“What is the single best technology investment of all time?”

An often-heard answer to this question is Softbank’s early investment in Alibaba. Indeed, Masa Son’s storied $20 million bet on Jack Ma (with his strong, shiny eyes) in 2000 has yielded Softbank a more than 4500% return. Even though, both Softbank and Alibaba are falling on hard times lately, it is hard to dispute the scale and impact of this single investment on Softbank, Alibaba, China, and arguably the entire world of tech.

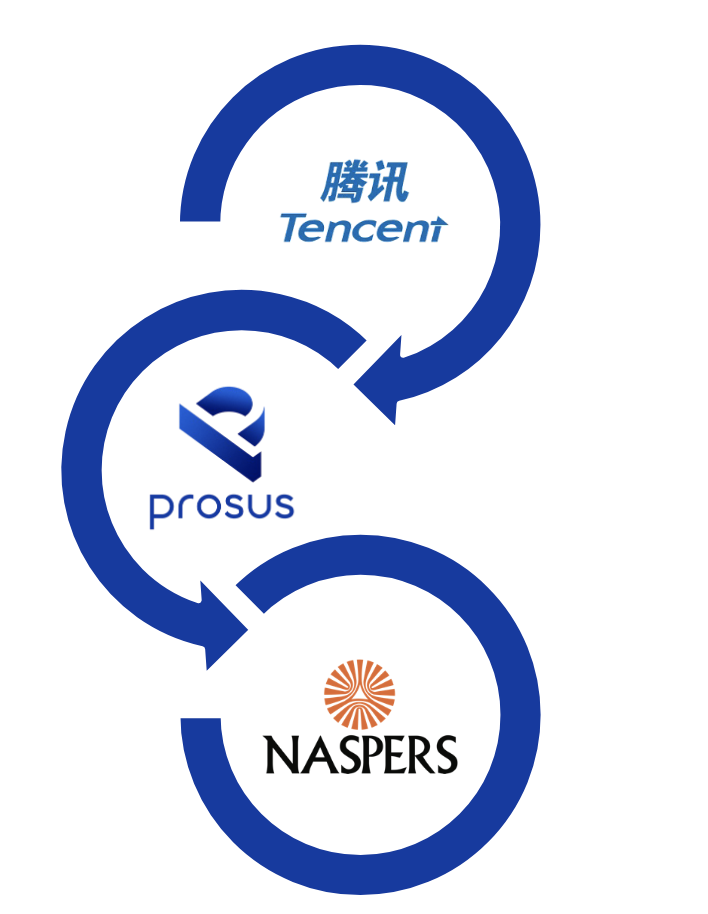

However, there is one other investment that happened around the same time, also into a fledgling Chinese tech firm by a non-Chinese investor, which yielded more than a 8000% return. That story – Naspers/Prosus’s $34 million investment into Tencent in 2001 – is, however, rarely told.

Partially due to Masa Son’s dramatic, loquacious, and larger-than-life personality, the lore of the Softbank-Alibaba “marriage” is well-documented. This union continues to dominate headlines today, with Softbank’s recent selling of Alibaba’s shares to rescue its own balance sheet from the massive Vision Fund losses.

The Naspers/Prosus-Tencent “marriage”, conceived under the (much) more low-key now-ex-Naspers CEO Koos Bekker, bears both similarities to the Softbank-Alibaba investment, but also important differences and lessons – making this story uniquely worth telling on its own. More than perhaps any other single technology investment, this one illustrates the increasingly interconnected nature of global technology investing, and the impact that one home run can enable, if you have a long enough time horizon.

Naspers? Prosus? Where? Who?

One of the reasons why this story has been hard to tell is that the investor’s history, brand, and identity is kind of confusing.

Naspers? Prosus? South African? Dutch? Who?

So before we get to the heart of the story, let’s first briefly explain the corporate history and relationship of Naspers and Prosus.

