As we shake off the holiday-induced “mental cobwebs'' and embrace a new year, I’m starting a new ritual – the Interconnected Annual Letter. Admittedly, this is a shameless mimicry of the ritual behind Warren Buffett’s famed Berkshire Hathaway annual letters, as well as that of other successful investors. Having read many of these letters, a similar narrative format looking back on what I’ve learned writing on and investing in Interconnected, I thought, would be a good way to “report” to you: our subscribers. (Imitation is the sincerest form of flattery, right?)

While we technically don't have “shareholders”, I treat every subscriber as a shareholder. I sincerely thank you for giving us your most valuable resource: attention and time. And even though I don’t have my own Carol Loomis, I hope the Interconnected Annual Letter will evolve into an artifact that is similarly insightful and charming over time – something worth referring to (and chuckling about) in future years.

Similar to Buffett’s and other investors’ annual letters, we begin by sharing the Interconnected Portfolio’s public market investment performance in 2022, along with a comparison to other commonly-used indices as benchmarks:

- Interconnected Portfolio*: +79.33%

- S&P 500: -19.44%

- DJIA: -8.78%

- NASDAQ 100: -32.97%

- Russell 2000: -21.56%

- MSCI World: -17.73%

- Wilshire 5000: -19.04%

*Some important context and caveats: I don’t manage other people’s money and don’t plan to any time soon. However, I manage the Interconnected Portfolio, which represents a significant proportion of my net worth, in the mode of a professional investor and a fiduciary of others. (If I don’t, I will go broke!) The level of responsibility is the same, minus the principal-agent problem and the allure of management fees. The performance number may look good for 2022, but it, in no way, predicts the likelihood of future performance. As Buffett wrote in his 1990 annual letter:

“Berkshire's 26-year record is meaningless in forecasting future results.”

If a (very good) track record of 26 years is meaningless in predicting future results, then a track record of one year is at least 26-times more meaningless, no matter how good. What is meaningful, I hope, are the writings, lessons, and reflections behind this single performance number. So let’s dig into those instead (sprinkled with fun, topical generative art).

Flexible Within Circle of Competence

The concept of “circle of competence” is well-known among professional investors. So are the brutal lessons of disasters when one steps out of it (e.g. when Long-Term Capital Management started doing M&A deals). The same concept should probably be applied to more writers too, so less of us become “professional opinion haver’s”, though the consequences will always be less painful no matter how far a writer’s opining strays.

Whether I’m wearing my writer hat or investor hat, I do my best to stay within my self-defined circle of competence bordered by these areas:

- DevOps

- Cloud infrastructure

- Open source (software and hardware)

- A subset of China tech that overlaps with the three areas above

- Technologies that have a strong influence on or by geopolitics and US domestic politics

This seemingly random collection of topics would make a lot more sense if you have a moment to peruse the About page. It is a rather tightly defined circle. Luckily, it has also been a quickly expanding one with surprising entrants, e.g. TSMC in Arizona.

The one big lesson I learned in 2022 about operating within one’s circle of competence is to be directionally flexible. I used to think that investing within that circle is solely about finding the winners and going long. Later on, it dawned on me that shorting the losers within that circle is an equally valid way to stress-test my competence. Furthermore, given that Fed policies have become major factors in all forms of investing, while globalization is (likely) dead, knowing how to spot “short-term losers” who are actually “long-term winners”, turns out to be a perfectly good way to invest within my circle of competence as well. One marker of competence is knowing how short is too short, how long is too long, given the circumstances.

Sadly, I did not learn this lesson until mid-2022 or our performance would have been better. That being said, I do not ever intend to be a professional short seller, even though this class of investors made out like bandits last year. From my experience, the best way to become competent (and stay competent) in any industry is to have an insatiable appetite for continuous learning that’s motivated by optimism. It is very hard to keep learning about something that you are inherently pessimistic about and don't think will work. Of course, we don’t live in fantasies and there are always things that will, in fact, not work. So we all have to choose our “circles” wisely.

Even though I shorted quite a few companies in the DevOps and cloud infrastructure realm last year, I continue to think these industries, led by a dramatic increase in developers globally, have promising years of growth ahead. However, the immediate view beyond the windshield still looks bumpy, so continuing to stay directionally flexible as the “sideways market” continues is a key lesson learned.

