The comically embarrassing timing between the final passage of the CHIPS and Science Act and Intel’s disastrous quarterly earnings, both occurring on the same day last week, elucidated one hard truth: Congress may be barking up the wrong tree.

Many have assumed that Intel – America’s semiconductor darling – just needs a new CEO, some extra incentives, and more favorable policies to regain its mojo, get back on top, and reverse America’s downward trajectory in losing its semiconductor manufacturing capacities.

Intel did get a new CEO in Pat Gelsinger in 2021. It will get some billions worth of taxpayer dollars out of CHIPS, as well as friendly local policies from states like Ohio – eagerly awaiting a new Intel foundry to be built there. But as Intel’s earnings revealed, the company’s core is rotting so precipitously that passing 10 more CHIPS Acts won’t revive it.

For analysis of Intel’s woe, I recommend reading two semiconductor-focused newsletters – Dylan Patel’s SemiAnalysis and Doug’s Fabricated Knowledge. I won’t pile on here. Instead, given Intel’s problems, to which companies should the CHIPS Act incentives go, so it is money well spent?

My proposal: the South Korean tech giants, Samsung and SK Hynix.

Samsung and SK Hynix

Even though Taiwan and TSMC get more media attention, due to its position as a geopolitical hotspot, South Korea has been a global leader in semiconductor manufacturing for decades. When Morris Chang, TSMC’s founder and ex-CEO, gave a wide ranging speech on the state of the global semiconductor landscape, he explicitly called out South Korea as a fierce competitor to Taiwan, while being dismissive of both the US and China.

(To read the English translation of Morris Chang’s speech, see “Morris Chang’s Last Speech” (premium content))

Samsung and SK Hynix are among the top four chip manufacturers globally. (The other two are Intel and TSMC.) Both companies appear to be better run and better capitalized than Intel. And both have already made successful investments in the US with plans to invest more – in fact, materially more than what is appropriated the CHIPS Act.

Samsung and SK Hynix are executing well, eager to pour money into America, and, frankly speaking, safer bets than Intel. Let’s look at each company’s footprint and plans:

Samsung: While known to most American consumers for its bendable smartphones or Smart TV, Samsung began building its first “Made in USA” semiconductor fab in Austin, Texas, in 1996. Since then, Samsung increased its Austin plant’s capacity twice in 2007 and 2017.

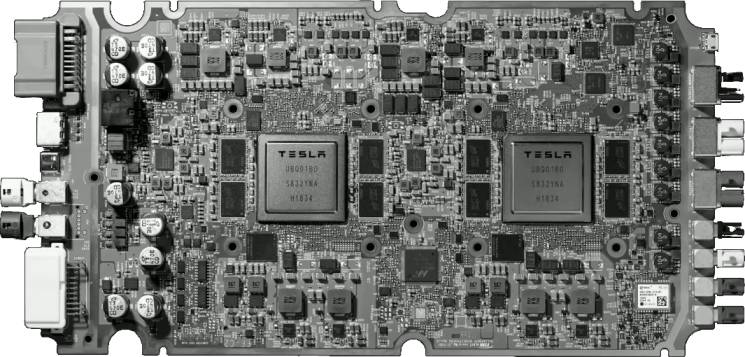

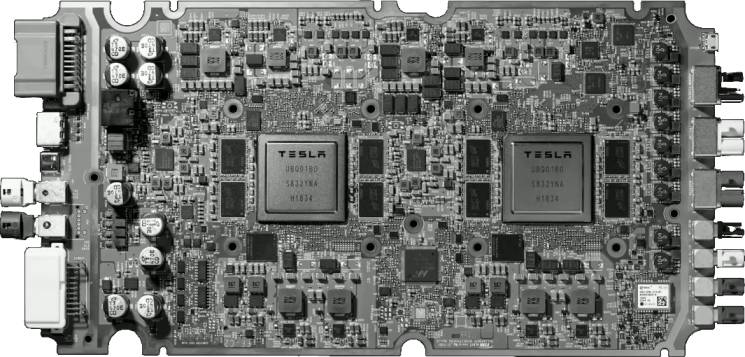

Samsung’s Austin fab primarily produces logic chips in the 14nm and 28nm/32nm range – as in, it does not house the most cutting-edge technologies capable of producing chips as small as 5nm or 3nm. That being said, this Samsung facility serves some marquee customers, most notably Tesla. It has been making Tesla’s all-important Full Self-Driving chip, literally the heart and brain of Tesla’s autonomous driving, since 2017 by using its 14nm technology.

