The Chinese economy may well be heading into a recession. But one sector that has continued to grow, seemingly unabated, is its cloud computing industry. According to Canalys, China’s total cloud spending in 2021 increased by 45%, bringing high expectations for more in 2022.

Last month, the China Academy of Information and Communications Technology (CAICT) published an in-depth, 47-page-long whitepaper, analyzing the current state of the country’s cloud industry. The CAICT is a think tank affiliated with the Ministry of Industry and Information Technology (MIIT) – a key regulator of China’s tech sector and a Ministry of frequent discussion in my previous writings (see tags: open source and e-CNY for more on MIIT). This is the 8th such whitepaper the CAICT has produced; the first one was published in 2012.

You can think of this whitepaper as the most official assessment of how China thinks its own cloud industry is doing, not what an outside industry analyst firm, like Canalys or Gartner, thinks in order to serve their clients, e.g. institutional investors and money managers.

So how is China’s cloud industry doing, according to China? In a nutshell: still in its early days and mostly stuck in the IaaS stage.

Let’s unpack this whitepaper for more details and nuances.

Cloud Maturity: China Versus the World

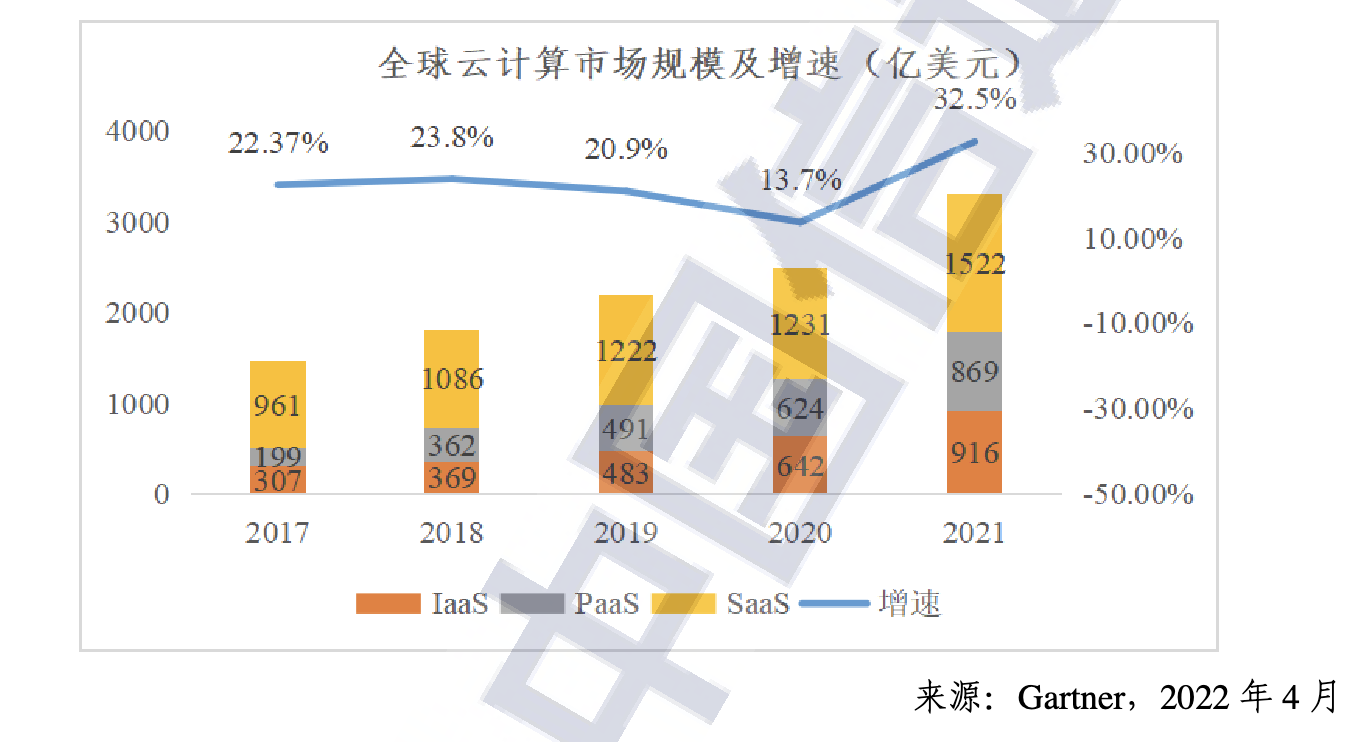

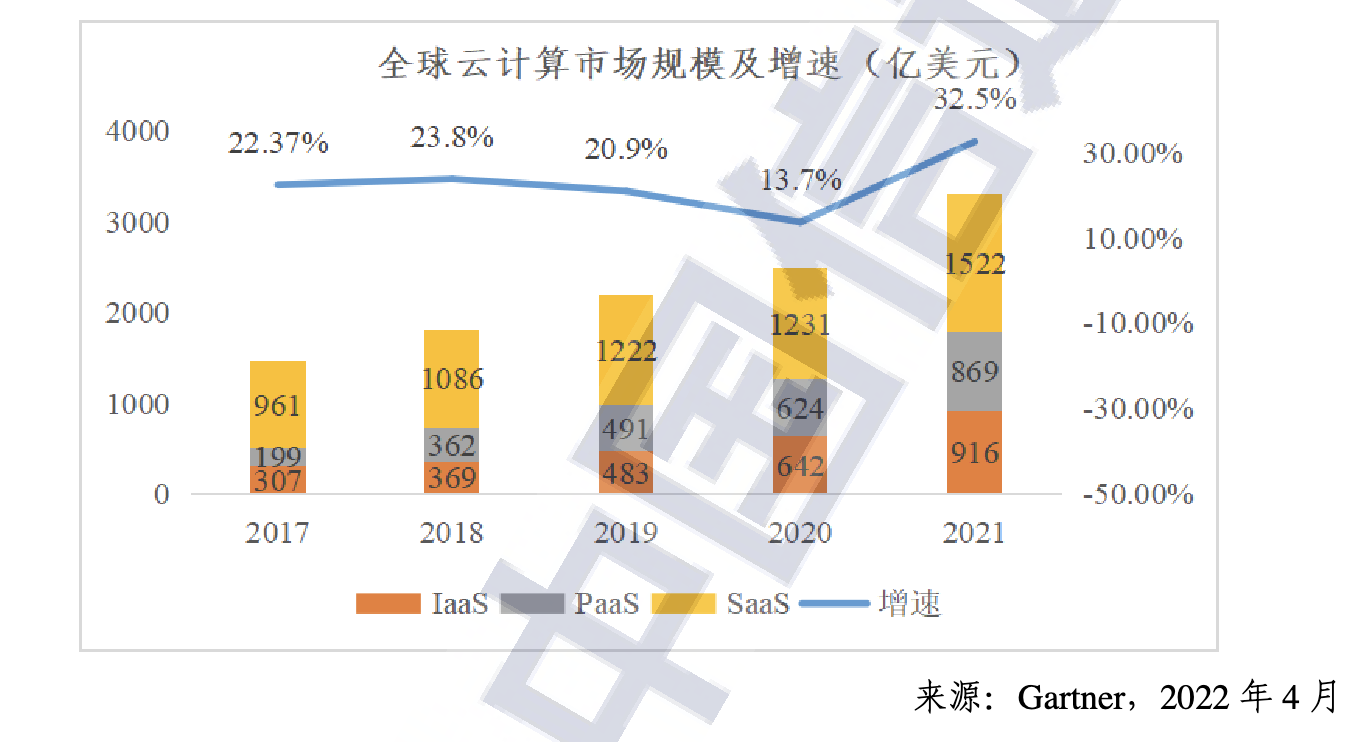

The whitepaper began by citing Gartner’s global cloud computing growth trajectory (see graph below). This shows that even an official Chinese think tank relies on Gartner as a main source of information to an extent. (Well done, Gartner!) Interestingly, the whitepaper separates the cloud market into three buckets – IaaS, PaaS, and SaaS – to illustrate some significant differences between China’s cloud industry growth characteristics and the world’s.

An aside on terminology, a full-fledged cloud computing service is generally broken down into three layers:

- IaaS (Infrastructure-as-a-service, aka processors like CPUs/GPUs, storage units like SSDs or hard drives, and networking bandwidth for rent)

- PaaS (Platform-as-a-service, aka database, application development, big data analytics engine, AI/ML frameworks for rent)

- SaaS (Software-as-a-service, aka user-facing applications like email, workplace messaging, video-conferencing, document-sharing for rent)

In Gartner’s global projection, while all three layers of the cloud are steadily growing, SaaS makes up the largest proportion, while IaaS and PaaS almost equally split the rest of the market. The picture is starkly different in China.

