JD Cloud is quietly, but effectively, positioning itself as the new “national champion” in China’s cloud computing market. This move became apparent when, during the weeklong “Two Meetings” deliberation that anointed China’s leaders of the next five years, JD Cloud’s top executive, Cao Peng, was the one who delivered a set of proposals on how the country can accelerate the modernization and digitization of its supply chain on the cloud with 100% domestic technologies.

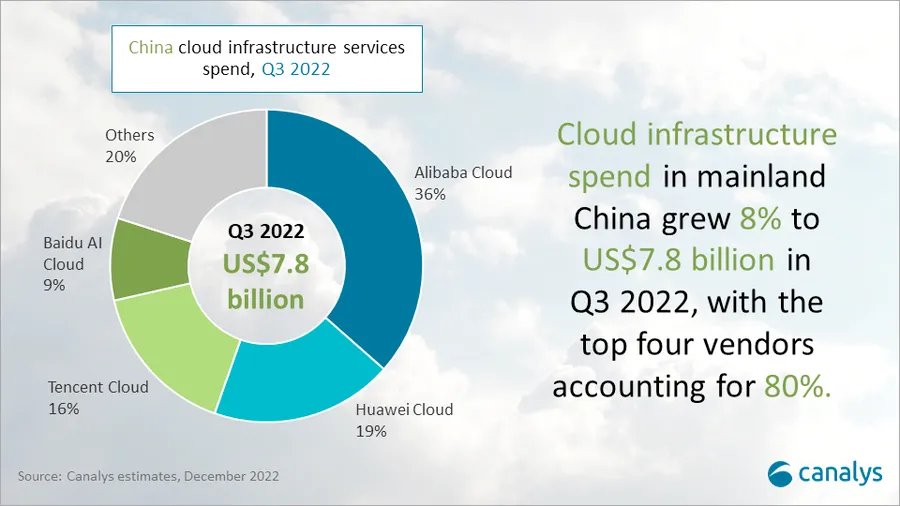

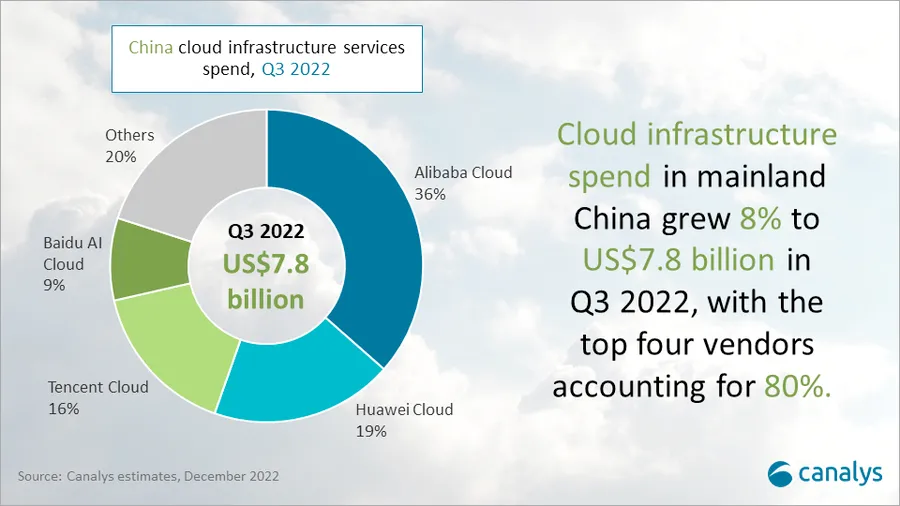

JD Cloud is a minor player in China’s cloud industry. So minor that the government's own think tank, China Academy of Information and Communications Technology, hardly mentioned JD’s name in its official white paper, which I analyzed in-depth a few months ago. Industry analysts feel the same way. In Canalys’s latest estimates of China’s cloud market, JD Cloud doesn’t even get a sliver on the pie chart.

Thus, it’s extra notable that it was JD Cloud’s executive of all the Chinese clouds, who had a voice during the all-important “Two Meetings.” It also helps that Cao Peng is a member of the National Committee of the People's Political Consultative Conference.