With some successful experience in the Lone Star state, Samsung announced an additional $17 billion in investment late last year to build another fab in Taylor, Texas – a town 40-minutes outside of Austin – to expand its logic chips making capacity and double-down on its Texas ecosystem of suppliers and partners.

Samsung’s success, technology, and commitment in the US is arguably comparable to Intel’s, despite Intel having “home turf advantage”. Among all of Intel’s US-based fabs, only the one based in Arizona has 14nm capabilities. Globally, Samsung overtook Intel as the #1 chip maker by revenue earlier this year.

SK Hynix: I bet few in America have ever heard of SK Hynix, or its corporate parent SK Group. Yet, it is the world’s 2nd largest memory chip maker. (The largest is Samsung.) SK Group, this classic South Korean “chaebol”, has been making big moves in America lately.

Two days before Intel’s disastrous earnings call, SK Group’s Chairman Chey Tae-won (he goes by “Tony”) made a White House visit to announce his plan of investing $22 billion in America across the semiconductor, green energy, and biotech industries. Because President Biden was still in quarantine from contracting Covid, the meeting ended up being a glorified Zoom call with Chey in the Roosevelt Room and Biden in the Residence.

This $22 billion is part of the $52 billion investment that SK plans to pour into the US by 2030, which Chey announced last year. The semiconductor portion is about $15 billion, spanning R&D programs, materials, and an advanced packaging and testing facility. (The other portion is going into building batteries, EV charging stations, and other green business projects.)

Interestingly, Intel sold a big chunk of its own memory chip business to SK Hynix worth $9 billion. Effectively, SK Hynix already owns a piece of what was previously Intel. A part of that “piece” is Intel’s last manufacturing facility in China, based in the northeastern port city of Dalian. One of Intel’s last remaining memory chip products, Optane, was officially shut down last week with a $559 million write-off, presumably so it can focus on its sagging logic chip business to compete with Samsung and TSMC.

Intel’s is shrinking, while SK is expanding at its expense.

Piggyback Off Of South Korea

Seeing how Samsung and SK have already committed a combined $32 billion to build up America’s semiconductor capabilities, how much is the CHIPS Act bringing to the table? The devil is always in the details, especially in a congressional funding package.