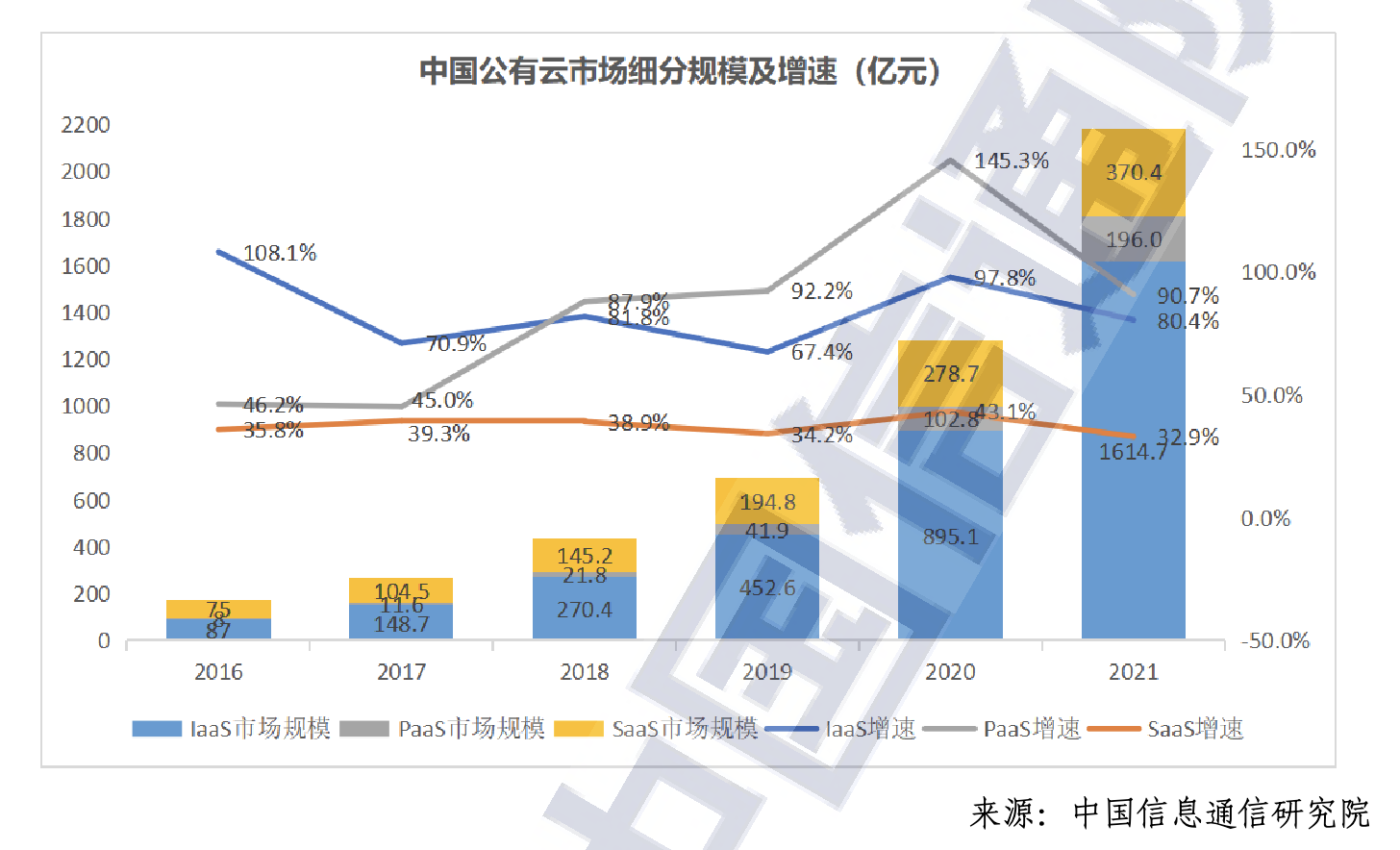

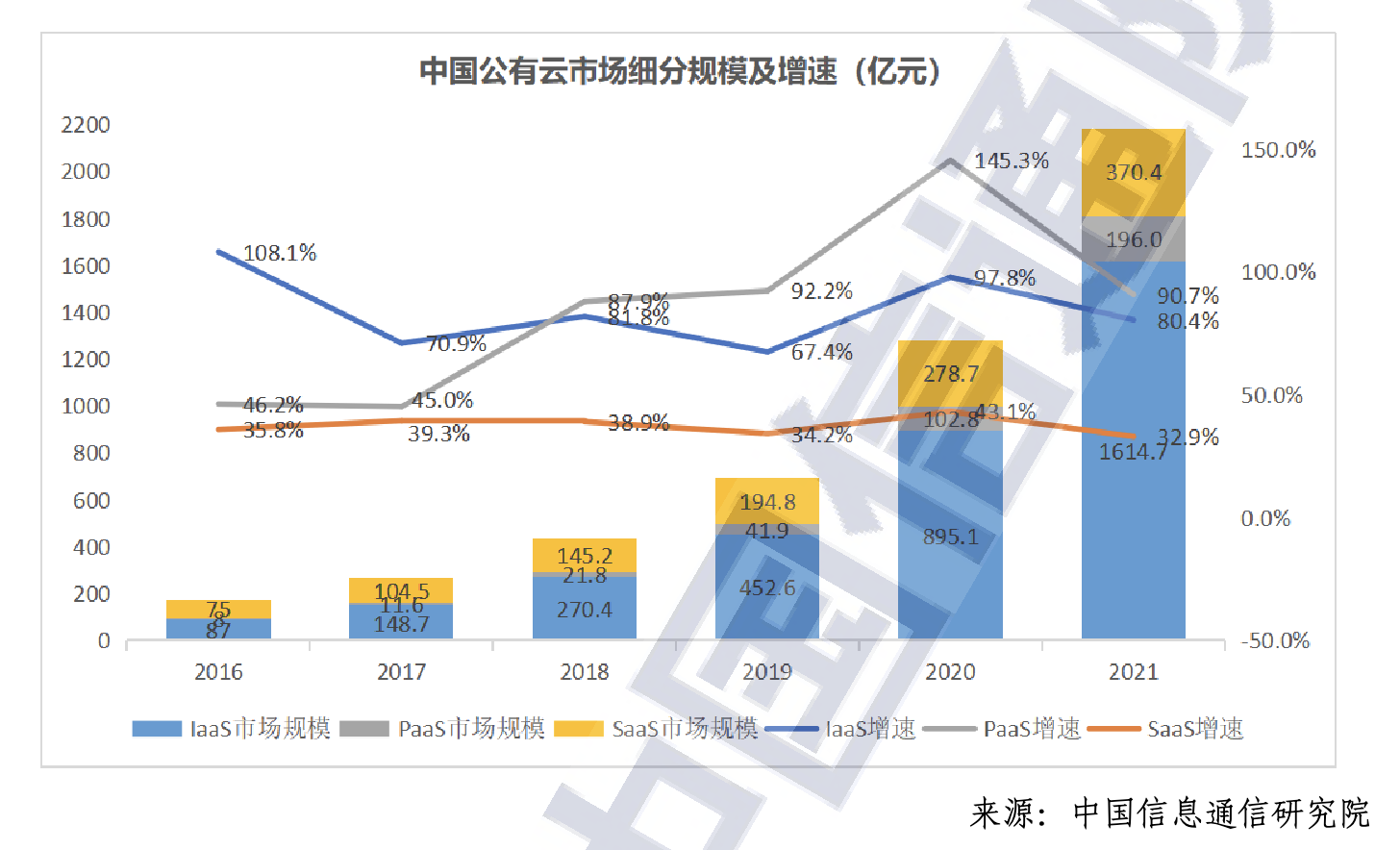

Based on CAICT’s own data (see graph below), IaaS (in blue) makes up almost three-fourth of China’s entire cloud and is growing rapidly (67.4%, 97.8%, 80.4% respectively in the last three years). SaaS (in yellow), on the other hand, is the second largest but markedly smaller with a much lower growth rate compared to IaaS (34.2%, 43.1%, 32.9% respectively in the last three years). PaaS (in gray), which architecturally sits between IaaS and SaaS, is the smallest of the three buckets, making up only 10% of the whole cloud computing pie. That being said, PaaS’s growth rate is higher than IaaS, albeit on a much smaller base.

