The “delisting” narrative of Chinese companies from the US has largely not materialized. Instead, just about every other week there’s news of a new Chinese company about to IPO in New York. The next one, Lufax, may even end up being the largest fintech IPO in US history, with its high-end fundraising target at $2.36 billion.

So far in 2020, US IPOs by Chinese companies (“Chinese” here is defined as the company’s corporate headquarters being located in China as stated in its S1 or F1 filing) have raised $9.1 billion -- the most since 2014. Of course, 2014 was an anomaly with Alibaba’s IPO raising a then-record $21.8 billion.

Under all this geopolitical tension and somewhat concrete legislative action in the Holding Foreign Companies Accountable Act (HFCAA), why are Chinese companies IPOing in the US undeterred?

I believe Wall Street and the IPO business model has something to do with it.

A Chart: 2020 US IPO of China-based Companies

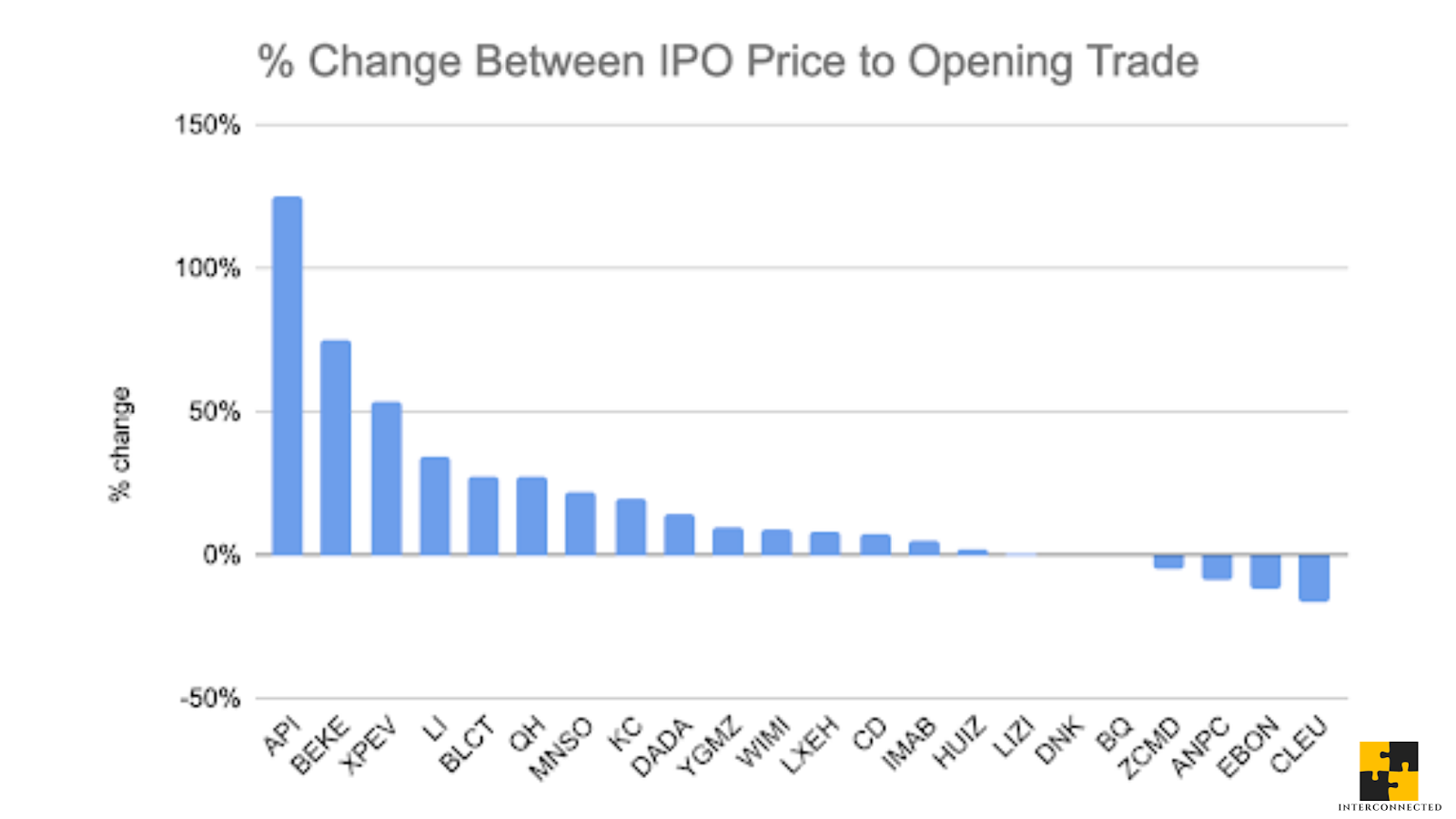

Before diving into the IPO business model (and its recent competitions), I first want to show you this chart I plotted. It shows all the US IPOs by Chinese companies thus far this year (not including Lufax), and the percentage change of each company’s IPO price and its opening day’s first trade price. Many of these are fast-growing, but unprofitable tech companies.

As you can see, some companies had the proverbial “first day pop”, like API (Agora) and BEKE (KE Holdings), while others’ shares started falling immediately after trading began. The median “first day pop” is 9% and the mean is 18%. Most of the companies that enjoyed a decent “pop” also raised much larger rounds than the ones that didn’t -- XPEV raised more than $1 billion and BEKE raised more than $2 billion.

The IPO Business Model

I plotted this chart, because it illustrates a key part of the IPO business model for the Wall Street bankers who facilitate them. Explained simply, an IPO is a size+volume-driven and relationship-driven business.

The size+volume part is straightforward -- bankers typically take a 7% commission based on the size of the IPO or amount raised, so the more money an IPO raises the better. Only in rare cases where the IPO company is super hot, like Facebook, does that commission decrease. And the more IPO deals that happen, aka volume, the more money bankers get to make.

