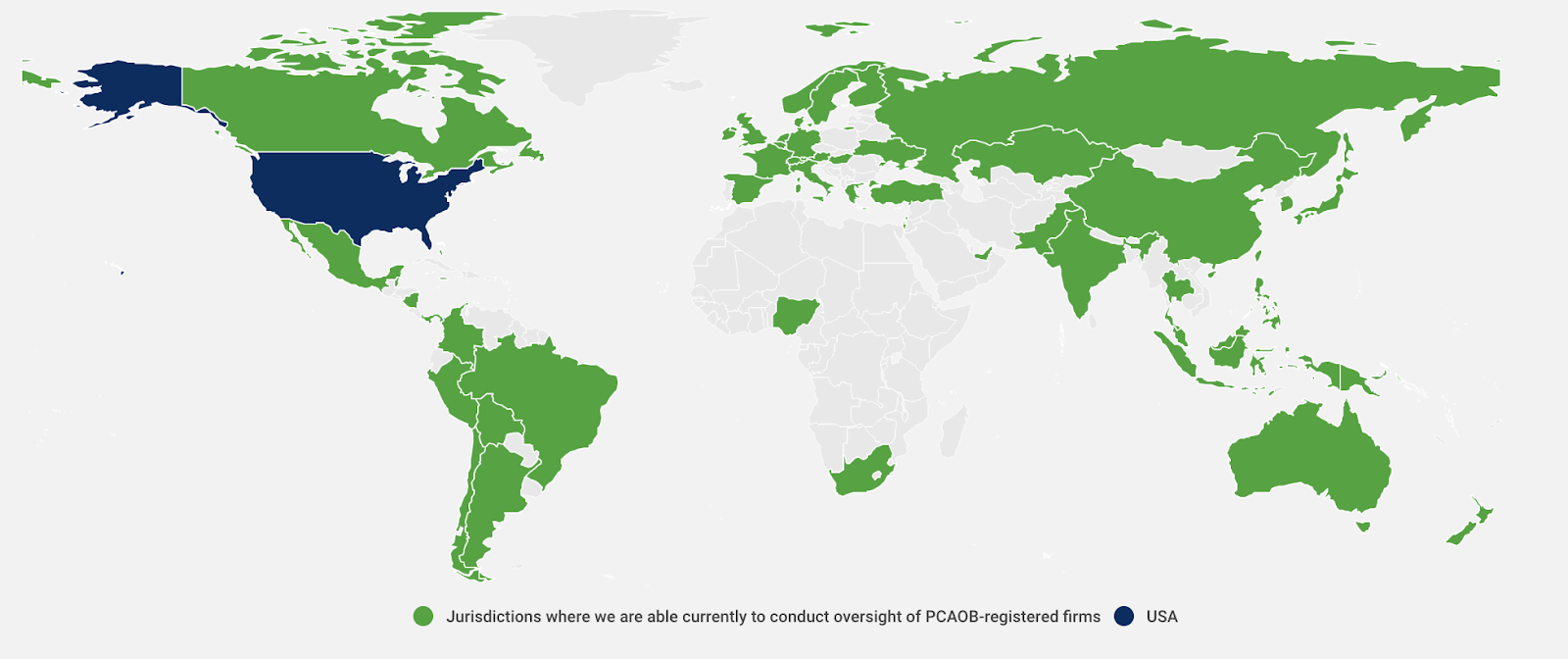

In the last three years, the threat of forced delisting for Chinese companies publicly traded in the US was constant. Billions of market cap evaporated while the investment world waited to see if the Public Company Accounting Oversight Board (or PCAOB or the auditor of auditors) can gain the access it needs and defuse this uncertainty.

A week before Christmas, this uncertainty appears to be defused for good. The PCAOB announced, quite dramatically, that it has secured the access it needed to investigate all Chinese firms’ books without Chinese government interference for the first time in history. Companies, like Pinduoduo and Full Truck Alliance, felt safe enough to cancel their backup listing plan on the Hong Kong Stock Exchange (HKEX). Mainland China and Hong Kong have finally turned “green” on the PCAOB’s oversight map.

I have devoted much digital ink writing about this “delisting saga” in the past. Now that this saga is over, for now, I want to share some reflections and learnings from both following this topic closely as a writer and investing during it.

Governments Can Be Both Adversarial and Reasonable

The delisting issue has often been wrapped up as yet-another-example of the growing adversarial nature between the US and China, in the same vein as the trade wars, sanctions, technological competitions, and other facets of an ever worsening relationship. The way this delisting saga ended shows that these two governments can, in fact, “compartmentalize” and cooperate to resolve some issues reasonably.

