In the Chinese startup ecosystem, no advice is more viral than this line: “if you stand where the wind blows, even a pig can fly.” It was coined by Lei Jun, the founder and CEO of Xiaomi, chairman of Kingsoft, and a prolific angel investor.

Amidst the wind of electric vehicle (EV) adoption that’s blowing across the world, there appears to be not one, but two “pigs”, that may be flying: CATL and CALB.

CATL is currently the world's largest battery maker by installed production capacity, already well-known in the EV industry, and well-covered by mainstream media outlets. It supplies major EV makers from Tesla and Honda, to Hyundai and Volkswagen. Its lesser-known rival, CALB, is actually an older company, suffered some setbacks, and is just starting to catch the EV wind again.

We briefly mentioned CALB in last week’s post, when discussing the potential opening of the Hong Kong Stock Exchange IPO window. Given the strategic importance of electrification not just to the technology and automotive sectors, but also many governments’ innovation agenda and in dealing with climate change, CALB deserves its own deep dive.

That’s what we will do today.

(Note: because the two companies' acronyms look almost identical and can be confusing, we are bolding the last two letters of CALB and CATL throughout this post, so readers can hopefully have an easier time seeing the two companies apart.)

First Mover (Dis)Advantage

CALB was conceived in 2007, predating CATL’s founding by four years. CALB was a venture within the Aviation Industry Corporation of China (AVIC), a state-owned enterprise in aerospace and defense, that was spun out later. It enjoyed a first mover advantage, focused on commercial EVs (because that was where government subsidies were going to), and became a market leader. In the 2012 Ministry of Industry and Information Technology’s public report on electric vehicles, CALB was ranked #1 in the number of EV models that use its batteries.

As it turns out, being first mover turned out to be more of a disadvantage – for two reasons.

The Government Gives and the Government Takes Away: in 2017, subsidies for commercial EVs ran out. This policy change spelled trouble for CALB and a whole host of other battery producers, whose business was primarily supplying that segment of the market. It ushered in a so-called “new energy winter” that lasted two years and almost killed CALB.

As the market began shifting towards consumer passenger EVs, CALB struggled to adjust while CATL took off. Why? Because of poor chemistry, not the human-kind, but the periodic-table-kind.