The relationship part gets at the “first day pop”. Because the bankers sort of represent both sides of the table -- helping the soon-to-be public company sell shares at a good price and helping the investors looking to buy shares of new public companies at a good price -- their job is to make both sides “happy”. Bankers can make sure the company is happy by engineering a “first day pop” that produces positive headlines and a big internal morale boost, while still raising the amount of money the company wants. And bankers can make sure their investors (also clients) are happy by manually allocating these IPO shares to them -- shares that are not available to others -- so when the “first day pop” occurs, these investors can sell it for a quick, handsome profit should they choose to. In addition, there’s also the so-called “greenshoe option”, where the underwriting bankers get an additional 15% of IPO shares to sell within 30 days after the IPO day. Being able to deliver this “access” to clients makes the bankers look good and solidifies client relationships with rich investors, who would want to work with the same bankers for the next IPO. It’s a repeat-player business.

I’m glossing over many intricacies of the IPO process, but simply put, bankers want to deliver the biggest IPO possible with a “first day pop” and do as many of these transactions as possible. Doesn’t work every time, but they sure do try.

While it’s generally been a good IPO year, what makes Chinese companies especially attractive customers for New York bankers is that the alternatives to a traditional IPO -- Direct Listing and SPAC -- are not viable options for Chinese companies.

Off Limit: Direct Listing, SPAC

Even from my simple description of the IPO business model above, it’s not hard to see that the process is problematic, specifically in its “dual-agency” set up where the bankers are representing the interests of both sides of the table. Influential venture capitalists, like Bill Gurley, have been criticizing this issue for many years. Thus, both Direct Listing and SPAC (Special Purpose Acquisition Company) are gaining prominence in the last two years as alternatives. SPAC’s popularity in particular has spiked this year.

To contrast these two alternatives with a traditional IPO in the plainest way possible: a Direct Listing lets a company’s shares trade publicly without raising any money (not yet allowed to), thus only providing liquidity and price discovery, while a SPAC raises money first, then uses that money to reverse-merge with a private company, thus taking that company public.

