As the global economy becomes increasingly technology-driven and less trade-driven, the most important demographic to understand is developers. These are not just underground hackers or hoodie-wearing code monkeys; they are creative problem solvers who use digital technology to build things. In my last deep-dive, I profiled Agora, the API platform company for building apps with real-time audio and video capabilities. One of the reasons behind its current success is its product’s developer-friendliness.

So how many developers are there? How many will there be to power this global economy? And where will the next generation of developers come from?

There are currently 56 million developers on GitHub, the world’s dominant developer collaboration platform, according to its own “2020 State of the Octoverse” report. GitLab is a fierce competitor of GitHub. BitBucket and SourceForge are both still around. Alternatives like Gitee are also being fostered. Thus, there are likely more than 56 million developers total at this moment.

GitHub predicts having 100 million developers on its platform by 2025, so we are looking at an almost doubling of the number of developers in the next five years. That’s why in my “Global by Nature” series -- my investment and opportunity set for the next 10 years -- I placed understanding developers at the very top of all considerations.

Digging deeper into GitHub’s report, there are some fascinating trends to illuminate where these next 50-million-plus developers will come from and what that means for the next phase of globalization.

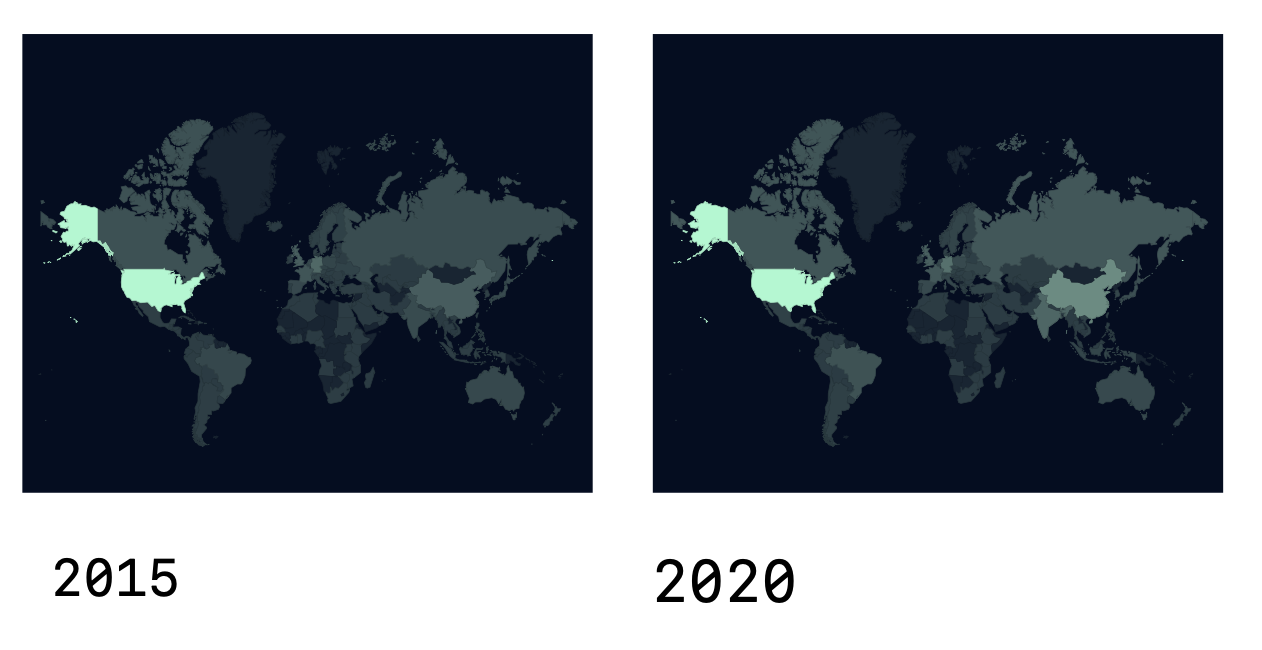

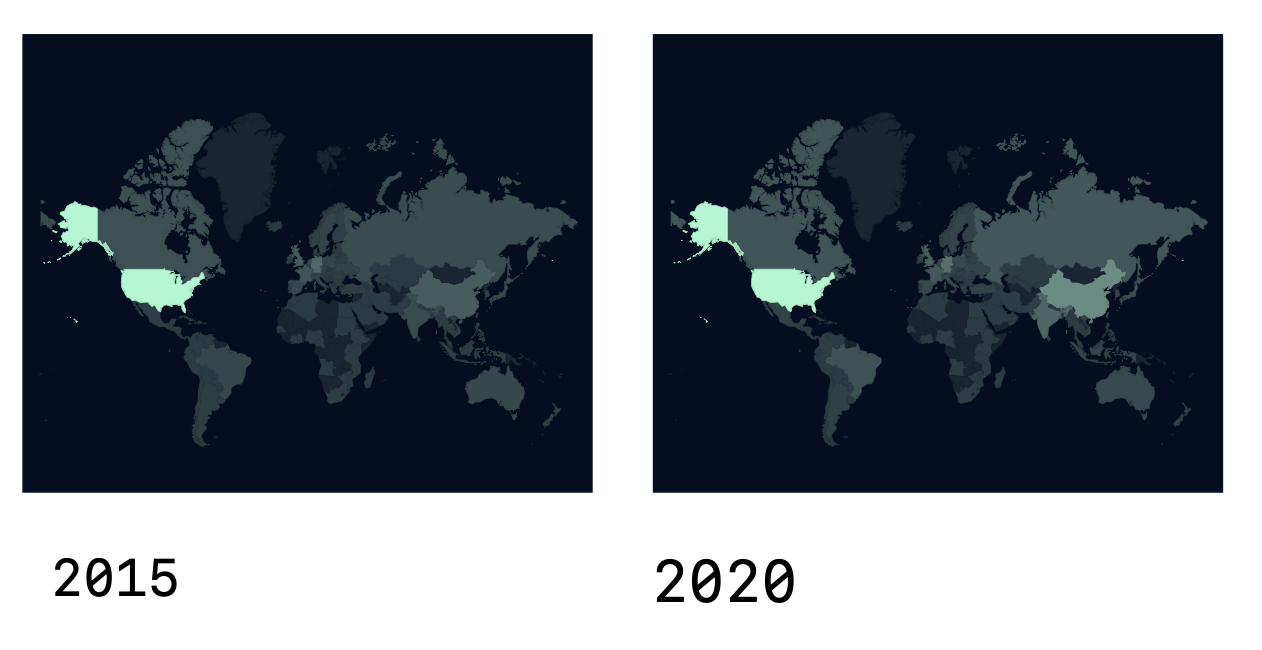

From 2015 to 2030

The 2020 State of Octoverse report provides a nice visual of where open source contributors were coming from and where they may be from in the future -- from 2015 to 2020 and projecting into 2025 and 2030. Open source technologies are powering the world’s economy. Thus, open source contributor count is both an effective heuristic of developer growth (most developers use or contribute to open source) and overall economic growth.

In 2015, the US was the lone bright spot, accounting for 30.4% of the world’s open source contributors. Germany and the UK were number 2 and 3 with 7.3% and 5.8% respectively.