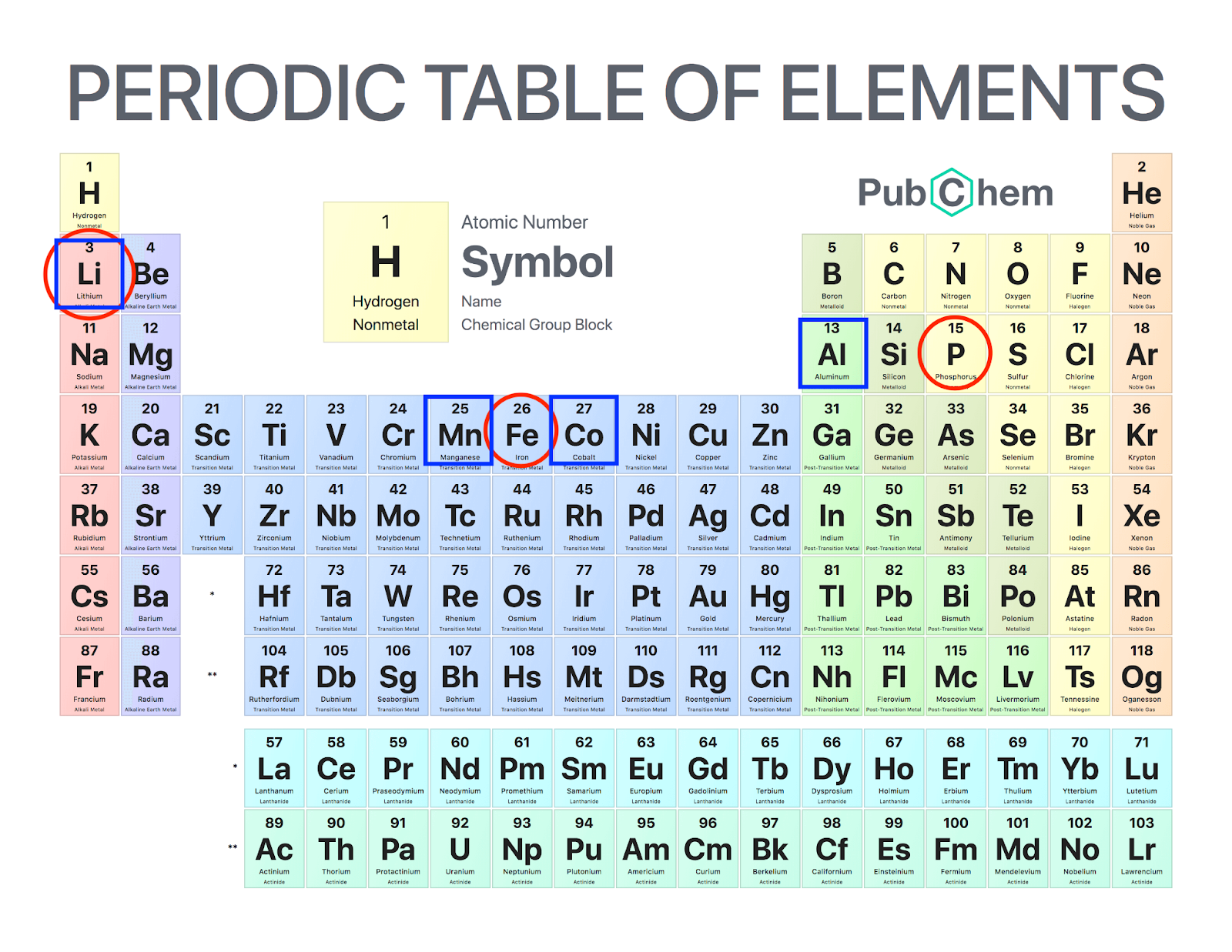

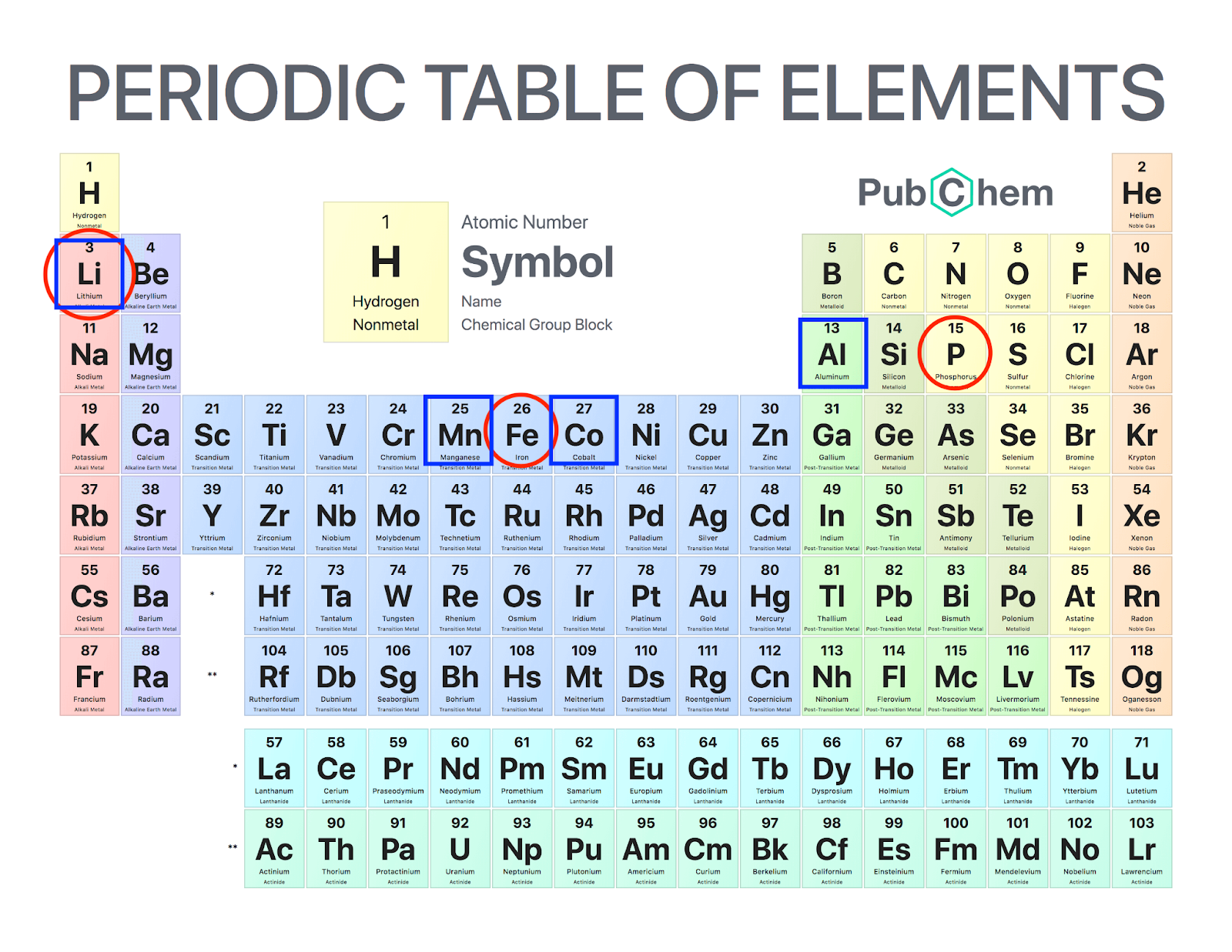

Poor Chemistry: broadly speaking, there are two types of lithium-ion batteries being used in EVs. One type is the lithium-iron-phosphate type, or LFP. The other category includes two subtypes: nickel-cobalt-aluminum (NCA) and nickel-manganese-cobalt (NMC), where nickel and cobalt are the new, key ingredients. I’ve circled (in red) the LFP elements and squared (in blue) the NCA and NMC elements in the periodic table below. (Lithium is, of course, in both types.)