This blog post by the VC firm, a16z , also has a good shorthand of how to compare these three options:

“If you need money, an IPO, for all its flaws, makes the most sense and is probably the best option; if you don’t, a Direct Listing may be preferable; if you need money, speed, and certainty, a SPAC may be best.”

The ongoing discussions about the pros and cons of these two new options vis-a-vis an IPO inside both Wall Street and Silicon Valley are fascinating and fierce. But they are both off limit to Chinese companies seeking to go public in the US, because:

- Direct Listing is for companies who don’t need new capital and, to trade well, should have some public name recognition, e.g. Spotify being the first direct listing back in 2018. Few Chinese companies, especially fast-growing tech companies, are profitable enough to not need new capital or have big name recognition.

- The SPAC hype is mostly an American phenomenon, and there are plenty of private companies in the US to target. It will be a long time, if ever, before American SPACs look for foreign companies to take public.

There are other “going public” options, just not good ones. With its rule change in 2018, the Hong Kong stock exchange now allows unprofitable companies to list, as does the new NASDAQ-like Shanghai STAR market. Both are trying to compete with Wall Street for business. However, the price and valuation for unprofitable companies tend to be lower, while both the higher valuation and reputational capital garnered from “going public in America” cannot be replicated. SPAC-like mergers are also available in Hong Kong, but that’s usually relegated to poor quality companies with no other options, which is the long-time reputation of SPAC in America as well until last year.

Essentially, unprofitable but promising Chinese companies need Wall Street. And Wall Street needs their business too!

Unserious Regulators

With Ant Group’s snub of NYSE/NASDAQ to opt for a simultaneous dual listing in Hong Kong and Shanghai, Wall Street will be fighting extra hard for IPO business from China.

But what about all the pending legislation and harsh rhetorics against Chinese companies? Just like the whole ByteDance ordeal, I suspect they are more for show than serious efforts to regulate a legitimate inconsistency in our capital market.

When the HFCAA first passed the US Senate back in May (and by unanimous consent, meaning every senator agreed with it, so they didn’t bother calling a floor vote to record who said “yes” and who said “no”), there appeared to be a lot of momentum behind the bill to gain approval in the House of Representatives, then to Trump for his signature. I had thought then that, given how unanimously anti-China Washington has been, legislators would fast track the bill and claim a rare victory over China.

That of course didn’t happen. The last public statement made by anyone on this bill was in August by Senator Rubio, who introduced a similar bill called EQUITABLE Act in 2019. (EQUITABLE stands for “Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges”. Yes, the Congressional acronym game remains strong.)

To be clear, I’m generally in support of the core substance of HFCAA. As I wrote in “Why Huawei Should IPO in America” back in May, it makes sense for the SEC’s Public Company Accounting Oversight Board (PCAOB), the auditor of auditors, to enforce the same standards on Chinese companies as it does to all foreign companies listed in the US. Rules are rules, and they should be applied evenly across the board. I also don’t think such a change would force all Chinese companies to delist. There are ethical, ambitious entrepreneurs from China (and everywhere) who would welcome that scrutiny, because their mission is to build a global, world-changing business and would crave the trustworthiness that comes with a higher regulatory standard. And the ones who do have problematic financial practices and shady connections will delist. It’s a self-selecting process.

Wall Street will lobby to deter or water down the HFCAA. Given its mutually-beneficial relationship with Chinese companies, that is to be expected. What is also expected, but hardly happens these days, is legislators and regulators putting their foot down and doing their job. Until that happens, Chinese companies of all shades of ethical standards will continue to list in New York, and bankers will happily continue to make money off of them.

Those “first day pops” will just keep on popping.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

华尔街钝化 "退市 "

中国公司从美国 "退市 "的舆论基本没有实现。相反,差不多每隔一周就会有一家新的中国公司即将在纽约上市。下一家是平安保险旗下的陆金所,它甚至可能成为美国历史上最大的金融科技IPO,其高端募资目标为23.6亿美元。

在2020年到目前为止,中国公司(这里 "中国 "的定义指的是在公司上市的S1或F1文件中公司总部地址位于中国)在美国的IPO已经筹集了91亿美元 -- 这是自2014年以来最多的一年。当然,2014年也很反常,那年阿里巴巴的IPO筹集了当时创纪录的218亿美元。

在这样一个地缘政治紧张的局势下,再加上美国国会正在申论的《外国公司责任法案》(HFCAA) ,为什么中国公司毫不畏惧地继续在美国上市呢?

