Sneaking in big announcements on the eve of major holidays seems to be en vogue with regulators these days.

China’s State Administration for Market Regulations announced its antitrust investigation into Alibaba on Christmas Eve, so I spent Christmas Day writing “Alibaba and Antitrust with Chinese Characteristics.” Not to be outdone, the New York Stock Exchange announced its intention to delist three state-owned telecom companies -- China Telecom, China Mobile, and China Unicom Hong Kong Limited -- on New Year’s Eve to comply with a Trump executive order (EO).

As if the announcement itself wasn’t headline-grabbing enough, the NYSE canceled the delisting plan (apparently because it wasn’t sure if the three telcos fall into the EO’s scope) only to reverse the cancellation and put delisting back on track, after receiving “new specific guidance” from the Treasury Department that these telcos are indeed covered by the EO.

Assuming nothing else happens, trading of these three companies will be suspended by 4 a.m. ET on Monday, January 11, 2021. Let’s dive into what this delisting means to the companies themselves and broadly to American’s future China policy.

Minimal Damage

In terms of business operations and financial impact, the real damage will be minimal. As the China Securities Regulatory Commission pointed out emphatically via the Global Times, the combined value of these three telcos’ American Depositary Receipts (ADRs) listed on the NYSE is worth about $3 billion. Their combined market cap, on the other hand, is about $145 billion, so exposure to the US capital market is only about 2%.

Furthermore, these three telcos are the only US-listed companies on the US Defense Department’s so-called “Communist Chinese military companies” list. So as far as using delisting as a tool to implement Trump’s EO, this is a one-time action.

Given such a tiny exposure, why were these three companies listed on the NYSE in the first place? As it turns out, they’ve been on the exchange for a long time, back when China’s own capital market was a fledgling version of its current self. Thus, there was a time when Chinese telcos, plus other state-owned enterprises, did need access to American capital to grow as companies. China Mobile, the largest of three, began trading on the NYSE in November 1997. China Unicom and China Telecom started trading in July 2000 and November 2002, respectively. To put those dates in context, the Shenzhen Stock Exchange and the current iteration of the Shanghai Stock Exchange weren’t founded until 1990, and Hong Kong only became a special administrative region in July 1997. Somewhat recent events that can feel like ancient history.