It is not entirely a surprise that the most reasonably dealt with issue impacts mostly the capital market and the professional investor class – the global, moneyed elites who have the most access to both governments and the most to lose when relationships sour. The manner in which the PCAOB carried out the Holding Foreign Companies Accountable Act (HFCAA), the law that gave the PCAOB the legislative chutzpah to aggressive vet auditors that audit Chinese companies, was also reasonable and professional.

When the HFCAA first passed, it was seen as just another way for an increasingly anti-China Congress to get rid of more Chinese presence in the US. But the bureaucrats of the PCAOB (and I’m using the term “bureaucrats” positively here to describe government officials devoid of political influence) dutifully carried out their work. More than 30 professional staffers went to Hong Kong for nine weeks, and verified its access to two auditors (namely, KPMG Huazhen LLP in Mainland China and PWC in Hong Kong) without Chinese government interference. As the bureaucrats of two accounting firms cooperated with the bureaucrats of PCAOB, while the bureaucrats of the China Securities Regulatory Commission stood by without interfering, a hot button issue between the US and China was actually resolved!

This made me think of something Charlie Munger said in early 2022, when asked about the risk he took on by owning Alibaba ADRs during the Daily Journal shareholders meeting:

“Assuming there is a reasonable honor among civilized nations, that risk doesn't seem all that big to me.”

Looks like Munger’s assumption proved true. The US and Chinese governments, while increasingly competitive with each other, by and large hold civilized attitudes on most issues (though the difference in human rights record notwithstanding). As long as the baseline attitude is civilized, no matter how adversarial the bilateral dynamic becomes, at least some issues can be resolved reasonably.

The “Reasonableness” Margin of Safety

If you were an investor who had enough confidence, intuition, and belief in the level of reasonableness that the US and China would apply to handling this delisting issue, you would have had a large margin of safety to buy Chinese firms’ shares, added more as the delisting fear escalated, and made a handsome profit in the end.

In hindsight, not even the best of the best investors were able to pull this off perfectly.

Munger began buying Alibaba shares in Q1 2021, under his Daily Journal portfolio, and added more during that calendar year to as many as 602,060 shares. But as the delisting fear persisted during 2022, he reduced his $BABA holding to now 300,000 shares. Some people suspected that he transferred some of the ADR shares to the HKEX and maintained the size of his Alibaba holding. I have no way to verify if he did this or not. But it’s clear he did not add to his holding while Alibaba, along with most Chinese firms, was on a steady decline for much of 2022.

Seth Klarman of Baupost Group, a famed value investor often mentioned in the same breath as Munger and Warren Buffett, did a bit better. He made an investment in New Oriental Education (ticker: EDU) in Q2 2022, to the tune of 8 million shares, after the stock fell off a tall cliff in 2021 and early 2022. Instead of adding to his holding as $EDU’s price continued to stay depressed, Klarman took some profit in Q3 2022 instead, as the share price showed modest recovery.

I, a much much much less capable investor than both Klarman and Munger, bought and sold shares of various Chinese companies throughout 2021 and 2022, but was not confident enough to hold onto any of them for long. Throughout the “delisting saga”, I personally placed the probability of a mass, wholesale delisting at no more than 10%, because cutting off the flow of global capital just to avoid a perfectly reasonable auditing requirement seems utterly unreasonable. However, I did not have enough chutzpah of my own to increase and hold on to my holdings. Of course, the delisting threat was just one of several reasons why Chinese stocks have been falling during the last three-plus years – Zero Covid, antitrust enforcement, policy changes on tech, education, property, and other major sectors, to name a few.

As Munger once said: “If investing wasn't hard, everyone would be rich.”

Hard, indeed.

Capital Markets Are More Than Just Capital

Many Chinese firms hedged against the delisting risk with costly Plan B’s to duel list on the HKEX.

Big Tech’s like Alibaba and Baidu did secondary listings. Newcomers like XPeng and Li Auto did dual-primary listings on both the NYSE and the HKEX. Pinduoduo and Full Truck Alliance had plans to do the same, but waited just long enough to receive the good news from the PCAOB and scrapped their plans.

These hedges gave the false impression that the HKEX, and the Stock Connect program that gives Mainland Chinese investors a conduit to the HKEX, is a good enough alternative to Wall Street that Chinese firms can stay within the comfort of their own border and still do fine.

That could not be further from reality.