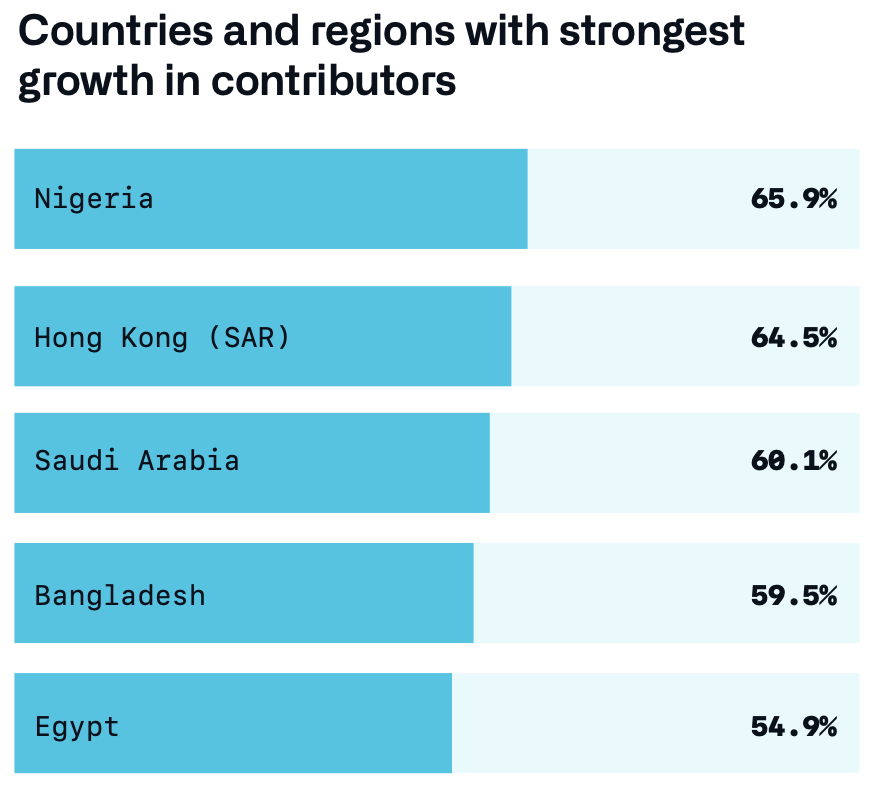

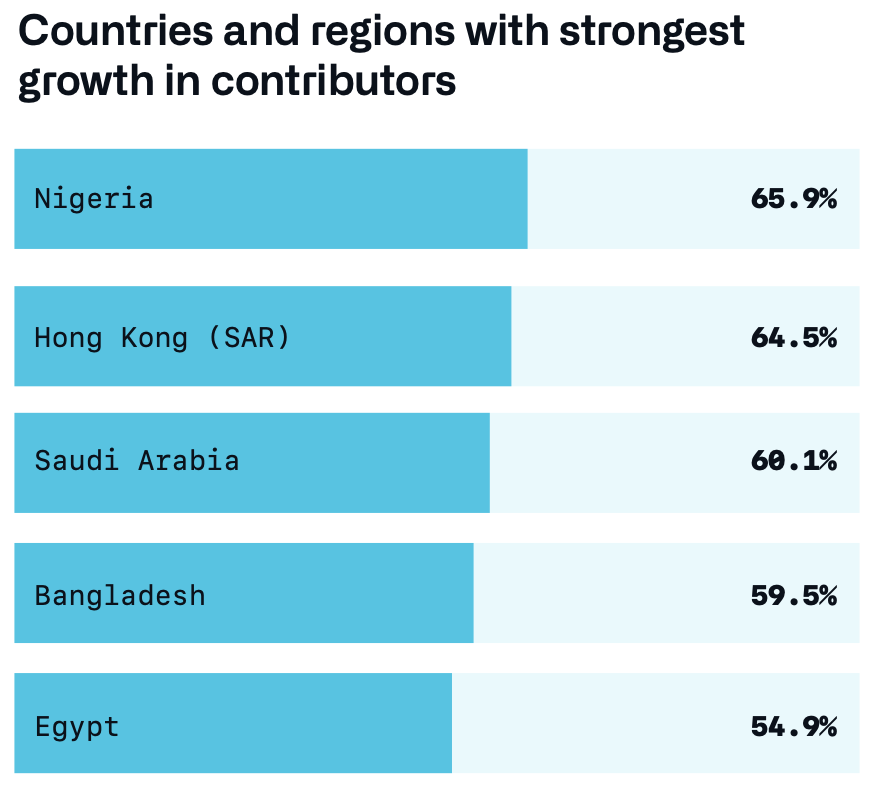

However, in just five years, that distribution has shifted quite significantly. By 2020, the US is still number 1 but its proportion of contributors has fallen to 22.7%, while China and India raced ahead to 9.76% and 5.2% respectively. Being the two largest developing countries, China and India’s growth shouldn’t come as a huge surprise. What may be surprising is the growth of other smaller countries and regions. Here’s the top five in terms of year-on-year growth rate in 2020:

Pakistan, Indonesia, Turkey, Colombia, and Peru round out the second half of the top 10. It’s also important to keep in mind that huge growth rates are usually the result of a small base number, so take that into account when you think about these rather large growth numbers. What’s more interesting to me is that the fastest growing developer clusters are coming from Africa, the Middle East, and Latin America.

