During Christmas last year, I read one of the few biographies available on Masayoshi Son, titled “Aiming High”. Written by Atsuo Inoue, the version I read was an English translation of the Japanese original. Perhaps due to the “lost in translation” problem, it was not the best biography I’ve read, and the book was mostly an uncritical celebration of Masa’s career and life story. However, it did give a window into how Masa thinks.

When Softbank grabbed headlines last week for suffering its biggest quarterly loss in company history – a whopping $24.5 billion USD – the news triggered me to both watch Softbank’s entire earnings presentation and re-read parts of “Aiming High”. Masa’s tone and outlook turn out to be surprisingly consistent throughout the years – a blended stream of seemingly contradictory reflections of extreme humility and extreme bravado – making his psychology difficult to understand. But if we dissect Masa's own words and, in turn, how Softbank’s business works, everything is quite rational.

Waxing schadenfreude on Masa’s financial losses may be one of the tech sector and business media’s favorite parlor game, generating headlines like “The SoftBank Experiment Has Failed”. Many people think what Masa is (and has been) doing is crazy and irrational. But these commentaries rarely see things through the eyes of Masa himself and understand his own rationality, all hidden in plain sight.

Home Runs Worked, So More Home Runs

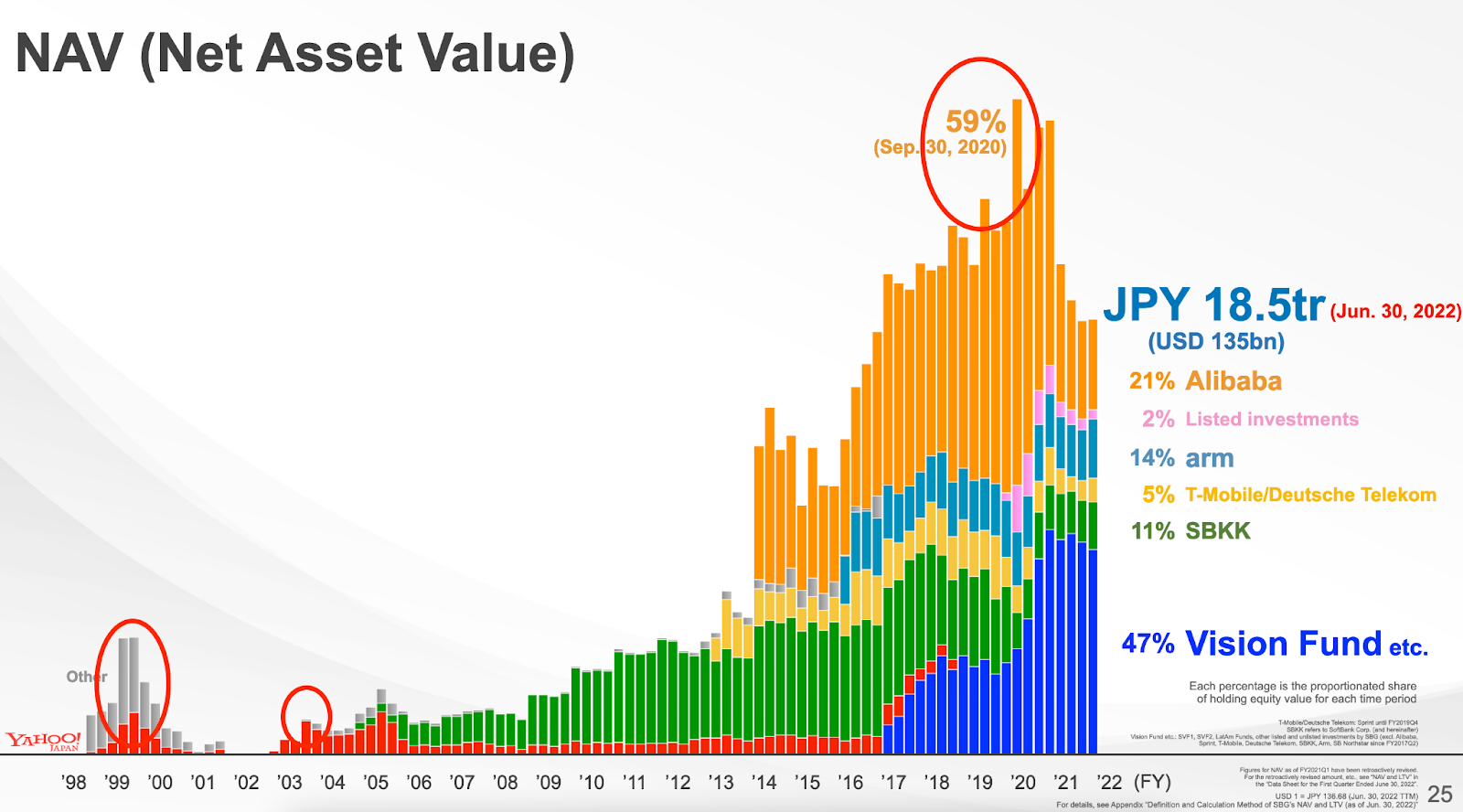

The one chart that illustrates best Masa’s rationality and thought process this slide in its earnings presentation:

Softbank has been, for most of its lifetime, a “home run” business, though it’s different from a typical VC business.

I circled in red three of the most telling moments of this phenomenon. The obvious, big circle is at the height of Alibaba’s valuation in September 2020, when it made up 59% of Softbank’s total Net Asset Value (NAV). The other two, less obvious circles both had to do with Yahoo. In the pre-2000, dotcom bubble moment, Yahoo accounted for close to half of Softbank’s NAV. During the post-dotcom-bubble years of 2002-2004, Yahoo accounted for almost all of Softbank’s NAV.

