There is no doubt that geopolitics is a major driver of TikTok’s fate in the United States. But if and when it does get sold, it’s still a multi-billion dollar transaction that has to make some business sense.

I have written quite a few posts on the various political and regulatory angles of TikTok already, so I won’t belabor those points here (though I do hope you give them a read for context of my general thinking). Instead, I’ll focus on how to think about what part of TikTok is worth, to whom, and why, in particular for Microsoft+Walmart and Oracle -- the two most likely groups of bidders to successfully buy TikTok.

Typically, an acquisition of any size needs to make sense along at least one, but hopefully more than one, of these dimensions:

- Product synergy

- Users and data

- Core technology

- Brand

- Company and people

Let’s take a look at the relative value of each of these in the context of TikTok.

Product Synergy: Cloud and E-Commerce

Cloud

The entire global cloud industry is still relatively young, growing quickly, and thus all the major vendors are in “land grabbing” mode, trying to gobble up market share first before worrying about profitability. But the landscape is also transitioning to “differentiation” mode, where cloud providers are looking for ways to “stand out”. While you can do a fair amount of differentiation with aggressive marketing, the most effective way to “stand out” is to demonstrate what types of workload your cloud can handle better than everyone else in the industry.

That’s where TikTok comes in. TikTok, as a product, has a unique set of workloads that requires:

- storing and processing a ton of videos;

- visual search with computer vision;

- live streaming;

- running AI algorithms continuously to serve different feeds and ads for different uses;

- (increasingly) e-commerce transactions directly in the app.

Thus, it’s no surprise that TikTok uses both AWS and GCP as its two cloud providers in the US -- the same two providers that Snap uses. Being the “visual communications” company, Snap’s workload is the closest mirror to TikTok’s, even though it lags far behind in AI, live streaming, and e-commerce. (Snap spends handsomely on these two clouds, which I did a deep-dive on in “AWS and GCP Are the Real Winners in Snapchat’s Growth” a few months back.)

For either Microsoft or Oracle, acquiring TikTok and running the product on its cloud will help differentiate itself from AWS and GCP along these workload dimensions. This differentiation is not just a marketing practice, but a real stress test of engineering. It’s a stress test that both Microsoft and Oracle lack, because they have always been enterprise software companies with little or no experience running consumer applications at scale. Both firms are good at being “enterprise ready”, but not at being “Internet ready”. And the ability to handle workload stress at scale is what cloud customers pay for.

To proxy what kind of “stress” a cloud can handle, it’s helpful to analyze the company’s other core businesses and the workloads required to run them well. (As an example of this type of “stress test” analysis, see a two-part series I wrote a few months ago profiling all the major cloud platforms: AWS, Azure, GCP, Alibaba Cloud, IBM Cloud, Oracle Cloud, Tencent Cloud.)