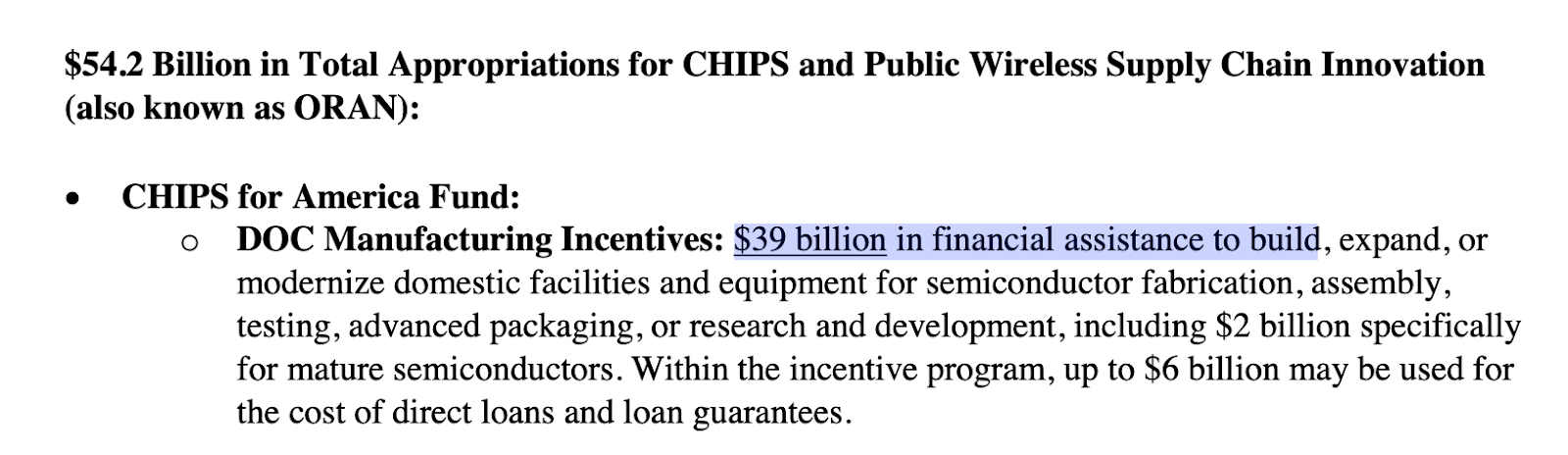

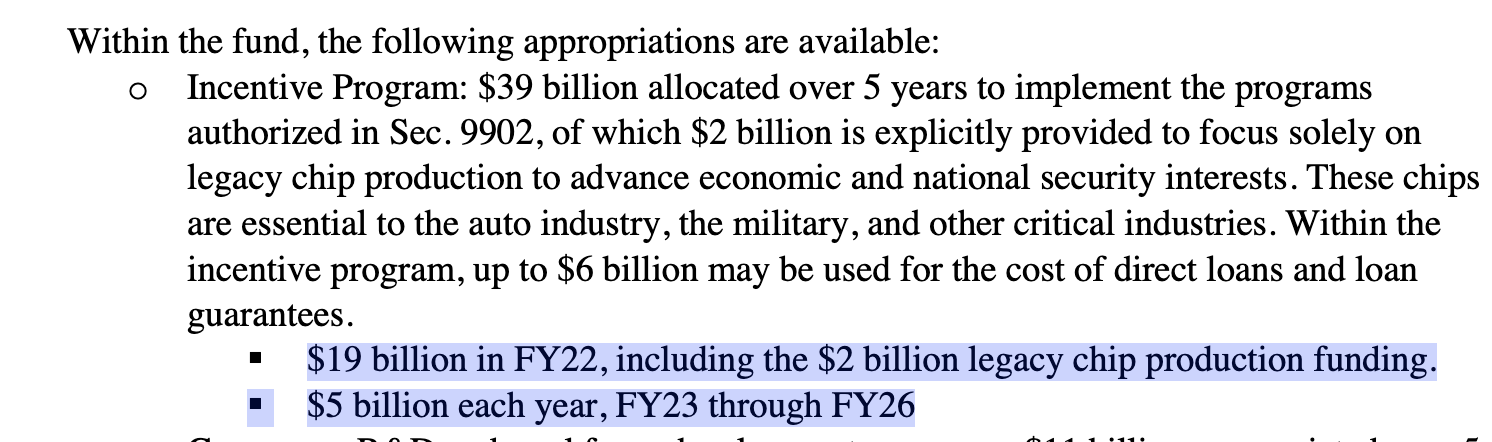

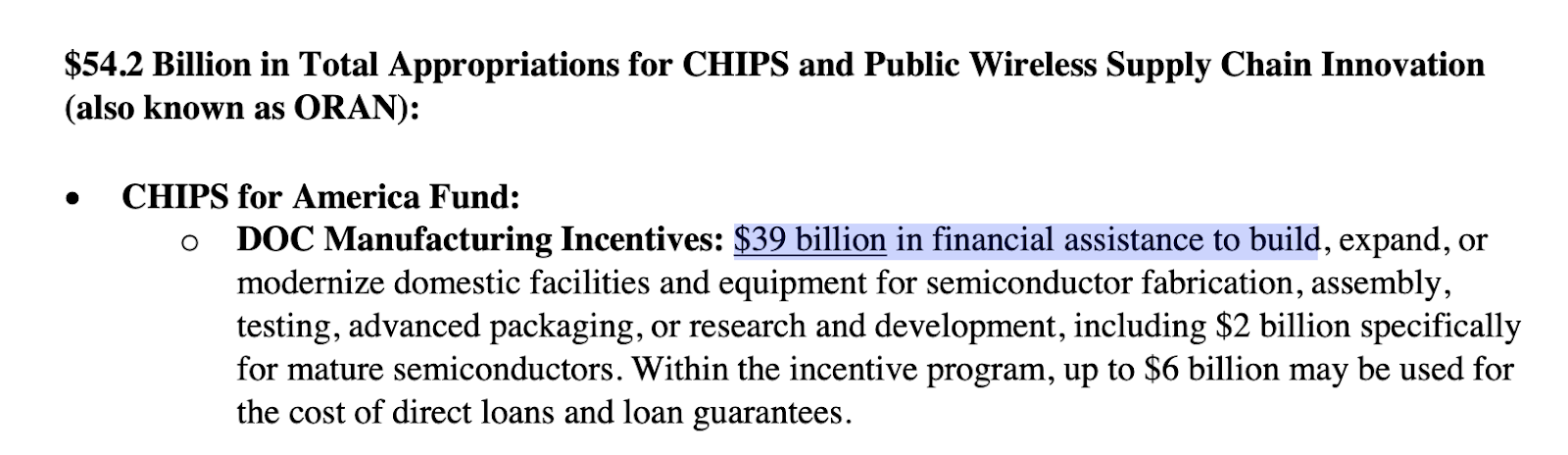

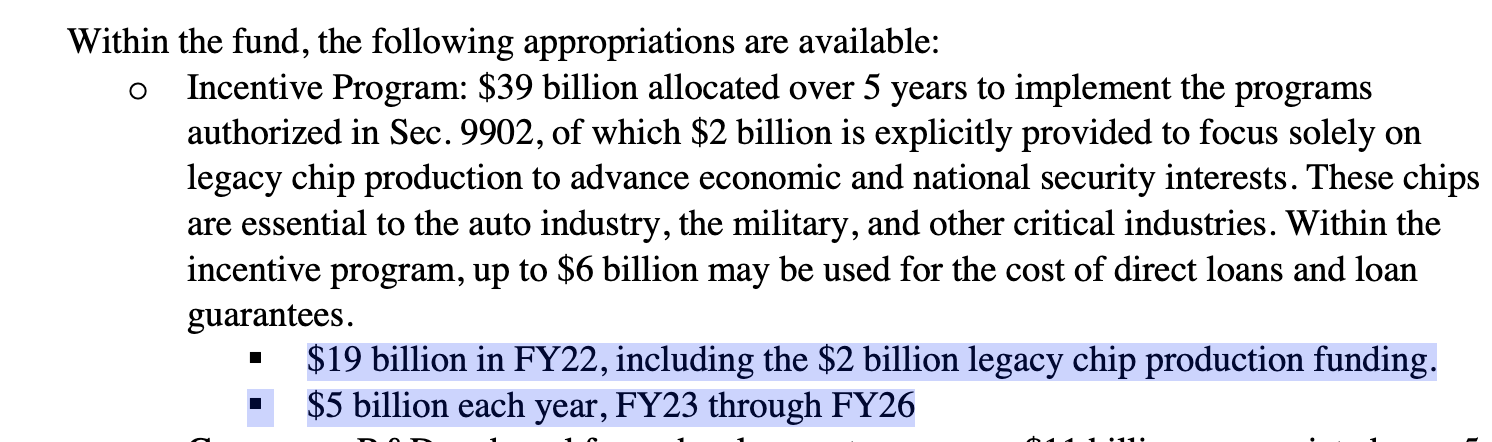

While the headline number that often gets reported is $52 billion, money appropriated from the CHIPS Act that will directly contribute to either building more semiconductor fabs or training more workers to operate those fabs is actually $39.2 billion.

Having spent some time reading the legislation’s fine print, I have pasted screenshots of the relevant parts, which you can read here and here.

Out of the $39 billion “Manufacturing Incentives”, only $19 billion is allowed to be spent this year. The remaining $20 billion must be split into $5 billion per year chunks to be spent in the following four years. (Talk about micromanagement!) Meanwhile, the Commerce Department, which is in charge of allocating this money, can charge up to 2% per fiscal year off of the larger base of $50 billion to hire people, find office space, buy computers, etc. to do the work – a $1 billion per year administrative budget! (If you are an investor, this is basically a 2% management fee for the lifetime of this “$50 billion taxpayer fund” without “carried interest” for the American people.) See more screenshots of fine prints below.

There are already serious and legitimate concerns being raised about the implementation of the CHIPS Act. Some people are worried that the money appropriated (whether you think it is $52 billion or $39.2 billion) is a drop in the bucket. Compared to the commitments of the two South Korean tech giants, Congress looks kind of cheap. Others are worried that these incentives will be misused by companies to do share buyback or fund dividends to shareholders, not build factories. This worry was fanned by Intel’s own CEO and CFO in a “shooting yourself in the foot” moment during its earnings call last week, simultaneously announcing less capital expenditure (to build fabs), while remaining committed to increasing dividend over time. To quell this worry, the Commerce Department had to issue a late Friday statement stating it will limit the size of CHIPS Act incentives to “no larger than is necessary” – whatever “necessary” means.