The outsized proportion of these “home runs” in Softbank’s NAV reveals a profound point. “Home run” investments are well-understood in the context of “power law” distribution, which underpins how most VC funds operate. However, they play a uniquely instrumental role in their contribution to Softbank’s balance sheet, giving it fuel to fund itself through both good and bad times. Thus, Softbank holds on to these “home runs” for as long as financially possible (unlike a VC), because its very success and survival depends on them as cushions.

During the before and after periods of the dotcom bubble, Softbank’s investment in Yahoo played that role. Now, as Masa goes through another tough period, Softbank’s Alibaba investment is playing that role – using its stake in China’s e-commerce and cloud computing giant to raise $22 billion in cash via a complex instrument called “prepaid forward contracts” to weather the storm.

An early investment in Alibaba may be the crowning accomplishment that leads most investors to sail into the sunset with fortune and glory. But in Masa’s rationality, Alibaba revealed a weakness in Softbank’s distinct organizational structure and corporate growth strategy – it needed more “home runs”. However, they did not have a good way to produce more.

As Masa admitted in “Aiming High”:

“In China and the rest of Asia we scouted Jack Ma well before anyone else, although that – if you want my opinion – was only a half-success at best and we could have done better.”

This “half-success” was confirmed in Sebastian Mallaby’s new chronicle of the VC industry, “The Power Law”. In the book, Mallaby described the way Masa found Jack Ma was mostly by happenstance, when Goldman Sachs was getting cold feet and wanted an investor to mark up its tiny China portfolio of seven fledgling tech startups, one of them being Alibaba. Masa ended up investing in several of those first generation China tech startups, including $20 million in Alibaba. Only Jack Ma’s outfit turned out to be a success of “home run” proportion.

In his many attempts at “home run” swings, Masa was haunted by his mistakes of omission, especially in his inability to take a swing at Amazon. During a 2020 interview, he candidly shared with an embarrassed laugh, how he could have invested $100 million in Amazon pre-IPO:

Given his success in investing $100 million in Yahoo one month before its IPO, Masa had every reason to believe that putting in another $100 million right before Amazon’s IPO would’ve given him another “home run” to keep the Softbank NAV pie growing.