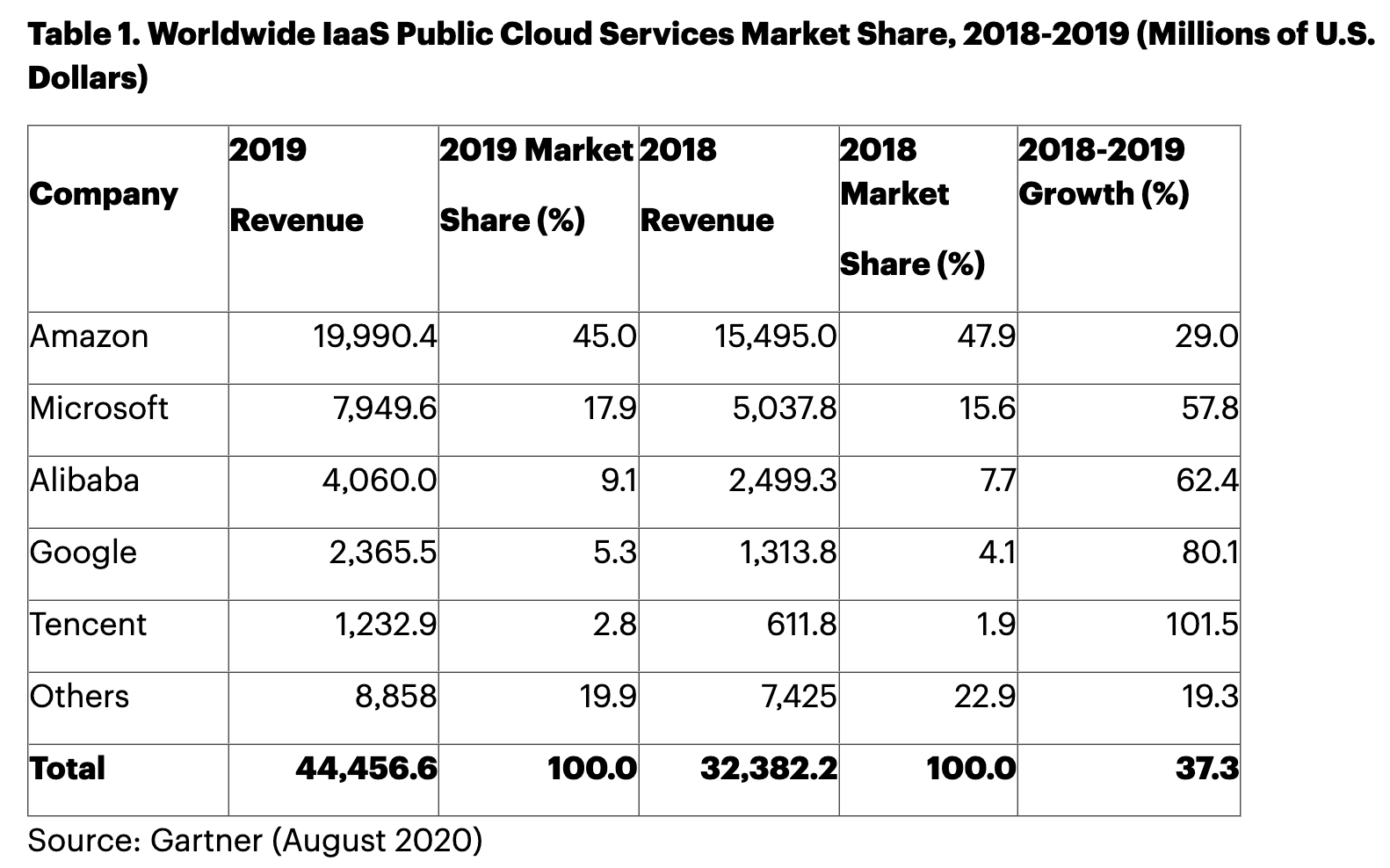

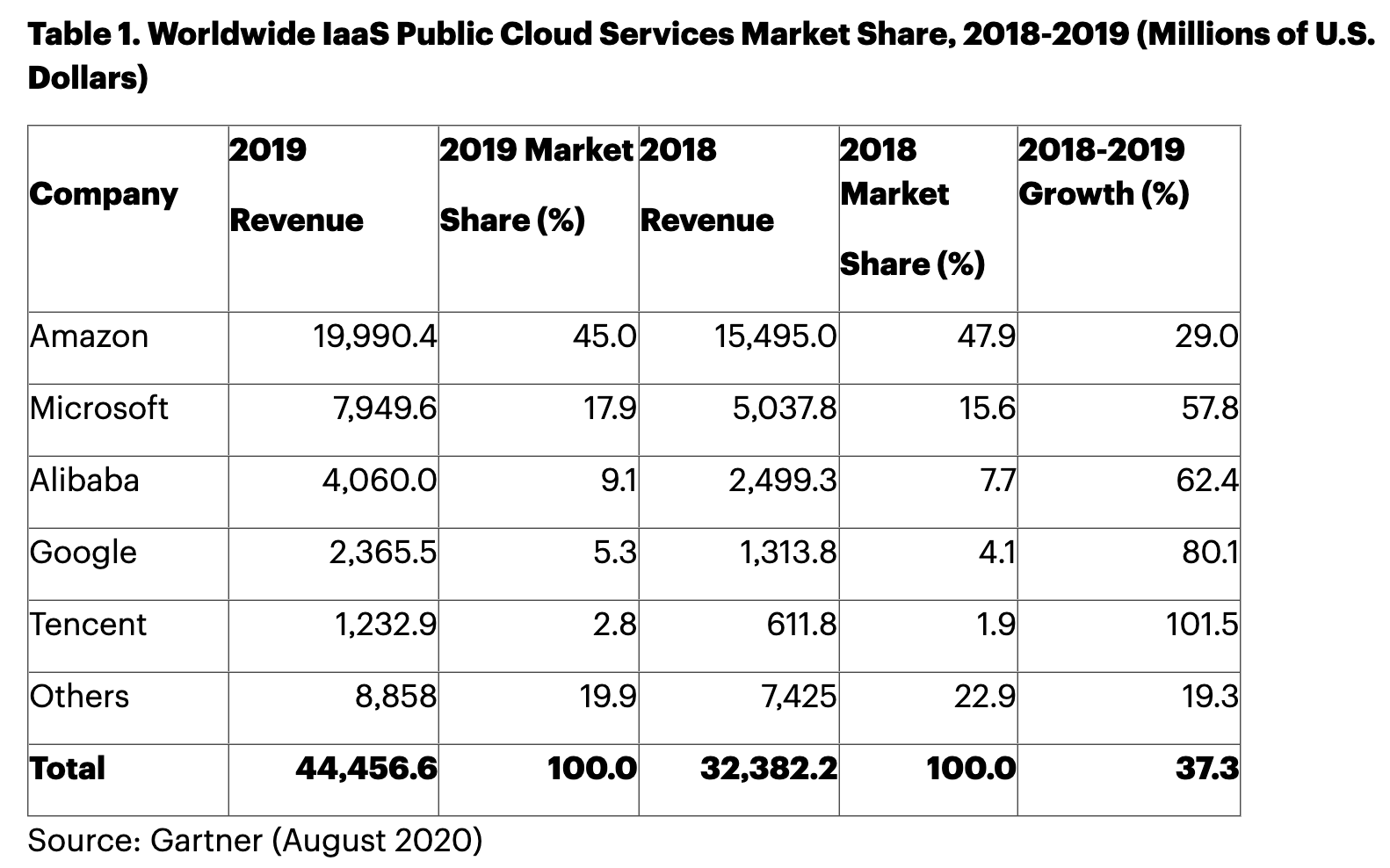

Based on Gartner’s new global cloud market share analysis released in August, the top five players are: AWS, Azure, Alibaba Cloud, GCP, Tencent.