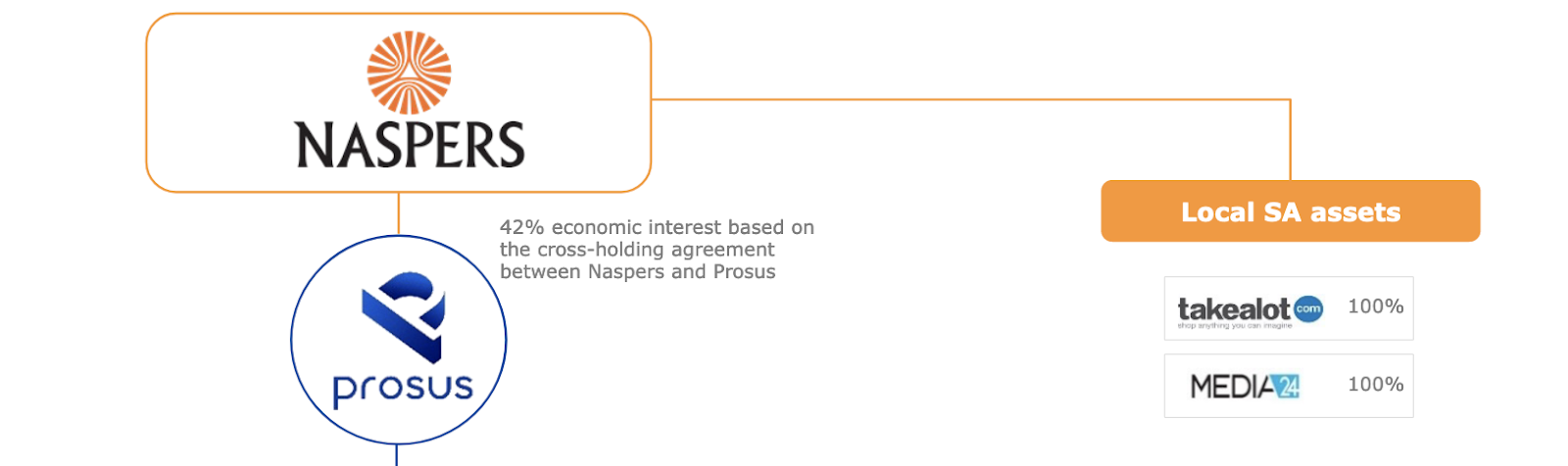

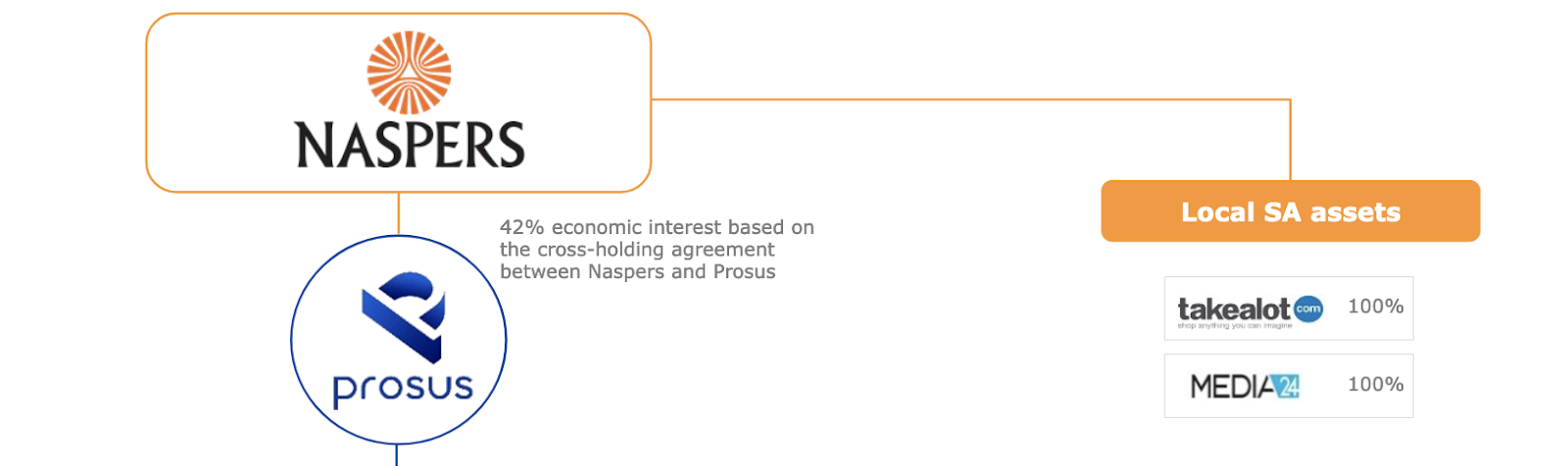

Naspers is a South African media conglomerate founded in 1914. It first started as a publishing company, grew throughout the 20th century, and played a significant role in South Africa’s complicated history, including a controversial alignment with the country’s Nationalist Party that implemented apartheid.

In the 1980s and 1990s, Naspers successfully expanded into both telecom and the paid TV business. In 1994, it became a public company on the Johannesburg Stock Exchange (where its shares still trade today). A few years later, under Koos Bekker’s leadership (who became CEO in 1997), Naspers sold the European portion of its paid TV business for roughly $2.2 billion dollars – seeding its war chest to expand into China, Russia, and other emerging markets at the dawn of the Internet.