我觉得这和华尔街的IPO商业模式有关系。

一张图:2020年中国公司赴美IPO的情况

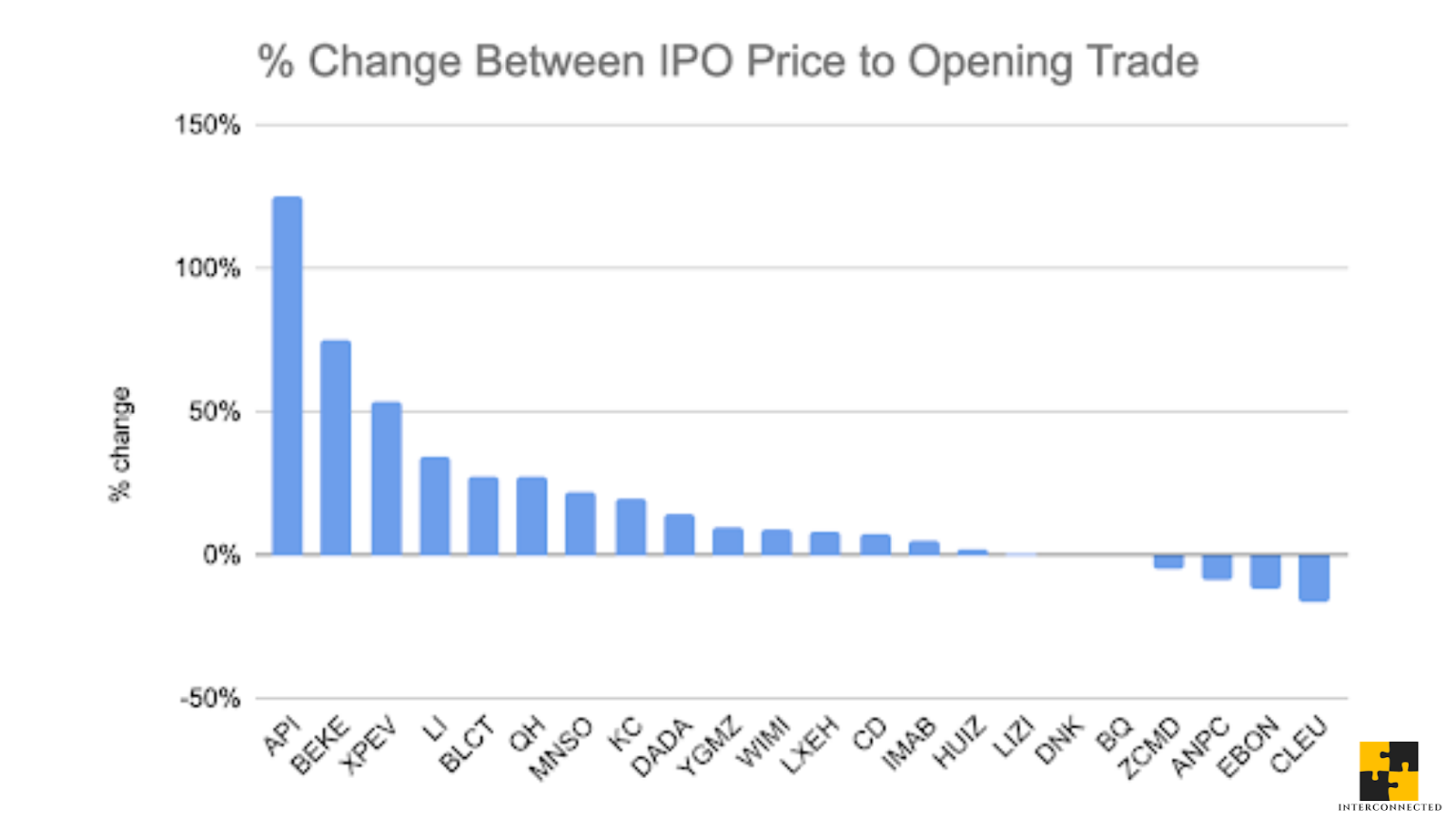

在深入讨论IPO商业模式(及其最近的竞争对手)之前,我首先想给大家分享一张我做的图。它显示了今年以来所有中国公司在美国的IPO(不包括陆金所),以及每家公司的IPO价格和首日交易价格的变化百分比。其中很多都是增长迅速、但仍未盈利的科技公司。

正如您所看到的,有些公司得到了众所周知的 "首日爆涨",比如API(声网)和BEKE(贝壳),而其他公司的股价在交易一开始就立即下跌。"首日爆涨 "的中位数是9%,平均值是18%。大多数“首日暴涨”了的公司筹集到的资金额也比没涨的公司要多 -- 小鹏筹集了超过10亿美元,贝壳筹集了超过20亿美元。

IPO商业模式

我做这张图是因为它能显示华尔街的IPO商业模式的一个关键部分。简单的说,IPO是一门“规模+数量”驱动和关系驱动的业务。

“规模+数量”这一块理解起来很直接:银行通常根据IPO的规模或筹集的金额收取7%的佣金,因此IPO筹集的资金越多越好。只有在上市公司超火爆的极少数情况下,比如Facebook,这个佣金才会减少。而且IPO交易数量越多,银行能赚到的钱就越多。

“关系驱动”这部分就和"首日爆涨"有关了。因为银行家其实代表了整个交易的两方 -- 既要帮助即将上市的公司把股票卖个好价钱,同时也要帮助那些想买新上市公司股票的投资人卖个好价钱 -- 他们目标就是要让双方都 "满意"。银行家们可以“操作”一个 "首日爆涨 "来确保公司方高兴,这个 "首日爆涨"让公司“上头条”,极大地鼓舞内部士气,同时还能筹集到公司想要的资金。同一拨银行家们也可以亲自分配这些IPO股票给他们的投资人,让这些客户满意 -- 这些IPO股票是不公开的,要靠关系。