Everyone is still trying to catch up to AWS. As for the brand-name laggards who didn’t make the top-five cut, namely Oracle and IBM, they urgently need to catch up, both by continuing to invest in building data centers and product R&D, as well as “stress testing” its product to differentiate.

What’s why Larry Ellison aggressively pursued Zoom as a customer (and succeeded) earlier this year when Zoom was going through hypergrowth (see “Why Zoom Chose Oracle”). IBM should have been in the picture as well, but is likely busy absorbing its massive acquisition of Red Hat that just closed last July.

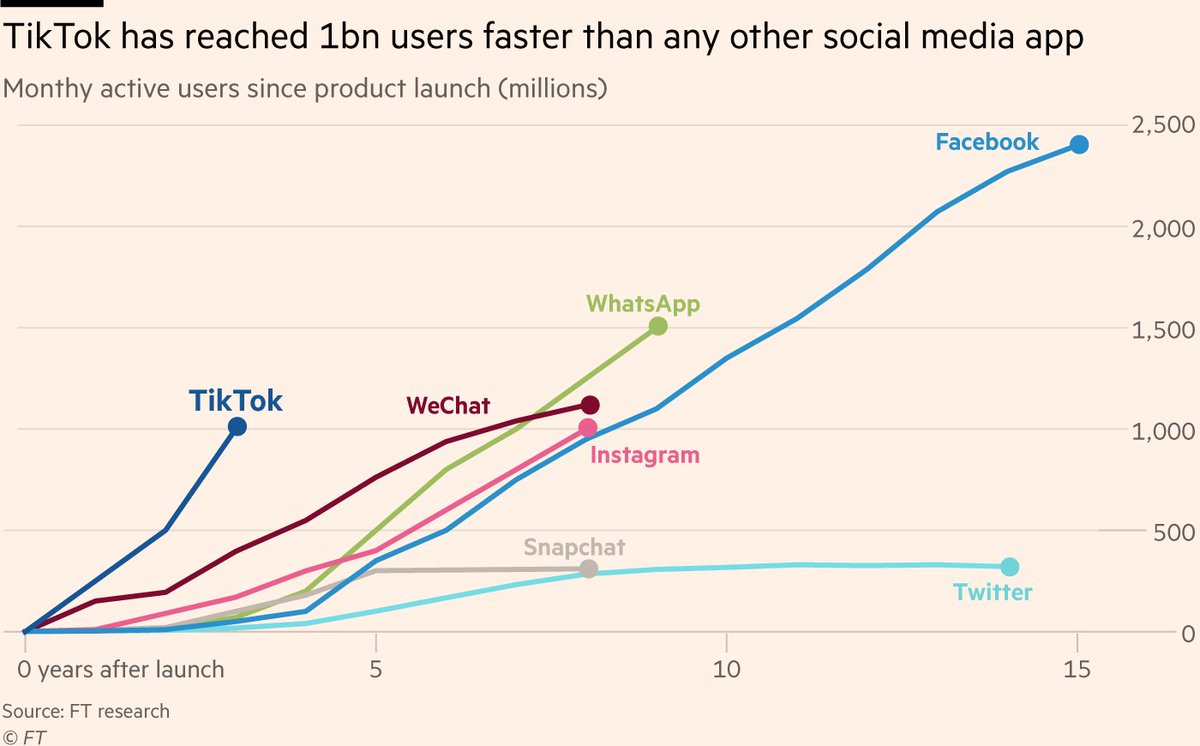

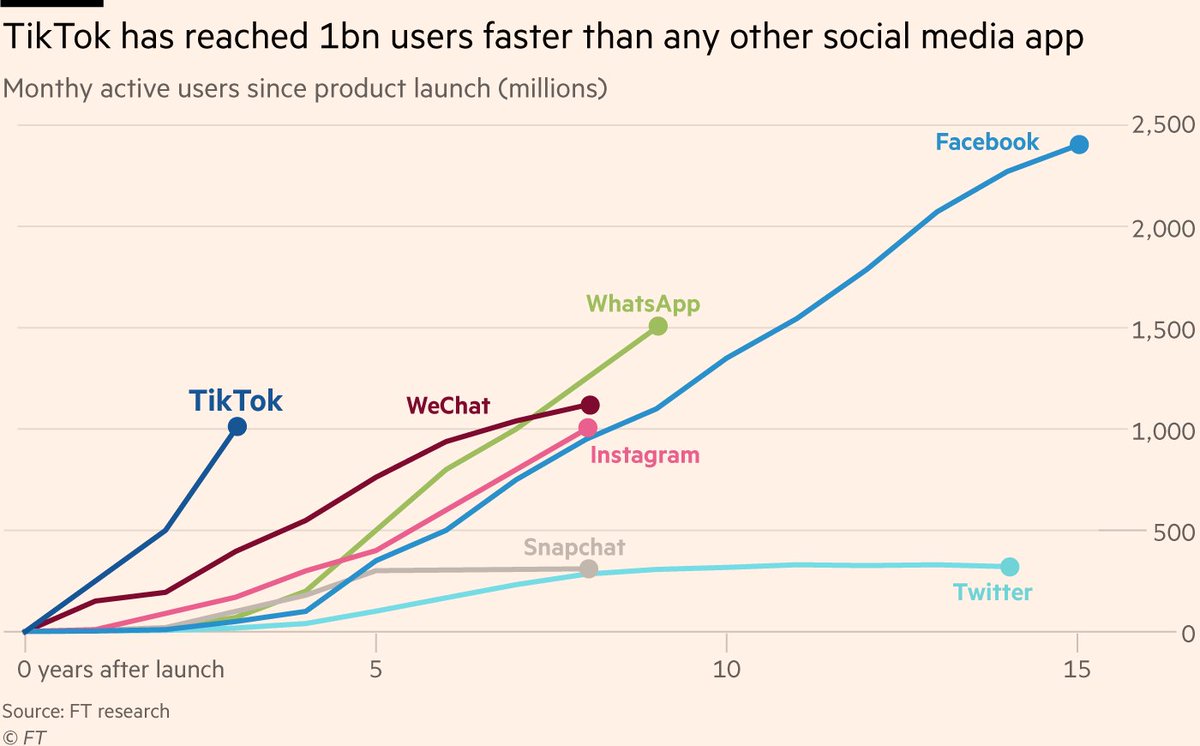

Having TikTok run on your cloud especially while it’s rapidly growing (100 million MAUs, 50 million DAUs, 800% MAU growth since January 2018 in the US), and run it well without downtime or performance degradation, is a legitimate accomplishment and extremely valuable for differentiation. After all, TikTok did reach 1 billion users faster than any social media app in history (even though it’s not really a social media app, more on that later).

E-Commerce

The e-commerce synergy with TikTok is weaker than the cloud one in the short-term, but will become increasingly important in the long-term. Douyin, the Chinese version of TikTok, already has many e-commerce capabilities like buying items directly from a video or livestream feed. These capabilities are becoming table stakes in the Chinese e-commerce space, but are quite novel in the US and Europe.

Large retailers are all trying to transition into e-commerce ASAP to not continue losing market share to Amazon, and hopefully surpass it one day with new ways to shop. From that angle, the Walmart alliance with Microsoft to bid on TikTok is very forward looking. Microsoft and Walmart already have a tight relationship on cloud, with a 5-year partnership inked in 2018. Walmart is about to launch its Amazon Prime competitor, Walmart+, on September 15, coincidentally (or not) on the same day as the US government deadline to sell (or ban) TikTok. While Walmart+ is still a nascent product, merging TikTok’s e-commerce potential with it, or even just creating the perception of that happening, will do wonders to Walmart’s reputation as becoming an innovative tech company.