Widen By Writing

The nice thing about writing a weekly newsletter that’s intentionally eclectic is that it serves as both a live polling of interests and an avenue to widen my circle of competence, however slowly. (How eclectic? Last year, we wrote about topics ranging from how data center locations and reproductive rights intersect to a product overview of China’s digital currency, the e-CNY.) Writing eclectically, in conjunction with active investing, over the last three years has been a constant source of self-improvement and joy.

The “polling function” is easy enough to report on objectively. Readers and subscribers vote by their clicks and views. And the collection of posts that garnered the most clicks and views in 2022 (more than 40%) are ones focused on semiconductors. This outcome no doubt mirrors the rising general public interest in the topic, whipped up by the passage of the CHIPS Act in the US, tougher global sanctions on the Chinese semiconductor industry, and a constant fear of war over Taiwan. Semiconductors look to remain a highly relevant topic in 2023, so we will continue to focus on these tiny but mighty chips. Two dimensions I hope to dive deeper in 2023, as my circle of competence would allow, are: 1. The strategic implication of RISC-V and open source chip design; 2. The US and China’s differing talent gaps and impact on their respective pursuit of high-end semiconductor manufacturing capabilities. I wrote about the former once last year (on Valentine’s Day with a holiday appropriate title) in “Romance of the Three Kingdoms: Semiconductor Edition”; it barely scratched the surface.

The “widening function” is more subjective and harder to report on. Writing is not just a way to disseminate what you know, but also a way to explore what you don’t know in a more focused way (as opposed to just passively reading). However, when writing is done publicly via a newsletter, exploring curiosities can be risky. You may turn off some subscribers who are not here to explore with you, but only here to absorb what you already know. (On a meta level, this annual letter is in itself an encounter of this risk.) Nevertheless, the power to explore and widen one’s interests and competence is what makes writers want to write more. The risk of losing readers in the process is a necessary form of creative destruction. And since the quality of “widening” cannot be reflected in clicks and views, here are two pieces of exploration that I think are most worth sharing, for no better reason other than that they brought me the most personal satisfaction and new knowledge:

- "CALB vs CATL: Can Two Battery Pigs Both Fly?"

- "Prosus: Softbank Without the Drama"

Of course, new knowledge is a far cry from a circle of competence. That’s why I have not yet invested in any EV company, battery makers, or South African telecom conglomerates. Even Tencent is a stretch for me, because I don’t have deep knowledge of social media and am not a gamer.

Oftentimes, finishing a piece on a company or an industry can give me the illusion of expertise right away. With that illusion comes a sense of unearned confidence in investing real money in a “new-acquired” circle of competence, when a new circle takes years if not decades to draw. I’ve made these mistakes before, and they are costly. I intend to avoid them in the future, while continuing to “widen by writing”, but only writing, until I’m ready.

“Help! Help!”