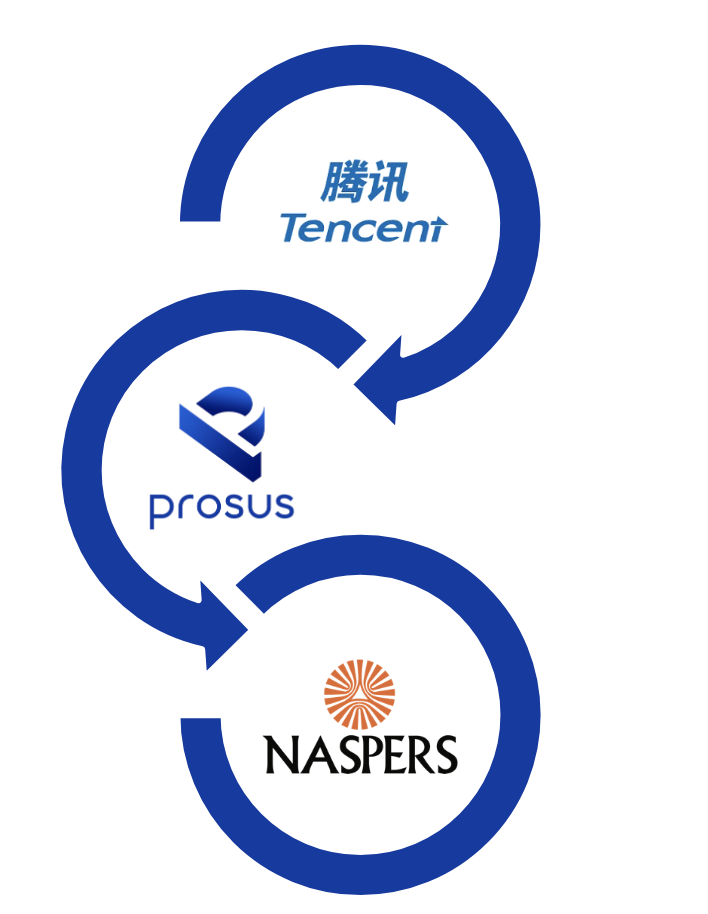

After two decades of technology investing, including China’s Tencent and Russia’s VK (formerly known as Mail.ru Group), Naspers amassed a huge portfolio of tech companies that spanned across the world. In 2019, it decided to spin out that portfolio into a separate entity called Prosus (the Latin word for “forward”) and listed it on the Euronext Amsterdam stock exchange in the Netherlands. Why list there? Likely because the Dutch has had a long history of doing international businesses, thus its exchange is more experienced in working with the cross-border accounting, taxation, and other corporate finance complexities that Prosus’s portfolio uniquely needs.

So 105 years after Naspers’s founding (and 18 years after its “marriage” with Tencent), it gave birth to Prosus – its global technology investment “baby”. As of today, Naspers holds 42% of Prosus.

Because of this rather complex history and low-key nature of both entities, the Naspers-Prosus brand is confusing and not well-known, even in the investing community and among tech founders today. (Personally, I did not pay attention to Prosus until its 2021 acquisition of Stack Overflow, a popular Q&A forum site among engineers, which I used frequently when I was a computer science student.)

In the rest of this post, for the purpose of both simplicity and (hopefully) clear writing, I will use “Naspers” and “Prosus” interchangeably, depending on the timing of the event in discussion – before 2019 will be Naspers, after 2019 will be Prosus.

“Finding” Tencent: A Mutual Rescue

Most famous investment stories are told either through the lens of an astute investor, who found a diamond in the rough due to his keen intuition, or the eyes of a tenacious founder, who convinced a powerful investor through his world-changing vision and grit. The reality is always more messy and haphazard, less straightforward and inspirational. The Naspers-Tencent story is no different.

Naspers did not find Tencent, nor did Tencent find Naspers. Instead, they found each other out of a combination of desperation and conviction that ended up rescuing each side from total failure.

In 1997, Naspers was an Internet pioneer in South Africa, having started one of the country’s first online portals called MWeb, which included messaging, blogging, email, gaming, and every product you could imagine in a web 1.0 business. But because of Africa’s tiny online population, MWeb did not succeed.

In the same year, Naspers, with its $2.2 billion windfall from selling its European paid TV business, started establishing itself in China. Its initial game plan was to leverage its technology expertise and decades of business experience to build its own Internet business. Naspers launched a series of web portals in China and invested in a few others, but they were all out-competed by home-grown leaders, like Sina, Sohu, and Netease – losing millions of dollars in the process. Naspers was getting desperate and running out of ideas.

In an almost parallel universe, Tencent, which got started in 1998 and launched QQ (a PC-based messaging service and precursor to WeChat) in 1999, was also growing desperate. QQ was wildly popular and eating up server costs like a bear coming out of hibernation. However, it had no business model and the company was running out of money. In April 2000, as the dotcom bubble began to burst in the US, Tencent managed to wrestle $2.2 million in investment from IDG and another firm, only to burn through that cash by the end of that year. Unwilling to invest more, IDG started to shop Tencent around to potential buyers to salvage what it surely thought at the time was a failed investment. Sina, Sohu, Yahoo China, and just about every sizable Chinese Internet outfit got a look at buying Tencent – and they all declined. (The common rationale was they could all build a QQ-like messenger themselves if they wanted to.)

It was at this moment of joint desperation for both Naspers and Tencent that the two companies’ paths crossed. Some accounts suggested that IDG eventually shopped the Tencent deal to Naspers when its China division, MIH, was running out of money and had barely enough funds left to make an investment. After a full year of deliberation, Naspers headquarters greenlighted the $34 million investment into Tencent. Some other accounts painted a more “romantic” encounter, where an MIH executive, David Wallerstein, kept on seeing QQ in every Internet cafe he visited in China, got intrigued, found Tencent’s office address, and went to visit the company to start negotiating an investment.