That does beg the question: why wouldn’t Amazon try to buy TikTok too? The truth is: Amazon has already been working with TikTok to allow users to buy directly on Amazon, advertising, and even content for Amazon Fire TV. Some of those partnerships will likely continue regardless of who ends up owning TikTok. Sadly, buying TikTok outright is a fool’s errand due to the simple reality that Trump doesn’t like Amazon. His disdain towards Jeff Bezos is well-documented. AWS is still fighting for a piece of the Defense Department’s JEDI cloud contract with a pending lawsuit alleging political interference from the Trump White House. There are already too many insurmountable hurdles.

As with all things related to TikTok, politics has a way of intruding.

Users and Data

Given TikTok’s staggering growth and the staggering amount of data being collected from its user base, acquiring those users and their data is obviously valuable; no insight here. And depending on what you read, TikTok’s data collection practice is either “just as bad” as the likes of Facebook and Google, or demonstrably worse.

What is worth thinking about is whether the acquirer has a good enough reputation to be entrusted with that data, whether it can derive value from the data, and keep growing the product to get more data.

Both Microsoft+Walmart and Oracle have decent reputations when it comes to data governance largely because their core business is either enterprise software or brick and mortar retail, where collecting user data is not at the center of their business model. This characteristic also makes them more trustworthy when it comes to national security concerns related to TikTok’s data. The irony of this reputation is that it’s built from their very ignorance in operating a product like TikTok. While it’s helping with the acquisition and various regulatory and public relations hoops the transaction will need to jump through, it also makes TikTok’s future business value and growth more murky.

Microsoft has had a bit more experience with consumer applications via acquisitions than Oracle, with LinkedIn and GitHub. However, LinkedIn is a first-generation social media product used primarily for enterprise sales or recruiting, not entertainment. GitHub’s status as a social network of the world’s developers is accidental at best. TikTok is not even a social media platform; it’s an algorithm-driven entertainment platform. I frankly don’t find Microsoft’s “experience” that relevant to its ability to run TikTok well.

The value of data is also tightly connected to the AI algorithms that make use of it, which is TikTok’s core technology. Is TikTok’s data more valuable than its technology?

Core Technology

I’m going to go out on a limb and opine that TikTok’s core AI technology is not worth as much as its users and data. This is one of those “strong opinions, weakly held”, but here’s why I believe that’s the case.