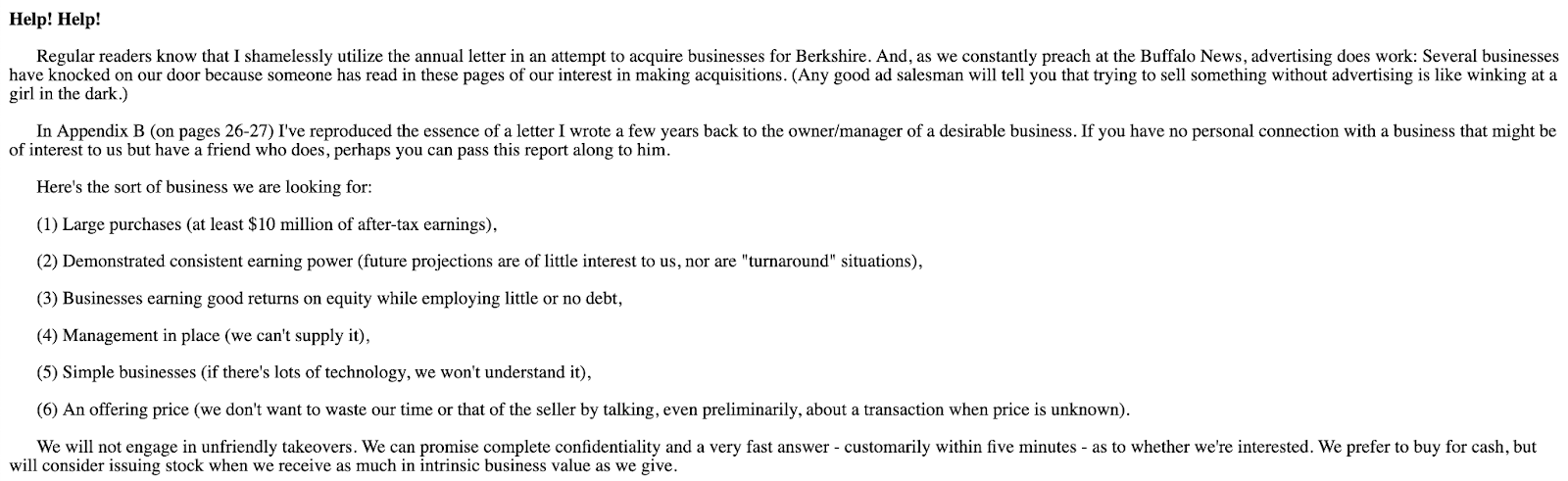

One of the less talked about “super powers” of Warren Buffett’s success is his ability as a consummate but tasteful marketer. To his credit, Buffett was always transparent and never shy about placing his “advertisements” directly in Berkshire’s annual letters, especially when he and Charlie Munger were looking for businesses to acquire. Indeed, he was a pioneer in the “newsletter as a distribution channel” tactic, long before any of us. Here is a screenshot from his 1990 annual letter:

So in a last act of mimicry, I’m also including a “Help! Help!” section to wrap up this annual letter. However, I’m not looking for businesses to buy, but for new relationships to build and learn from, specifically with family offices. During 2022, I got to know a few family offices who reached out to me because of my writing. I learned a great deal about how they operate, what they care about, and how they see the world. It was a set of fresh perspectives I did not have before. These connections were organic, ad-hoc, and the highlights of working on Interconnected. Stealing a page (or tweet) from Sahil Bloom’s personal annual review framework, conversations with family offices created the most energy for me in 2022.

What created energy this year?

— Sahil Bloom (@SahilBloom) December 15, 2022

Review your calendars from the year.

What activities, people, or projects consistently CREATED energy in my life?

Write them down.

Did I spend ample time on the energy creators or did they get neglected?

Goal: More time on these in 2023.

In 2023, I hope to be more intentional about connecting with and learning from family offices that are:

- Managing $100 million or more in assets (can be a single family or multi-family office)

- Regularly evaluate and hire outside managers to manage capital

- Ideally located outside the US (or have non-US perspectives, as these are the views I’m more curious about and have more blindspots in)

If you have connections to this type of family office (or indeed are part of one yourself), I would appreciate an introduction to have a 45-minute to 1-hour Zoom call to get to know each other. I don’t have anything to sell, except my curiosity. I will have many prepared questions to ask to learn about how you operate, what you care about, and how you see the world. I am also an open book and happy to share my unvarnished points of view on any topic that resides within my circle of competence (see above).

With that, I hope everyone has a fruitful and productive 2023, full of growth in both wealth and knowledge.

Sincerely,

Kevin S. Xu

2022年《互联》年度信

在大家试图甩掉圣诞节日之后的 "思维蜘蛛网" 并迎接新的一年时,我今天启动一个新的“仪式” – 一年一度的《互联》年度信。诚然,这个“仪式” 是我对巴菲特著名的Berkshire Hathaway公司的年度股东信,以及其他成功投资者类似信件的无耻模仿。我读过很多的年度信。用同样的叙述形式回顾去年我在《互联》上的写作和投资所学到的东西,我想,是向大家 – 我们的读者和订阅者 – 最好的 "报告" 方式。(模仿就是最真诚的奉承,对吗?)

虽然严格上来说我们并没有 "股东",但我把每一位订阅者都当作 "股东" 来对待。我真诚地感谢您给予《互联》您最宝贵的资源:精力和时间。尽管我没有自己的Carol Loomis,但我希望《互联》年度信能随着时间的推移演变成一个同样具有洞察力和魅力的作品 – 在多年以后都值得参考(和嘲笑)。

与巴菲特和其他投资者的年度信类似,我们首先分享《互联》Portfolio 在2022年的股市投资的表现,以及与其他常用指数作为基准的比较:

- 互联 Portfolio*: +79.33%

- S&P 500: -19.44%

- DJIA: -8.78%

- NASDAQ 100: -32.97%

- Russell 2000: -21.56%

- MSCI World: -17.73%

*一些重要的背景信息和声明:我不管理其他人的资金,也不打算在短期内管理外界资金。但是,我以专业投资者和受托人的视角来管理互联的portfolio,因为它占我个人净资产的很大一部分。(如果我不这样做,我就破产了!)基本负责任的程度是相同的,但除去常见的“委托代理问题”和管理费的诱惑。2022年的表现可能看起来不错,但它决不能用来预测未来的业绩。正如巴菲特在他1990年的年度信中写到的:

"Berkshire的26年的记录对于预测未来的业绩毫无意义。"

如果26年的(非常好的)业绩都对预测未来毫无意义,那一年的业绩,不管多好,至少是26倍的“毫无意义”。我希望更有意义的成分是这个单一的业绩数字背后的写作、教训和反思。因此,让我们专注挖掘这些东西(并洒上一篇用AI生成有趣的图片)。

在能力圈内灵活运作

在专业投资圈中,"能力圈" 这个概念众所周知。当一个人走出这个“圈”的时候,灾难性的残酷教训也是处处可见(例如,当Long-Term Capital Management开始做并购的时候)。同样的概念也许也应该适用于更多的作者,这样我们中就不会有那么多人为了眼球而演变成 "专业的意见贩子",尽管无论一位作者的意见偏离知识圈多远,后果都不会那么惨痛。

无论我是戴着作者的帽子还是投资者的帽子,都会尽力保持在自我定义的,以这些领域为边界的能力圈内运作:

- DevOps

- 云基础设施

- 开源(软件和硬件)

- 与上述三个领域重叠的中国科技公司

- 对地缘政治和美国国内政治有强烈影响或受其影响的科技领域

如果您有时间浏览一下《互联》的 “About” 页面,这些看似很奇葩的领域集合会更合理些。这是一个定义的相当窄的“圈子”。幸好,它也是个正在迅速扩大的“圈子”,并时不时会有新的成员,例如在亚利桑那州落户的台积电。

回顾2022年,关于在一个人的“能力圈”里运作中总结出的一个重要教训是:要对方向保持灵活性。我一贯认为,在“能力圈”里做投资关注的仅仅是找到赢家并重仓加码。后来,我突然意识到,在“圈”里做空失败者也是一种同样有效的测试自己能力的方式。此外,鉴于美联储政策已经成为所有形式的投资的主要因素,而全球化也(可能)已经结束,知道如何发现那些实际上是 "长期赢家 "的 "短期输家",其实也是我在 “能力圈” 内进行投资的一个非常好的方法。能力的一个标志是知道在这种情况下,多空是太空,多长是太长。

可悲的是,我直到2022年中期才总结出这个教训,否则业绩会更好。值得澄清的是,我永远不打算成为一个长期做空的投资者,尽管这类投资者去年赚得盆满钵满。据我的个人经验,在任何行业中要想成为一个杰出的人(并保持杰出)的最好方法是不断持久的学习和拥有一种永不满足的欲望,这种欲望通常是由乐观的态度激发的。如果你对某个领域本质上持悲观态度,认为它不会成功,那就很难坚持持久的学习。当然,我们不活在幻想中,总有一些事情确实不会成功。所以每个人都必须明智地选择自己的 "圈子"。

尽管我去年做空了不少DevOps和云基础设施领域里的公司,但我仍然认为这些行业在全球开发者快速增长的大趋势带动下,会有多年的增长空间。然而,在短期未来仍然很颠簸,所谓的 "横向市场" 会持续的状态下,继续在"能力圈"内保持方向上的灵活性是一条关键的经验教训。

通过写作拓宽“能力圈”

每周写《互联》的一个好处是,它既是我用来对自己熟悉的领域知识的传播方式,也是扩大我的“能力圈”的一个途径,无论进展有多么缓慢。整个写作的过程既有“投票功能”也有"拓宽功能"。写的话题刻意比较“杂”。到底有多“杂”? 去年,从数据中心的地理位置与美国女性生殖权利的关系到中国的数字货币e-CNY的产品概述,介入的领域多放多面。在过去的三年里,不拘一格的写作,结合活跃的投资,一直是自我完善和职业满足的来源。