Zooming out, it’s rather clear that America is relatively immature in designing, funding, and executing an industrial policy from the top-down to boost a sagging but important sector. In a previous post, “Can the US ‘Out China’ China?” I called out this problem of America simply lacking “industrial planning muscle”, which it either never had or hasn’t exercised in a while. The CHIPS Act may be America’s first serious “workout”, as it steps into a “trial and error” phase of industrial policy. As Danny Crichton articulated in the Lux Capital “Securities” newsletter:

“Trying and failing is the only way America will learn how to strategize and salvage its industrial base.”

And while America tries to figure out this “industrial policy thing”, it would be smart to simply piggyback off of the successes and experiences of companies who have been the products of an ally country, say South Korea, who is actually good at executing industrial policies.

As Americans, we want Intel to do well, and we need Intel to do well, so there is a true American “national champion” in the semiconductor space. But until that happens, there is no shame in free-riding off of our South Korean friends for a while, channeling tax incentives to Samsung and SK, and not wasting it on Intel.

美国《芯片法案》拨款的最佳选择应该是韩国,而不是英特尔

(本篇中文版文章是读者 Ben Yu 做的编译,我做了一些修改后发表。非常感谢Ben的贡献!)

在上周的同一天里发生了两件颇有联系的事:美国《芯片法案》的通过和英特尔糟糕的季度业绩,结合起来,看似意味着美国国会找错了帮扶对象。

很多人认为,英特尔作为美国半导体业的中流砥柱,只需要一个新的 CEO,加上一些额外的激励政策就可以重返巅峰,帮助美国扭转半导体制造业不断下滑的趋势。

2021 年,Pat Gelsinger 成为英特尔的 CEO,英特尔从《芯片法案》中获得价值数十亿美元的纳税人补助金,以及来自俄亥俄州等州友好的地方政策——等待在那里建立一个新的英特尔工厂。但正如英特尔的收益所显示的那样,该公司的核心业务正在急剧下滑,以至于《芯片法案》在重复批款通过十次也无法重振该公司。

为了更了解英特尔当前的困境,我推荐阅读两份关注半导体的 Newsletter:

- Dylan Patel 的《SemiAnalysis》

- Doug 的 《Fabricated Knowledge》

在这里,我就不再讨论他们已经讨论过的事,我想思考的是《芯片法案》的资金投向哪些公司会是更好的选择。

先说结论,我的建议是应该投给韩国的两家科技巨头:三星和 SK 海力士。

三星和 SK 海力士

尽管台湾和台积电因为地缘政治的原因受到了更多的媒体关注,但不可忽略的是韩国在过去几十年来也一直是半导体制造业的领先国家。台积电创始人张忠谋去年在一次概括全球半导体市场情况的演讲中明确指出韩国是台湾最强大的竞争对手,而美国和中国在半导体产业则没有什么优势。

引申阅读:《张忠谋的最后一次演讲》(付费内容)

全球四大芯片制造商分别是台积电、三星、SK 海力士和英特尔。这几家公司似乎都比英特尔的经营状况好。三星和 SK 海力士也都在美国进行过成功的投资,并计划增加投入——实际上,它们的投资额远远超过了《芯片法案》的拨款。

三星和 SK 海力士都有在美国扩张投资计划的动力,它们的执行力也很强,选择它们会比选择英特尔要更安全。

三星:大多数消费者可能是因为曲面屏手机或智能电视熟悉三星这个品牌,然而实际上三星在 1996 年就开始在得克萨斯州奥斯汀市建造半导体工厂,后来在 2007 年和 2017 年分别增加了工厂的产能。

三星在奥斯汀市的工厂主要生产 14 纳米和 28 纳米/32 纳米范围内的逻辑芯片,也就是说它还没有引进最尖端的 5 纳米或 3 纳米芯片生产技术。话虽如此,这家三星工厂已经为一些大客户提供服务,例如特斯拉。自 2017 年以来,该工厂一直在为特斯拉提供以 14 纳米技术做的全自动驾驶芯片,对于特斯拉的自动驾驶来说这是至关重要的组成部分。

凭借在德克萨斯州的一些成功经验,三星宣布在去年年底追加 170 亿美元的投资,在德克萨斯州的泰勒市(距奥斯汀 40 分钟车程)建立另一家工厂,以扩大其在美国的逻辑芯片制造能力,并加大对德克萨斯州供应商和合作伙伴生态系统的投入。

