If you work in tech long enough, you will experience many company reorgs. They are almost as routine as sales kickoffs or quarterly earnings calls. But every once in a while, a consequential company does a reorg so major and out of the box that it could shake up how an entire industry does things.

Google becoming Alphabet in 2015 was one example. Alibaba’s most recent reorg, announced earlier this week, is, in my view, another.

Dubbed “1+6+n”, Alibaba plans to evolve into a single holding company (the “1”) with six distinct businesses – each with its own CEO, board of directors, P&L, and the autonomy to set business strategy (the “6”). Additionally, there are also a handful of smaller units under the holding company that are less mature, more speculative bets (the “n”).

The six units are:

- China Commerce (Taobao, Tmall, Taobao Deals, Taocaicai, Freshippo, Tmall Supermarket, Sun Art, Tmall Global. Alibaba Health, and 1688.com)

- International Commerce (Lazada, AliExpress, Trendyol, and Daraz)

- Local Consumer Services (Ele.me, Amap, and Fliggy)

- Cainiao (domestic and international logistics)

- Cloud (Alibaba Cloud, DingTalk, and other cloud-based B2B SaaS products)

- Digital Media and Entertainment (Youku and Alibaba’s own movie studio)

Of the six, the China Commerce unit will continue to be wholly-owned by the holding company. The other five units all have the option to raise outside capital and IPO on their own one day, though Alibaba will remain the biggest shareholder for the foreseeable future. What’s in the “n” is less clear. One often-mentioned unit is T-Head Semiconductors, a home-grown semiconductor design unit, which has been rumored to want to raise outside capital. In the analyst conference call that followed the announcement, Alibaba CEO Daniel Zhang did not reveal when this new structure will become effective.

For folks who follow Alibaba closely, or just track its quarterly earnings casually, this major reorg is not entirely a surprise. Alibaba has been breaking down its earnings roughly into these six units as early as May 2019, when it released its fiscal year 2019 earnings. As time went on, what goes into each of the six shifted a bit, while the P&L of each unit became more transparent.

If you look at Alibaba’s most recent end of calendar year 2022 earnings report, it is quite easy to have a view of the revenue and profitability (on adjusted EBITA basis) of each of the six units. China Commerce is the most profitable ($8.5 billion USD), since it is by far the most mature. Cloud was narrowly profitable ($52 million USD) and has been that way for at least four quarters now. Both Cainiao and the Digital Media and Entertainment unit swing back and forth between narrow losses and tiny profits. International Commerce and Local Consumer Services are the two “money burning machines” with $111 million and $455 million in losses, respectively.

With this picture in mind, it is not terribly difficult to see the trajectory of each of these units. Cloud is probably IPO ready and could get listed within the next 1-3 years, depending on market appetite. Cainiao and Digital Media and Entertainment could use some operational tweaks, but their fundamental economics look sound and probably don’t need outside capital before entertaining their own IPO’s. International Commerce and Local Consumer Services are the two “problem children” that would likely need the most outside capital injection and time to improve their unit economics.

This level of transparency is something that Alibaba does not get enough credit for. Alphabet, the closest Big Tech holding company corollary, does not come close to the same level of transparency – how much money YouTube is making (or losing) is still a mystery.

So what should we make of this major, if not unprecedented, corporate structural change that Alibaba will now embark on? As always, there’s the charitable interpretation and the cynical interpretation.

Charitable Interpretation: A Berkshire-like Model

If executed well, Alibaba could look like Berkshire Hathaway.

The Berkshire model, in a nutshell, is a super lightweight holding entity that owns many many businesses – some wholly, some partially, some of which are synergistic, some of which are totally uncorrelated, and all of which operate independently and generate lots of cash. Warren Buffett and Charlie Munger’s job, in essence, is to acquire businesses and make capital allocation decisions of all the generated cash. It is so lightweight that Buffett has been famously running this business empire with no more than 50 people in Omaha, Nebraska, for the last 58 years (and counting).

No analogy matches 100%, including this one. But there are some elements of Berkshire in what Alibaba is at least proposing to do.

