The US-China tech “cold war” appears to have a new front: the cloud.

According to the New York Times, both the Departments of State and Commerce are looking into new ways to restrict Chinese cloud hyperscalers, e.g. AliCloud, Huawei Cloud, Tencent Cloud, etc. The justifications are the usual, if not oftentimes vague, dual threats of national security and stealing sensitive American data. If any new rules or restrictions were to be announced, they would seek to limit the growth and traction of these “Chinese clouds” both domestically in the US and around the world.

The domestic restrictions are predictable enough – just another straw of a multi-year regulatory squeeze to totally eliminate Chinese tech presence in America. Although AliCloud and Tencent Cloud still operate data centers on both the west and east coasts of the US, their traction and ambition have been dramatically downsized. Instead of competing with AWS or GCP head-to-head for large customers, they are limited to servicing non-sensitive SMEs and providing additional cloud capacity for Chinese customers seeking some expansion growth in the US. (And when this expansion growth reaches a certain scale, like TikTok with AliCloud, it is forced to switch to an American cloud vendor, like what ByteDance is doing with Oracle Cloud.)

However, who will win this new front outside of the US is far from certain and with a lot at stake. Based on some estimates, the current size of the global cloud computing market is $569 billion USD and is projected to grow to $2.4 trillion USD by 2030. That is a ton of CPU/GPU compute, data storage, and network bandwidth consumption up for grabs.

Thus, this global “cloud proxy war” between American clouds and Chinese clouds can evolve in interesting ways, especially in fast-growing, diplomatic bellwether regions where the geopolitical allegiances are anything but clear. I’ll highlight three of these regions today: Southeast Asia, Latin America, and the Middle East.

Three New “Battlefronts”

On some level, the competition in these three regions has been underway for a few years now. In some regions, the American clouds are ahead in their investments, while the Chinese clouds have more traction in other places. The battle is already fierce, and any new policy from the US government would elevate the competition to a new level.

When I wrote “Where Can the Chinese Internet Go?” two years ago, I briefly profiled these three regions’ growth prospects for Alibaba and Tencent in particular. Even though the entire Internet sector in China is going through a massive slow down, the cloud data center expansions have continued apace. So one way to size up the two sides of this “cloud proxy war” is to look at the existing data center investment footprint, among the top three Chinese clouds (AliCloud, Tencent Cloud, Huawei Cloud) and the top three American clouds (AWS, Azure, GCP) in Southeast Asia, Latin America, and the Middle East.