What does this mean?

China’s cloud journey or “digital transformation” (to use the industry buzzword) is still in its infancy. Adopting IaaS (from owning your own machines and networking equipment to renting from a cloud vendor) is the first step for any large enterprise’s migration to the cloud. It is clear that most of China’s cloud spending growth is still happening at this layer, and will need some time to mature before spending moves to the PaaS and SaaS layer.

Public versus Private:

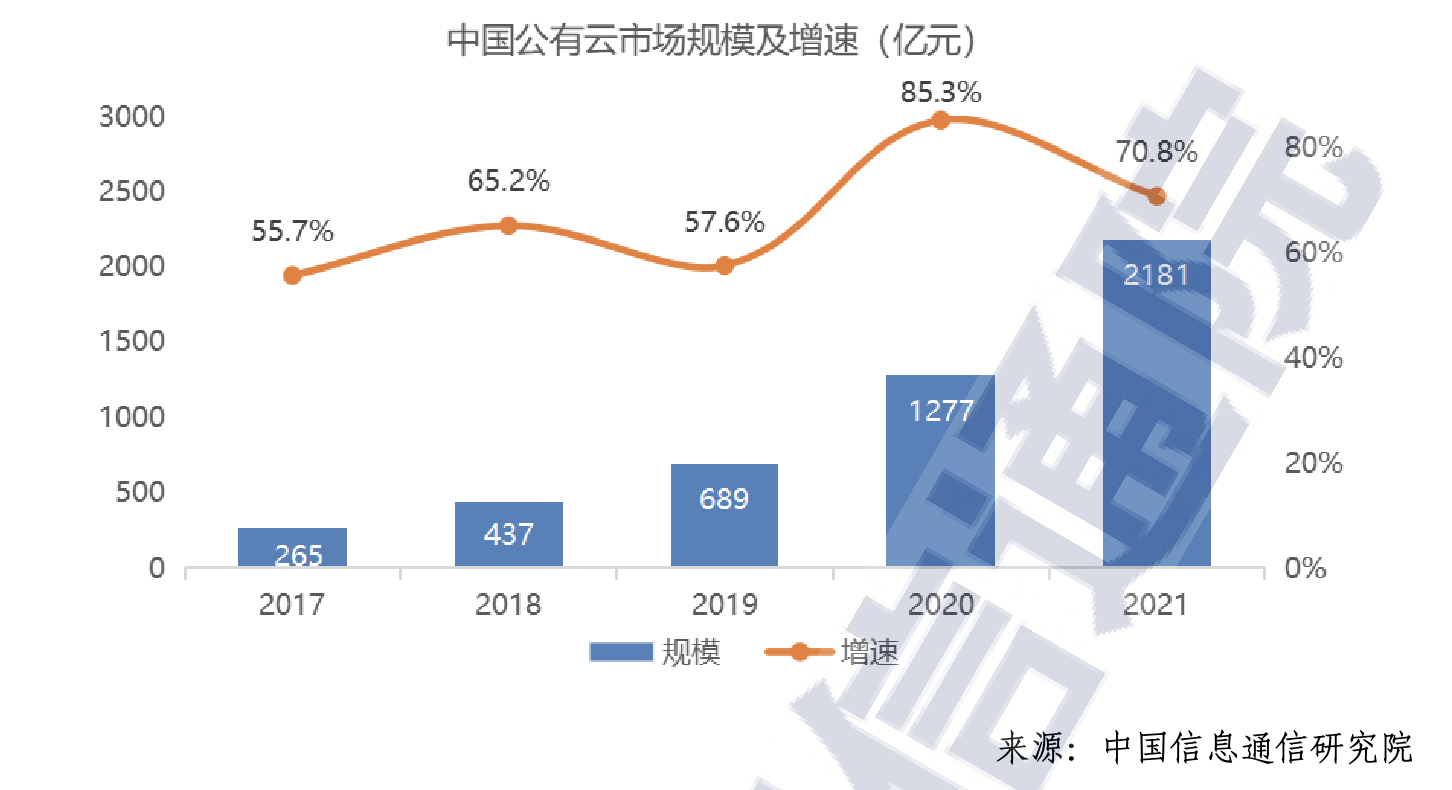

This whitepaper also provides a useful breakdown of the relative adoption size and rate between public and private clouds. In short, China’s public cloud is about twice as large as its private cloud (218.1 billion RMB vs 104.8 billion RMB) and is also growing twice as fast (70.8% vs 28.7%)! (See graph below, first one is private cloud, second one is public cloud.)

This data contradicts a common perception in the market that the demand for public cloud in China is declining – a conclusion drawn from AliCloud and Tencent Cloud’s slowing growth rate. However, China’s cloud market, both public and private, is much more crowded and competitive than the duopoly of Alibaba and Tencent.