The concept of “data density” is what determines a lot of the value in a technology business. In the cloud industry, convincing your prospective users to migrate and store their data in your cloud is the most important step in growing long-term customer value. That’s why cloud storage is cheap (or comes with steep discounts), but compute resources and networking bandwidths are not. In e-commerce, the accumulative data on your shoppers’ preferences, behaviors, and habits is much more useful than the actual value of the items they buy. Same for an ad-funded social network. Same for a self-driving car company, whose cars need to self-drive millions of miles -- a “data density” building exercise -- before reaching the necessary level of safety and stability.

With “data density”, whichever combination of Deep Learning AI algorithms or frameworks (many of which are open sourced and commoditized) you apply to the data, you’ll get some powerful results.

Without “data density”, the algorithms will not be able to live up to their full potential, regardless of how “smart” or optimized they are.

This is not to say that TikTok’s algorithms are not valuable. Of course they are. Otherwise, the Chinese regulators would not be revising its own technology “entity list” to add “data analytics-based personalized information push service technology” as a new item. Because of this addition, whoever buys TikTok may not get to have its powerful algorithms. That’s obviously not ideal for the acquirer, and may drive the eventual sale price down. But the acquirer will have the users and data -- the more valuable piece -- to rebuild the recommendation engine if it really wants to. Given its advances in AI and strong partnerships with organizations like OpenAI (creator of GPT-3), Microsoft is most likely to succeed in this regard. Oracle...much less so.

You may reasonably ask: Facebook and YouTube both have a boatload of user data. Why didn’t they build something like TikTok to compete head on?

Facebook is certainly trying, first with Lasso (shut down) and now with Instagram Reels. Its inability to compete with TikTok and its predecessor Musical.ly does confound me. My best guess is Facebook’s DNA is social, where incentivizing new users to “friend” others is at the core of its product stickiness and growth strategy. TikTok is fundamentally different. You don’t have to “friend” anyone, “connect” with anyone, or even “follow” anyone to get some entertainment out of TikTok. It’s not that social. Thus, incubating a TikTok out of Facebook requires some fundamental learning and unlearning, which is hard for a company of that size to do.

As for YouTube, it does have the world’s largest catalogue of user-generated videos backed by the world’s most advanced AI company, Google. In short: YouTube was dealt a great hand to be TikTok before TikTok. But that outfit appears to be focused on showing as many ads as possible these days, especially now that it's a separate line item in Alphabet’s earnings. As for innovation, well...YouTube circa 2015 looks pretty much the same as YouTube today.

Brand

A cool brand is extraordinarily valuable in the long run, but hard to quantify in the short run. TikTok is a cool brand -- a somewhat underlooked element of this whole transaction. It’s cool like Instagram, Snapchat, and Vine used to be cool.

Owning a cool brand can rejuvenate an old, not-so-cool company, which is a category that includes Microsoft, Walmart, and Oracle. (Although Microsoft has done an amazing job of rebuilding its coolness among developers by driving the popularity of the VSCode IDE, acquiring GitHub, and embracing open source -- a great story that I’ll write about on another day.)

All the possible acquirers could use a brand reboot. An effective image makeover could attract more talent, boost internal morale, and lead to more customers, so it’s worthwhile to pay a “cool premium”. How well it’ll work in the long run depends on how they will treat TikTok after the deal closes. I’m sure the boilerplate “TikTok will remain TikTok” line will be repeated on the public relations front, if only to not scare away TikTok’s core users, who skew young and have probably never used Windows, shopped much at a Supercenter, or even heard of Oracle RAC. But it’s a tough balance to maintain.

TikTok’s nemesis, Facebook, has had arguably the most experience in keeping a cool product untouched to maintain its coolness after acquisition. But even that could not last forever; a “From Facebook” splash was added to Instagram and Whatsapp last August and already appeared in Oculus.

Will “From Facebook” make Facebook itself more cool, or Instagram and Whatsapp less cool? It’s too early to tell. Generally though, I would not deem a product that has both teenagers and their grandmas cool, unless the grandma can do this.

Will we see a “Brought you by Microsoft”, “Powered by Oracle” or “Courtesy of Walmart” when loading TikTok one day? Your guess is as good as mine.

Company and People

The last dimension we will look at is “company and people”. Usually in an acquisition, even in a fire sale, there’s some value to acquiring the best technical talent and leadership who built the company, the so-called “acquihire”.

In TikTok’s case, this piece is probably the least valuable of all the five dimensions we’ve looked at. I mean no disrespect to the people who work at TikTok. By and large, ByteDance has a solid reputation for having cream of the crop engineering and product talent. Its US operation has been aggressively poaching top talent from the two meccas of tech talent, Google and Facebook. I presume the overall quality of talent is quite good.

But most of these personnel likely have not hit their strides to become productive. They came together during a year when TikTok was going through hypergrowth and when the proverbial geopolitical “shit” hit the fan. Assuming they haven’t quit, many of them not only needed to onboard properly in TikTok US, but also jell with their counterpart teams in China. Having run a much smaller cross-border team in the past, I know first-hand how difficult that “jelling” can be, even under the best circumstances.