The problem was Softbank ran out of money.

In this rather introspective admission when talking about his reasoning for raising Vision Fund 1 in “Aiming High”, Masa said:

“Going forward there’ll be no excuses. I’ve realised that up until now the problem has always been we never had the money….We always had loans to repay. I’ll tell you a story about Jeff Bezos, before Amazon went public. The two of us met in private and I told him I want to invest in the company – we actually ended up going back and forth with negotiations for about four hours. But SoftBank were just that little bit short on the financial front.”

So to avoid future errors of admission, to always get a swing at the next Amazon, the most rational thing to do was, of course, to raise $100 billion dollars.

Money = Home Runs

Despite its lofty goal of investing in the “AI Revolution'', Vision Fund was all about making sure Masa never runs out of money. Even though Vision Fund 1 was often labeled a venture capital fund, it was structured as a traditional private equity fund. The fund has a five year investment period upon final closing and a minimum fund lifetime of 12 years.

Besides Softbank’s own $28 billion, here is where the rest of the $100 billion of Vision Fund 1 came from:

- Saudi Arabia’s sovereign wealth fund: $45 billion

- Abu Dhabi’s national wealth fund: $15 billion

- Apple: $1 billion

- Rest of $11 billion from: Qualcomm, Foxconn Technology, Sharp (owned by Foxconn), Larry Ellison’s family office

Now that we are five years past Vision Fund 1’s closing in 2017, what did Masa learn during this time? Here is what he said during Softbank earnings presentation’s Q&A segment:

“For Vision Fund 1, we were making big swings, Uber, Didi, WeWork…we were making big swings, and couldn’t hit the ball…Because my emotion was very strong to specific companies…that’s something that I learned.”

As it turns out, even if you have all the money in the world to take big swings, it does not make up for bad judgment. Masa is refreshingly honest about admitting his many bad judgments. But a more subtle learning that he did not share so publicly, but showed in the way he now runs Vision Fund 2, is he realized he did not necessarily need “home runs” to keep Softbank’s NAV growing or his outside investors happy.