Which Cloud Vendor is Winning?

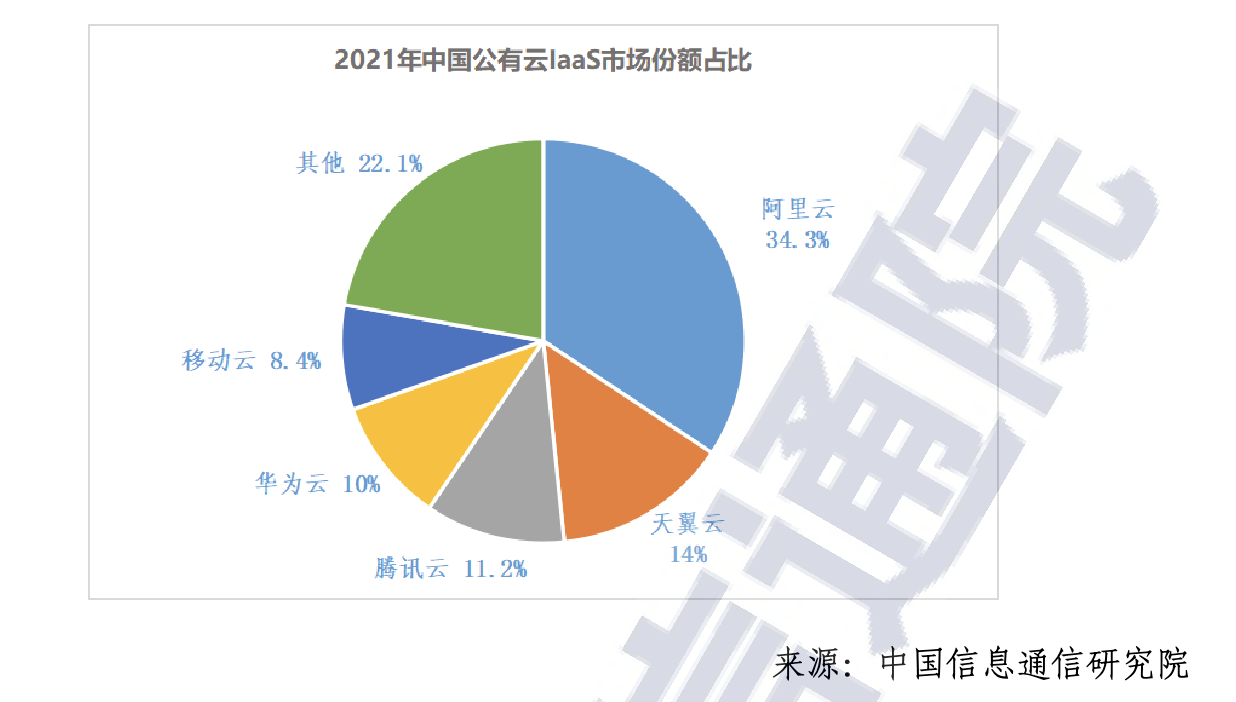

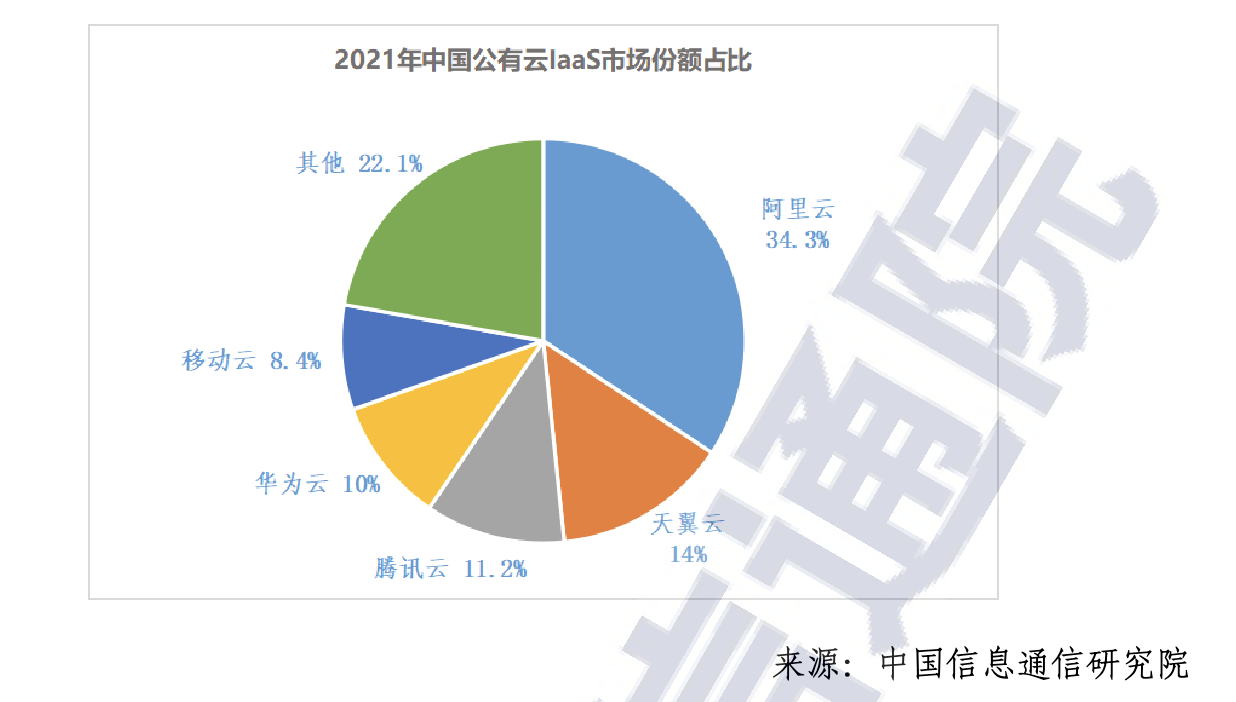

Based on CAICT’s numbers, the top five public cloud IaaS providers by market share in 2021 are:

- AliCloud: 34.3%

- CTyun: 14% (China Telecom’s cloud)

- Tencent Cloud: 11.2%

- Huawei Cloud: 10%

- Mobile Cloud: 8.4% (China Mobile’s cloud)

Although AliCloud remains the leading provider by a healthy margin, state-owned telcos like China Telecom and China Mobile are becoming formidable players in the fast-growing IaaS layer. Telcos entering the cloud market is quite common in many markets. They are typically the default Internet Service Providers (ISPs) and mobile data providers of a country, with the foundational infrastructure and networking capacities already in place. Becoming a cloud IaaS vendor is a matter of converting their existing resources to a “for rent” model. (In fact, it is a bit surprising that AT&T and Verizon are not bigger players in the US cloud market.)

What’s also noteworthy is the increasingly even distribution of market shares. It was only a few years ago when AliCloud was more than 50%, and its aggressive marketing department would gloat about being bigger than the next ten competitors combined. Not any more!

The public cloud PaaS market share leaders, in CAICT’s eyes, are the following:

- AliCloud

- Huawei Cloud

- Tencent Cloud

- Baidu Cloud

Naming these vendors as leaders is not surprising, because building attractive PaaS solutions requires attracting more capable tech talent, which pure tech giants like Alibaba and Huawei are better positioned to do than SOEs, like China Telecom. It takes more than just converting existing infrastructure to a different, for-rent business model to compete in PaaS.

However, the whitepaper does not provide a proportional breakdown for the PaaS layer, and did not even mention the SaaS layer. That’s likely because these two segments are simply too small and immature in the grand scheme of things, as we already illustrated.

Three Tiers of Maturity

While China’s overall migration to the cloud is progressing quickly, the progress is not evenly distributed. The CAICT provides its evaluation of which industries are ahead and which industries are lagging behind, separated into three tiers.

Tier-1: Internet and IT services sector. Unsurprisingly, these two sectors are the most tech-native and tech-forward of all the sectors. In CAICT’s assessment, their cloud journey is quite mature, having already integrated advanced technologies in AI, big data, and even blockchain to the use of best-in-class cloud technologies. They are the leaders of the pack.

Tier-2: Financial services, government, and transportation sector. This tier-2 can be roughly understood as sectors that are not on the bleeding-edge per se, but are mature enough in their cloud migration to be comfortably adopting technologies and architectures, like containerization, microservices, and middlewares in their core systems. Successfully adopting these types of technologies is a good indicator of becoming more “cloud native”. Having the financial sector in this category is not surprising, given that banks and financial institutions tend to be early adopters compared to large enterprises in other sectors. This is especially true in China, where the advancement of fintech and neobanks is fast and pose serious competition. What did surprise me is having both government and transportation – two common late adopters of technology – included in this tier-2. If the government sector’s receptiveness to the cloud is indeed on the same level as financial services, then the rise of “govcloud” as a product line could be a key driver of growth for China’s cloud industry in the next few years.

Tier-3: Energy, healthcare, and industrial sector. This tier-3 encompasses sectors that are still “nibbling around the edges” when it comes to cloud. For the energy sector, in particular, cloud adoption is literally limited to the edge – small workloads in far-flung remote regions, not at the corporate headquarters or where its core systems are managed. The CAICT whitepaper gently called out these sectors as laggards, whose progress to “cloudify” their core systems has much room to improve.