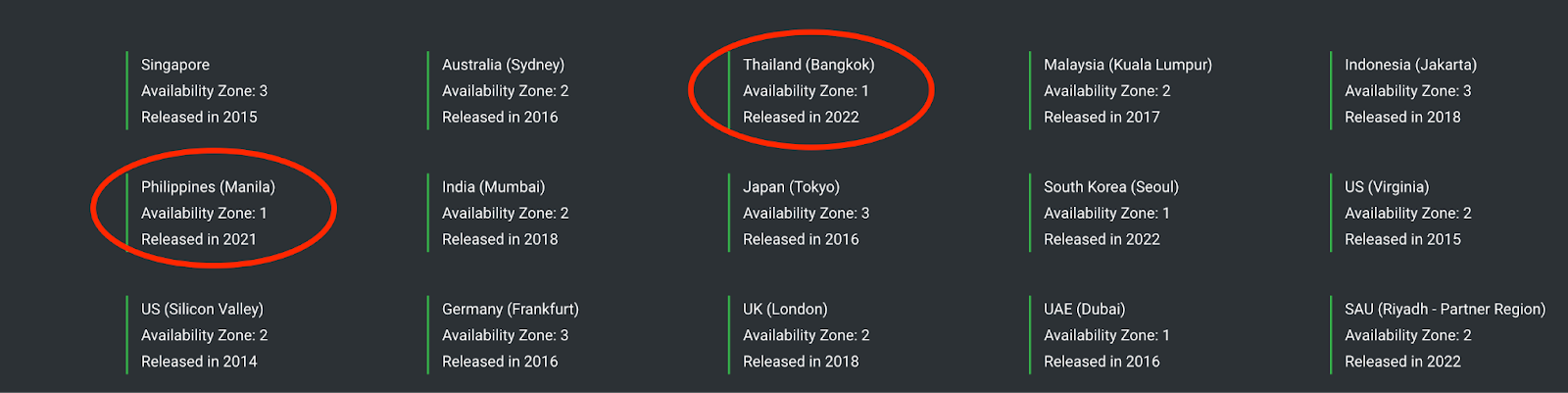

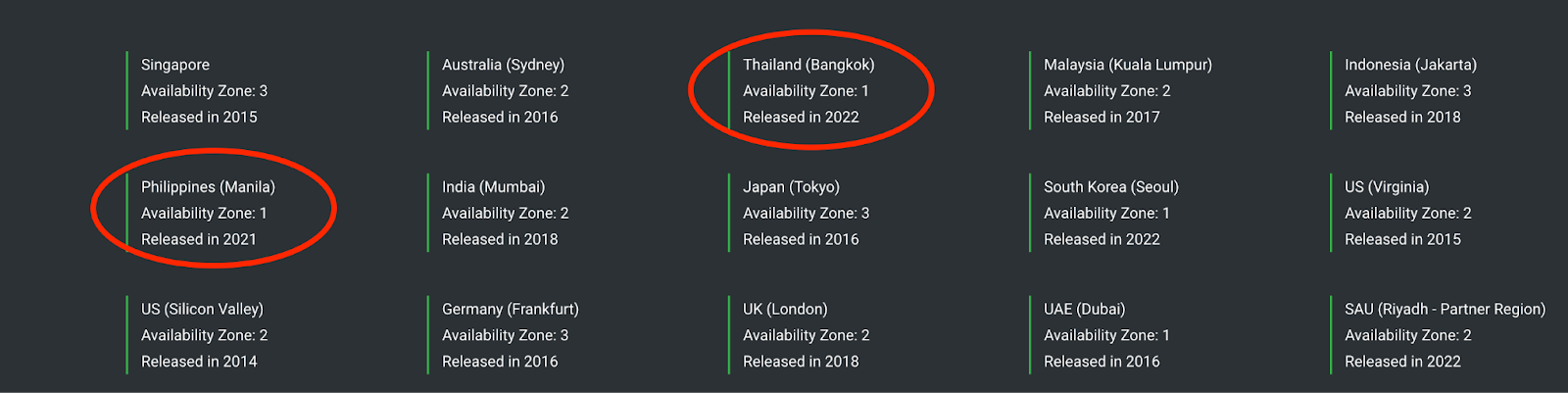

Southeast Asia:

In the last three years, the Chinese clouds have all deepened their cloud data center footprint in Southeast Asia, particularly in Thailand, in addition to longstanding build outs in Singapore and Indonesia. (AliCloud has also added a data center in the Philippines.)

This progress outpaces their American counterparts. AWS has data centers in Singapore and Indonesia, but its Thailand and Malaysia locations are still being developed. Azure has a data center presence in Singapore, but its Indonesia and Malaysia locations are still labeled “coming soon”. GCP (Google Cloud Platform) has a solid data center presence in Singapore and Indonesia, but no publicly-known plans to expand further in this region.