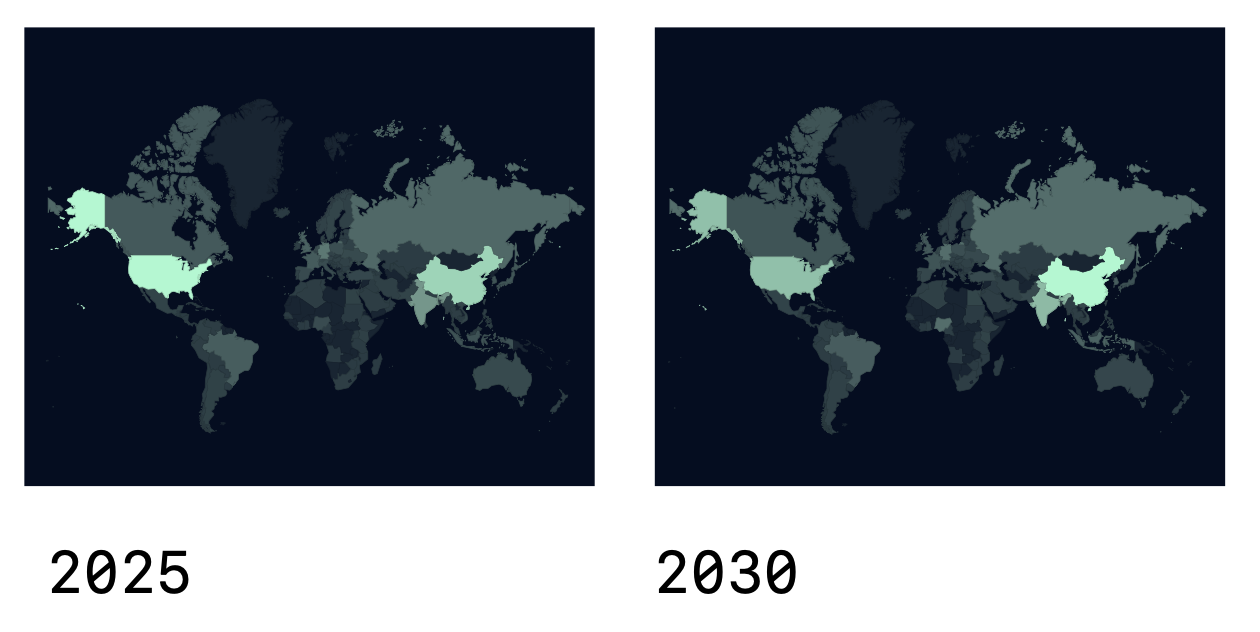

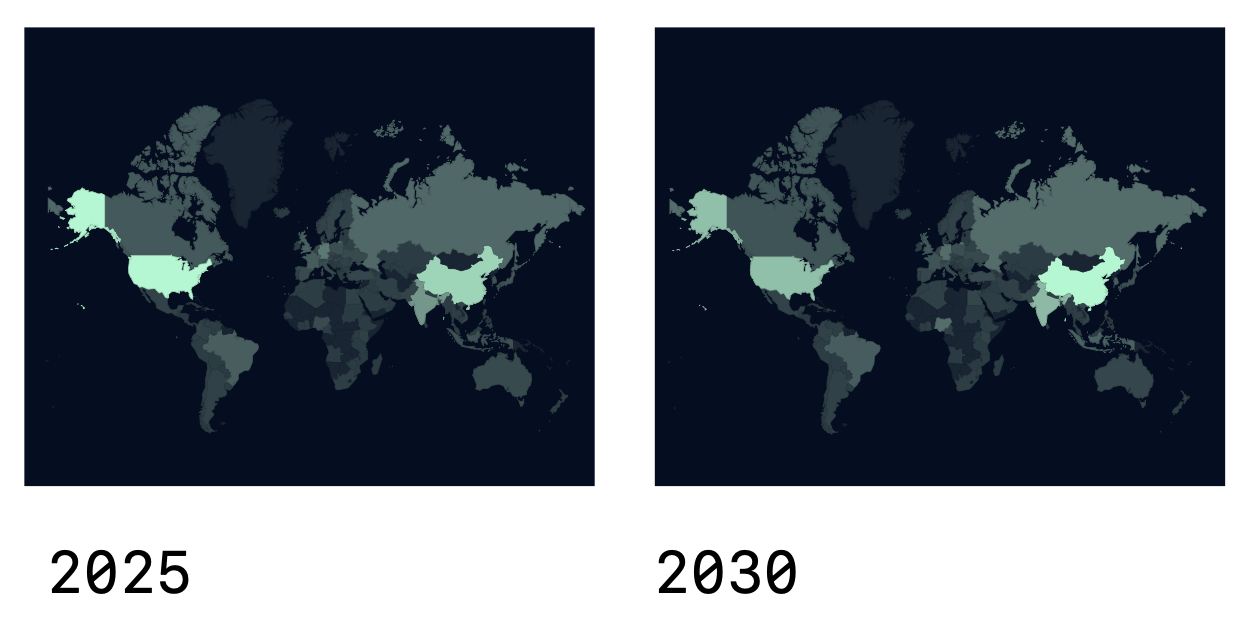

Looking into GitHub’s “crystal ball,” by 2025, the US’s open source contribution is expected to decrease and stabilize to around 16.4%. China’s share will continue to increase to 13.3%, India’s to 7.9%, while Brazil and Nigeria may register 3% and 1.5% respectively.

GitHub did not provide a prediction for 2030, but its report did provide the same visual for what 10 years from now may look like. If you squint hard enough, China appears to be a brighter spot than the US, while India, Brazil, Russia, and Nigeria continue to get noticeably brighter. One other country that looks more visible is Indonesia.

With the exception of South Africa, this trend aligns well with the overall growth of the BRICS countries (Brazil, Russia, India, China, South Africa). It’s a short-hand of the major emerging economies, which became a loose international group that was first organized back in 2009. Its developed economies counterpart, the G7, appears to not be a part of this global developer growth wave; only the US and Germany look to maintain significant open source contributor shares.

Emerging Market Developers’ Impact

Of course, squinting is not real analysis. But it is clear that the distribution of developers will be more widespread around the world. What’s not so clear is where and how they will make economic impact.

I see the emerging market developers’ impact falling into three buckets in the next 10 years: outsourcing outposts, building domestic markets, founding global-scale startups.