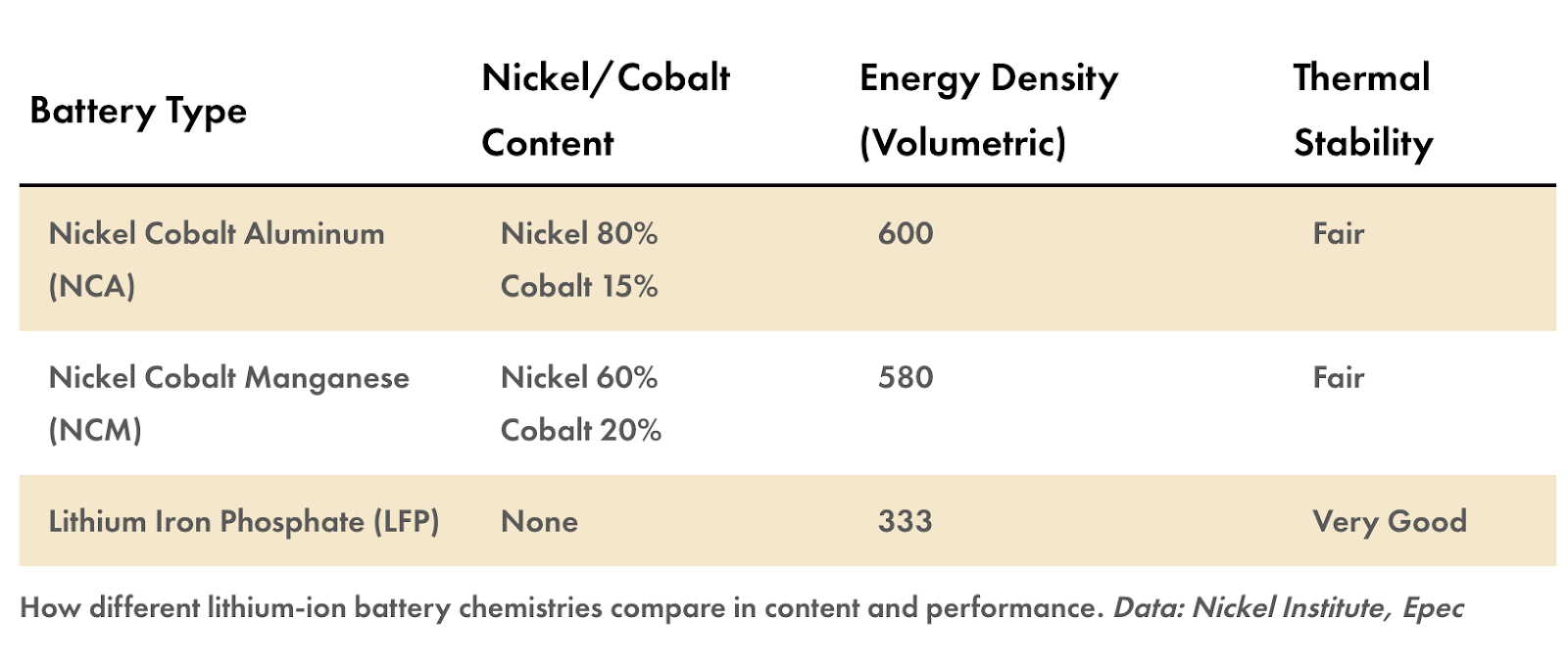

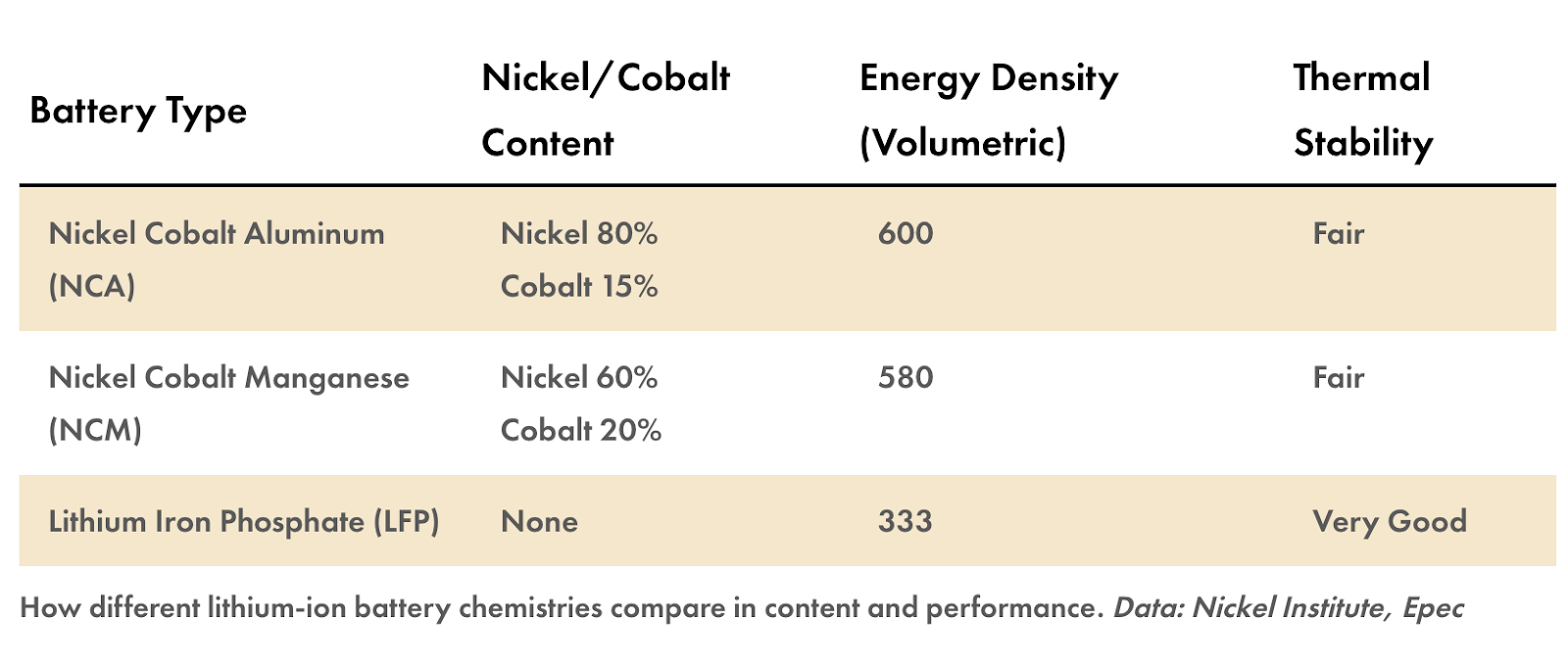

The key tradeoff between LFP and NCA/NMC is that LFP has lower energy density than NCA/NMC, but better thermal stability. In more plain language: EVs that have LFP batteries cannot go as far as EVs with NCA/NMC batteries before needing to recharge, but NCA/NMC heat up faster (so can cause fire) than LFP.

Want to go farther per charge? You might cause a fire. Don’t want to risk a fire? Then you would have to charge more often.