Yesterday, JD held a “JD Cloud Summit” in Guangzhou to further amplify the messaging of its proposal and, not surprisingly, touted why JD Cloud should be the go-to cloud platform to use. What emerged from JD’s proposal and its event, which Cao Peng also spoke at length, are two new slogans that illustrate both the progress and struggle that China’s facing in completely switching its digital infrastructure from foreign to domestic technologies – and two opportunities JD Cloud hopes to capitalize on.

Slogan 1: Real Replacement, Real Usage (“真替真用”)

This slogan shows that, despite all the calls-to-action to switch to “Made in China” technologies, made more urgent by the US’s increasingly tighter export control, companies still don’t trust domestic technologies enough to use them for real.

This struggle was explained in more detail by the plain-spoken Cao, who shared that most companies are willing to try homegrown technologies in the development and testing stage, but not in production (or real usage).

For readers who are not familiar with how companies adopt new technologies, the “development to testing to production” migration process is typical. If you are a large company and/or a less technically capable company, the process can often take one to two years, depending on the level of urgency, technical sophistication, and dedicated engineering resources. Companies will usually create a development environment to “play around” with the new technologies, and if all goes well, test it in a staging environment that simulates the real world to “kick the tires” further. Passing the threshold from “testing” to “production”, which basically means deploying the technology into the wild, is very hard. There is always a chance that new technologies could cause issues, interrupt business operations, and lose revenue or customers. Rolling back an in-production deployment is also difficult and messy. Even if all goes well, it is best practice to keep your previous technology stack around for a while as a failsafe.

By coming up with this slogan as a key message, it signals that even with all the urgency from the top and pressure from the outside, most companies don’t yet trust domestic technologies enough to put them in production and risk business losses. This fear is understandable, because most domestic technologies are unproven and most businesses are trying to recover from Zero Covid and don’t want to add another risk to their operations. Meanwhile, the risk of not being able to, say procure the latest Nvidia GPUs, is more remote and can be circumvented rather easily than US regulators care to admit.

To inject more confidence into domestic technologies and position itself as the “national champion”, JD shared that 80% of its own workloads now run on “Made in China”' solutions. Companies who are slow to make the foreign-to-domestic switch can leverage JD’s experience – all distilled and packaged into a platform called JD Cloud. It is perhaps not lost on JD’s audience, and certainly not to the sharp readers of this newsletter, that even the “national champion” is only at 80% and not 100%.

Slogan 2: Multi-Cloud, Multi-Silicon, Multi-Workload (“多云多芯多活”)

If slogan 1 speaks directly to China’s overall challenges in adopting domestic technologies, slogan 2 sounds more self-interested – tailored to benefit JD Cloud. It is pushing a multi-cloud narrative that commonly benefits the smaller players. (That’s why AWS, as the longtime global cloud computing leader, would not allow even the utterance of the word “multi-cloud” at its Reinvent conference a few years ago. It relented in more recent years, when ignoring multi-cloud became impractical and tone deaf.)

As a small player, JD Cloud benefits from a “multi-cloud” industry landscape. As the “national champion”, JD Cloud embraces a comprehensive menu of domestic chips (“multi-silicon”) and homegrown infrastructure software products to handle all types of use cases (“multi-workload”), so customers can (in theory) use a high-performance cloud that uses 100% “Made in China” solutions from top to bottom.

