A couple of weeks ago, we published a detailed breakdown of China’s cloud industry’s current state of development, which resonated with many industry analysts and technologists. We combed through the official whitepaper published by the government-affiliated think tank, China Academy of Information and Communications Technology (CAICT), and combined our own domain knowledge.

The one-sentence answer to the rather broad, complex question of “how is China’s cloud industry doing?” is: China’s cloud transformation is still in its infancy and starting to permeate industries beyond the Internet tech sector.

With this observation in mind and as an investor, I could not help but think about how to “place bets” on China’s cloud. As news like the US government banning Nvidia from selling its cloud data center chips to China continues to complicate the future, how should one invest in the “walled garden” that is China’s cloud?

This post outlines my current thinking.

(The standard “this is not investment advice” disclaimer applies to this post and all Interconnected posts. Please do your own research before making any investment decisions.)

Gross Margins: IaaS vs PaaS vs SaaS

Before I name specific companies and discuss why they are either good bets or bad bets, it is important to first lay out the architectural differences between the three layers of a cloud (IaaS, PaaS, SaaS), their respective gross margins, and the business logic that connects these layers. These fundamentals are important for analyzing the potential of any cloud platform.

Here’s my plain language definition of these three layers:

- IaaS (Infrastructure-as-a-service, aka processors like CPUs/GPUs, storage units like SSDs or hard drives, and networking bandwidth for rent)

- PaaS (Platform-as-a-service, aka database, application development, big data analytics engine, AI/ML frameworks for rent)

- SaaS (Software-as-a-service, aka user-facing applications like email, workplace messaging, video-conferencing, document-sharing for rent)

In terms of gross margins, SaaS has the highest margin (more than 80%), PaaS the second highest (between 50-70%), and IaaS has the lowest (between 30-50%). While gross margins may vary by vendor and could be higher than the range I laid out, depending on economies of scale of data centers and the extent of automation implemented, these three ranges generally hold true. These gross margin differences also reflect the relative “value-add” that these three layers offer to their users – IaaS being the most commodity-like and least value-add, SaaS being the most, while PaaS sits in the middle.