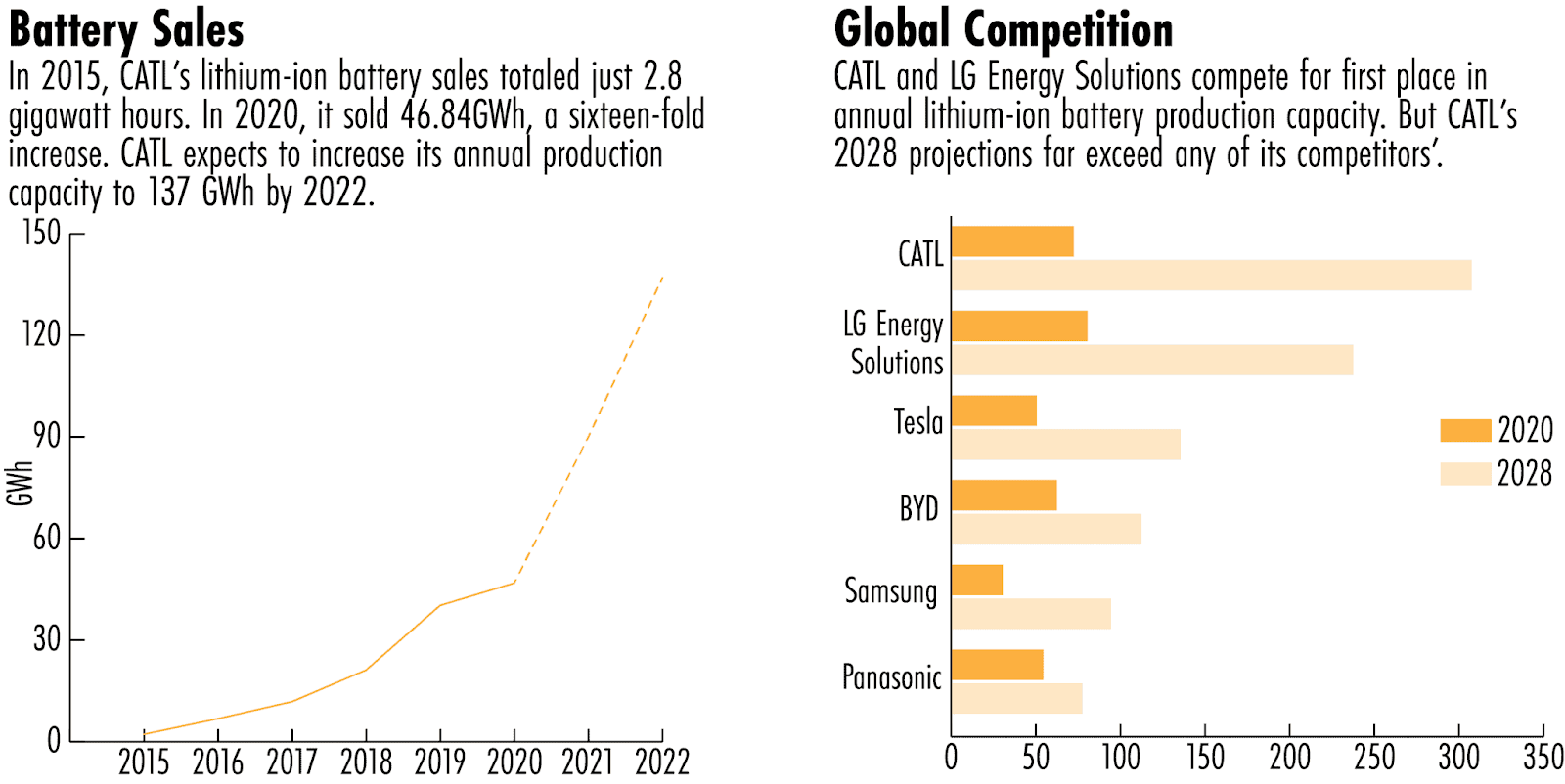

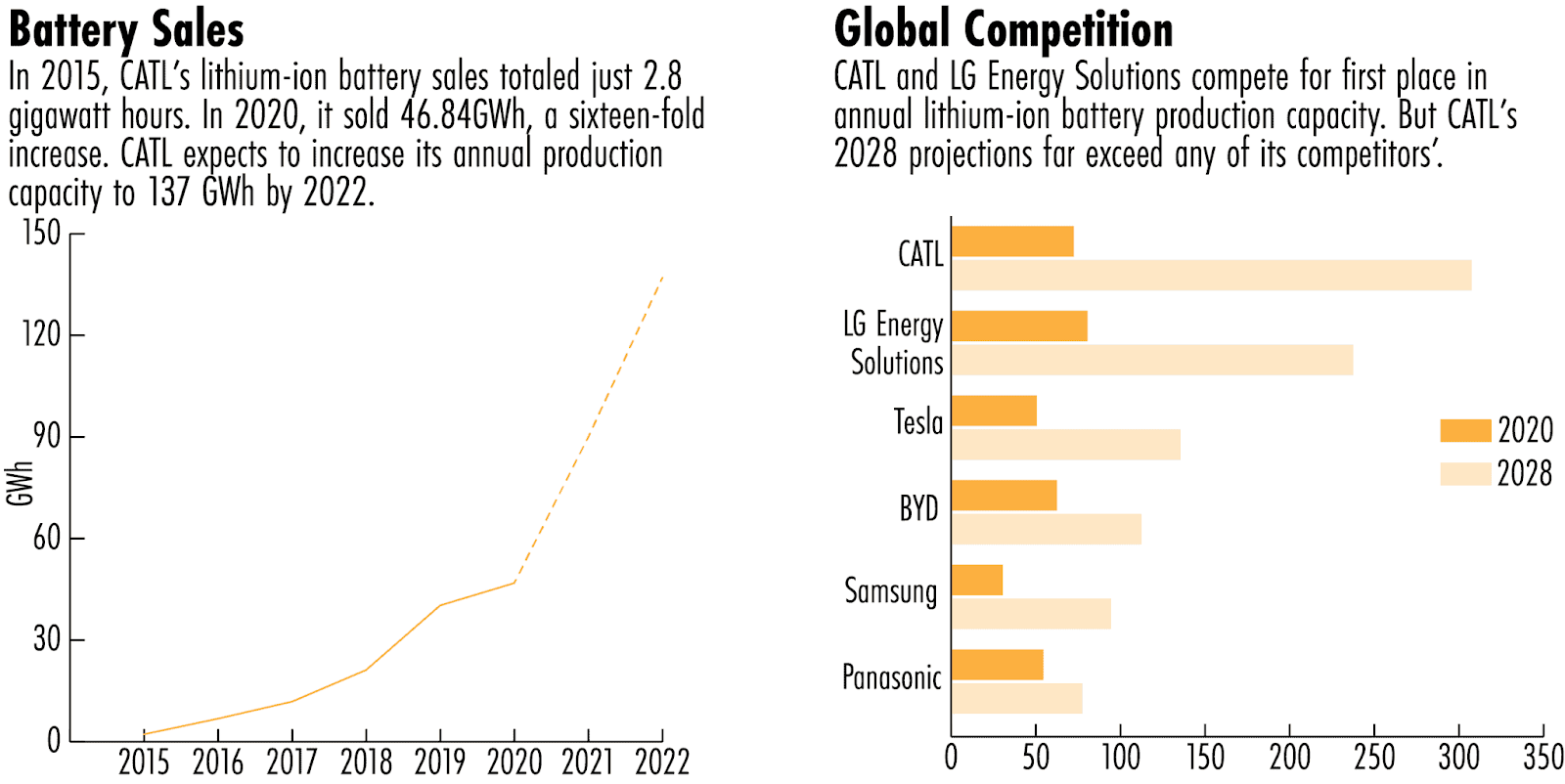

CALB began its journey with developing LFP batteries. As government subsidies waned and more passenger EVs needed longer distance between each recharge to be attractive to consumers, its batteries became less suited to the market’s direction. Meanwhile, CATL, which started developing NCA/NMC batteries early, took over! Additionally, CATL has been effective in vertically integrating its raw materials acquisition and manufacturing plants to keep the cost of production low, propelling it to the top of the list in both its China and global market share.