All this chaos is happening while ByteDance is trying to increase its headcount from roughly 60,000 to 100,000 by the end of 2020, a hiring plan announced in March. To put this 40,000 person increase in perspective, Facebook’s entire headcount at the end of 2019 was about 45,000. ByteDance’s recruiting department is probably not going to hit its OKR this year.

As for leadership, TikTok’s shining white knight, Kevin Mayer, already quit. But he was always more of a “mercenary” than a “missionary” anyway. Whether it’s Microsoft+Walmart, Oracle, or another acquirer, the “global role [he] signed up for” has become obsolete.

While this analysis is by no means comprehensive, I hope it gives you a good overview of what TikTok’s worth, to whom, and why, from a pure business perspective.

Geopolitical concerns are permeating the tech and business worlds these days, so much so that they get over-indexed in our thinking sometimes. This is not to say that there aren’t real national security concerns with TikTok, but there is a regulatory framework to deal with them, properly and separately.

At the end of the day, technology decisions still have to make technological sense. Business decisions still have to make business sense. Interconnectedness is everywhere, but sometimes, it doesn’t need to be.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. New posts will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

TikTok为什么,又对谁,有什么价值?

毫无疑问,地缘政治是TikTok在美国未来命运的主要驱动力。但如果它真的被出售,这仍然是一个数十亿美元的交易,必须也要有些商业价值和意义。

我已经在围绕TikTok的各种政治和监管角度上写了不少文章,所以我在这里不再赘述那些观点(我倒是希望您能看看那些文章,了解下我的总体思路和观点)。在这篇文章里,我将集中讨论如何思考TikTok的商业价值,哪一部分对谁有价值,背后的原因又是什么,尤其是对于微软+沃尔玛和甲骨文,这两组最有可能买下TikTok的团队。

通常情况下,任何规模的收购都需要满足以下其中一个(但最好不止是一个)方面:

- 产品协同效应

- 用户和数据

- 核心技术

- 品牌

- 公司和员工

让我们分析一下TikTok在这几个方面的相对价值。

产品协同

云

整个全球云计算产业还比较年轻,增长迅速,因此所有主要云厂商都处于“抢地”模式,先抢占市场份额,以后在想怎么盈利。但这一格局也在向“差异化”方向过渡,每个云平台都在寻找“脱颖而出”的方式。虽然可以通过各种强势的营销手段去做差异化,但“脱颖而出”的最好方法就是展示自己的云能够比业界其他选择更好地处理哪些类型的技术负载。

这就是TikTok的用武之地。因为TikTok的产品特性,它有一套独特的工作负载:

- 存储和处理大量的视频;

- 以计算机视觉为基础的视觉检索;

- 直播;

- 持续运行各种人工智能算法,给不同用户看不同的视频和广告;

- (越来越多)直接在app里进行电商交易。

这也是为什么TikTok在美国使用AWS和GCP作为其两个云提供商,因为Snap用的也是这两家。作为一家“视觉通信”公司,Snap的技术负载特性是与TikTok最接近的,尽管它在人工智能、直播和电商方面都还远远落后。(Snap也在这两个云上花了很多钱,几个月前我在《AWS和GCP才是Snapchat增长的真正赢家》一文中做了深入分析。)

对于微软或甲骨文来说,收购TikTok再把它运行在自己的云平台上有助于和AWS和GCP相比时做差异化。这种差异化不仅仅是营销宣传部门的事,更是对基础工程团队的一种挑战和“压力测试”。这是微软和甲骨文都缺乏的一种压力测试,因为它们都一直是企业级软件公司,几乎没有或根本没有大规模运行 toC 应用程序的经验。两家公司都擅长“企业级”服务,但并不擅长“互联网级”的需求。而云客户买的就是能承受大规模工作负载压力的平台。

那怎么能看出哪家的云能承受什么样的“压力”呢?分析公司的其他核心业务以及运行那些业务所需的负载特性是很有帮助的。(前几个月我做了一套这种“压力测试”分析,看了几家最大的云平台:AWS、Azure、GCP、阿里云、IBM云、甲骨文云、腾讯云。)

根据Gartner今年8月发布的最新全球云市场份额分析,排名前五的是:AWS、Azure、阿里云、GCP、腾讯。

每家都在追AWS。至于没有进前五的大牌落后者,即甲骨文和IBM,它们迫切需要迎头赶上,既要继续投资建设数据中心和产品研发,又要对其产品进行“压力测试”,从以实现差异化。

这就是为什么Larry Ellison在今年早些时候,当Zoom正在经历超速增长时,努力(也成功)的说服Zoom成为自己的云客户(参见《Zoom为什么选择了Oracle》)。IBM其实也应该参与其中,但可能正忙于吸收去年7月才close的对Red Hat的大规模收购。

把TikTok运行在自己的云上,尤其是在它极速增长的时候(在美国有1亿MAU,5000万DAU,自2018年1月以来MAU增长了800%),并且在不停机,性能不下降的情况下成功运行它,是个不小的成就,也是在差异化上非常有价值的。毕竟,TikTok确实比历史上任何一个社交媒体app达到10亿用户量级的速度都要快(尽管它其实并不算是个社交媒体,稍后会深度分析这一点)。