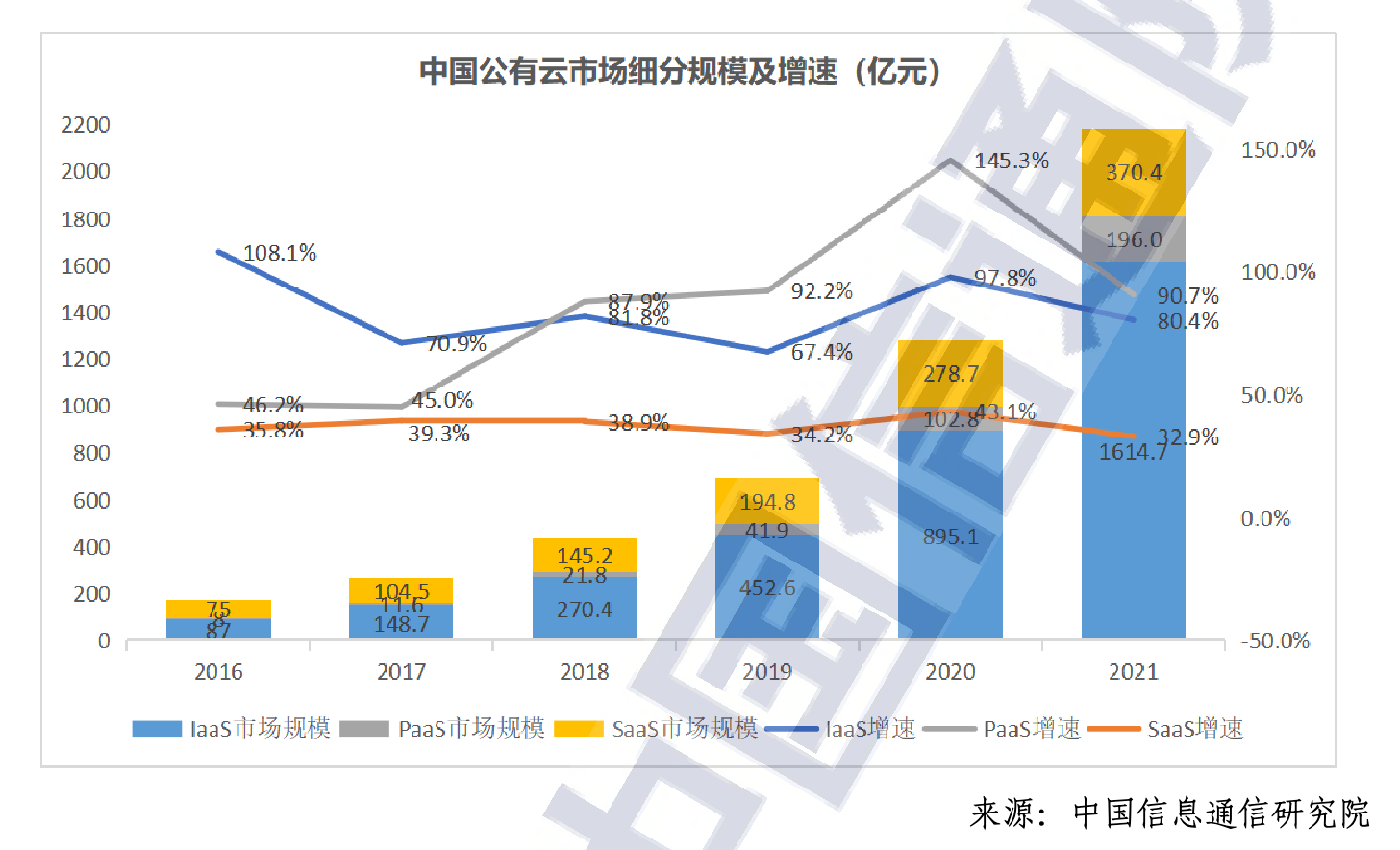

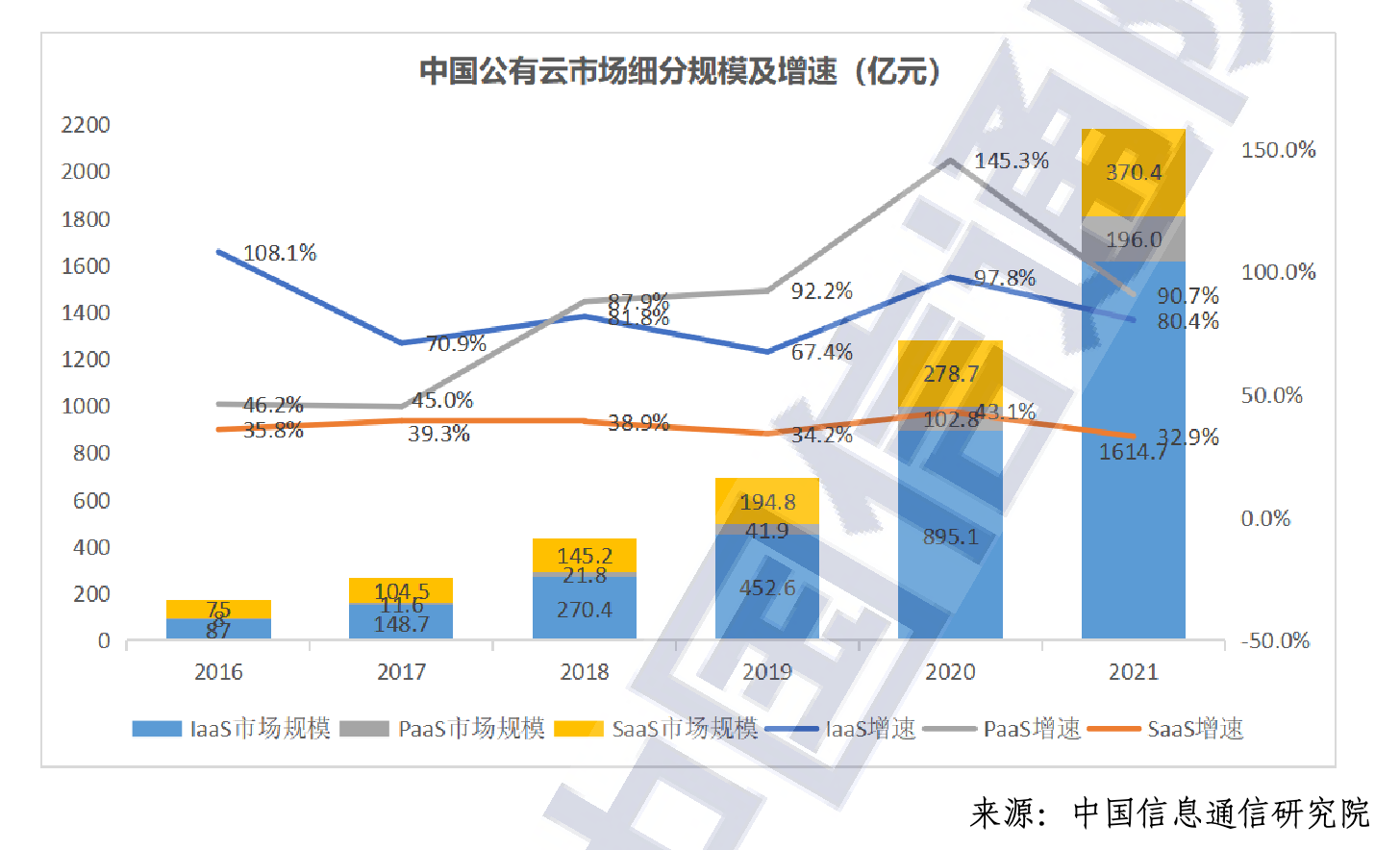

With these fundamentals in mind, I want to revisit this chart in the CAICT whitepaper that breaks down the relative size and growth rate of IaaS, PaaS, and SaaS.

According to this chart, IaaS (in blue) makes up almost 75% of China’s entire public cloud and is growing rapidly (67.4%, 97.8%, 80.4% respectively in the last three years). SaaS (in yellow) is the second largest though significantly smaller, while PaaS (in gray) is the smallest of the three layers.

On the surface, this picture suggests that most of China’s public cloud growth comes from the adoption of low-margin IaaS with a long (long) road ahead to evolve into the higher-margin SaaS and PaaS layers. This stands in stark contrast to the more mature US cloud market, where SaaS makes up the largest share, while PaaS and IaaS equally split the rest.

However, the biggest IaaS providers tend to become winners of tomorrow, even though they have to endure losing money on the low-margin business today. That’s because IaaS holds strategic importance as the first step a given large enterprise needs to take on their cloud transformation journey. IaaS is basically the “gateway drug” of cloud. Once an enterprise chooses a particular cloud platform’s IaaS, it is much easier for the same cloud platform to sell higher-margin PaaS and SaaS solutions later – dramatically increasing this enterprise customer’s lifetime value. By the same token, it is also difficult for an enterprise to migrate from one cloud to another, once it is committed to a cloud’s IaaS layer. Such “lift and shift” efforts happen rarely and are typically a multi-year decision followed by another multi-year migration process.

While I would not go as far as to say you're stuck on a cloud once you choose its IaaS, the reality is pretty close to a “lock in”. That is also why cloud platforms tend to offer steep discounts when selling its IaaS solution – artificially driving down the gross margin of this layer further. It is a worthwhile discount, because the profit generated later with PaaS and SaaS will be hefty.

Thus, the strongest IaaS players tend to have the best chance of long-term profitability, if they have high-quality, follow-on PaaS and SaaS products to offer.

The Fastest “Cloud Horse”