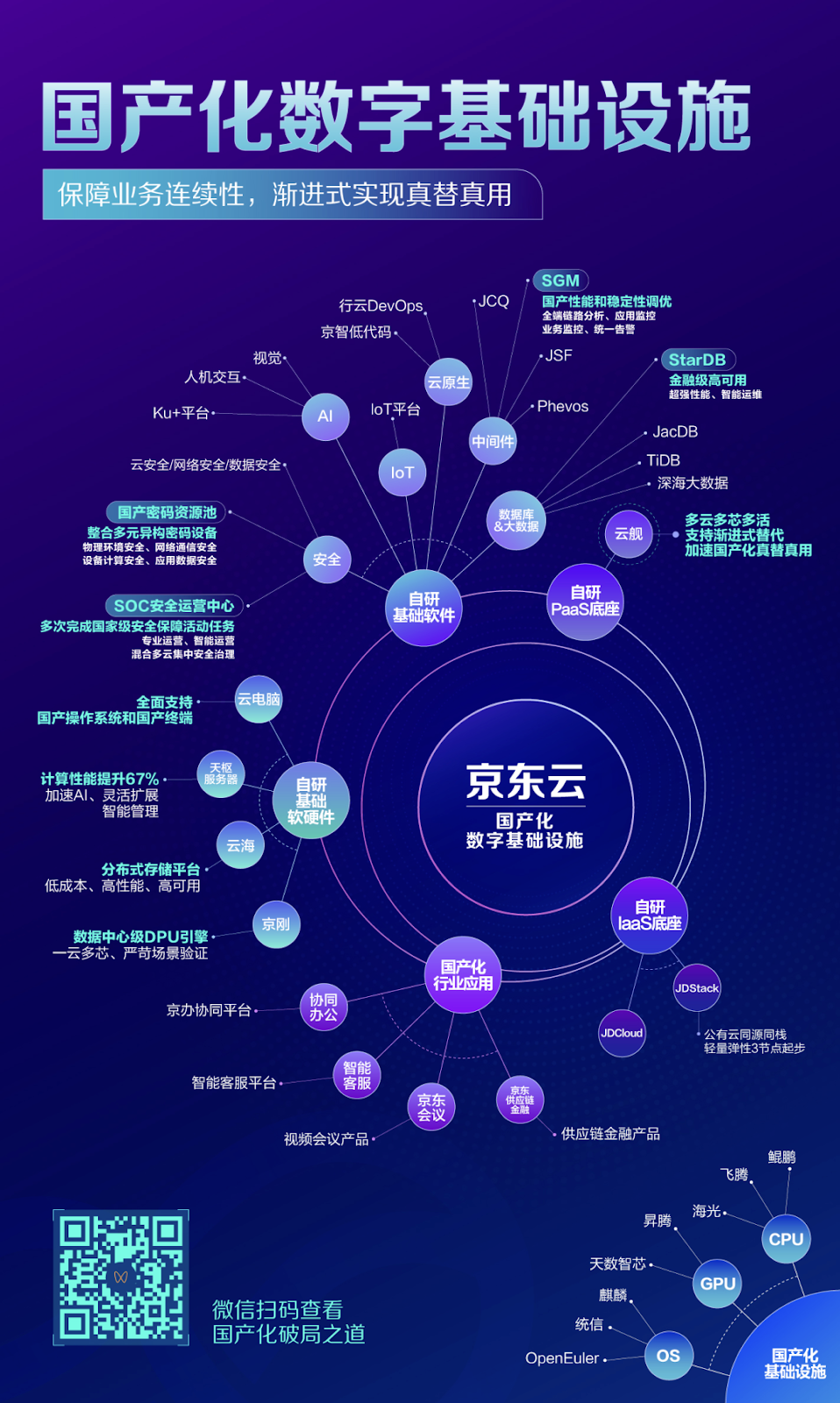

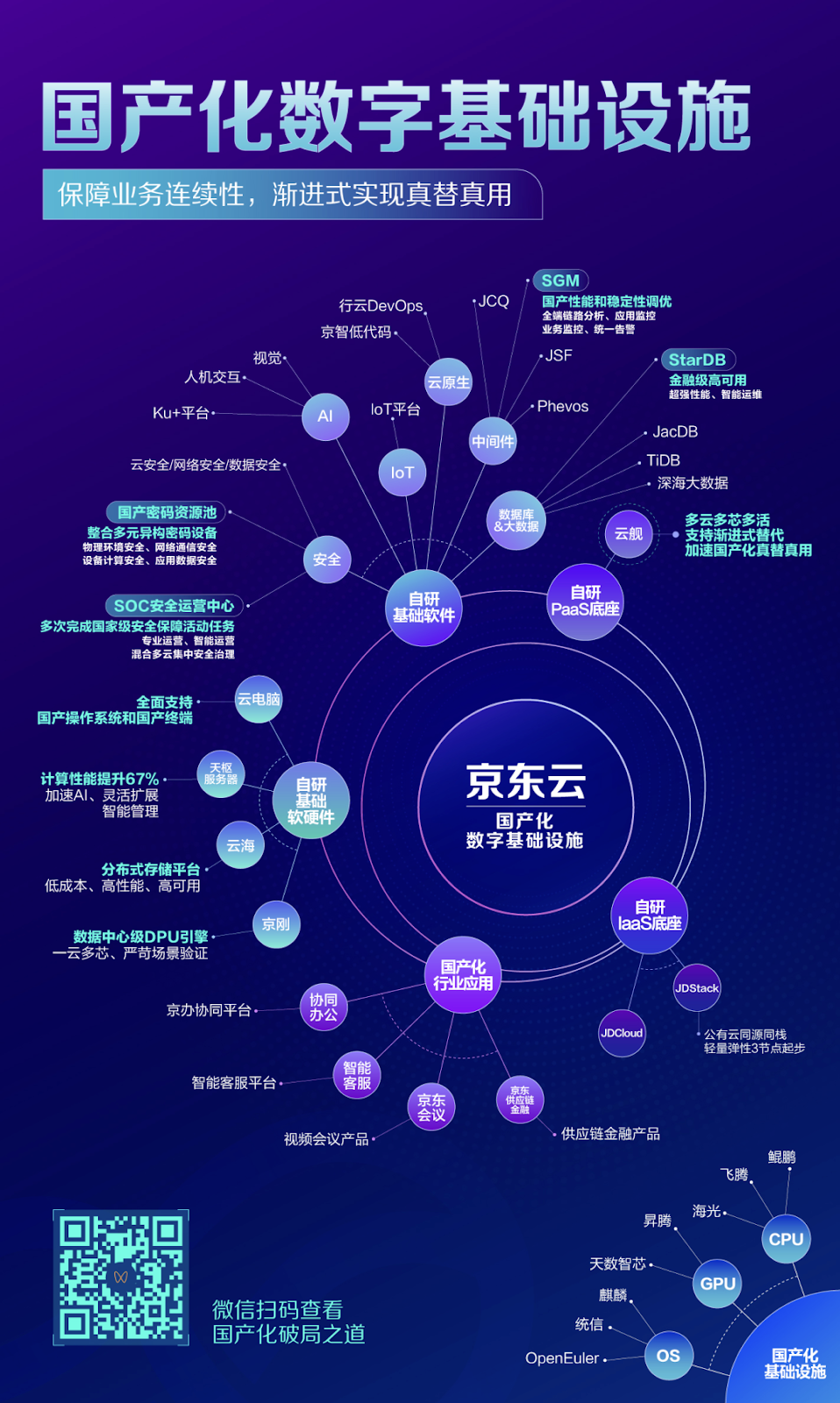

How comprehensive? This infographic, aggressively promoted by JD, shows all the components of an entirely homegrown digital infrastructure that makes up JD Cloud.

What is noteworthy about this infographic (and you don’t really need to read Chinese to appreciate it) is that it goes into painstaking detail to highlight and squeeze in every homegrown product worth mentioning in the cloud computing stack. JD Cloud claims to integrate them all, starting from the CPUs/GPUs and operating systems layer, to the IaaS and PaaS layer, to even the SaaS layer that includes collaboration products, like Google Doc, and virtual meeting tools, like Zoom. The stack also includes open source projects created by Chinese companies, like TiDB (by PingCAP) and OpenEuler (by Huawei).

If you take this infographic at face value, there already appears to be multiple “Made in China” alternatives in every layer of the cloud. In theory, all the pieces of a 100% domestic cloud are already in place. Of course, where the rubber meets the road is how well these solutions work in production, not just individually but together in a single, coherent cloud platform. That’s the challenge. And that’s the problem where JD Cloud, poised to be at the center of a multi-cloud, multi-silicon (domestic silicon, of course) world, is positioning itself to solve.

Can JD Execute Better This Time?

It has always been perplexing to me why JD is not more of a leader in the cloud. It is not because JD lacks technical prowess or innovative capabilities. In fact, JD was an early adopter in a lot of cutting edge tech that has now become mainstream. Back in 2018, JD was an early user of Kubernetes, a now-ubiquitous cloud container orchestration software that popularized the notion of multi-cloud. For a while, JD managed the largest Kubernetes cluster in the world! However, JD was slow to package its cloud capabilities into products to meet market demands.

While JD Cloud was late to the market, China’s fast-growing (though recently slowing) cloud sector has been carved out by other big players, each with its own lanes. AliCloud, the market leader, serves SMBs and startups well and is moving up into large enterprises. Tencent Cloud caters to social and gaming products, not surprising given that those verticals are also where its own core products shine. Huawei Cloud is a strong fit for the public sector and state-owned enterprises, given its longstanding roots and relationships with those sectors. Baidu is trying its damn hardest to carve out an “AI lane” for itself (see my previous writing on Baidu and AI). ByteDance Cloud, a new entrant, is squeezing into the space by packaging its own powerful recommendation engines as a cloud to lure companies who aspire to be like ByteDance one day.