Of course, if you are a Chinese firm whose market and ambition rest solely within China (or a straight up state-owned enterprise), then listing on the HKEX or Shanghai or Shenzhen is perfectly fine. Being publicly traded in New York is more trouble than it's worth in this day and age. And logistically, sophisticated foreign institutional investors can figure out ways to invest in these purely domestic companies if they really want to. There is no capital access issue, just higher transaction cost.

However, there is a large crop of Chinese firms with global ambitions – either because the Chinese domestic market is not big enough for them to scale, or their products indeed have international appeal, or they simply sold their early investors on the dream with a high valuation and must deliver sooner or later. Examples would be firms in electric vehicles, enterprise software, cloud infrastructure, and maybe a subset of the semiconductor industry.

For these types of companies, listing on the NYSE or NASDAQ is still the most preferred path by far. This is partially because the SEC’s disclosure-oriented regime is more friendly to high-growth companies than Hong Kong’s compliance-oriented regulatory regime. But more importantly, the reputational halo effect of being listed on either the NYSE or NASDAQ is not something the HKEX can replicate. A newly-listed company in New York, at least within the sectors I spelled out above, simply has a better chance of becoming a global brand while attracting enough capital to deliver on its ambition. An HKEX listing currently cannot and may be increasingly unlikely to deliver that reputation bump, as Hong Kong continues to evolve inward.

So from the Chinese government’s perspective, it is worth cooperating with the PCAOB if only to not thwart the global prospect of its most promising and ambitious companies, whose success will eventually accrue back to China, either financially or reputationally.

When there are enough incentives to be reasonable, reasonableness tends to prevail, even between the increasingly adversarial governments of two superpowers. I may sound too optimistic here (as it is my nature), but as the end of the “delisting saga” has shown, there could be other issues of conflict between the US and China that can still be resolved reasonably.

And it pays (literally) to know what the next of those issues may be.

关于退市风波的反思

在过去的三年里,在美上市的中国公司时时面临着被强制退市的危机。在投资界等待上市公司会计监督委员会(简称PCAOB,也就是监管审计师的机构)获得所需的财务资料审查权限并化解这一不确定性的同时,数十亿美元的市值慢慢蒸发。

圣诞节前一周,这一不确定性似乎被永久化解了。PCAOB宣布,已经获得了所需的审查权限,历史上首次在不受中国政府干预地状态下审查了中国公司的账目。像拼多多和满帮这样的公司觉得安全到可以取消在香港联合交易所(HKEX)备份上市的Plan B。中国大陆和香港终于在PCAOB的监管地图上变成了“绿色”。

我过去写过很多篇关于这场“退市风波”的文章。既然这个风波暂时告一段落,我想分享一些在追踪这个话题的过程中作为一名作者,又是一名投资人的感悟和经验。

政府既可以对抗,也可以保持理智

退市问题通常被视为中美两国日益对抗性关系的又一个例子,与贸易战、制裁、科技竞争和其他恶化关系的各种方面一样。这次退市风波的结束和它结束的方式表明,这两个政府还是可以“区隔”不同问题,并理智的合作化解某些问题。

以理智的方式处理一项影响到资本市场和投资界的问题并不完全令人惊讶,因为退市会影响到的是全球最富裕的精英派,这群人在两国政府之内都有很多关系,当情况恶化时损失也最大。PCAOB执行《外国公司责任追究法》(HFCAA)的方式也是合理且专业的。这是一项授权PCAOB以立法权威来对审计中国公司的审计师进行严格审查的法律。

当HFCAA首次通过时,人们认为这只是一个日益反华的国会想减弱中国在美国的影响力的另一种手段。但是PCAOB的官僚们(在这里我是正面地用“官僚”一词来形容没有被政治风向影响,公事公办的官员)尽职尽责地开展工作。超过30名专业工作人员花了九个星期在香港,核实了其对两家审计师(即中国大陆的毕马威华振会计师事务所和普华永道的香港分所)的审查权限,也没有受到中国政府的干预。两家会计师事务所的员工与PCAOB的官员好好合作,中国证券监督管理委员会的官员在一旁不予干涉,中美两国之间的一个热点问题也就解决了!