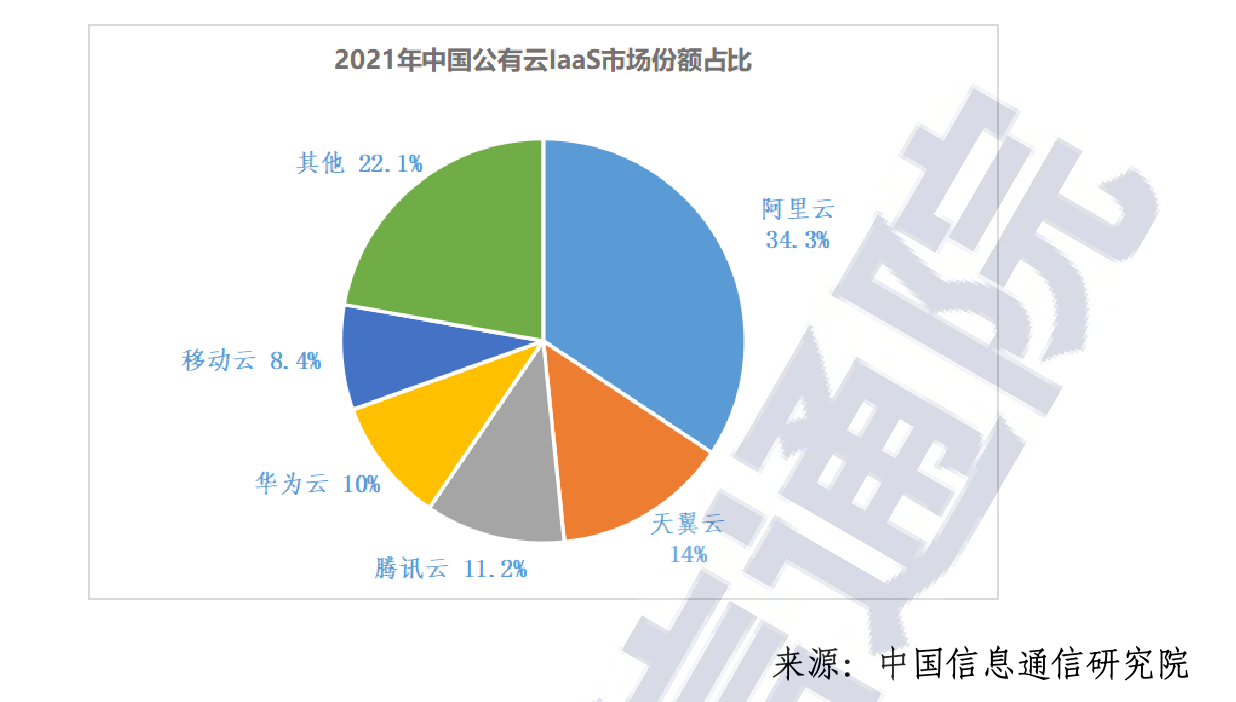

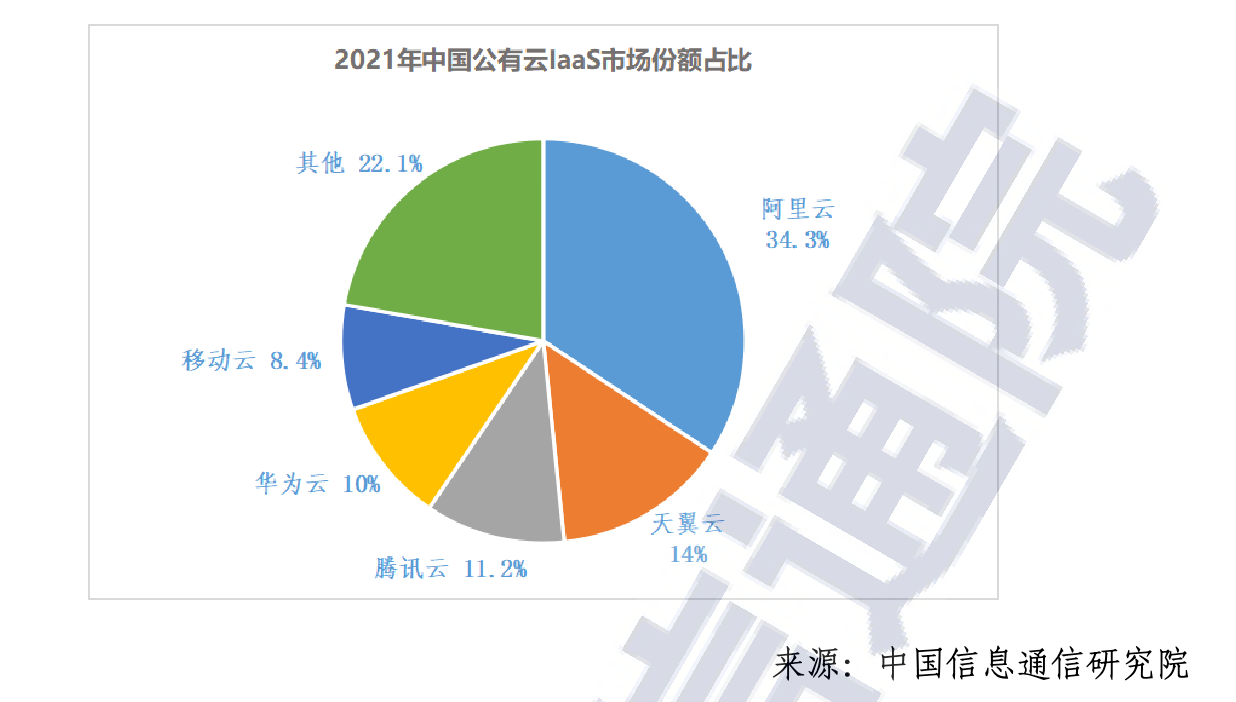

With these cloud fundamentals and business logics in mind, let’s see which Chinese cloud has the largest IaaS market share. Again, according to the CAICT’s research (graph below), the top five public cloud IaaS providers by market share in 2021 are:

- AliCloud: 34.3%

- CTyun: 14% (China Telecom’s cloud)

- Tencent Cloud: 11.2%

- Huawei Cloud: 10%

- Mobile Cloud: 8.4% (China Mobile’s cloud)

Furthermore, the CAICT data shows that the leading public cloud PaaS players are: AliCloud, Huawei Cloud, Tencent Cloud, Baidu Cloud. The whitepaper did not provide a percentage breakdown for the PaaS category, likely because this layer is too small, as previously noted.

AliCloud – as the largest IaaS player by a wide margin, a leading PaaS player, and the maker of an emerging enterprise SaaS product in DingTalk – is likely China’s fastest “cloud horse” to bet on. Even though AliCloud’s current growth rate has been hobbled to 10% year-over-year, due largely to a slowing 2022 Chinese economy that’s teetering on a recession, its long-term growth and profitability potential remains intact, as long as cloud computing’s fundamental economic and business logic continue to hold. Alibaba also has its own cloud semiconductor design division, called PingTouGe, making it less vulnerable to events like the Nvidia ban (more on that below).

Similarly, Tencent Cloud could also be a good bet on China’s future cloud industry evolution, though it has a much smaller IaaS base to grow from compared to AliCloud. Huawei Cloud is also becoming a formidable competitor and expanding well, while other parts of Huawei contracts. Unfortunately, it is a private company and off limits to an average retail investor.

The two state-owned telcos, China Telecom and China Mobile, have become legitimate IaaS providers as well. However, they are both tricky investment targets, having been forced to delist from the US in early 2021 during Trump’s “lame duck” period as president for their connections to the military (for more on that delisting, see previous post “Lame Duck Delisting”). SOEs like telcos also tend to have a harder time attracting top-tier technical talent to build appealing PaaS and SaaS products, so the likelihood of these two telcos moving up the cloud “value chain” is low.

The challenge of investing in China’s cloud growth is there are very few “pure play” options. To invest in AliCloud or Tencent Cloud, you would have to be exposed to the volatilities of the other business units of the parent company. Of course, a similar situation exists in the US market as well; to invest in AWS or GCP, you would have to buy Amazon or Alphabet stocks. However, when it comes to the PaaS or SaaS layer, there are only a handful of public companies that are purely exposed to the Chinese cloud market, e.g. Kingsoft and UCloud. With multiple IPOs last year and a mature cloud market overall, the choices are plentiful on the US side.

There is one upside to investing in China’s cloud, which is its walled garden nature. There are few real foreign competitors on the scene, so the most important factor is how quickly can the leading cloud platforms evolve while competing against each other.

X-Factor: Nvidia Ban

Even though direct foreign competition is not a major factor, US sanctions can still undermine China’s cloud growth. The recent ban of Nvidia’s A100 and forthcoming H100 chips is a prime example. Being able to acquire high-end processors like A100 and H100 is a key component to building more powerful data centers, so they can, in turn, enable more powerful PaaS and SaaS products – the higher margin cloud solutions. This is especially crucial for laying the cloud computing foundation necessary to build cutting-edge technologies like self-driving.

The Nvidia ban certainly opens up more opportunities for domestic chip startups, like Cambricon, Iluvatar CoreX, and Moore Threads, vying to get into the data center business. But becoming a credible alternative, not just the next available less quality alternative, to the best chip company in the world, will take more than just a few billion dollars of VC money. As I shared in a tweet thread when the Nvidia ban news first came out, one of the second order effects of the ban could be that China’s cloud evolution takes a major step back and has difficulties leveling up beyond IaaS.