Where does that leave JD Cloud? Well, beyond being an e-commerce juggernaut, JD does have differentiating capabilities in managing a complex and highly-efficient set of warehousing, delivery, and supply chain operations. These capabilities are “infrastructural” by nature, thus are amenable to be packaged into cloud services, which is, at the end of the day, just digital infrastructure for rent. Now that it is hard-pivoting into its role as a “national champion” – a label that commands more market power in an age of deglobalization and constant sanctioning risks – JD Cloud may be getting a second chance.

Coming out of the “Two Meetings”, JD clearly has the ear, if not the backing, of the newly-anointed government leaders and will play a key role in China’s next phase of digitization. Given the challenges ahead, especially as encapsulated in “Real Replacement, Real Usage”, JD Cloud must deliver a solid, enterprise-level cloud experience without foreign technologies or it will risk embarrassing itself and China’s entire push to adopt domestic technologies.

The Spiderman rule applies to all. Being a “national champion” comes with both great power and great responsibility.

京东云是新的“国家队主力”吗?

京东云正在悄然而有效地将自己定位为中国云计算市场中新的“国家队主力”。这一举动在为期一周的“两会”期间暴露出来。京东云的技术委员会主席,曹鹏,也是京东云事业部总裁,在“两会”期间为新一代国家领导提出了一套关于加快数智化社会供应链建设和降低社会物流成本的建议。

京东云在国产云市场中是个小角色。这个角色小到,以至于连官方智囊 – 中国信息通信研究院 – 在去年出版的白皮书中连提都没提“京东”这两个字。云行业分析师也持有相同的看法。在Canalys最新估算的中国云市场份额中,京东云在饼图上连一小块都没有占。

因此,在所有云平台公司中,京东云的老大“两会”期间代表行业发声,还是有些引人注目的。曹鹏作为全国政协委员的身份也是其有发言权的原因之一。

昨天,京东在广州又紧接着举办了一场“京东云峰会”,进一步强化其题给领导的建议中的内容,并接机宣扬为什么京东云应是加快数智化社会供应链建设的首选云。从京东的提案和宣传活动中,以及曹鹏的发言中,浮现出两个新口号。这两个口号反映了中国在将数字基础设施从国外技术转向国产技术方面的进展与挑战 —— 以及京东云希望抓住的商业契机。

“真替真用”

“真替真用”这条口号背后的意义是,尽管一直在大声呼吁用国产技术,同时美国日益严格的出口管制使这种呼声变得更加紧迫,但众多企业仍然信不过国产技术去放心真正深入使用。

曹鹏直言不讳地描述了这个挑战。他表示,大多数公司愿意在开发和测试阶段尝试国产技术,但不愿在生产环境中使用(也就是所谓的真用)。

对于不熟悉大企业如何采购和采用新技术的读者来说,我稍微科普一下一般流程。从 “开发到测试到生产” 的迁移过程是很典型的。如果您是一家大型企业或技术能力较弱的公司,这个过程通常需要一到两年时间,具体落实时间段取决于紧迫程度、技术精湛程度和投入的工程资源。公司通常会创建一个开发环境来 “玩玩” 新技术,如果一切顺利,将其放到一个模拟现实场景的“测试”环境中进一步“踢轮胎”。从“测试” 过渡到 “生产”(也就是把新技术放到真枪实弹的场景中)非常困难。新技术总有可能出问题,中断业务运营,导致收入或客户流失。回滚一套已投入到生产环境的部署也是件很头疼的事情。即使一切顺利,最好还是留住之前的技术栈作为一个安全备份措施以防万一。

用这个口号作为主题信息,表明即使在来自最高层的压力和外部威胁的紧迫情况下,大多数公司仍信不过国产技术,不想冒损失业务的风险。这种担忧是可以理解的,因为大多数国产技术尚未得到验证,而大多数企业都在努力从清零中恢复过来,不希望为自己的生意在加上额外的风险。同时,像今后因为美国制裁而无法采购到最新的英伟达GPU的这种风险,相对感觉更小更遥远,而且有很多可以合法避开美国监管的方式。