By 2020, only one battery “pig” was flying and that was CATL.

(Note: I have purposely not mentioned BYD in this post, even though it is also a big battery producer, because its batteries mostly supply BYD’s own EVs, thus quite different from pure play battery makers, like CATL and CALB.)

Major Turnaround

In July 2018, with CALB in dire state, a new boss was brought in to turn things around, Liu Jingyu.

A rare female executive in China’s high-tech sector, Liu already had a reputation for being a strong leader and effective “turnaround artist”. In 2013, she took over another struggling company that was affiliated with the Aviation Industry Corporation of China and steered it from massive losses to profitability in 10 months.

Two major reasons contributed to CALB’s turnaround. One has to do with Liu’s leadership. The other, ironically, has to do with its rival’s runaway growth.

All-in on NCA/NCM: with the market’s preference shifting, Liu wasted no time re-focusing the company’s overall strategy to be “all-in” on developing NCA/NCM batteries. In terms of go-to-market, it shifted direction to serving the consumer EVs market, not its original commercial customers.

CALB’s production of NCA/NCM batteries soon ramped up. And to recapture market share, it aggressively priced its products 20-30% lower than its competitors’. But where would it find customers in a new, somewhat unfamiliar consumer EVs market?

Answer: CATL’s customers

Be the cheaper backup supplier: perhaps a victim of its own success, CATL started having trouble supplying its larger customers, right around the time that CALB was going through its corporate restructuring. The first automaker that switched from CATL to CALB was Chang’an Automobile, one of the “Big Four” car manufacturers in China (albeit the smallest of the four).

The second, arguably more strategic, customer was Guangzhou Automobile Group (or GAC Group), China’s 5th largest automaker. In 2017, due to supply delays caused by CATL, GAC could not meet the delivery target of its new EV model, GE3. As GAC was looking for a backup option to CATL, either by working with another supplier or building its own battery, the newly-reformed CALB swooped in. Aftering locking in GAC, CALB’s prospects began to improve, as larger (and cooler) automakers, like Dongfeng, Geely, and XPeng, started using CALB in the same way.

On the back of this new “wind”, CALB’s installed production capacity doubled in each of the last three years – 2019: 107%, 2020: 128%, 2021: 132% – an unprecedented growth rate that would make even a high-flying SaaS company jealous.

Thanks to a strategic shift towards NCA/NCM batteries and willingness to be a cheap, reliable backup to the market leader, an old “pig” is flying again!

Global Top 3 and the Return of LFP?

GAC’s strategic logic for using CALB is quite similar to any large enterprise’s reasoning for adopting “multi-cloud” for its IT infrastructure. No large enterprise wants to be locked-in to Amazon’s AWS or Alphabet’s GCP forever. It would rather have options, redundancy, and a credible way to play one vendor off the other to negotiate better prices.

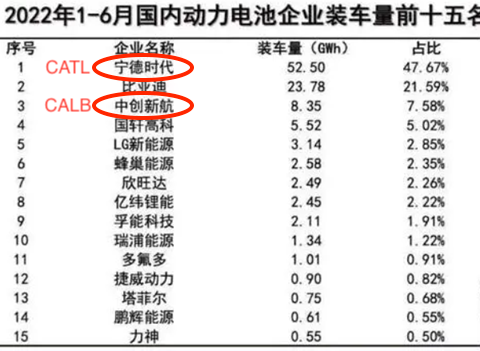

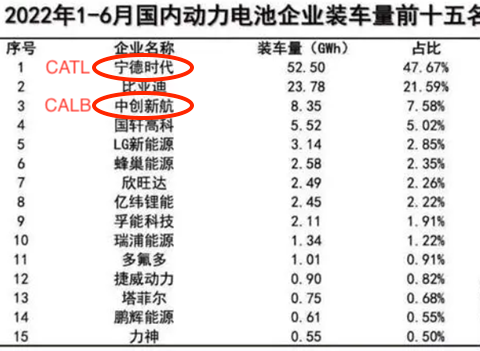

So far, this logic has helped CALB become a market leader in China. According to research done by the China Industry Technology Innovation Strategic Alliance for Electric Vehicle (an industry group and a mouthful), during the first half of 2022, CALB’s domestic market share is #3 at 7.58%, behind CATL’s 47.67% and BYD’s 21.59% (see chart in Chinese below).

To be clear, CALB still lags CATL by many many miles (or kilometers), but its incredible growth rate in the last three years makes it a noteworthy contender.

Also, being China’s #3 is not where CALB’s ambition lies. On the first day of its HKEX IPO, Liu proclaimed that her goal is to build CALB into a top-3 battery maker, globally. To reach that scale, CALB will have to become more than just a cheaper option and a negotiation chip for when customers want to haggle with CATL. CLAB will need to compete with Korean giants, like LG Energy and Samsung, Japanese conglomerates, like Panasonic, and CATL itself, who is taking serious note of its small domestic rival (and suing it for IP infringement).