Ripple effect #2:

— KΞVIN XU (kevinxu.eth) (@kevinsxu) September 2, 2022

China's cloud industry taking a major step back by not having access to high-end Nvidia chips, thus not being able to level up beyond IaaS

(see previous thread on China's cloud growth and characteristics -> https://t.co/VU6x2pdUNJ)

These confluence of factors make investing in China’s cloud a tricky game, though by no means impossible. Globally, cloud digital transformation is a macro trend. As China’s own technical talent pool continues to become more expensive, cloud-based PaaS and SaaS solutions will become attractive over time, and the industry will eventually resemble similar maturity that the US is experiencing now.

Thus, it is a question of “when”, not “if”. Then again, in the world of investing, the question of “when”, not “if”, is alway the harder (and more valuable) one to answer.

如何投资中国的云计算市场?

(本篇中文版文章是读者 Ben Yu 做的编译,我做了一些修改后发表。非常感谢Ben的贡献!)

几周前,我们发布了文章《中国的云计算市场发展到什么阶段了?》。在这篇文章中,我们结合个人判断,梳理了信通院发布的白皮书里的重要内容,介绍了目前中国云计算市场的情况,很多行业分析师和技术专家对此有共鸣。

简单来说,中国的云计算行业还处于非常早期的阶段,正逐步开始扩散和影响到互联网之外的行业。即然这个行业这么早期,那作为一名投资者,我自然而然地开始思考如何在中国的云计算上布局。考虑到最近美国政府禁止英伟达向中国出售芯片的新闻,未来的走势并不明朗,但我还是想和大家分享一些自己目前的想法。

(说明:本文不构成投资建议,在做出任何投资决策之前,请先自己做好充分的调研。)

毛利率:IaaS vs PaaS vs SaaS

在看具体公司是否是好的投资选择前,需要再回顾一下云计算市场的三个不同部分,它们的毛利率、业务逻辑都有巨大的差异。

以下是对这三部分的简单定义:

- IaaS:Infrastructure-as-a-service,指基础设施即服务,把 IT 基础设施作为一种服务通过网络对外提供,并根据用户对资源的实际使用量或占用量进行计费的一种服务模式,提供的内容主要包括 CPU、内存、 存储、网络、虚拟化软件、分布式系统等。

- PaaS:Platform-as-a-service,指平台即服务,提供运算平台与解决方案服务,广泛用于开发框架、商业分析、人工智能等。

- SaaS:Software-as-a-service,指软件即服务,是大部分用户最直接接触到的一类服务,如电子邮件、视频会议、在线文档等等。

就毛利率而言,SaaS 的毛利率最高,超过 80% ,其次是 PaaS,毛利率大约在 50%-70%,IaaS 的毛利率最低,大约在 30%-50%。虽然具体的毛利率会因为规模和企业自动化程度有所浮动,但基本上不会偏离上述的范围。毛利率的差异也反映了这三个部分为用户提供的价值:IaaS 相对价值是最低的,SaaS 是最高的,而 PaaS 位于中间。

考虑到这些,我想就信通院发布的白皮书中的这张图表重新做些讨论,这张图介绍了 IaaS、 PaaS 和 SaaS 的相对市场规模和增速。

根据这张图表,蓝色部分的 IaaS 几乎占中国整个公有云的 75% ,并且还在快速增长(过去三年的增长率分别为 67.4% ,97.8% ,80.4%),其次是黄色部分的 SaaS,但是明显要小得多,而灰色部分的 PaaS 则是占比最小的。

从表面上看,中国公有云的大部分增长来自于低利润率的 IaaS,还需要很长时间来发展利润率更高的 SaaS 和 PaaS,这和更为成熟的美国云计算市场形成了明显的对比。在美国,SaaS 占据了最大份额,而 PaaS 和 IaaS 则平分其余市场。

虽然 IaaS 的毛利率很低,甚至有可能导致亏损,但 IaaS 的战略价值明显更大。IaaS 是大型企业开始数字化的第一步,而一旦企业选择了某个云服务厂商,这个厂商就可以销售更高利润的 PaaS 和 SaaS,这些都可以更大程度上提高企业客户的 CLV(客户生命周期价值)。

虽然不至于说选择了一个云服务厂商,就再也不能换了,但的确会有比较高的替换成本,常常是几年作为一个单位重新考虑是否要更换,所以近乎是锁定了,这也是为什么云服务厂商在销售 IaaS 解决方案时往往愿意提供比较大的折扣,因为随后售出的 PaaS 和 SaaS 解决方案产生的利润可以弥补在 IaaS 上的让利。