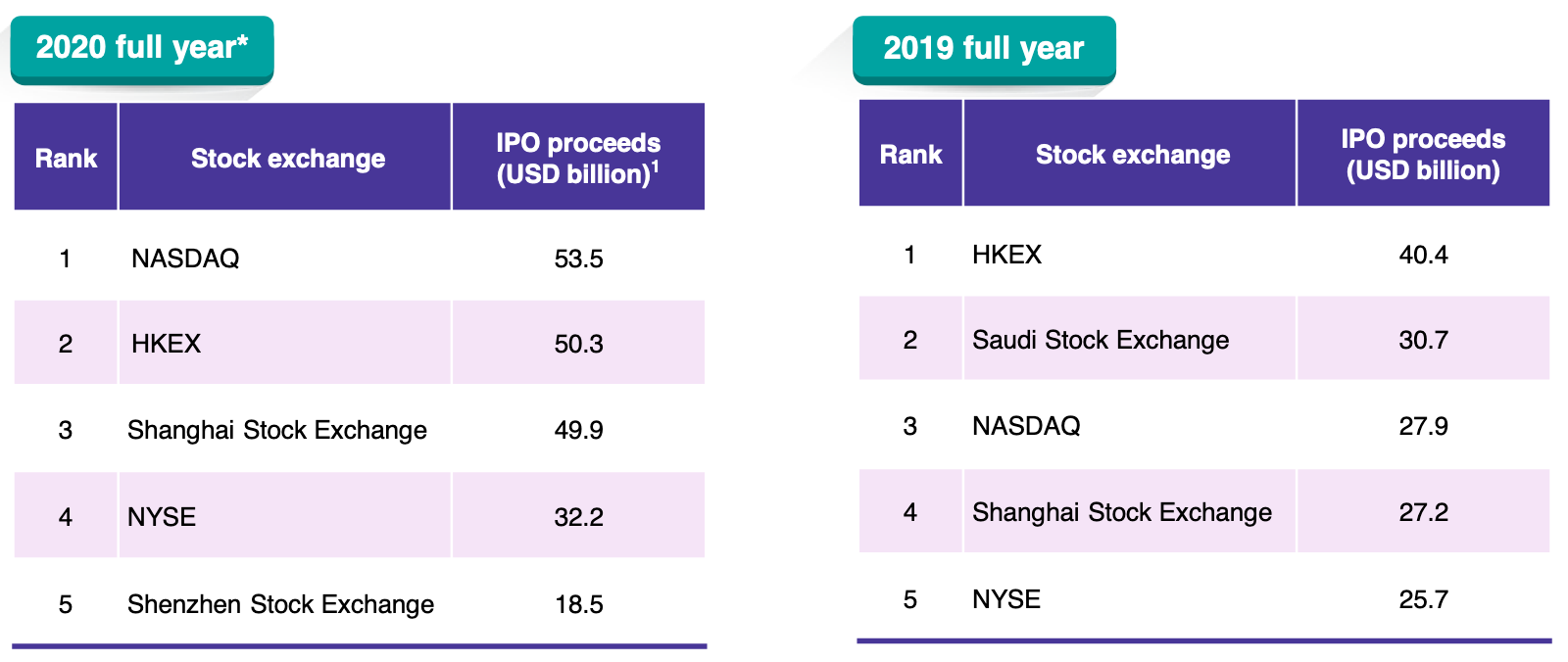

Of course, the stock exchanges in Hong Kong, Shanghai, and Shenzhen have all grown by leaps and bounds since then. Based on this report by KPMG on IPOs and capital markets, the Hong Kong and Shanghai stock exchanges have been ranked top 5 in the world by amount of money raised from IPOs in the last two years. Shenzhen was top five in 2020. The Saudi stock exchange only made the cut in 2019 because of that one-time, massive IPO by Aramco.

Given the increasing fluidity of different capital markets, American funds that want to continue owning shares of Chinese companies can simply dump the ADRs listed on Wall Street and buy shares of the same companies being traded in Hong Kong or Shanghai -- inconvenient but not difficult. Last year, some funds that wanted to continue owning shares of companies like Alibaba have swapped New York-listed shares for Hong Kong-listed ones, to hedge against future delisting.

The degree to which this delisting will reduce American money from investing in Chinese companies that may be bad actors -- the stated goal of the EO -- will be minimal. So will the damage being done to these companies’ balance sheets and business operations, almost all of which happen inside China.

Nevertheless, we shouldn’t take this delisting lightly; it’s still an important action because of its symbolism and timing.

Lame Duck Trapdoor

No Chinese company has ever been forced by policy to delist from an American stock exchange, though companies, like SMIC and 58.com, have delisted voluntarily to either avoid tougher regulations or just to boost its valuation in a more friendly market. Thus, this mandatory delisting by the NYSE symbolizes yet another new level of hostility between the US and China. It’s also an action that’s difficult for the Chinese government to respond (or retaliate) proportionally. While the Ministry of Commerce has vowed “to take necessary measures to protect Chinese enterprises' legitimate rights and interests”, what can actually be done is unclear. Few American companies are listed on any Chinese or Hong Kong stock exchanges, so a similar delisting action would not work. It’s possible that the “Unreliable Entity List” (UEL), a new policy tool introduced by the Ministry last year, will be used in some way to facilitate these “necessary measures.” Which American company gets “listed” so there’s some level of response, but not too much, similar to the minimal damage done to the three Chinese telcos, will be a tricky dance move to finesse. (If the UEL is used, my current prediction is Cisco, whose revenue is already falling sharply in China, while its products and services can be sufficiently replaced by Huawei’s.)

Beyond the symbolic tit-for-tat, the timing of this delisting, which occurred during Trump’s “lame duck” period, further corners the options available to the incoming Biden administration. When the Holding Foreign Companies Accountable Act (HFCAA) was poised to pass Congress back in November and December, Trump’s EO, signed during the week after Election Day when it was clear that he would not be re-elected, is somewhat redundant.

The HFCAA mandates that all foreign companies traded on an American stock exchange abide by the accounting standards set forth by the SEC’s Public Company Accounting Oversight Board -- the auditor of the auditors. As the HFCAA gets implemented, chances are the three Chinese telcos (and likely a handful of other companies) will have to delist anyway. And to be clear, I support the spirit of the HFCAA and believe the same accounting standard should be applied equally across the board, so much so that I’ve advocated for Huawei to go public in the US, if it is indeed a good actor with nothing to hide.

The Holding Foreign Companies Accountable Act is now law.

— Kevin Xu (@kevinsxu) January 5, 2021

If Huawei is a good actor and has nothing to hide, the smartest and boldest thing it could do is IPO in New York.https://t.co/8SiA5JE8TX

So why did Trump sign his executive order to accelerate the pace of delisting in his waning days as president?

It’s another way to rack up more “Fuck China” accomplishments. Just signing the HFCAA into law wouldn’t score as many points. The law passed by unanimous consent in both the House and the Senate, meaning every member wanted to vote “yes” so there was no point in even calling for a formal vote procedure. Such level of agreement only happens when Congress names a post office. If everyone agrees, Trump’s own agreement does not stand out. By doing more, however unnecessary, and being the undisputedly toughest American politician on China, Trump can either empower his own position if a 2024 presidential run is in sight, or strengthen his new role as the “kingmaker” to the Republican Party’s new generation of ambitious, opportunistic China hawks, like Senators Hawley, Rubio, Cruz, and Cotton.