If there is one wind blowing in CALB’s favor, it is the return of LFP – the type of lithium-ion battery that fell out of favor but is making a comeback. Due to the soaring prices of nickel and cobalt, and the unfortunate fact the vast majority of EV fires involve NCA/NCM batteries, more automakers now want LFP batteries – to reduce cost and improve safety.

Tesla has committed to building many of its entry-level Model 3’s with LFP. Volkswagen and Ford have announced similar commitments to LFP. CATL is pouring R&D dollars into its cell-to-pack technology to improve its LFP battery density without compromising on thermal stability (or safety), to keep customers like Tesla and others happy.

And which other Chinese battery maker actually started its journey with LFP? CALB!

LFP’s return to relevance is certainly an interesting turn of event, if not a historical opportunity, for CALB. How CALB will turn its lineage with LFP into a competitive advantage, if at all, remains to be seen.

As China’s own new energy agenda progresses, where hard requirements for using domestic suppliers will no doubt continue, CALB should sit comfortably near the top of its domestic market, as long as it does not screw up. Globally, more countries are also “domesticating” the supply and manufacturing chain of EVs to boost homegrown companies. A good recent example is the way President Biden’s Inflation Reduction Act works, where the new tax credit for EVs only applies to vehicles that are assembled domestically and their batteries are sourced and made domestically.

For a pig to fly, it needs to catch a wind that’s both blowing in the right direction and for a long time. While the LFP wind is blowing one way, the policy winds seem to be blowing in a different way. That makes “flying” for both CALB and CATL hopeful but complicated.

宁德时代和中创新航:风口中的电动车电池行业

(本篇中文版文章是读者 Ben Yu 做的编译,我做了一些修改后发表。非常感谢Ben的贡献!)

很多中国创业者都对雷军说的这句话耳熟能详:“站在风口上,猪都能飞起来。”

面对这次全球电动车浪潮,顺着风口备受关注的电池公司有两家:宁德时代和中创新航。

宁德时代是目前全球装机量最大的电池制造商,在电动车产业里是一家明星公司,被很多主流媒体报道过。它的客户包括特斯拉、本田、现代和大众等。中创新航虽然成立时间更早,但经历过几次业务挫折,直到这两年在电动车行业才开始逐渐为人所知。

在上周讨论公司在港交所 IPO 回暖的文章中,我们提到过中创新航。鉴于电气化不仅对技术和汽车行业,而且对许多政府的创新议程和应对气候变化有很强的战略意义,值得更深入了解中创新航这家公司。

先发优势还是先发劣势?

中创新航成立于 2007 年,比宁德时代还要早 4 年。中创新航是中国航空工业集团旗下的企业,该公司是一家从事航空和国防的国企,中创后来被独立剥离出来。早成立具有先发优势,专注于商用电动车(因为政府的补贴),并成为市场领导者。在 2012 年工信部关于电动汽车的公开报告中,中创新航的装机量全国排名第一。

然而现在回看,会发现在这个领域先发带来的劣势处处潜在。对中创来说,主要面对了两个劣势:

“政策红利”:在 2017 年,国家对商用电动车的补贴用完了。这一政策变化打击了中创新航和一大批其他电池制造商,因为他们的主要业务就是给这个市场供货。这股“新能源寒冬”持续了两年,中创新航差点没能挺过去。

随着市场开始转向大众消费者电动车,中创新航努力调整,而宁德时代则顺势起飞。为什么会有这样的差异?这就涉及到化学原理。

化学:广义上讲,有两种类型的锂离子电池被用于电动汽车。一种是磷酸铁锂电池(LFP),另一类三元电池包括两个子类型:镍钴铝(NCA)和镍钴锰(NCM),其中镍和钴是新的关键成分。我在下面的周期表中圈出了 LFP 元素(红色),并将 NCA 和 NCM 元素用方形(蓝色)表示(当然两种类型的元素都有锂)。

LFP 和 NCA/NCM 之间的关键区别是,LFP 的能量密度比 NCA/NCM 低,但热稳定性更好。用更通俗的话说,使用 LFP 电池的电动车在充电后不能像使用 NCA/NCM 电池的电动车那样开得远,但 NCA/NCM 比 LFP 升温更快(所以更可能引起火灾)。

即,想每次充完电能开的更远,就会有更高引发火灾的概率,而想要更安全就要更频繁地充电。

中创新航最开始开发的是 LFP 电池。随着政府补贴的减少和消费者级电动车需求的增加(消费者更在乎一次充电后的行驶距离),LFP 电池的需求也随之变少。与此同时,早早开始开发 NCA/NCM 电池的宁德时代开始崛起。另外,宁德时代一直积极垂直整合原材料采购和制造厂,以保持自己较低的生产成本,这都促使这家公司在中国和全球市场中领先其他竞争对手。

当时间快进到 2020 年的时候,所有电池供应商里遥遥领先的就只有宁德时代了。

(注意:我在这篇文章里没有提到比亚迪,虽然它也是电池供应商,但主要还是服务于自己品牌的电动车,和宁德时代、中创新航这样纯电池供应商有比较大的不同。)