在 "首日爆款 "发生时,这些拿到IPO股票的投资人可以选择立即卖出,“赚一笔”。此外,还有所谓的 "绿鞋期权" (greenshoe option),即帮助IPO的银行在IPO日之后的30天内,可以额外获得15%的IPO股票去出售。能够帮客户买到IPO股票让银行家们很有面子,也巩固了他们与资金雄厚的投资人的客户关系,让他们在下一次IPO时会与同一位银行家合作。这是一个重复玩家的生意。

整个IPO过程很复杂,以上的概括简化了很多细节。但简单地说,银行家们总是期望把每一个IPO都做出 "首日爆涨",而且交易量越多越好。虽然不是每次都能成功,但他们肯定会努力去这么做。

虽然今年的IPO市场情况普遍不错,但中国公司对纽约的银行家来说特别有吸引力,因为传统IPO的“竞争对手” -- 直接挂牌和SPAC -- 对中国公司来说是不可行的。

做不到:直接挂牌, SPAC

即使从我上面对IPO商业模式的简单描述中,也不难看出这个过程是有问题的,特别是银行 "双面代表 "的这层关系。许多大牌的风险投资家,如Bill Gurley,多年来一直在批评这个问题。因此,其他两种上市的方式 -- 直接挂牌和SPAC (Special Purpose Acquisition Company)-- 在近两年越来越火,尤其是SPAC的受欢迎程度在今年急剧上升。

用最通俗的方式解释一下这两种方式与传统的IPO的区别:直接挂牌(Direct Listing)让公司的股票在不募集新资金的情况下公开交易(目前美国法律不允许用“直接挂牌”方式募集资金),只能提供股票的流动性和更准确的股价;而SPAC则是先在一个空壳里募好资金,然后用这笔钱与一家未上市公司反向并购,从而让这家公司上市。

风投基金a16z的这篇博文,也对如何比较这三种方式做了个简单通俗的解释:

"如果你需要钱,IPO,尽管有很多缺陷,但却是最合理的方式也可能是最好的选择;如果你不需要钱,直接挂牌也许是最好的选择;如果你需要钱、很快的交易速度和确定性,SPAC可能是最好的选择。"

在华尔街和硅谷业内,关于这两种新方式与传统IPO的利弊的讨论很有趣,也很激烈,但这两种方式对想在美国上市的中国公司来说基本都不可行:

- 直接挂牌是针对那些不需要新资本的公司的,而且如果要在开始交易时让股票卖个好价钱,应该需要有一定的公众知名度,比如Spotify在2018年作为第一家直接挂牌的公司。中国公司里,尤其是快速增长的科技公司,很少是有足够盈利而不需要新资本的,同时它们在美国也没有多大知名度。

- SPAC最近的火爆总体是个美国资本市场的现象,在美国有很多未上市的企业是SPAC的目标。离美国SPAC需要找外国公司上市的那一天还要很久,甚至永远不会发生。

当然对想"上市 "的中国公司来说还有其他选择,只是没有什么很好的选择。港交所在2018年修改了规则,现在允许不盈利的公司上市,上海科创板也是如此,两方都在试图与华尔街抢IPO的生意。不过,未盈利公司的整体价格和估值往往偏低,而 "赴美上市 "能让它们获得更高的估值以及“声誉资本”,这一点目前是无法被复制的。 类似SPAC的反向并购在香港也有,但那通常是给质量差、没有其他选择的公司,这也是SPAC在美国直到去年的长期声誉。

因此,不盈利但有前途的中国公司需要华尔街,而华尔街也需要它们的生意!

不认真的监管者

随着蚂蚁集团跳过NYSE/NASDAQ,选择在香港和上海同步双重上市,华尔街将会格外努力去争取来自中国的IPO生意。

但那些针对中国公司的立法提议和严厉批评呢?就像对字节跳动的“折腾”一样,我怀疑这些监管作为更多是为了作秀,而不是认真去规范美国资本市场内一些的确需要更改的问题。

当HFCAA5月份首次在美国参议院通过时(而且是以“一致同意”的方式通过的,也就是说每个参议员都同意了,所以他们懒得去做现场投票来记录谁说 "同意 "谁说 "不同意"),该法案似乎有很强的动力在众议院也立即获得批准,然后被交给特朗普签署。我当时还以为,鉴于华盛顿一直一致的反华态度,议员们会快速通过该法案,并宣称针对中国取得了罕见的胜利。

实际上这并没有发生。最近一次对此法案发表的公开声明是参议员Marco Rubio在八月份的一份官宣。他在2019年提出了一个类似的法案,名为EQUITABLE Act。(EQUITABLE是"Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges "的缩写。是的,国会的“缩写能力”仍然很强)

需要说明的是,我个人总体上是支持HFCAA的核心内容的。正如我5月份在《为什么华为该赴美上市》一文中写到的,美国证券交易委员会(SEC)的上市公司会计监督委员会(PCAOB),作为审计师的审计师,对中国公司执行与对所有在美国上市的外国公司一样的标准是有道理的。规矩就是规矩,应该一视同仁。我也不认为这种改变会迫使所有中国公司退市。中国(以及世界各地)有许多有道德、有抱负的企业家会欢迎这种审查,因为他们的使命是建立一个全球化的、能改变世界的公司,他们会渴望更高的监管标准能为市场带来的诚信。而那些确实有问题的、不道德的、有见不得人的黑幕关系的公司自己就会退市。这是一个自我选择的过程。

华尔街是会游说阻止或淡化HFCAA的。鉴于其与中国公司的互利关系,这是可预料到的。同样也应该在意料之中但很少发生的是,立法者和监管者抵制腐败和诱惑,做好自己的本职工作。在监管者开始认真做事之前,道德标准不一的中国公司将继续在纽约上市,而银行家们也会很乐意地继续赚它们的钱。

那些 "首日爆涨"只会一直“爆”下去。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,和我交流互动!