It’s important to note that solely comparing the number of locations does not paint an accurate picture. Each location’s number of “availability zones” (or AZs) is also a useful factor to measure depth of investment. Without getting into too many cloud computing jargons, essentially the more availability zones a single location has, the more maturity, redundancy, and performance that location has. Here’s summary of each cloud’s Southeast Asian locations and their respective AZs count:

- AWS: Singapore - 4; Indonesia - 3; Total - 7

- Azure: Singapore - 3; Total - 3

- GCP: Singapore - 3; Indonesia - 3; Total - 6

- AliCloud: Singapore - 3; Indonesia - 3; Malaysia - 2; Philippines - 1; Thailand - 1; Total - 10

- Tencent Cloud: Singapore - 4; Indonesia - 2; Thailand - 2; Total - 8

- Huawei Cloud: Singapore - 4; Indonesia - 3; Thailand - 3; Total: 10

On an AZs-by-AZs basis, AliCloud and Huawei Cloud are in the lead in Southeast Asia each with 10, with AliCloud having more geographically diversity. AWS has the most from the American side with seven.

Latin America:

Latin America is a region where Chinese technology companies have been making inroads for many years, from e-commerce to ridesharing to electric vehicles. More recently, Chinese manufacturers of all kinds are setting up shop in different Latin American countries (Mexico, in particular) to produce products that can be more easily sold into the US that are mostly Chinese made, but with a light coating of “friendshoring” and “nearshoring” added.

On the cloud front, let’s do the same availability zones-based exercise on Latin America between the American clouds and their Chinese counterparts to see which has made the most in-region investments and inroads so far:

- AWS: Brazil - 3; Total - 3

- Azure: Brazil - 3; Total - 3

- GCP: Brazil - 3; Chile - 3; Total - 6

- AliCloud: None

- Tencent Cloud: Brazil - 1; Total - 1

- Huawei Cloud: Brazil - 2; Chile - 2; Peru - 2; Mexico - 2; Argentina - 1; Total: 9

Huawei is the leader here, with both the most AZ’s and geographical diversity, dramatically outpacing its Chinese and American competitors. GCP has the most among the American clouds with six.

In general, the cloud computing footprints are less built out in Latin America compared to Southeast Asia. This matches up with the two regions' overall difference in digitization and technology adoption. Latin America is about five to seven years behind Southeast Asia. This gap explains why Southeast Asian tech, like Shopee, is doing very well in Brazil, while Latin American-native tech companies look to Southeast Asia (and China to some extent) for lessons and inspirations. The two regions are much closer in their development cycle than compared to the U.S., so cross-regional lessons are more relevant and useful.

The Middle East:

Now, let’s do the same AZ-to-AZ comparison for the Middle Eastern region:

- AWS: Bahrain - 4; UAE - 3; Total - 7

- Azure: UAE - 3; Qatar - 3; Total - 6

- GCP: Qatar - 3; Israel - 3; Total - 6

- AliCloud: Saudi Arabia - 2; UAE - 1; Total - 3

- Tencent Cloud: None

- Huawei Cloud: Turkey - 3; Total - 3

Here the American clouds are clearly ahead, with more locations and more availability zones. The only noteworthy point from the Chinese clouds is Huawei being the only vendor with a data center presence in Turkey (Istanbul).

Zooming out, the Middle East has the least number of AZ’s compared to Southeast Asia and Latin America. This is likely due to both the relatively lack of digitization and tech penetration in the region and its physical proximity to Europe and India, both of which have more established data centers that can service the Middle Eastern region. With oil-infused sovereign wealth funds more aggressively investing in tech, the region may see more growth that would warrant additional data center investments soon. Mubadala, the Abu Dhabi sovereign wealth fund, is publicly going “on offense” as sources of capital become tight in western markets. Saudi Arabia’s Public Investment Fund, in a rare move of transparency in the capital allocator community, publicly disclosed its investments in many top technology funds, like a16z and Coatue.

The Middle East is a region that will become a prime battleground between the US and China, both technologically and diplomatically. The US is no doubt the incumbent and a long time diplomatic “resident” of the region with many ill-fated wars and ineffectual peace talks. Meanwhile, China, the diplomatic newcomer, notched an early win by brokering the restoration of relationships between Saudi Arabia and Iran.