For one, Zhang was emphatic in his announcement about reforming the back office operations of Alibaba to become “lighter and thinner”, as it transitions into a holding company – only keeping what is needed to be a compliant publicly-traded company. He also emphasized that each of the six units will have a high degree of autonomy and authority, which is not limited to raising capital and doing independent IPO’s, but also setting its own compensation and incentive plans and choosing its own tools and services. (Presumably, Youku or Lazada could choose to not use AliCloud as its cloud infrastructure, and use Tencent or AWS instead.) To the extent that Alibaba Holding’s back office resources or know-how’s can be jointly leveraged, they will be provided to the six units at a market rate, just like any third-party service provider.

Furthermore, some of these business units are not that correlated on a fundamental level. Sure, there is an obviously tight connection between China and International Commerce, as well as with Local Consumer Services. But the Cainiao and Youku businesses are very different and unconnected. Cloud also operates on a fundamentally different set of economics than all the other businesses, even though it serves all the other units as internal customers. This moderate degree of “uncorrelated-ness” could make the new Alibaba Holding much more resilient. It also gives the holding company some interesting capital allocation options in the future, both among the six units and beyond into more cutting edge and less mature realms.

Sadly, the similarity with Berkshire stops there. One big gaping problem is that, unlike Berkshire’s businesses, none of Alibaba’s business units produce any real profits right now. Adjusted EBITA, as any Munger acolyte would know, are just “bullshit earnings.” Then again, over the last two years, Munger was also intrigued by Alibaba and even used leverage to buy shares, only to retreat and admit it was one of his “worst mistakes.”

Whether, and to what extent, Alibaba Holding will evolve into a “Berkshire of China Tech”, the larger cultural change this massive reorg is trying to achieve is injecting more startup juice back into a bureaucratic behemoth that’s becoming slow, if not sclerotic.

In a previous post, I wrote rather euphemistically about how Alibaba may be becoming a “mature company.” One indicator of this “maturity”, among other things, is issuing color-coded badges for all employees, where different colors correspond to different levels of seniority. Coincidentally, the colored-badge system was introduced in 2019, during Alibaba’s 20th anniversary celebration – the same year that the company’s earnings report began breaking down numbers by the six units. The thick air of bureaucracy was already suffocating creativity and nimbleness back then, catalyzing the change we now see today.

With fierce competition from all fronts, both domestically and abroad, and the insatiable need for growth as a technology company, the most straightforward way to motivate people to drink the “startup kool-aid” again is a more autonomous structure, combined with compensation incentives to match an “IPO dream”, as if you are working at a Series D, pre-IPO startup.