The real story is likely a combination of both tales. Given that Naspers’s Tencent investment did happen in mid-2001, it is quite possible that this investment was Naspers’s last ditch effort in China, with all of its own initiatives failing and the tech bubble bursting. Because MIH was a corporate investment arm, the year-long back and forth deliberation between the in-country team and corporate HQ in South Africa also makes sense and is typical of a corporate investment timeline and process.

That being said, the unique insight and high-level of conviction that Naspers had of Tencent should not be discounted. During this 2000-2001 timeframe, QQ’s user base was in the millions and had already surpassed the entire Internet user base of Africa. This fact may not have impressed Sina or Netease, but Naspers, with the scars of its failed MWeb venture in mind, came to China with a “prepared mind”. Seeing a 3-year-old Tencent already amassing a user base larger than its home continent with no end in sight, Naspers could care less that QQ did not have a business model, when lack of users was what doomed MWeb. This conviction, whether individually or collectively achieved inside Naspers, may also explain why Wallerstein joined Tencent in 2001 and still serves as its so-called Chief eXploration Office (CXO) today.

In more ways than one, Naspers and Tencent saved each other, via a confluence of desperation and conviction. This stands in contrast to the Softbank-Alibaba story, where neither elements were present. As documented in Sebastian Mallaby’s new chronicle of the VC industry, “The Power Law”, Masa Son got access to Alibaba in 2000, because Goldman Sachs Asia was getting cold feet about its batch of early Chinese tech investments and wanted to offload them to someone else. (This was similar to IDG’s situation with Tencent.) Back then, Masa Son’s was fresh off of his victory investing in a pre-IPO Yahoo, had capital to deploy, was not (and still is not) price sensitive, had a vague inkling that China’s Internet is booming because Cisco networking equipments were selling well there (he was on the Cisco board), thus invested in several companies that Golden offered to him, including Alibaba.

Softbank was not desperate then (though Alibaba was). Softbank also did not have the level of insight and experience operating an Internet business that Naspers had then. Masa Son, more or less, sprayed and prayed on Goldman’s China portfolio, and only Alibaba turned out to be a home run.

Holding On To A Rocketship

If the Naspers-Tencent relationship started off with a dose of desperation and luck, strong conviction and intentional long-term ownership anchored this investment for the following two decades as the Tencent rocketship took off.

Here is a brief breakdown of Naspers’s ownership stake in Tencent during the years before its IPO:

- 2001: 32.8% – from the first $34 million investment, acquired from Tencent’s two outside investors, IDG and Yingke

- 2002: 46.5% – acquired from a group of Tencent founders (except Pony Ma); Tencent founders now owned 46.3%, IDG owned 7.2%

- 2003: 50% - pre-IPO cap table restructuring acquired IDG’s remaining stake; Tencent founders owned the other 50%

- 2004 Tencent IPO: Naspers owned 37.5% immediately post-IPO; Tencent founders owned 37.5%

Naspers and the Tencent co-founders basically own the same proportion of the company throughout much of its lifetime. Due to an extraordinarily high degree of conviction and the convenient reality that these investments were made off of a corporate balance sheet with no outside investors (thus none of the pressure to sell that comes with them), Naspers did not sell a single share of Tencent for the first 14 years since the IPO. Because of its Tencent stake, Naspers was for a while the most valuable company in all of Africa in 2017 — not bad for making good use of lessons from a failed website.

Furthermore, Naspers’s stake is enhanced by Tencent’s own mastery in capital allocation and investing, beyond building WeChat, a massive gaming business, a growing advertisement business, and a cloud computing platform. Tencent’s portfolio does not only bolster the who’s who of China tech’s big winners (Pinduoduo, JD, Meituan, NIO, etc.), but also brand name American tech companies (Snap, Reddit, Epic Games, etc.), and new winners from other emerging markets (e.g. Nubank from Brazil, SEA Group from Southeast Asia).

By adding to its holding, then holding on that holding, Naspers has been compounding from a three-part flywheel: Tencent’s own growth, Tencent’s investment portfolio’s growth, funds to build Naspes’s own investment portfolio – all of which eventually became Prosus.

Naspers and Softbank are similar in this regard. Both did not sell their respective stakes in Tencent and Alibaba for a long time. Both also had the advantage of never being forced to sell, because they made the investments using their own money, not someone else’s money.

That similarity, of course, stopped when Masa Son decided to raise Vision Fund I, which did include (a lot of) outside money. To fund a portion of Vision Fund I and to buy Arm, Softbank started selling Alibaba shares in 2016, about 16 years after Masa Son saw Jack Ma’s strong, shiny eyes. Naspers held on to all of its Tencent shares until 2018, about 17 years after it wrote that first check, by selling 2% to shore up its own balance sheet and fund new opportunities, like buying Stack Overflow for $1.8 billion and capitalizing its venture arm, Prosus Ventures.

This year, both companies announced more selling of their shares, albeit in very different fashion.