Unlike congressional legislations, EOs can be easily revoked by a new president, but seems unlikely to happen. New lame duck EOs on China, like delisting and the recent Chinese apps transaction ban (another action with minimal damage but maximal symbolism), narrow the Biden administration’s policy options further. Any semblance of reasonable dealing or engagement with China will be attacked, and there’s no congressional gridlock to point to, because everyone in Congress already despises China. There’s no other direction to go but tougher, even though the number of policy actions is dwindling, so the “surface area” of toughness must expand.

We may be seeing this “expansion” already, with the incoming National Security Advisor, Jake Sullivan, tweeting to raise concerns about the China-EU investment agreement signed just before 2020 expired.

The Biden-Harris administration would welcome early consultations with our European partners on our common concerns about China's economic practices. https://t.co/J4LVEZhEld

— Jake Sullivan (@jakejsullivan) December 22, 2020

At least two of the companies currently on the “Communist Chinese military companies” list -- China State Construction and Panda Electronics -- are listed on the Frankfurt stock exchange. Will we see the Biden administration pressure European allies to delist Chinese companies on their own exchanges as well?

To be clear, I fully expect the Biden administration to be more competent policymakers and promulgators in all areas compared to the Trump administration. For one, they would not make the amateur mistake of issuing unclear guidance around what is and isn’t covered in an executive order.

But for anyone hoping for a more cooperative and more nuanced set of China policies in the next four years, the probability of that happening has always been low. And this lame duck delisting just lower it further.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

跛脚鸭退市

在重大节日前夕偷偷发布重磅监管新闻,在最近似乎很时髦。

中国国家市场监管总局在平安夜宣布对阿里巴巴进行反垄断调查,促使我在圣诞节当天写了一篇《阿里巴巴与有中国特色的反垄断》。不甘示弱,纽约证券交易所在新年夜也做了条官宣,逼三家国有电信公司退市,分别是中国电信、中国移动和中国联通香港有限公司,以履行特朗普政府的一条行政命令(executive order,EO)。

仿佛消息本身头条价值还不够,纽交所又取消了退市计划(显然是因为不确定这三家电信是否落入EO的范围内),但在收到财政部的 "新的具体指导意见" 后,又出尔反尔,重新启动了退市的安排。

假设没有新变动,这三家公司的交易将在美国东部时间2021年1月11日星期一凌晨4点暂停。那我们就深入探讨一下这次退市对公司本身以及对美国未来的中国政策意味着什么吧。

皮毛损伤

从业务经营和财务影响来看,退市实际损失微乎其微。正如中国证监会通过《环球时报》指出的,这三家电信公司在纽交所上市的美国存托凭证(ADR)合计价值约30亿美元,而它们的市值总和约为1450亿美元,因此在美国资本市场的暴露仅有2%左右。

此外,这三家电信公司也是美国国防部所谓的 "中共军工企业" 名单中唯一在美国上市的公司。所以,用退市这个工具来履行特朗普的EO,也只能用一次。

既然暴露如此之小,这三家公司当初又为什么要在纽交所上市呢?其实它们已经在纽交所上市有一阵子了,早在中国自己的资本市场还未成熟的时候。因此,当时的中国电信公司,以及其他国有企业,可能确实需要美国资本来继续发展。三家公司中最大的中国移动是1997年11月开始在纽交所交易。中国联通和中国电信分别于2000年7月和2002年11月开始交易。把这几个日期放宽点看,深圳证券交易所和当前版本的上海证券交易所都是在1990年才成立的,而香港在1997年7月才回归成为特别行政区。其实都是最近的事,虽然感觉像古老历史。

当然,现在的香港、上海、深圳证券交易所今非昔比。据毕马威的这份关于IPO和资本市场的报告,在过去两年中,香港和上海证券交易所的IPO募集资金排名全球前五。2020年,深圳也名列前五。沙特证券交易所在2019年能入前五是因为Aramco的一次性大规模IPO。

鉴于不同资本市场的流动性越来越流畅,想要继续持有中国公司股票的美国基金抛掉在华尔街上市的美国存托凭证,买入在香港或上海交易的同一家公司的股票即可。虽然有点不方便,但也并不困难。去年,一些想继续持有阿里巴巴等公司股票的基金已经把纽约交易的股票换成了香港交易的股票,以对冲未来可能发生的退市。

这次退市对减少美国资金投资于可能“不好”的中国公司的影响(也是此EO既定的政策目标)将是微乎其微的。对这些公司的资产负债表和业务运营造成的损伤也是如此,因为业务几乎都在中国境内。