为了增强对国产技术的信心,并将自己定位为“国家队主力”,京东表示,现在自己内部80%的负载已经运行在百分之百的国产技术上。对于需要开始“国产化”的公司,可以借鉴京东的经验 —— 这些经验都被浓缩并打包成“京东云”这个平台。值得一提的是,就连“国家队主力”也只达到了80%,而不是100%。

“多云多芯多活”

如果 “真替真用” 一针见血点出中国在采用国产技术方面还有很多挑战,那么“多云多芯多活” 则听起来更自私些,基本就是为京东云打广告。推动“多云”的模式,通常有利于小玩家。(这就是为什么作为长期的全球云计算领头羊,AWS,在它几年前的Reinvent大会上严格不允许任何参与者提“多云”这一词。近几年才开始放宽,因为”多云”的趋势已经没法忽视。)

作为一个小玩家,京东云一定会从“多云”中受益。作为“国家队主力”,京东云拥抱一系列国产芯片(及“多芯”)以及国产的基础设施软件产品,来处理各种类型的负载(及“多活”),这样客户(理论上)就可以安心的用上一套100%的国产云了。

京东云拥抱国产技术又到底有多么全面呢?这张京东大力推广的信息图展示了组成京东云平台中每一层的国产技术。

值得注意的是,这张图里详细地突出了云计算堆栈中每一个值得一提的国产产品,也努力的把它们都“挤了”进去,同时也特意突出京东自研的技术。从CPU/GPU和操作系统层,到IaaS和PaaS层,甚至深入到协同和虚拟会议工具的SaaS层,京东云都可以把它们结合起来。技术栈还包括由中国公司创建的开源项目,如TiDB(由PingCAP开发)和OpenEuler(由华为开发)。

如果您完全相信这张图里的所有信息,那云平台的每一层都已经有了多个国产的替代品。理论上,100%的国产云已经是现实。当然,这些解决方案在生产环境中的表现如何,而且不仅仅是单个的性能,而是结合起来的综合性能,还有待考验。这就是国产化面对的挑战。这也就是京东云在 “多云多芯多活” 中试图解决的问题。

京东的第二次机会

让我一直困惑的是,为什么京东云没有做的更大。这并不是因为京东本身缺乏技术实力或创新能力。事实上,京东是许多尖端技术的早期采用者,这些技术有些已经成为业界主流。早在2018年,京东就是Kubernetes的早期用户,Kubernetes现在是无处不在的云容器编排软件,也普及了“多云”模式。有一段时间,京东管理着世界上最大的Kubernetes集群!然而,京东将自身的云计算能力打包成产品面对市场需求的速度太慢。

在京东缓慢步入云市场的同时,中国云领域的飞速增长(尽管近期开始放缓)已被其他大厂瓜分,每家都有自己舒服的定位和赛道。领头羊位置的阿里云善于服务于中小企业和创业公司,而且正在向大型企业推进。腾讯云主要面向社交和游戏公司,这也并不奇怪,就是其自身核心产品擅长的领域。华为云的赛道是政府和国企,与这些领域有深渊长期的客户关系。百度正在竭尽全力为自己杀出一条“AI云”的赛道(刚兴趣的朋友,请参阅我之前关于百度和人工智能的文章)。作为新入行的字节跳动云(及火山引擎)也在把自身强大的推荐引擎打包成云服务,吸引那些渴望有一天也像字节一样成功的公司。

那么京东云该何去何从呢?除了是电商巨头,京东在管理复杂、高效的仓储、配送和供应链运营方面确实具有独特的能力和经验。这些能力本质上都是 “基础设施”,因此非常适合打包成云服务。归根结底,云服务也就是可以租赁的数字化基础设施。现在,京东云正努力转型成为“国家队主力”。这个标签在“脱去全球化”的大时代中,还是有很强的市场吸引力的。因此,京东云可能正在迎来第二次机会。

在“两会”结束后,京东显然已经引起了新一代领导人的关注,甚至得到了他们默认的支持,将在中国下一阶段数字化中发挥关键作用。鉴于未来的挑战,尤其是在“真替真用”方面,京东云必须在没有任何外国技术的情况下提供可靠的、企业级的云计算体验,否则它将冒着让自己和整个国家在推动采用国产技术转型过程中失败的尴尬风险。

“蜘蛛侠”守则适用于所有人。成为 “国家队主力” 既意味着巨大的权力,也意味着巨大的责任。