Hitting Rough Times

As the global macro economic environment deteriorates, Softbank, Prosus, and every company that invests in technology is feeling the pain. In his usual dramatic way, Masa Son announced Softbank’s vomit-inducing quarterly loss of $24.5 billion last month with a portrait of Japan’s first shogun, to show both his desire to repent for his mistakes and his courage to come back victorious. To make up for all the losses in the meantime, he plans to sell more Alibaba shares. The drama dominated headlines for days, which I discussed in a previous post.

A couple of months earlier, in June, Prosus also announced more selling of its Tencent shares to keep improving its balance sheet, fund share buybacks, and boost its financial position during a tough, uncertain time. As the “Softbank without the drama”, Prosus made its announcement in a typically boring earnings press release.

Softbank is likely in a more dire state, having taken huge outside investments from Saudi Arabia and Abu Dhabi to fuel Vision Fund I, which took big swings at Uber, Didi, and WeWork – all of which are bad judgments that Masa Son has publicly admitted. Its portfolio of private companies will follow suit with valuation write-downs later this year.

Having taken no outside money, Prosus’s more quiet, conservative approach puts it in a better position to weather the storm. This is not to say that Prosus’s future is any more easy or certain than Softbank’s. Because of Russia’s invasion of Ukraine, Prosus had to write off its 27.29% stake in VK, worth roughly $760 million. Tencent’s stock price has dropped more than 60% since its February 2021 peak. Its global investment portfolio is also facing double scrutiny, from Chinese regulators for antitrust reasons and US regulators for geopolitical concerns.

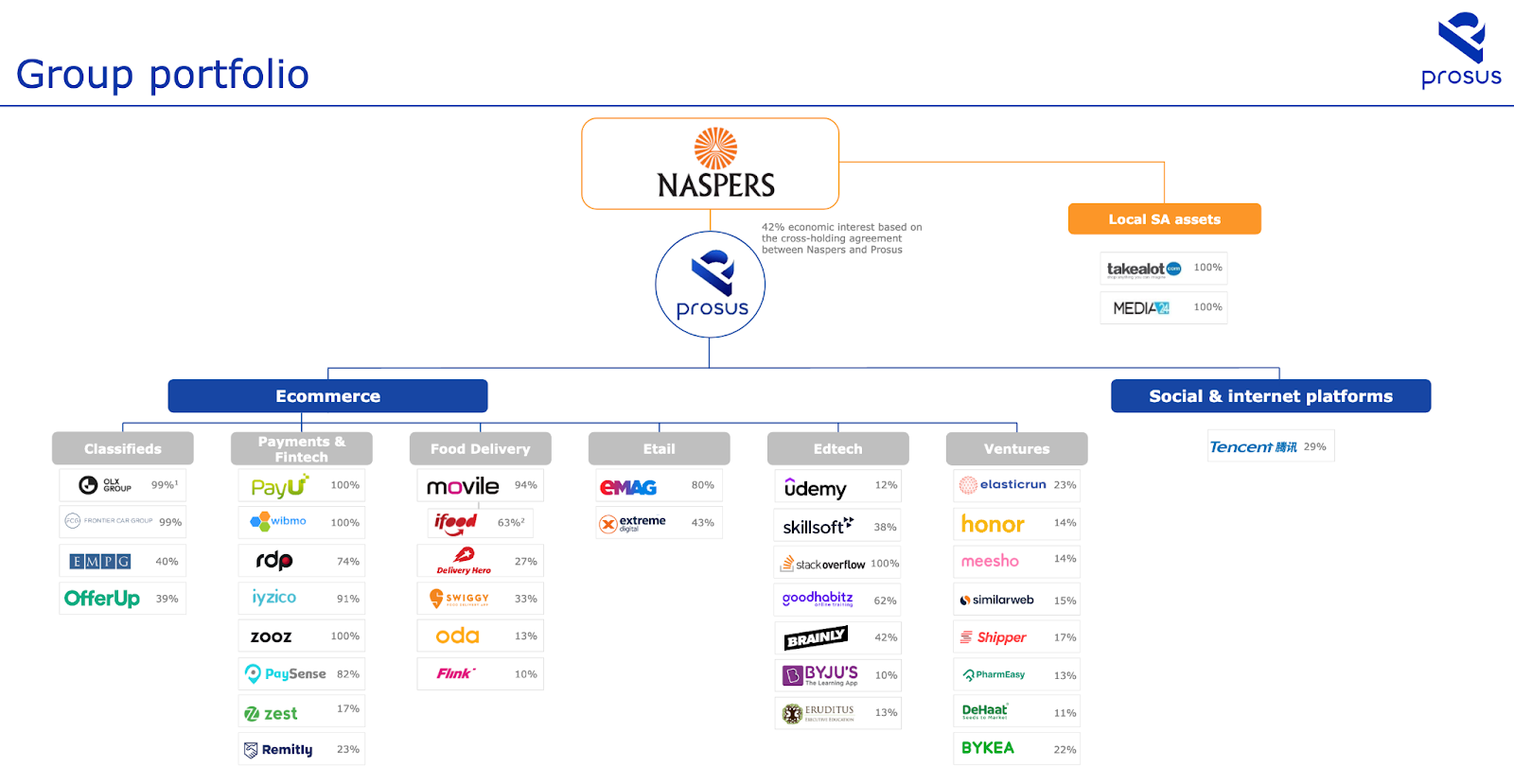

However, Prosus Ventures has continued to pour money into fast-growing tech companies in emerging markets. Notably, during its most recent fiscal year, out of the $900 million worth of investment it made, $800 million went to startups in India.