"投票功能" 的结果很容易向大家汇报。读者和订阅者会诚实的用他们的点击和浏览量来投票。而在2022年获得最多点击和浏览量的文章主题(超过40%)都和半导体有关。这一结果无疑反映了公众对半导体行业的关注度在不断上升,美国CHIPS法案的通过,对中国半导体行业更严厉的全球制裁,以及因台湾引起战争的持续恐惧都是原因。半导体看起来在2023年仍然会是一个“很火”的话题,所以《互联》将继续关注这些微小但强大的芯片。在我的能力圈允许的情况下,我希望在2023年深入研究与半导体有关的两个层面:1. RISC-V和开源芯片设计的战略意义;2.美国和中国不同的人才差距和对各自追求高端半导体制造能力的影响。去年关于第一个层面,我曾在情人节那天出版了一篇文章:《“三国演义”半导体版》;它仅仅触及了皮毛。

"拓宽功能" 的结果更为主观些,更难汇报。写作不仅是一种传播知识的方式,也是一种以更集中的方式探索你所不了解的领域的方式(相对于只是被动地阅读)。然而,当你通过写《互联》这种公开博客的方式“拓宽”时,探索自我的好奇心是有些风险的。有些订阅者会不高兴,因为他们不是来和你一起探索的,而只是来吸收你现有的知识的。然而,探索和拓宽自己的兴趣和“能力圈”是所有作者有欲望长期继续写东西的核心原因之一。在这个过程中,失去一些读者的风险时时存在,但又是必要的“创造性破坏”(creative destruction)。既然 "拓宽" 的质量不能反映在点击率和浏量中,我想分享两篇去年我认为最值得分享的“拓宽”文章,没有其他理由,只是因为它们给我带来了最多的个人满足和新知识:

- 《Prosus:没有八卦的软银》

当然,新知识与新“能力圈”相差甚远。这就是为什么我还没有投资任何电动车公司、电池制造商或南非电信集团。即使是腾讯,对我来说也是一个挑战,因为我对社交媒体没有深度的认知,也不打游戏。

很多时候,刚写完一篇关于某个公司或行业的文章时,会给作者一种突然获有专业知识的幻觉。这种错觉会带来了一种不劳而获的自信,立即用真金白银投资一个 "新" 能力圈中。一个真实的能力圈需要几年甚至几十年才能画出来。我犯过这种错误,代价也很高。未来会尽力避免这种错误,同时继续通过写作“拓宽能力圈”,但只用写作,直到我真正准备好以后。

"帮忙! 帮忙!"

巴菲特成功的一个很少人议论的 “要素” 是他既积极又有品味的”推销“能力。值得称道的是,巴菲特总是很透明,从不羞于在Berkshire的年度信中直接登他的 "广告",特别是当他和芒格在寻找合适的企业收购目标时。事实上,他是 "把写blog当作分销渠道" 策略的先驱者,比我们任何人都早。以下是他1990年年度信的截图:

所以在我最后一举模仿中,也包括一个 "帮忙! 帮忙!" 部分来作为这封年度信的尾。我到没有在寻找要购买的企业,而是在寻找可以建立和学习的新关系,特别是与家族办公室。在2022年期间,我认识了几个家族办公室,他们因为读到我的文章与我主动联系。我学到了很多关于他们如何运作,关心什么,以及观察世界的视角。这是我以前所没有接触到的一套新观点。这些关系建立的方式很随意,也是去年写《互联》的一大亮点。从Sahil Bloom的个人年终审查框架中借用一页内容,与家族办公室的对话在2022年为我创造了最大的正能量。

What created energy this year?

— Sahil Bloom (@SahilBloom) December 15, 2022

Review your calendars from the year.

What activities, people, or projects consistently CREATED energy in my life?

Write them down.

Did I spend ample time on the energy creators or did they get neglected?

Goal: More time on these in 2023.

在2023年,我希望能更有专注性地与更多的家族办公室联系,向它们学习,尤其是有以下特征的:

- 管理1000万美元以上的资产(可以是一个家族或多个家族办公室)

- 定期评估和聘请外部投资者管理资本

- 最好位于美国之外(或拥有非美国为中心的观点,因为这些观点是我更好奇的,而且有更多盲点)

如果您与这种类型的家族办公室有联系(或者您本身就是其中一员),我希望能通过您的介绍与这种家族办公室接触上,打一个45分钟到1小时的Zoom电话会议,彼此了解。我没有任何要卖的东西,只有我的好奇心。我会准备许多好的问题,以了解他们如何运作,关心什么,以什么视角看待世界。我也会很开放很透明,乐于分享对任何在我“能力圈”内的话题的不加修饰的观点。

在此,我希望大家都有一个富有成效的2023年,不仅是财富还是知识都会翻倍的增长。

谢谢,

Kevin S. Xu