电商业务

与云业务比,TikTok的电商协同效应目前相对弱一些,但长期看会变得越来越重要。抖音已经具备了很多电商功能,比如直接从视频或直播中购买商品。这些功能中国电商市场已经日益普遍,但在美国和欧洲还相当新颖。

大型零售商都在努力尽快过渡到电商领域,以避免市场份额继续输给亚马逊,也许还指望有一天以新的网购方式超越亚马逊。从这个角度来看,沃尔玛与微软结盟竞购TikTok还是有点前瞻性的。微软和沃尔玛在云计算领域已经有了紧密的合作关系,双方早在2018年就签署了长达5年的合作关系。沃尔玛即将于9月15日推出一款与Amazon Prime直接竞争的产品,Walmart+,这一天恰好是(或是故意的?)美国政府指令销售(或禁止)TikTok的最后期限的同一天。虽然Walmart+仍然是个新产品,但将TikTok的电商潜力与之相结合,或者起码创造这种未来的可能,都会对沃尔玛想打造成一家有创新的科技公司的声誉有好处。

这也引出了一个问题:为什么亚马逊不尝试收购TikTok?事实是,亚马逊已经与TikTok在合作,允许用户直接在亚马逊上购买东西,也与Amazon Fire TV做内容合作。不管谁最终拥有TikTok,一些合作关系可能都会继续下去。可惜,由于特朗普不喜欢亚马逊这一简单的现实,购买TikTok的这个想法无从起步。特朗普对Jeff Bezos的敌意已经众所周知。AWS仍在争取国防部JEDI云合同的一部分,诉讼未决,指控特朗普白宫对招标过程有政治干预。对亚马逊来说,已经有太多无法逾越的障碍了。

就像所有与TikTok有关的事情一样,政治考虑总是会介入其中。

用户和数据

鉴于TikTok的惊人增长和从其用户群中收集的惊人数据量,得到这些用户及其数据显然是有价值的;这没什么可说的。取决您看什么信息内容,TikTok的数据收集做法要么和Facebook,Google一样糟糕,要么明显更糟。

值得思考的是,收购方是否有足够好的声誉可以安全托管这些数据,同时是否能够从数据中获取价值,并不断让产品增长从而获得更多数据。

微软+沃尔玛和甲骨文在数据治理方面声誉都不错,这主要是因为它们的核心业务要么是企业软件,要么是实体零售。总之,收集用户数据并不是其商业模式的重点。这一特点也使它们在涉及TikTok数据管理的国家安全问题上更值得信赖。但有点讽刺的是,这个声誉是建立在它们对像TikTok这样的产品一无所知的基础上的。虽然这有助于收购以及最终交易需要跨越的各种监管和公关圈套,但这也让TikTok未来的商业价值和增长前景变得更加模糊。

与甲骨文相比,微软在 toC 产品方面的收购及运维经验更丰富一些。毕竟买了LinkedIn和GitHub。然而,LinkedIn是款第一代社交媒体产品,主要用于企业销售或招聘,而不是娱乐。GitHub作为全球开发者的社交网络的地位充其量也只是偶然发生的。而TikTok其实根本不是一个以社交驱动的产品。坦白地说,我并不认为微软的“经验”对它今后能不能好好做好TikTok有太大关系。

数据的价值也与需要它的人工智能算法紧密相连,这也就是TikTok的核心技术。TikTok的数据比它的技术更有价值吗?

核心技术

冒点风险的说,我觉得TikTok的核心AI技术的价值没有它的用户和数据价值高。这是个“强观点,微坚持”的一个想法,我是怎么想的呢?

“数据密度”这个概念可以决定许多科技产品的价值。在云计算行业里,迁移潜在用户的数据是最重要的一步。这就是为什么云存储很便宜(或者折扣很高),但计算资源和网络带宽却不便宜。在电商业务中,关于购物者偏好、行为和习惯的累积数据比他们具体购买的商品的价值要有用得多。对一个广告资助的社交网络也是一样。对于一家无人驾驶公司来说也是一样,他们的汽车需要无人驾驶数百万英里——这就是个累积“数据密度”的过程——才能达到必要的安全和稳定性。

有了“数据密度”,无论用哪些深度学习AI算法或框架(许多都已经开源而且广泛产品化)的组合,都能得到一些不错的结果。

如果没有“数据密度”,这些算法将无法充分发挥它们的潜力,无论它们有多“聪明”,有多优化。

这并不是说TikTok的AI技术和算法没有价值。它们当然有。否则,中国监管机构也不会修改自己的技术“实体清单”,将“基于数据分析的个性化信息推送服务技术”作为一个新项目。因为加了这一项,无论谁最后买了TikTok,都可能得不到它强大的AI算法。对买家来说,这当然不理想,可能也会压低最终的售价。但如果收购方真的愿意,还是可以在它将拥有更有价值的用户和数据上重建推荐引擎。鉴于其在AI方面的进度以及与OpenAI(GPT-3的创建者)等组织的紧密合作关系,微软是最有能力在这方面取得成功的。甲骨文…就不好说了。

您可能会想问:Facebook和YouTube都有大量的用户数据。为什么它们不建造类似TikTok的产品来直接竞争呢?