Outsourcing outposts: this category is the easiest to understand, because it has been happening for a long time. Large, mature tech companies like IBM and Intel will continue to move low-end non-core technical jobs to cheaper locations with a large pool of technical workforce. India has been a big beneficiary of this trend. Other countries like Brazil and Nigeria may soon follow. Unless there are policy changes in the US that force these companies to onshore more jobs back to America to boost domestic employment, offshoring will continue, just to different locations depending on the price and size of the developer pool. The local economic impact of these “offshore developers” will be somewhat limited, as most of the savings and efficiency gains will be accrued to the multinationals doing the offshoring.

Building domestic markets: more and more tech startups are being founded in emerging markets to serve those emerging markets. I briefly profiled four tech giants in Southeast Asia in a previous post -- Grab, Gojek, SEA Group, Tokopedia. SEA Group is already a publicly traded company in New York and Grab may soon do the same. India also has a strong corp of high-growth tech companies with 21 unicorns to date, which I wrote a deep dive on in July of last year in “Unicorns Entanglement: India, China, America”. Companies like Mercado (e-commerce), Rappi (delivery service), and Nubank (neobank) lead the way in the LATAM region. Jumia (e-commerce) is the current standout in Africa. While none of these markets are anywhere near the same level as the US, the EU or China when it comes to technological sophistication or output, they all have high-growth developer clusters, as we saw above. That means they will catch up fast, particularly as more of these emerging market developers learn, use, and contribute to best-in-class open source projects, which are a big equalizer of technology access. These developers will have plenty of great companies to work for to build their domestic markets.