Where Diplomacy and Cloud Collide

This impending global “cloud proxy war” (should it occur) feels reminiscent of the global 5G war, where the US government applied its diplomatic muscle forcefully to pressure countries not to use telecom equipment from Huawei and ZTE to build their domestic 5G networks. This pressure has worked to some degree in countries like Germany, France, the Netherlands, Japan, and India – all formal allies of the US, but has been less effective in other parts of the world. This is in large part due to no American tech alternatives – it’s hard to credibly pressure a country to not use something, when your own country’s technology is also behind.

US diplomats won’t have the same problem with cloud computing. By almost every measure and dimension, the top three American clouds are more advanced than the top three Chinese clouds. The only imaginable advantage the Chinese clouds may have is to play an extreme price war, buoyed by government subsidies, on mostly undifferentiated and commoditized cloud services, like object storage or containerized servers. It is a “war” the American side should win.

The three regions we highlighted – Southeast Asia, Latin America, the Middle East – are all “swing” regions, where their diplomatic alliances are less one-sided towards either the US or China. This bellwether status will likely continue in a strategic way, as these regions don’t want to fall under either camp and would prefer to be courted to maximize their own influence, independence, and get the best deals. These deals may very well come in the form of more data center investments to boost the pace of digitization or heavily-discounted cloud contracts with large local enterprises or governments – all of which make these three regions worth watching closely, as diplomacy and cloud collide.

As much as this “cloud proxy war” may be a contest that heavily favors the American clouds, the US government’s hostile attitude towards Big Tech adds an awkward wrinkle. While the State Department looks to enlist AWS, Azure, and GCP to push back against the Chinese clouds globally, the FTC is suing Amazon for dark patterns in Prime, attempting to block Microsoft’s acquisition of Activision Blizzard, while the Justice Department is suing Google for monopoly in digital advertising.

It’s hard to willingly do your government’s bidding abroad, when that same government is trying to break you up at home. And even if AWS, Azure, and GCP decide to “put country first” and set aside those petty, anticompetitive grievances, do you really want foreign service officers to do your presales?

中国vs美国的云计算“大战”

中美科技“冷战”似乎又出现了一条新的战线:云计算。

据《纽约时报》报道,美国国务院和商务部都在探索新的方案来限制中国的云计算平台的扩展,例如阿里云、华为云、腾讯云等。理由如常,即国家安全和窃取敏感美国数据的双重威胁,即使具体威胁的细节还是很模糊。如果要宣布任何新的规则或限制,它们将寻求限制这些“中国云”在美国境内以及全球范围的扩大和影响力。

在美国国内加力限制并不奇怪 – 仅是多年监管紧缩的又一个举动,完全消除中国科技在美国的任何生存空间。尽管阿里云和腾讯云仍在美国的东西海岸都有数据中心,但他们的影响力和野心已大幅缩减。两家公司已不再与AWS或GCP正面竞争大客户,而是限制在为非敏感中小企业提供服务,以及为寻求在美国市场扩张的中国客户提供外加的云计算容量。(当这种出海扩张大到一定规模时,比如TikTok用阿里云,就会被迫切换到像字节与甲骨文云合作的那样,必须用美国本地的云计算供应商。)

然而,美国境外,这个新战线上谁会胜出一筹还远非是定局,而且利害攸关。根据业界估计,当前全球云计算市场的规模为5690亿美元,预计到2030年将增长到2.4万亿美元。这意味着大量的CPU/GPU计算、数据存储和网络带宽消耗来去何方,还等待分配。

因此,“美国云”和“中国云”之间的全球 “大战” 还有很多演变的可能性,特别是在经济快速增长,而且盟友关系还不明确的地域。今天,我将重点看看这种地区的其中三个:东南亚、拉丁美洲和中东。

三条新“战线”