与之相比,在英特尔所有的美国工厂中,只有亚利桑那州的工厂拥有 14 纳米技术。在今年的上半年里,三星正式取代英特尔成为全球第一大的芯片制造商。

SK 海力士:我猜很少有人听说过 SK 海力士,或者它的母公司,韩国 SK 集团。然而它是全球第二大的存储芯片制造商(最大的是三星)。SK 集团作为韩国数一数二的财阀,最近在美国也有下一步的投资计划。

就在英特尔财报公布的两天前,SK 集团的董事长崔泰源拜访白宫,和拜登总统视频会议(因为拜登染上了新冠),宣布了他在美国半导体、绿色能源和生物技术行业共计 220 亿美元的投资计划。

崔泰源在去年曾宣布,SK 计划在 2030 年之前向美国投资 520 亿美元,这笔 220 亿美元的投资就是其中的一部分。半导体部分约为 150 亿美元,涵盖研发项目、材料和先进的封装和测试设施(另一部分将用于造电池、电动汽车充电站和其他绿色商业项目)。

值得一提的是,英特尔将自己的大部分内存芯片业务以 90 亿美元的价格出售给了 SK 海力士。所以从某种角度看,SK 海力士已经拥有了英特尔曾经有的一部分。这笔交易也包括了英特尔在中国的最后一个制造厂,位于大连。英特尔仅存的内存芯片产品之一 Optane 上周也正式被关闭,造成 5.59 亿美元的注销损失。据推测此举是为了让英特尔能够专注于其下滑的逻辑芯片业务,与三星和台积电竞争。

英特尔的业务在不断萎缩,而 SK 海力士则在扩张。

借助韩国的成功

我们已经了解三星和 SK 海力士承诺投入总计 320 亿美元在美国的半导体制造业上,那《芯片法案》能带来些什么呢?我们来看一下美国国会在次法案里的资助计划。

虽然经常被媒体报道的数字是 520 亿美元资助,但从《芯片法案》中拨出的直接用于建造更多半导体工厂,或培训更多工人经营这些工厂的资金实际上是 392 亿美元。

我放了一些法案细节内容的截图在下面,可以点击这两个链接阅读完整版本(资料1、资料2)

在 390 亿美元制造业激励预算中,今年只允许支出 190 亿美元。其余的 200 亿美元必须分成每年 50 亿美元,在接下来的四年中支出。与此同时,负责分配这笔资金的美国商务部每个财政年度可以从 500 亿美元的大基数中扣除 2% 的费用,用于雇佣员工、寻找办公场所、购买电脑等工作——相当于每年 10 亿美元的行政预算。如果你是一个投资人,基本上可以理解这是在这个“500 亿美元的纳税人基金”的中收取 2% 的管理费,但对美国人民来说并没有“结转利息”的收益。

对于《芯片法案》的实施,很多人已经提出担忧。一些人担心,拨款(无论是 520 亿美元,还是 392 亿美元)与韩国两大科技巨头的投资相比,美国国会的投入看起来有些微不足道。还有人担心,这些激励措施会被公司滥用于股票回购或资助股东分红,而不是建造工厂。英特尔公布 2022 年第二季度净亏损 454,000,000 美元,这是英特尔 30 多年来首次出现 GAAP 净亏损,同时英特尔宣布减少资本支出(例如建设工厂),但承诺会增加股息,而让人更加不安。为了平息这种担忧,商务部不得不在周五晚些时候发表声明,表示将把《芯片法案》的激励规模限制在“不超过必要的范围”(然而这里”必要“的定义是模糊的)。

退一步来看,很明显,美国在设计、资助和操作一项自上而下的工业政策以推动一个不景气但有战略重要性的行业方面相对来说并不成熟。在之前的一篇文章《美国能否"比中国更中国"?》中,我指出美国根本上缺乏“工业规划能力”这一问题,它要么从未拥有过,要么已经有一段时间没有行使过了。《芯片法案》可能是美国近些年第一次正式的实战,它现在已经步入到产业政策中“尝试和改错”(trial and error)阶段。就像 Danny Crichton 在 Newsletter 《Securities" by Lux Capital》中说到的:

”尝试和失败是美国学会如何制定战略和挽救其工业基础的唯一途径。”

在美国试图搞清楚怎么操作工业政策的时候,借鉴一些盟国的成功工业政策所培养出的公司的成功经验应该是最明智的,比如韩国,它在各种产业上非常善于执行政策。

对于美国来说,当然希望英特尔这样一家本土企业能够做的更好。在达成这一愿景之前,借助韩国的力量也不失为一个明智之举。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周一篇新文章送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!