Facebook当然一直在尝试,先是Lasso(已经关了),现在是Instagram Reels。FB的各种产品无法与TikTok竞争,甚至与当年的Musical.ly竞争,还真是件让我困惑的事情。我最好的猜测是Facebook的DNA是社交,激励新用户与他人“交友”是其产品粘性和增长战略的核心。TikTok是根本不同的一种产品。你不必“加”任何人,“跟”任何人,就可以从TikTok里得到一些娱乐,与社交毫无关系。因此,从Facebook里孵化出一个TikTok需要一些根本的新学习和忘却,而对于这种规模的公司来说,还是很难做到的。

至于YouTube,它确实拥有世界上最大的用户生成视频目录,背后还有世界上最先进的AI公司谷歌撑腰。YouTube其实抓了一手好牌,完全应该是最先做成TikTok的。但看似YouTube现在唯一在乎的就是打广告赚钱,尤其是在谷歌季报里把YouTube单独列出来以后。至于创新嘛...2015年的YouTube和今天的YouTube看起来基本完全一样。

品牌

一个酷的品牌从长远来看是非常有价值的,但在短期内很难量化。TikTok是一个很酷的品牌,这一点在整个交易中却很少提到。它就像Instagram、Snapchat和Vine过去那样的酷。

拥有一个酷品牌可以让一个不那么酷的老公司焕发活力,这类公司里绝对包括微软、沃尔玛和甲骨文。(尽管微软通过推动VSCode IDE的流行,收购GitHub,并拥抱开源,在开发者群体里重建了它的形象,这个转型是个好故事,我会改天再继续分析。)

所有可能的买家都在某种程度上需要个酷品牌改造自己的形象。一个有效的形象改造可以吸引更多的人才、鼓舞内部士气和增加更多的客户,所以为“酷“多付点钱是值得的。但从长远来看,最终的效果如何还取决于交易结束后买家将如何对待TikTok。我相信 “TikTok会一直是TikTok” 这句“台词”将在公关层面不厌其烦的重复,哪怕只是为了不吓跑TikTok的核心用户:他们都偏年轻,可能从没用过Windows,也没在“沃尔玛超级中心” 买过多少东西,就更没听说过甲骨文RAC了。但这是一个很难维持的平衡。

TikTok的死敌,Facebook,在收购后保持酷产品不变的做法可以说是最有经验的了。但即便如此,显然也不可能永远持续下去。去年8月,Facebook宣布要在Instagram和Whatsapp主页上加一段标语:“来自Facebook”。同样的标语,在Oculus上也早就有了。

“来自Facebook”会让Facebook本身变得更酷,还是Instagram和Whatsapp变得越来越不酷?现在说还为时过早。不过,一般来说,我不会认为既有青少年又有他们爷爷奶奶呢的产品“酷”,除非奶奶能做这个。

会有一天,在启动TikTok的时候,大家会看到与微软,甲骨文,或沃尔玛的标语吗?谁现在都不知道。

公司和员工

最后一个维度是“公司和员工”。通常在收购中,即使是个大甩卖的情况下,能获得些优秀的技术人才和领导才能,都是有些价值,这就是所谓的“acquihire”。

看看TikTok的状况,“公司和员工”应该是我们分析的所有五个维度中最没有价值的一个。我无意冒犯在TikTok工作的员工。总的来说,字节跳动一直拥有能吸引一流人才的声誉。它在美国的业务也一直在从谷歌和Facebook这两家科技人才聚集的圣地努力挖人。我猜测团队的整体素质是相当不错的。

但是,这些人中的大多数都是在过去一年TikTok的飞速增长过程中加入的,可能都还没有开始发挥实力,就被卷入当前的地缘政治风波里了。假设都还没辞职,他们中的许多人不仅需要在美国TikTok框架里走正常的入职过程,还需要和中国的各层同事们开始磨合。以我在过去管理过一支规模小得多的跨境团队的经验来看,这个过程就算在最佳的环境下,都是很困难的。

混乱和风波在不断发生,而字节跳动在3月份宣布,要在2020年年底前将全球员工总数从大约6万人增加到10万人。把这4万人的增长换个角度看,Facebook在2019年底的所有工作人员人数也就才4.5万人。字节跳动的招聘部门今年的OKR应该是做不到了。

至于领导才能,TikTok的“白衣骑士” Kevin Mayer 已经不干了。但其实他一直是个“雇佣兵”而不是“传教士”。无论是微软+沃尔玛、甲骨文,还是另一个买家,都不需要 “他签约的全球级别角色”。

虽然这篇分析并不全面,但我希望它能从纯商业的角度较好地概述TikTok为什么,又对谁,有什么价值。

如今,地缘政治的干涉正渗透着科技和商业界的每一个角落,以至于我们的思维有时会过多的去想一些政治层面。这并不是说TikTok没有国家安全问题,但是是可以有一套适当和单独的监管框架来处理这些问题的。

归根结底,技术决策仍然必须具有技术意义。商业决策也仍然必须有商业意义。互联性无处不在,但在有些事情上并不需要如此。

如果您喜欢所读的内容,请用email订阅加入“互联”。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,与我交流互动!