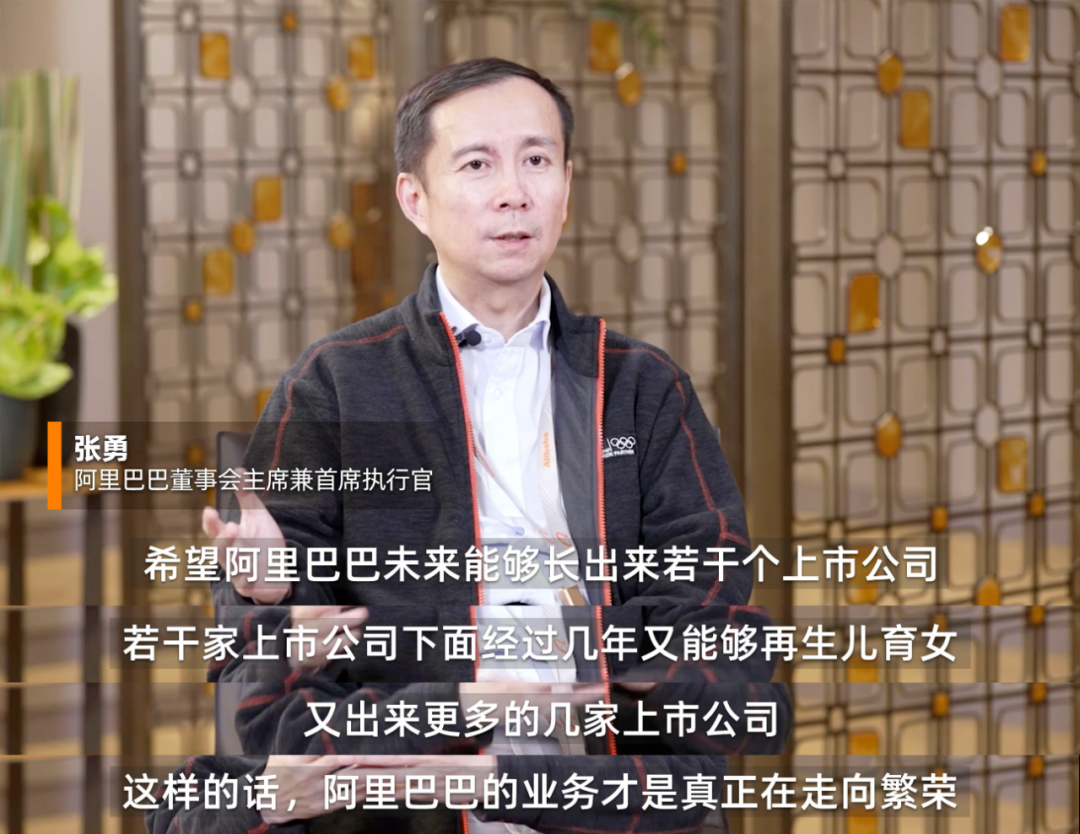

Zhang, in a pre-recorded Q&A video for internal employees regarding the reorg news, made this pitch in the signature Alibaba way – folksy, plain-spoken, yet unabashedly ambitious.

“We hope that in the future, Alibaba will be able to give birth to several publicly-listed companies. And a few years later, these listed companies will be able to give birth to more companies, some of them will become publicly-listed companies too. Only in this way will Alibaba's businesses be truly on a path towards prosperity.” [My unofficial translation with the help of ChatGPT Plus]

By “prosperity”, Zhang is not only talking about Alibaba as a whole, but the path to individual wealth that motivated so many people to join its ranks. Unfortunately, that path was only available to the pre-2014 Alibaba employees, before its New York IPO. The same path that lured so many people to Ant Financials is still closed as of today.

With this reorg, there are theoretically five more paths to IPO’s and making “lying flat” money. That should motivate people, no matter what color your badge is.

Cynical Interpretation: Corporate Engineering and Antitrust Dodging

The cynical interpretation of the Alibaba reorg comes in two flavors: corporate and financial engineering to boost its share price, with the added benefit of dodging future antitrust penalties. Both flavors have some rationale to them.

Corporate and Financial Engineering: It’s a gross understatement to say that Alibaba’s share price has fallen from grace. During the 20th Party Congress last October – a moment of peak pessimism towards China – $BABA shares traded at $58, which is $10 below its IPO price of $68 in 2014! While the price has recovered a bit since then, shares have been wobbling within a range similar to 2015 and well below its all time high of $309.

Although very few company leaders like to admit it, a falling share price has an awful effect on employee morale and normal productivity, let alone creativity and extra drive. If a smart corporate reorg can boost the share price, reverse the market’s narrative, and give employees some hope, then why not? And if this reorg also creates room for some financial engineering, so one decent business could turn into six awesome businesses some day, then double why not?

Alibaba’s price has popped 16% in the two days since the reorg announcement. JPMorgan analysts think the price could more than double. Looks like the “engineering” worked so far; investors are eating it up!

Dodging Antitrust: by breaking a single tech giant into six smaller and loosely-tied businesses under a holding company, Alibaba may have just solved its antitrust problems overnight. By “looking small”, Alibaba makes its rivals look bigger, more powerful, and more competitive along each of the six business units’ respective markets. This could help lessen the attention regulators would pay to Alibaba. And even if one of its six units gets into antitrust trouble in the future, the eventual penalty would be smaller and financially less damaging.

An antitrust penalty is customarily tied to a percentage of the offending company’s previous year total revenue. When Alibaba was punished for its “picking one from two” practice, which forced online merchants to choose only one e-commerce platform to sell products, the final fine was $2.8 billion USD ($18.2 billion RMB). That amount was 4% of Alibaba’s entire China revenue in 2019. Effectively, revenue from AliCloud, DingTalk, and Youku all chipped in to pay for Taobao’s mistake. If an offending company is smaller, the revenue base from which to levy a penalty would also be smaller.

Of course, antitrust regulations are more than just about size. It is also about market share and how a company wields its market power. Even if you are part of a tiny market, but you own 90% of the market share and decide to raise prices and start rent-seeking, you would still be in antitrust trouble.

But “looking small” always helps. And if this “anti-antitrust” tactic works, other China Big Techs may follow. Heck, even some American Big Techs that are under the same scrutiny may take a page or two out of the Alibaba reorg playbook.

Whether you take the charitable view or the cynical view of this Alibaba reorg, it is most definitely not a routine reorg.