尽管如此,我们不应该轻视这次退市决策,因为它本身的象征意义和发生的时间都有长远影响。

跛脚鸭陷阱门

从来没有任何一家中国公司被政策强制而从美国证券交易所退市,尽管有像中芯国际和58同城这些公司自愿退市(一是避免更严格的监管,二可能只是为了去一个更友好的市场提高估值)。因此,纽交所此次强制退市象征着中美之间的敌意又达到了新高。中国政府也难以按比例作出回应(或报复)。虽然商务部誓言 "采取必要措施保护中国企业的合法权益",但具体能做什么还不清楚。很少有美国公司在中国或香港的证券交易所上市,所以类似的退市做法行不通。还有一个工具就是商务部去年出炉的 "不可靠实体名单",可以用来执行某种 "必要措施"。找到哪家美国公司列入名单,既能达到某种程度的回应,效果又不会过重,类似这三家电信公司被迫退市的影响,将是个高难度动作。(如果采用“不可靠实体名单"这个工具,我目前的预测是思科,其在中国的收入已经急剧下降,而其产品和服务可以充分被华为替代。)

除了象征性的“针锋相对”之外,这次退市发生在特朗普的 "跛脚鸭 "时期,也进一步减少了即将上任的拜登政府的政策选择。当《外国公司责任法案》(HFCAA)早在11月和12月就准备顺利通过国会时,特朗普也知道自己连任无望,但还是在大选日之后的一周签署了EO,其实有些多余。

根据HFCAA的规定,所有在美国上市的外国公司都必须遵守美国证券交易委员会(SEC)的上市公司会计监督委员会——也就是审计师的审计机构——规定的会计准则。随着HFCAA的实施,这次被影响的三家中国电信公司(很可能还包括其他一些公司)都可能不得不退市。要说明的是,我大体支持HFCAA,认为应该一视同仁地使用同样的会计准则监管所有上市公司,以至于我曾经主张华为在美国上市,如果它的确是一家毫无隐瞒的好公司。

The Holding Foreign Companies Accountable Act is now law.

— Kevin Xu (@kevinsxu) January 5, 2021

If Huawei is a good actor and has nothing to hide, the smartest and boldest thing it could do is IPO in New York.https://t.co/8SiA5JE8TX

那么特朗普为什么还要在即将下台的这最后几天,加快退市步伐呢?

这是另一种积累更多 "Fuck China" 政绩的方式。仅仅签署HFCAA成为法律并不能得多少分,因为该法律在参众两院以“一致同意”的方式通过,也就是每位立法议员都想投 "赞成票",所以都没有必要走正式投票和数票的过程。在美国国会能达到这么高度一致的提议,也只有在命名邮局这种不疼不痒的小事时才会发生了。如果大家都同意,特朗普自己的支持也就并不突出了。附加上个EO,无论多么没有必要,特朗普能把自己打造成无可争议的美国对华最强硬的政治人物,即对2024年如果再次竞选总统有帮助,也可以加强自己退位后的地位,作为 "王者"的新角色来影响共和党内的新一代野心勃勃、机会主义的中国鹰派,如参议员Hawley、Cruz、Rubio、Cotton。

与国会立法不同,EO很容易就可以被新总统撤销,但似乎可能性不大。最近针对中国的“跛脚鸭EO”,如退市和对中国科技公司的app交易的禁令(另一个损害虽小但象征意义很大的举动),进一步减少了拜登政府的政策选择。任何半点与中国的理智交易或接触都会受到攻击,也不能指望国会僵局背锅,因为国会所有成员都不喜欢中国。即使具体的政策工具越来越少,拜登政府除了走更加强硬的道路,没有其他方向可走,所以强硬的 "面积" 也必须扩大。

我们可能已经看到了些 "扩大" 的迹象。即将上任的新国家安全顾问 Jake Sullivan 在推特上对2020年底签署的中欧投资协议提出了质疑和担忧:

The Biden-Harris administration would welcome early consultations with our European partners on our common concerns about China's economic practices. https://t.co/J4LVEZhEld

— Jake Sullivan (@jakejsullivan) December 22, 2020

目前在 "中共军工企业" 名单中,至少有两家公司 -- 中国国建和熊猫电子 -- 在法兰克福证券交易所上市。是否会看到拜登政府向欧洲盟友施压,要求它们也逼着中国公司从自己的交易所退市呢?

与特朗普政府相比,我相信拜登政府在各个方面的政策管理、制定和执行能力都会更称职。他们起码不会犯一些幼稚外行的错误,连EO涵盖什么,不涵盖什么这种基本指令都传达不好。

但对期望未来四年会有一套更倾向于合作、更细致微妙的对华政策的人们来说,如愿的概率一直很低。而这次跛脚鸭退市,进一步降低了这个概率。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,和我交流互动!