Founding global-scale startups: this last scenario will take the longest time to play out but, from an investor’s point of view, is also the most attractive to me. As a developer hub matures and levels-up, it will solve harder and harder problems -- first for the outsourcers, then its domestic emerging markets to bring them up-to-par with mature markets, then ultimately tackling problems that even the mature markets might need solutions to! These developers’ economic impact will be global.

It’s not unfathomable to imagine some cloud computing, enterprise tech, and AI products being built by developers in India or Brazil and selling well in the US and EU. (After all, most technology spending is still happening in developed countries.) Climate change technology is another sector where emerging market solutions can flow to developed markets. The Israeli developer ecosystem is already creating startups that are serving markets well-beyond its own border or Europe. Enterprise tech companies founded in Russia and China are also making progress in the US and EU, though they are facing unprecedented geopolitical headwinds.

This future creates both the exciting prospect of global companies being built outside of wealthy countries and the tough challenge of building, scaling, and operating global companies from places where there was no history of having done so. And much of how this future will play out will depend on how this next crop of developers use the technological superpower at their fingertips, now that we know where they will come from.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn, Clubhouse (@kevinsxu).

下一批5000万开发者会从哪里来?

随着全球经济越来越被科技主导,而不是贸易,最需要深入了解的人群是:开发者。这些人不只是什么地下黑客或穿着hoodie的码农,他们是用技术解决问题的创造者。在上一篇深度分析中,我介绍了声网,一家提供实时音频和视频功能的API平台公司。它目前能成功的背后原因之一就是其产品对开发者的友好性。

那么这世界上到底有多少开发者?会有多少人去推动这个全球经济的发展?下一代开发者又将从何而来?

根据GitHub自己出版的 "2020年Octoverse状态" 报告,目前GitHub上有5600万开发者。GitHub即是全球最主流的开发者协作平台。GitLab是GitHub的竞争对手之一。BitBucket 和 SourceForge也都还在。像Gitee这样的替代品也在培育发展中。因此,全球目前的开发者人数应该超过5600万。

GitHub预测,2025年其平台上将有1亿开发者,所以未来5年内开发者数量几乎翻倍。这也就是为什么在我的 "生来全球化"系列中(也是我未来10年的投资关注点和理念),我把了解开发者放在所有考虑因素的首位。

挖一挖GitHub的报告就可以看到一些趋势的走向,并可以阐明这下一批5000多万的开发者将来自哪里,以及这对全球化的下一个阶段意味着什么。

2015年到2030年

这篇2020年Octoverse状态报告提供了一组很好看的世界地图,来显示开源贡献者都来自哪些国家,以及他们未来可能会从哪里来。这组地图每五年一张,从2015年到2020年,展望到2025年和2030年。开源技术正在推动世界经济的发展。因此,开源贡献者数量也是开发者增长和整体经济增长一个说明问题的指标。(大多数开发者都使用或贡献于开源项目。)

2015年,美国是全世界唯一的亮点,占全球开源贡献者的30.4%。德国和英国分别以7.3%和5.8%的比例位居第二和第三位。

然而,在短短5年内,格局就有相当大的变化。到了2020年,美国仍然是第一,但其开源贡献者比例已经下降到22.7%,而中国和印度则飞速前进,分别达到9.76%和5.2%。作为两个最大的发展中国家,中国和印度的增长也并不奇怪。令人惊讶的更是其他较小国家和地区的增长。以下是2020年同比增长率排名的前五:

巴基斯坦、印度尼西亚、土耳其、哥伦比亚和秘鲁分别是第六到第十名。当然需要记住的是,大的增长率通常是因为一个小基数的结果,所以大家在看这些数字时要切记这一点。更让我觉得有意思的是,增长最快的开发者集群来自非洲、中东和拉丁美洲。

从GitHub的 "水晶球" 往未来看,到2025年,美国的开源贡献率预计会下降并稳定在16.4%左右。中国的份额将继续增长到13.3%,印度的份额将增长到7.9%,而巴西和尼日利亚的份额可能分别会达到3%和1.5%。