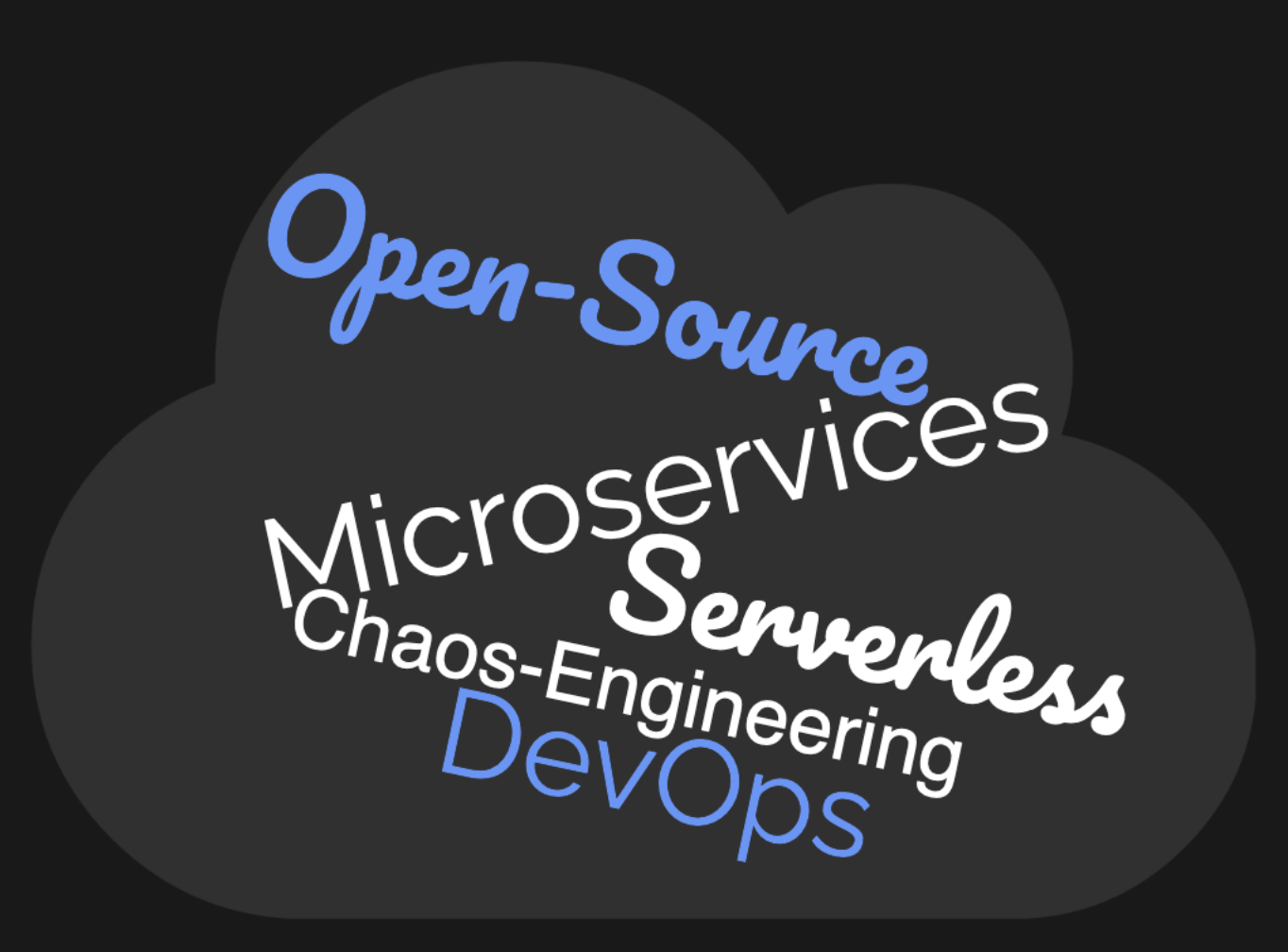

Buzzword Cloud

Even though it was written by a government think tank, there is no shortage of industry buzzwords in this whitepaper. Here is a list of my favorite buzzwords and their frequency of appearance:

- Microservices: 10

- Open Source: 8

- Chaos Engineering: 4

- DevOps: 3

- Serverless: 3

Because this CAICT whitepaper does not share any information on its research process, it is difficult to verify the source and reliability of its data and commentaries. However, the whitepaper reads mostly like what you would expect from any think tank or a group of government technocrats – dry, to the point, appropriately boring. It also pinpoints many weaknesses in China’s cloud industry, especially in areas like cybersecurity and software supply chain, and is not a full-throated celebration of the industry's growth.

While we should always treat government publication with a grain of salt, this one’s purpose seems mostly to inform without any ulterior agenda.

中国的云计算市场发展到什么阶段了?

(本篇中文版文章是读者 Ben Yu 做的编译,我做了一些修改后发表。非常感谢Ben的贡献!)

虽然中国整体的经济状态不容乐观,但有一个行业似乎是例外,仍在继续增长——云计算行业。根据 Canalys 的数据显示,中国 2021 年的云计算支出总额增长了 45% ,这让所有人都对 2022 年的增长情况有较高的预期。

上个月,中国信息通信研究院(简称信通院)发布了一份 47 页的云计算白皮书,分析了该行业在中国的现状。信通院隶属于工业和信息化部(简称工信部),而众所周知工信部是目前对中国科技公司进行监管的一个重要机构,在我之前写的许多文章中可以看到它的身影(详情可见:开源和e-CNY标签)。这次是信通院发布的第 8 本白皮书,第一本可以追溯到 2012 年。

这本白皮书的影响力该怎么理解呢?它可以被是为中国权威机构对中国整个云计算行业发展情况的“官方”评估,这和 Canalys 或 Gartner 这样的分析公司为他们的客户(如投资者和基金经理)而编写的报告是完全不同的。

那么在这本白皮书里,云计算行业表现如何?一言以蔽之:仍然处于行业早期阶段,还处于 IaaS 是主流的阶段。

我们来仔细看看白皮书里的内容。

云服务市场: 中国市场 VS 全球市场

白皮书里首先引用了 Gartner 有关全球云计算增长情况的数据(见下图)。值得注意的是,白皮书将云计算市场分为三个层面—— IaaS、 PaaS 和 SaaS,从这三个部分来说明中国市场和全球市场在增长上的表现差异。

首先,让我们对一些行业专用名词做些解释:

- IaaS:Infrastructure-as-a-service,指基础设施即服务,把 IT 基础设施作为一种服务通过网络对外提供,并根据用户对资源的实际使用量或占用量进行计费的一种服务模式,提供的内容主要包括 CPU、内存、 存储、网络、虚拟化软件、分布式系统等。