Here is a picture of the Prosus portfolio based on its recent earnings release:

Prosus now sports an enviable portfolio of public and private tech companies comparable to Softbank’s – spanning an interconnected set of categories, including classified, fintech, delivery, edtech, blockchain, and more. This is made possible largely because of that $34 million dollar check it wrote to Tencent 21 years ago and the steady, shrewd, and long-term shareholder behavior it displayed since – no drama, no fanfare.

Both Softbank’s high-profile style and Prosus’s low-key approach have their own benefits and drawbacks. Both will likely never change their respective ways. It will no doubt be interesting to see who will do better in the future. But we probably all know whose story will always get told more, regardless of the result.

Prosus: 平行宇宙里的软银

(本篇中文版文章是读者 Ben Yu 做的编译,我做了一些修改后发表。非常感谢Ben的贡献!)

如果问你:“有史以来最成功科技投资是哪一笔?”,你的答案会是什么呢?

很多人都会想到软银早期投资阿里巴巴。2000 年,孙正义以 2000 万美元押注马云的传奇故事广为流传(有关这个故事,可以看这个视频),最终为软银带来了超过 4500% 的回报。尽管最近软银和阿里都在谷底,但没有人会质疑当时这笔投资对软银、阿里、中国乃至整个科技界带来的影响。

但很多人不知道的是,大约同一时间,还有另外一笔投资也发生在一家刚刚起步的中国科技公司身上,同样也是由一位非中国投资者投的,最后获得了超过 8000% 的回报——2001 年,Naspers/Prosus 投资腾讯 3400 万美元。

一方面,孙正义本人的性格让他容易受人瞩目,这也让软银的关注度比较高。当然这种关注度到今天也依然在——软银出售了阿里股票,来拯救自己的资产负债表,摆脱愿景基金的巨额亏损。

而回到 Naspers/Prosus 投资腾讯上,这笔投资是前 Naspers CEO Koos Bekker 推动的,他为人低调,和孙正义截然不同。这笔投资和软银/阿里有相似之处,但也有鲜明的区别和值得学习的要点,这也是为什么我想要分享和这笔投资有关的故事。与其他任何一笔科技投资相比,这一笔更能体现全球化趋势与投资之间的紧密关系。以及,如果站在足够长的时间线里,押对一次公司可以带来的回报到底有多大。

Naspers/Prosus 到底是家什么公司?

这个故事不为人熟知的一个很大的原因是投资者的历史、品牌和身份都让人倍感困惑。

Naspers 是什么?Prosus 是什么?是南非的还是荷兰的公司?

让我们先来简单梳理一下 Naspers 和 Prosus 之间的关系。

Naspers 是一家成立于 1914 年的南非综合媒体。它最初是一家出版公司,在整个 20 世纪发展壮大,在南非复杂的历史中发挥了重要作用,包括与南非实行种族隔离的国民党有争议的结盟。

在 20 世纪 80 年代和 90 年代,Naspers 成功地拓展了电信和付费电视业务。1994 年,该公司成为南非证券交易所上市公司(其股票至今仍在交易)。几年后,在 Koos Bekker(在 1997 年成为 CEO)的领导下,Naspers 以大约 22 亿美元的价格出售了其收费电视业务的欧洲部分,为在互联网刚刚起步时进军中国、俄罗斯和其他新兴市场提供了资金。

20 年间,Naspers 积累了一个跨越全世界的庞大科技投资帝国,包括中国的腾讯和俄罗斯的 VK 公司 (2021 年之前被称为 Mail.ru 集团)。2019 年,该公司决定将这一投资组合分拆为一个名为 Prosus 的独立实体(拉丁语中表示“前锋”的意思),并将其在荷兰阿姆斯特丹证券交易所上市。之所以选择荷兰,可能是因为荷兰人有长期从事国际业务的历史,因此他们的交易所在处理跨境会计、税务和其他公司金融复杂性方面更有经验,而这些正是 Prosus 需要的。

也就是说,在 Naspers 成立 105 年、投资腾讯的 18 年后,它孵化出了 Prosus。今天为止 Naspers 持有 Prosus 42% 的股份。

由于 Naspers 和 Prosus 的历史相当复杂,而且两家公司的性质都很低调,即使在投资界和当今的科技创始人中,该品牌也令人困惑,不为人所知。(就我个人而言,直到 2021 年 Prosus 收购 Stack Overflow 之前,我都没有关注过它。 Stack Overflow 是一个深受工程师欢迎的问答论坛网站,当我还是CS专业的学生时,经常用它。)

在这篇文章的其余部分,我会交替使用“Naspers”和“Prosus”,这取决于讨论事件的时间点——2019 年之前将是 Naspers,2019 年之后将是 Prosus。