这让我想起了查理·芒格(Charlie Munger)在2022年初说的一段话,当时他在每日日报(Daily Journal)股东大会上被问及买阿里巴巴的ADR会不会有风险时说道:

“假设文明国家之间能保持对对方合理的尊重,这个风险在我看来并不是很大。”

看起来芒格的假设是正确的。尽管美国和中国政府在大多数问题上的分歧和竞争性越来越激烈,但在大多数问题上还在保持着文明的态度。只要基本态度是文明的,无论双边关系多么恶化,至少有些问题还是可以合理解决的。

以“合理性”为基础的“安全边际”

如果您是一位对中美两国在处理这个退市问题上的合理性持有足够信心的投资人,那您应该已在退市恐慌期间重仓加码了很多在美上市的中国公司股票,并最终获得丰厚的收益。

事后来看,即使是最厉害的投资人也无法完美地做到这一点。

芒格在2021年第一季度开始在每日日报的旗下购买阿里的股票,那年曾最多持有602,060股。但随着2022年退市恐慌持续,他把手上的阿里股票减少到现在的300,000股。有人怀疑他将一部分ADR股票转移到港交所,保持阿里持股的数量。我无法核实他是否有没有这么做。但很明显,他没有在阿里和大多数中国公司在2022年的稳步下跌时加码增股。

Seth Klarman,Baupost Group的著名价值投资人,也经常与芒格和沃伦·巴菲特(Warren Buffett)相提并论,表现得稍微好一点。他在2022年第二季度投了新东方教育,买了800万股,这是在2021年和2022年初股票暴跌之后的举动。然而在东方的股价持续低迷时,Klarman没有继续买,而在2022年第三季度股价回升是,卖出了一些兑现。

我,作为一个远不及克拉门和芒格的投资人,在2021年和2022年期间买卖了多家中国公司的股票,但没有足够的信心长期持有它们。在整个退市风波期间,我个人当时认为大规模退市的可能性不超过10%,因为仅仅为了逃避一项完全合理的审计要求而切断全球资本市场的流动是不合理的。然而,我并没有足够的勇气来加码和长期持股。当然,退市威胁仅是中国股票在过去三年多时间里下跌的多种原因之一,其他还有清零、反垄断、以及针对科技、教育、房地产等主要行业的政策监管变化等。

正如芒格曾经说过:“如果投资不难,那每个人都会很有钱了。”

确实很难。

资本市场不仅仅是资本

许多中国公司在港交所进行二次上市来对冲退市风险。

像阿里和百度这样的大厂都操作了二次上市。新兴公司如小鹏汽车和理想汽车在纽约证券交易所和香港交易所进行了双重同时上市。拼多多和满帮也有同样的计划,但他们等到了PCAOB的好消息后取消了计划。

这些对冲措施给人一种错觉,即港交所和允许中国内地投资者进入港交所的“沪港通”计划足够能成为与华尔街媲美的上市选择,中国公司既可以留在本国的边境内,还依然可以好好活下去。

事实并非如此。

当然,如果您是一家产品市场局限于国内,而且没有野心出海的公司(或是一家国企),那在港交所或上海或深圳上市没什么问题;在纽约上市肯定更麻烦。从流程上看,如果有钱的外国机构投资组织真的想投这些纯粹服务国内的公司,他们总可以找到方法。资本进入没什么阻碍,只是交易成本会高些。

然而,很多中国公司有出海的野心 — 要么是因为国内市场规模不够大,支撑不了长期发展,要么是因为自身的产品确实具有国际吸引力,要么是因为他们向早期投资人画了个大饼,估值过高,必须出海发展才能兑现。电动汽车、企业软件、云基础设施以及部分半导体行业的公司都有这些特点。

对于这类公司来说,纽交所或纳斯达克仍然是最受欢迎的上市途径。这里部分原因是因为美国证券交易委员会(SEC)以披露为导向的监管制度比香港以合规为导向的监管制度对公司更友好。但更重要的是,能在纽交所或纳斯达克上市所得到的“名誉光环”是港交所目前无法复制的。在纽约上市的新公司,至少在我上述提到的领域内,更有可能成为国际品牌,同时还能吸引足够的资本来实现梦想。目前港交所还无法,今后也可能越来越难,能给在所上市的公司提供这种声誉提升,因为香港发展的方向是“向内”的。

因此,从中国政府的角度来看,与PCAOB合作是值得的,哪怕只是为了不阻碍本国最有前途和野心的公司出海的前景,这些公司的成功最终也会以财富或名誉 “报效祖国”。

当理性能给予足够的激励时,即使在两个关系日益恶化的超级大国之间,理性时不时还是会占上风的。我可能听起来过于乐观(这也是我的天性),但正如“退市风波”的结尾所证明的,美国和中国之间还是有些问题和冲突可以理性解决的。

如果能预测下一个能被“理性解决”的问题,那回报也一定是丰厚的。