- PaaS:Platform-as-a-service,指平台即服务,提供运算平台与解决方案服务,广泛用于开发框架、商业分析、人工智能等。

- SaaS:Software-as-a-service,指软件即服务,是大部分用户最直接接触到的一类服务,如电子邮件、视频会议、在线文档等等。

根据 Gartner 提供的全球数据,虽然三种服务都在增长,但 SaaS 占据了最大的增长比例,相比之下 IaaS 和 PaaS 平分了剩余市场。然而,中国市场的情况则截然不同。

根据信通院提供的数据(见下图),IaaS (图中蓝色部分)几乎占中国整个云计算市场的四分之三,并且还在快速增长(过去三年分别为 67.4% ,97.8% ,80.4%)。相较之下,SaaS(图中黄色部分)部分明显占比更少,增长率也远低于 IaaS(过去三年分别为 34.2% ,43.1% ,32.9%)。PaaS (灰色部分)在架构上位于 IaaS 和 SaaS 之间,是其中占比最少的,仅占整个云计算市场的 10%,但从增长率上看,PaaS 要高于 IaaS(虽然基数小)。

上述的数据意味着,中国的云计算市场,或说“数字化转型”仍处于起步阶段。采用 IaaS(从拥有自己的服务器和网络设备到从云供应商租用)是任何大型企业向云迁移的第一步。很明显,中国大部分的云支出增长仍然发生在这一层,在支出转移到 PaaS 和 SaaS 层之前,需要一些时间来成熟。

公有云 VS 私有云:

白皮书还罗列了公有云和私有云的数据。简而言之,中国的公有云大约是私有云的两倍(2181 亿人民币 vs 1048 亿人民币),增长速度也是私有云的两倍(70.8% vs 28.7%) 。下面两张图,第一张是私有云,第二张是公有云。

这个数据和市场上大部分人的看法完全不同,因为阿里云和腾讯云的增长在放缓,很多人因而认为企业对公有云的需求程度有所下降。然而无论是公有云还是私有云,这个赛道并不完全被阿里巴巴和腾讯垄断,有更多的选手身处其中。

云服务厂商市场情况

根据信通院的数据,2021 年按市场份额排名前五的公有云 IaaS 提供商是:

- 阿里云:34.3%

- 天翼云:14%(中国电信)

- 腾讯云:11.2%

- 华为云:10%

- 移动云:8.4%(中国移动)

虽然阿里云目前依然是“领头羊”,但是像中国电信和中国移动这样的国有电信公司也在迅速崛起。电信公司进入云计算市场在全球各地都非常常见,它们通常是一个国家的默认互联网服务提供商(ISP)和移动数据提供商,其基础设施和网络能力已经到位。要成为一个云 IaaS 供应商,只需将现有资源转换为“出租”模式即可,一个例外是美国的云计算市场,AT&T 和 Verizon 反而没有什么大的声量。

同样值得注意的是,市场份额的分配越来越均衡。就在几年前,阿里云的市场占有率还在 50% 以上,当时阿里的营销话术是“阿里云的市场份额是其他 10 家竞争对手的总和”。然而现在情况已不再如此。

在信通院的数据中,公有云 PaaS 市场排名如下:

- 阿里云

- 华为云

- 腾讯云

- 百度云

很容易发现,这些都是国内最头部公司的产品,这是因为建造好的 PaaS 需要吸引很多优秀的科技人才的加入,而阿里巴巴和华为等科技巨头比中国电信等国有企业对他们来说更有吸引力,这意味着要在 PaaS 中竞争,需要的不仅仅是将现有基础设施转换为不同的出租业务模式而已,还包括公司文化、组织架构等方面。

白皮书里没有提到 PaaS 层的具体情况,SaaS 也没有提到,很可能是这两者的市场实在太小,以至于不值得拆分开来看详细的数据。

行业应用水平的三个梯度

尽管中国云计算市场的整体增长速度很快,但聚焦在具体行业上,增长速度就有较大的差异。信通院基于应用水平将行业分成 3 个梯度。

第一梯度:互联网和信息服务业。这两个行业已基本实现云计算的深化应用,能够充分将人工智能、大数据、区块链等新兴技术和云原生能力融合。这并不让人意外,毕竟这两个行业是所有行业里 IT 能力最强的。

第二梯度:金融、政务、交通等行业。可以理解为这些行业虽然本身不算前沿,当时在云化改造上已经足够成熟,普遍采用容器、微服务、中间件等云原生技术进行底层架构的云化升级。银行和金融机构的数字化程度高并不让人意外,因为他们都面临比较激烈的竞争。政务和交通行业反而值得玩味,2G 业务可能是未来整个中国云计算市场增长的关键驱动力。

第三梯度:能源、医疗、工业等行业。这个梯度包含那些对云服务还没有深入使用的行业。例如能源行业的生产环境大多处于边远地区,对分布式云的应用还不足够。基本上信通院在白皮书里比较温和地指出了这些行业的待改进部分还有很多很多。

流行语云

尽管这本白皮书是由一个政府机构编写的,但不乏还是参杂了很多行业的“流行语”(buzzword)。下面是一些我关注到的和出现次数:

- 微服务:10

- 开源:8

- 混沌工程:4

- DevOps:3

- Serverless: 3

这本白皮书没有罗列任何有关其研究过程的信息,因此很难核实其数据的来源和可靠性。另外,这本白皮书和其他政府编写的文档一样枯燥无味,没有读起来“津津有味”的感受。该报告还指出了中国云计算市场许多急于完善的地方,尤其是在网络安全和软件供应链等领域。

作为读者,虽然应该保持对政府发布文档的属实程度报以谨慎的态度,但是这本白皮书里的信息总体还是比较客观的。