“寻找”腾讯:相互成就

对于观众来说,喜闻乐见的投资故事要么是一个聪明绝顶的投资人凭借自己敏锐的直觉,从废墟中发现一颗钻石,要么是一个目标坚定的创始人有着改变世界的远见和勇气,最终打动了投资人。但现实往往没有那么戏剧性,Naspers 和腾讯的故事就是如此。

实际上,Naspers 没有找到腾讯,腾讯也没有找到 Naspers。相反,他们是在绝望和信念的共同作用下找到彼此,最终双方互相成就。

1997 年,Naspers 是南非的互联网先驱,创建了该国最早的门户网站之一 MWeb,其中包括信息、博客、电子邮件、游戏以及所有你能想象到的 web 1.0 业务中的产品。但是由于非洲在线人口很少,MWeb 没有成功。

同年,Naspers 通过出售其欧洲付费电视业务获得了 22 亿美元的意外之财,开始在中国站稳脚跟。它最初的计划是利用其技术专长和几十年的商业经验来建立自己的互联网业务。Naspers 在中国推出了一系列门户网站,并在其他一些门户网站上进行了投资,但它们都被新浪、搜狐和网易等本土领军企业击败,在此过程中损失了数百万美元。Naspers 已经走投无路,无计可施了。

同一时刻,腾讯的处境也异常艰难。腾讯成立于 1998 年,1999 年推出了 QQ。虽然 QQ 的用户量很大,但没有找到商业模式,资金也快要见底。2000 年 4 月,随着美国互联网泡沫开始破灭,腾讯设法从 IDG 和另一家公司获得了 220 万美元的投资,但到当年年底,这笔资金就被烧光了。由于不愿加大投资力度,IDG 开始与潜在买家牵线出售腾讯。新浪、搜狐、雅虎,以及几乎所有规模较大的中国互联网企业都拒绝收购腾讯,理由很简单,他们认为只要他们想做就可以随时自己做出一个 QQ。

在这种情况下,Naspers 和腾讯相遇。一些报道称,IDG 最终向 Naspers 出售了这笔腾讯交易,当时其中国部门 MIH 资金短缺,几乎没有足够的资金进行投资。经过整整一年的考虑,Naspers 总部批准了对腾讯 3400 万美元的投资。有一些报道则描绘的更为浪漫:MIH 的一位高管 David Wallerstein 在中国访问的每家网吧都能看到 QQ,激起了他的兴趣,找到了腾讯的办公地址,然后立即前往办公楼找马化腾,开始谈投资。

现实情况可能是两个故事的结合。鉴于 Naspers 在腾讯的投资确实发生在 2001 年年中,这笔投资很可能是 Naspers 在中国的最后一笔投资,其自身的所有举措都以失败告终,科技泡沫也随之破裂。由于 MIH 是一个企业投资部门,国内团队和南非企业总部之间长达一年的反复讨论也是典型的企业投资时间表和流程。

尽管如此,Naspers 对腾讯的独特洞察力和高度信念不应被忽视。在 2000-2001 年的时间框架内,QQ 的用户基数达到了数百万,已经超过了整个非洲的互联网用户基数。这一事实可能没有给新浪或网易留下深刻印象,但 Naspers 带着 MWeb 的失败带来的教训,带着“有备而来”的心态来到中国。看到一个成立 3 年的腾讯已经积累了比其本土大陆还要多的用户基础,而且还在持续增长,Naspers 并不在乎 QQ 还没找到商业模式,因为它知道缺乏用户基数才是更大的问题。这种信念下,无论是个人的还是集体的,都可以解释为什么 Wallerstein 在 2001 年加入腾讯,直到今天仍然担任其所谓的首席探索官(CXO)。

在很多方面,Naspers 和腾讯因为自身的发展、遇到的挑战而相遇,并成就彼此,这和软银与阿里的故事形成了鲜明对比。正如 Sebastian Mallaby 在风险投资行业的新编年史《The Power Law》中所记载的那样,孙正义在 2000 年投阿里,因为高盛亚洲对其早期的一批中国科技投资打怵了,希望将它们出售给其他公司(这与 IDG 与腾讯的情况类似)。当时,孙正义刚刚获得胜利,投资了上市前的雅虎,有资金配置,对价格并不敏感。当时对中国互联网有一个模糊的概念,觉得会蓬勃发展,因为思科的网络设备在那里卖得很好(他当时是思科董事会成员),因此孙正义投了好几家公司,其中就包括阿里。

当时软银没有遇到挑战,只有阿里需要帮助。软银也没有 Naspers 那时的洞察力和经营互联网业务的经验。在孙正义当时投的所有公司里,结果也只有阿里巴巴表现出色。

坐上要起飞的火箭

Naspers 与腾讯的关系,也让 Naspers 在随后 20 年里高速发展。

以下是 Naspers 在腾讯 IPO 前几年所持股份的各个阶段:

- 2001 年:32.8% ——第一笔 3400 万美元的投资,来自腾讯的两个外部投资者——IDG 和盈科。

- 2002 年:46.5%——从一群腾讯创始人手中收购(马化腾除外),腾讯创始人彼时拥有 46.3% ,IDG 拥有 7.2%。

- 2003 年:50% ——上市前的资产负债表重组收购了国际数据集团的剩余股份,腾讯创始人拥有剩余的 50%。

- 2004 年腾讯 IPO:上市后 Naspers 持股 37.5% ,腾讯创始人持股 37.5%。

Naspers 持有的股份在大部分时间里都和腾讯联合创始人持有的比例相同。基本可以确定的是这些投资是在没有外部投资者的公司资产负债表之外进行的(因此没有随之而来的出售压力),Naspers 在腾讯上市后的头 14 年里没有出售过一股股票。由于持有腾讯的股份,Naspers 在 2017 年一度成为全非洲市值最高的公司——而回到故事的开始,一切的缘起来自于一个失败的项目。

此外,腾讯自身在资本配置和投资方面的成功,加大了 Naspers 的持股比例。除了微信外,腾讯的游戏业务、广告业务和云计算服务也在不断增长。腾讯投资的项目不仅包括很多今天耳熟能详的科技公司(拼多多、京东、美团、蔚来汽车等等),还包括美国的科技公司品牌(Snap、 Reddit、 Epic Games 等),以及其他新兴市场的头部玩家(例如巴西的 Nubank、东南亚的冬海集团)。

通过持有这些股份,Naspers 一直在从以下三个方面增长:腾讯自身的增长、腾讯投资组合的增长、构建 Naspers 自身投资组合的资金——所有这些最终都变成了 Prosus。

Naspers 和软银在这方面是相似的。长期以来,两家公司都没有出售在腾讯和阿里的股份。这两家公司的优势还在于从未被迫出售,因为他们用自己的钱进行投资,而不是别人的钱。

当然,这种相似性在孙正义决定筹集愿景基金 I 时消失了,该基金的确包括很多外部资金。为了为愿景基金 I 提供部分资金,并收购 ARM,软银从 2016 年开始就在出售阿里股票。而 Naspers 持有所有腾讯股票直到 2018 年,通过出售 2% 的股份来支撑自己的资产负债表,并为新的市场机会提供资金,比如以 18 亿美元收购 Stack Overflow 并为其风险投资部门 Prosus Ventures 注资。

今年,两家公司都宣布了更多的股票出售计划,尽管出售方式截然不同。

遭遇艰难时期

随着全球宏观经济环境的恶化,软银、Prosus 和每一家投资于科技公司都感受到了衰退。孙正义以他惯常的戏剧性方式宣布,上个月软银的季度亏损达到 245 亿美元,同时还配图日本第一位幕府将军的画像,以表明他愿意为自己的错误忏悔,并有勇气再次获胜。与此同时,为了弥补所有损失,他计划出售更多阿里股票。这则新闻连续几天占据头条,我在之前写的文章里也深度讨论过这个事情。

在今年 6 月份,Prosus 也宣布进一步出售其在腾讯的股票,以保持其资产负债表状况的改善,基金股票回购,并在一个艰难而不确定的时期提升其财务状况。Prosus 不像软银那么戏剧性,它是在一份典型而乏味的财报发布会上宣布这一消息的。

软银的处境可能更为糟糕,它从沙特阿拉伯和阿布扎比获得了巨额外部投资,以推动愿景基金 I 的发展。该基金在Uber、滴滴和 WeWork 上大幅波动,孙正义公开承认这些都是错误的投资判断。今年晚些时候,该公司的私营企业投资组合也将进行估值减记。

由于没有接受任何外部资金,Prosus 更低调,这种保守的做法使其处于更有利的地位,能够经受住衰退的考验。这并不是说 Prosus 的未来比软银的更容易或更确定。由于俄罗斯入侵乌克兰,Prosus 不得不注销其在 VK 公司 27.29% 的股份,价值约 7.6 亿美元。自 2021 年 2 月达到峰值以来,腾讯股价已下跌超过 60% 。其全球投资组合也面临着双重审查,一方面是中国监管机构出于反垄断原因,另一方面是美国监管机构出于地缘政治考虑。

然而,Prosus 在继续向新兴市场快速增长的科技公司投入大量资金。值得注意的是,在最近一个财政年度,在其 9 亿美元的投资中,有 8 亿美元流向了印度的创业公司。

下面是根据 Prosus 最近发布的收益情况对其投资组合进行的描述:

Prosus 现在拥有一个令人羡慕的上市和私有科技公司组合,可与软银媲美——跨越一系列相互关联的类别,包括广告分类、金融科技、配送、教育科技、区块链等等。而这一切之所以会发生,很大程度上是因为它在 21 年前开给腾讯的 3400 万美元支票,以及自那以后表现出的稳健、精明和长期股东的行为——低调沉稳地做着一切。

软银的高调风格和 Prosus 的低调做法各有利弊。双方可能永远不会改变各自的方式。看看谁将来会做得更好,无疑是件有趣的事情。当然我们也都知道,无论结果如何,软银的故事总是会被更多人口口相传。