因此,一家云厂商如果配有高质量的 PaaS 和 SaaS 解决方案,那往往有长期向好的收入表现。

最快的“云马”

让我们再来看看信通院的数据,2021 年按市场份额排名前五的公有云 IaaS 服务厂商是:

- 阿里云:34.3%

- 天翼云:14%(中国电信)

- 腾讯云:11.2%

- 华为云:10%

- 移动云:8.4%(中国移动)

此外,信通院的数据显示,领先的 PaaS 服务厂商是:阿里云、华为云、腾讯云、百度云。白皮书里没有提供 PaaS 类别的百分比细分,可能是因为这一层目前还太小了。

阿里云: 作为最头部的的 Iaas 和 PaaS 厂商,同时也在积极推出很多 SaaS产品,阿里云算是中国云计算市场的头部玩家。在 2022 年中国经济增长放缓的大环境下,阿里云目前的年增长率已经跌至 10% ,但只要云计算的基本经济和商业逻辑继续保持不变,其长期增长和盈利潜力仍然向好。阿里巴巴还拥有自己的云半导体设计部门平头哥,这使其不那么容易受到英伟达禁令等事件的影响(详情见下文)。

类似的,尽管和阿里云相比,腾讯云的 IaaS 市场份额要小很多,但腾讯云的长期发展也比较向好。华为云的表现也值得关注,尽管华为其他业务在收缩,但华为云在增长。然而华为是一家私人公司,对普通散户来说没办法投资。

那中国电信和中国移动这两家国有电信运营商呢?在特朗普任职总统的最后两个月中,这几家国有电信公司都被迫退市(关于退市,可以阅读此前的这篇文章《Lame Duck Delisting》),这让它们都不是最好的投资选择,尤其如果你是位海外投资人。而且,国企通常很难吸引到人才来开发 PaaS 和 SaaS,因此这两家电信公司很难通过提供成熟解决方案来获取更高的利润。

这对于投资者来说是一个棘手的难题,想要投资中国云计算市场的话,可以选择的“纯碎云”(cloud pure play)投资目标非常少。虽然可以投阿里云和腾讯云,但必须承担其母公司其它业务部门的波动性。

当然,美国市场也存在类似情况,要投资 AWS 或 GCP,就必须买亚马逊或 Google 的股票。然而当投资选择涉及到具体的 PaaS 或 SaaS 时,中国上市的云服务产品就更少了,仅有比如像金山和UCloud这几家。美国在这方面则是一个非常成熟的市场,有很多投资选择。

另一个值得注意的是,中国云市场的一个特点是很少有真正的外企竞争对手,所以更多时候是看国内云服务厂商彼此间的竞争。

新难题:英伟达禁令

虽然外来竞争较少,但美国的制裁依然可以破坏中国的云服务增长,最近英伟达的 A100 和即将推出的 H100 芯片的禁令就是一个最好的例子。A100 和 H100 这样的高端处理器是建立更强大的数据中心的关键组成部分,也就是说没有它们,就很难构建更强大、利润更高的 PaaS 和SaaS,这对于整个市场生态来说都非常重要。

英伟达的禁令利好寒武纪、天数智芯和摩尔线程等中国本土的芯片初创企业,但要成为一个一流的芯片公司,而不仅仅是提供一个勉强可用的替代品,需要的不仅仅是几十亿美元的风投资金。我在 Twitter 第一时间分享了关于英伟达禁令的看法,这个禁令的第二层影响可能是中国的云计算发展倒退一大步,并且在 IaaS 之外的地方很难有新的发展。

Ripple effect #2:

— KΞVIN XU (kevinxu.eth) (@kevinsxu) September 2, 2022

China's cloud industry taking a major step back by not having access to high-end Nvidia chips, thus not being able to level up beyond IaaS

(see previous thread on China's cloud growth and characteristics -> https://t.co/VU6x2pdUNJ)

在这些因素的共同作用下,投资中国云计算市场是个难题。放眼全球,上云和数字化也是一时半会儿不会改变的大趋势。随着中国技术人才的薪资越来越高,PaaS 和 SaaS 的解决方案会变得更有吸引力,如果参考美国的市场情况,可以展望中国云计算市场还有巨大的增长空间。

因此,对于想要投资中国云市场的投资人来说,“什么时候买入” 显然比 “要不要买入” 更重要。