弯道超车

2018 年 7 月,在中创新航陷入困境的时候,刘静瑜作为 CEO 加入,试图改善公司情况。

刘静瑜是中国科技公司里非常少见的女高管,她因为强有力的领导风格和卓有成效的盈利手段而被人熟知。2013 年,她接管了另一家陷入困境的公司,这家公司隶属于中国航空工业集团,并在 10 个月内扭亏为盈。

中创新航的转型有两个重要原因,一个和刘静瑜的领导能力有关,另一个则有一些戏剧化,主要是因为竞争对手增长太快了。

全部押注在 NCA/NCM:随着市场偏好的转变,刘静瑜接手后立即将公司的总体战略聚焦在开发 NCA/NCM 电池上,同时也转为服务那些消费者电动车公司,而不是原本的商务电动车客户。

中创新航的 NCA/NCM 电池的供给量迅速增加。为了夺回市场份额,中创新航将产品定价比竞争对手低 20%~30%。但首先的一个挑战是在一个新的、陌生的消费者电动车市场上,怎么找自己的客户?答案是:找宁德时代的客户。

成为更便宜的备用供应商:在中创新航转型的同时,宁德时代因为增长太快,供应能力开始吃力,越来越难及时服务更多客户。第一个转为选择中创新航的汽车品牌是长安汽车,中国“四大”汽车制造商之一(尽管是四大中最小的)。

第二个更具有战略意义的客户是中国第五大汽车制造商广州汽车集团。2017 年,由于宁德时代造成的供应延迟,广汽未能实现其新型电动汽车 GE3 的交付目标。当广汽寻找市场上其他选择时,转型后的中创新航进入视线中。有了广汽这个大客户后,中创新航的客户陆续增加,包括东风、吉利、小鹏等各大规模的电动汽车品牌。

在这个风口上,中创新航的装机量在过去三年里每年都翻一番:2019 年是 107% ,2020 年是 128% ,2021 年是 132%。这是一个前所未有的增长率,即使是一家激进的 SaaS 公司也会非常羡慕这种增长速度。

由于向 NCA/NCM 电池的战略转变,并愿意成为市场头部玩家的廉价、可靠的替代品,中创新航开始崛起。

全球前三的公司和 LFP 电池的市场回暖

广汽使用中创新航的战略逻辑和大型企业为 IT 基础设施采用多云的理由非常相似,因为没有大型公司愿意永远被 AWS 或 GCP 绑定,所以更愿意通过各种手段使用多家云服务供应商,并可以讨价还价,压低价格。

到目前为止,这种市场选择已经帮助中创新航成为中国市场的头部玩家,根据电动汽车产业技术创新战略联盟的研究,2022 年上半年,中创新航在国内市场的占有率为 7.58%,排名第三,落后于宁德时代的 47.67% 和比亚迪的 21.59%。

很明显中创新航仍然落后宁德时代很多,但其在过去三年的惊人增长率使其成为一个值得注意的竞争对手。

成为中国第三大电池制造商并不是中创新航的目标。在港交所上市的第一天,刘静瑜就宣称她的目标是将中创新航打造成为全球前三的电池制造商。为了达到这一规模,中创新航将不得不成为不仅仅是一个更便宜的选择,以及当客户想与宁德时代博弈价格的筹码。中创新航的竞争对手会包括韩国巨头(如LG能源和三星)、日本企业(如松下)以及宁德时代。宁德时代也开始关注,并正在就知识产权侵权清理国内的这家小型竞争对手。

中创新航现在有一个市场机会在于 LFP 电池需求的增加。虽然这种电池的需求下降过,但由于镍和钴价格的飞涨,以及大部分出事故造成火灾问题的电动车大多数都使用 NCA/NCM 电池,越来越多的汽车制造商希望采用 LFP 电池,以降低成本和提高安全性。

特斯拉正计划用 LFP 电池生产更多入门级的 Model 3。大众和福特也已经宣布了对 LFP 的类似使用计划。宁德时代正在投入研发资金,在不影响热稳定性或安全性的前提下,提高 LFP 电池的密度,从而让特斯拉和其他公司等客户满意。

还有哪家中国电池制造商曾有 LFP 的生产能力?答案当然是中创新航。

对中创新航来说,LFP 电池需求的回暖是非常戏剧性的转折。中创新航是否能够借助这个市场变化增强自己的竞争优势是非常值得关注的。

随着中国自己的新能源议程的进展,对使用国内制造商的硬性要求无疑将继续下去,不出意外的话,中创新航应该能够稳定占据国内市场的前几名。而在全球范围内,越来越多的国家也在将电动汽车的供应和制造链“本土化”,以促进本国公司的发展。最近的一个很好的例子是拜登的减少通货膨胀法案的运作方式,其中电动车的新税收优惠只适用于在国内组装的车辆,其电池也要求在国内采购和制造的。

企业需要顺势而为,抓住一个风口。LFP 电池回温,全世界电动车潮流继续,但各个国家政策又倾向“本土化”,各种风口似乎是相反方向在吹,这也让宁德时代和中创新航的未来发展变得复杂。