GitHub没有提供对2030年的预测,但报告中给了一张2030年的地图。如果努力眯着眼睛看,中国似乎比美国更亮一些,而印度、巴西、俄罗斯和尼日利亚也继续变得更明显。还有一个看起来更亮的国家就是印度尼西亚。

除了南非以外,这一趋势与金砖五国(巴西、俄罗斯、印度、中国、南非)的整体发展十分吻合。“金砖五国” 即是主要新兴经济体的简称,早在2009年就成为了一个国际集团。它的发达国家的对应体,G7,似乎不会是这股全球开发者增长浪潮的一部分;只有美国和德国看起来会保持一定的开源贡献者的份额。

新兴市场开发者的影响力

当然,“眯着眼睛看” 不是严谨的分析。但很明显的是,开发者这个群体将会在世界各地更加分散。不明显易懂的是,他们将在哪里产出什么性质的经济影响。

我认为新兴市场开发者的经济影响在未来10年可分为三类:外包、建设国内市场、创建全球规模的创业公司。

外包:这一类是最容易理解的,因为它已经发生一段时间了。像IBM和英特尔这种大厂将会继续把低端的,非核心技术工作转移到拥有大量技术劳动红利的地点。印度一直是这一趋势的一大受益者。巴西和尼日利亚等国家也可能会扮演这个角色。除非美国有政策变化,迫使这些公司将更多的工作岗位转移回美国,以促进国内就业,否则离岸外包将继续。需要考虑的只是根据薪水和开发者集群的规模,转移到不同的地方而已。这些 "外包开发者" 对当地经济的影响将是有限的,因为大部分红利会累加到进行外包的跨国公司身上。

建立国内市场:现在已经有越来越多的科技创业公司在新兴市场成立,并为这些市场服务。我前一阵子写了一篇文章,介绍了东南亚的四家科技巨头 -- Grab、Gojek、SEA Group、Tokopedia。SEA Group已经是家纽约上市公司,Grab也很可能近期赴美上市。印度也有一批很厉害的科技公司,至今已有21家印度独角兽,我在去年7月写的《独角兽的纠缠:印度,中国,美国》中也有深度分析过。Mercado(电商)、Rappi(配送服务)、Nubank(互联网银行)等公司是拉美地区的领头羊。Jumia(电商)是目前非洲地区的佼佼者。虽然在技术成熟度或产出方面,这些市场远没有达到美国、欧盟或中国的水平,但正如我们在上面看到的,这些地区都有高速增长的开发者集群。这意味着他们会迅速赶上,特别是当这些新兴市场的开发者学习、使用和贡献于一流的开源项目时。开源的使用是平等的,所以开源技术也是一大平衡力量。这些地域的开发者将有很多优秀的公司雇佣他们,建立国内市场。

创办全球规模的创业公司:最后一种情况将需要最长的时间来实现,但作为一个投资人的角度来看,也是最吸引人的。随着一个开发者集群变得成熟,水平逐渐提高,它会去解决越来越难的问题 -- 首先是解决外包商的问题,然后是解决其国内新兴市场的问题,使其与成熟市场接轨,最后是解决一些连成熟市场都会有需求的问题! 这些开发者的经济影响力会是全球性的。

完全可以想象一些云计算、企业服务和人工智能产品,起源于印度或巴西的开发者,但在美国和欧盟会有很好的销量。(毕竟大部分技术支出仍发生在发达国家。)气候变化科技产品是另一个新兴市场的解决方案可以流向发达市场的领域。以色列的开发者生态已经打造出一些公司,业务覆盖面远远超出本国国界以及欧洲市场。在俄罗斯和中国成立的一些企业服务公司也在美国和欧盟有业务进展,尽管他们面临着前所未有的地缘政治阻力。

这个未来将会有能在富裕国家以外创造出有全球规模的公司的激进前景。当然对这些来自于从来没有过全球规模公司的地域的创业开发者来说,也会从扩张和运营等多方面面临严峻的挑战。我们现在已经知道他们将从哪里来了。这个未来会如何发展,在很大程度上将取决于这下一批开发者如何利用他们手中的科技去塑造未来。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!