在某种程度上,在这三个地区中的中美竞争已经持续好几年了。在有些地区,美国云的投资领先,而在其他地方,中国云却更有影响力。竞争已经非常激烈,美国政府的任何新政策都将使竞争提升到更高的热度。

两年前,当我写《中国互联网还能去哪里?》一文时,我简要描述了阿里和腾讯在这三个地区的增长前景。尽管中国整体互联网行业正在经历大幅放缓,但在云数据中心的投资上却一直在稳步进行。因此,分析这场中美云计算大战的一种方式是查看在东南亚、拉美和中东的前三家中国云(阿里云、腾讯云、华为云)和前三家美国云(AWS,Azure,GCP)之间各自现有的数据中心投资足迹。

东南亚

在过去的三年中,中国云大厂都在东南亚深入投资,扩大了自身云数据中心的足迹,特别是在泰国,除了在新加坡和印度尼西亚的长期投资外。(阿里云还在菲律宾增加了一个数据中心。)

这一进展超过了他们的美国同行。AWS在新加坡和印尼有数据中心,但其泰国和马来西亚的投资还没有上线。Azure在新加坡有数据中心,但其印尼和马来西亚的投资仍被标记为“即将推出”。GCP(谷歌云平台)在新加坡和印尼都有坚实的数据中心基础,但在东南亚其他国家还没有公布进一步扩展的计划。

值得注意的是,从技术角度看,仅比较数据中心地点的数量并不够。每个地点的“可用区域”(availability zones 或 AZs)数量也是衡量投资深度的重要因素。避开云计算的行话,简单来说在一个数据中心地点的可用区域越多,该位置的成熟度、冗余和性能就越高。以下是每家云在东南亚的所有地点及其各自AZs的总计:

- AWS:新加坡 - 4; 印尼 - 3; 总计 - 7

- Azure:新加坡 - 3; 总计 - 3

- GCP:新加坡 - 3; 印尼 - 3; 总计 - 6

- 阿里云:新加坡 - 3; 印尼 - 3; 马来西亚 - 2; 菲律宾 - 1; 泰国 - 1; 总计 - 10

- 腾讯云:新加坡 - 4; 印尼 - 2; 泰国 - 2; 总计 - 8

- 华为云:新加坡 - 4; 印尼- 3; 泰国 - 3; 总计: 10

从AZs对AZs的角度来比,阿里云和华为云在东南亚处在领先地位,每家有10个,其中阿里云的地域覆盖更广。美国云中,AWS以七个AZs居首。

拉美

拉丁美洲是中国科技公司多年来一直在努力突破的市场,从电商到共享出行,再到电动汽车。最近,各种类型的中国制造商也在不同的拉美国家(尤其是墨西哥)设立工厂,以便在中美关系冷话,制造业偏向“本土化”的大方向持续的环境下,还能继续销进美国市场。

在云计算投资方面,我们看看在拉美地区,美国云和中国云迄今为止哪家的投资最多,市场突破最深:

- AWS:巴西 - 3; 总计 - 3

- Azure:巴西 - 3; 总计 - 3

- GCP:巴西 - 3; 智利 - 3; 总计 - 6

- 阿里云:无

- 腾讯云:巴西 - 1; 总计 - 1

- 华为云:巴西 - 2; 智利 - 2; 秘鲁 - 2; 墨西哥 - 2; 阿根廷 - 1; 总计: 9

华为云在拉美摇摇领先,有最多的AZs和最广的地域覆盖,远远超过其它来自中国和美国的竞争对手。在美国云队伍中,GCP的AZs数量最多,总共六个。

总的来说,与东南亚相比,拉美的云计算投资深度较浅。这与两个地区在数字化和技术采用方面的整体差异相吻合。拉美大约比东南亚落后五到七年。这个差距可用来分析为什么东南亚领先的科技平台,比如Shopee,在巴西做得非常好,而拉美本土的科技公司则常常对表东南亚以及中国的公司,从中寻找经验和灵感。与美国相比,中国和东南亚的发展周期与拉美更接近,因此跨地域的实战经验更有用些。

中东

那让我们再看看在中东地区,中美云厂商各自AZ对AZ的比较:

- AWS:巴林 - 4; 阿联酋 - 3; 总计 - 7

- Azure:阿联酋 - 3; 卡塔尔 - 3; 总计 - 6

- GCP:卡塔尔 - 3; 以色列 - 3; 总计 - 6

- 阿里云:沙特阿拉伯 - 2; 阿联酋 - 1; 总计 - 3

- 腾讯云:无

- 华为云:土耳其 - 3; 总计 - 3

放宽视角来看,与东南亚和拉美相比,中东地区的AZs数量最少。这可能是由于该地区相对较低的数字化和科技渗透度,以及其与欧洲和印度较近的地理位置,这两个地区都有更成熟的数据中心基础已经可以服务中东地区的需求。随着石油注入的主权财富基金更积极地向科技领域投资,该地区可能会看到更多的增长,这将更快的促使数据中心投资。阿布扎比主权财富基金穆巴达拉正在公开采取“进攻”策略,因为西方市场的资本来源趋紧。沙特阿拉伯的公共投资基金在资本配置者群体中也罕见的公开披露了其在许多顶级科技基金作为LP的投入,如a16z和Coatue。

中东是一个将成为美国和中国之间主要的竞争战场,无论是在科技上还是外交上。美国无疑是当前并长期在该地区投入的大国,也因此经历了许多不幸的战争和无效的和平谈判。与此同时,作为“外交新人”的中国,在调解沙特阿拉伯和伊朗之间关系恢复方面已取得了早期的胜利。

外交与云计算的碰撞

如果发生的话,这一即将到来的全球云计算大战让人想起了几年前的5G斗争,当时美国政府强力施加外交压力,迫使各国不要用华为和中兴的电信设备建设本国的5G网络。在德国、法国、荷兰、日本和印度等与美国有正式联盟关系的国家,外交压力在某种程度上奏效了,但在世界其他地方效果较差。这在很大程度上是因为美国没有本土的替代品,外交压力背后底气不足。

美国外交官不会在云计算方面遇到同样的问题。几乎在每一项衡量维度上,美国前三大云平台都比中国前三大云先进。中国云唯一可以想到的优势也就是靠政府补贴的支持下,打一场价格战,针对那些大致无差别和商品化的底层云服务,如存储或容器化服务器。这是一场美方应该赢的科技战。

本篇文章强调的三个地区 - 东南亚、拉丁美洲、中东 - 都是所谓的 “外交摇摆” 地区,他们与中美两大国的盟友关系并不明显倾向于那一方。这种“摇摆”状况是有战略价值的,因此会继续一段时间,这三大地区不想站队,归入任何一方,从而享受着 “被追” 的地位,放大自己的影响力、独立性,来获得最佳的待遇。这些待遇很可能以增大数据中心投资以提高数字化速度的形式呈现,或与当地大企业或政府部门给大幅折扣的云计算合同的形式出现。所有这些因素都使这三个地区值得密切关注,因为外交正与云计算相碰撞。

尽管这场云计算大战是一场美国云厂商占有极大优势的竞争,但美国政府对科技大厂的敌视态度加上了一丝尴尬。正当国务院寻求动员AWS、Azure和GCP在全球范围内对抗中国云厂商时,联邦贸易委员会(FTC)正在起诉亚马逊Prime产品的“暗模式”(dark pattern)手法,试图阻止微软收购游戏公司动视暴雪,而司法部正在起诉谷歌在互联网广告生意的垄断。

当自家政府在国内试图打压你的时候,很难自愿地在海外为政府效劳。即使AWS、Azure和GCP决定 “国家优先” 是重要的,撇开那些来自监管者琐碎的反垄断怨言,你真的想让外交官员来做云计算服务的预售工作吗?