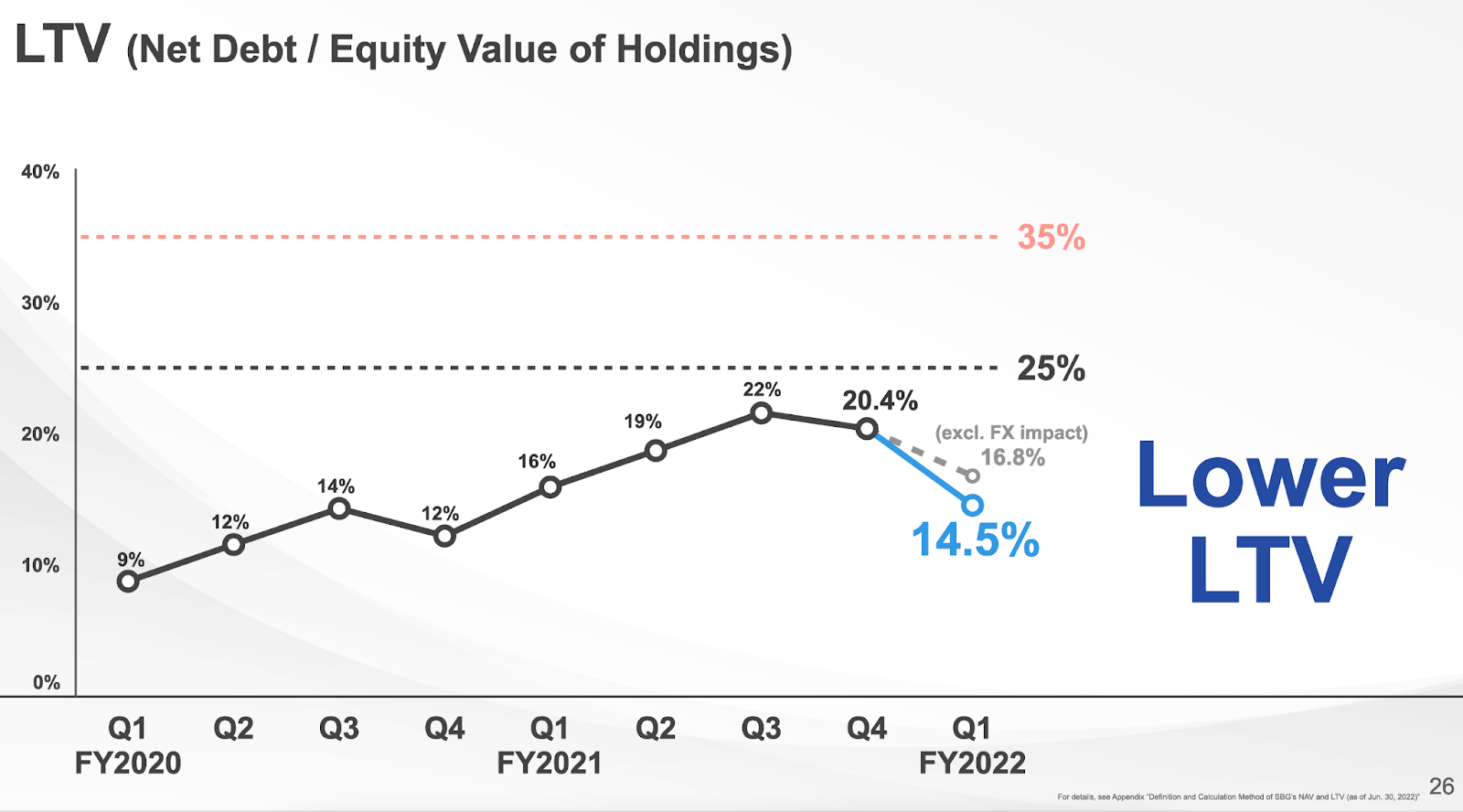

Given the size and nature of Vision Fund 1’s outside investors, all sovereign wealth funds or massive corporations (with the exception of Ellison’s family office), they are not expecting the high-level returns (in the form of “home runs”) in the same way typical endowments expect from typical VC firms. As long as the Vision Funds can keep growing Softbanks NAV over time and keep the company’s loan-to-value (LTV) ratio below 25% – a rather financially conservative threshold for an aggressive risk taker like Masa – Softbank can always live to fight another day.

All three Vision Funds (1, 2, and LatAm) combined now make up 47% of Softbank’s total NAV, its largest category partly because Alibaba’s value fell precipitously. By converting part of its Alibaba stake into cash, Masa has managed Softbank’s LTV down to 14.5% from a recent high of 22%, in order to be in “defense mode”.

With some hard lessons learned from Vision Fund 1, what is now the most rational thing to do in “defense mode”?

In Masa’s own words:

“Rather than aiming for the home run, we try to aim for first base hit or second base hit, make sure we have good hits…”

From Home Runs to Base Hits

Unlike Vision Fund 1, Vision Fund 2’s only source of capital is Softbank itself. It is essentially a corporate venture arm, not a VC or private equity fund. Masa is also taking full control of Vision Fund 2, either because he no longer trusts Rajeev Misra, who managed Vision Fund 1, or because he wants to redeem his own mistakes.

But with all these ups and downs of multi-billion dollar proportions, what is Masa really trying to build? Again, in “Aiming High”, he shared this reflection:

“‘What did Son Masayoshi invent?’ I want future generations to ask that question and I want the answer to be I invented an organizational structure which has shown growth over 300 years…we’ve got to adopt a ‘cluster of number ones’ strategy.” (Bold emphasis mine)

“Home runs” like Yahoo and Alibaba used to work for the organizational structure of Softbank. So Masa rationally wanted to try to hit more “home runs”. After failing and losing billions of dollars in the process, he is adjusting his game to go for base hits. If you hit enough of them, base hits can generate just as many NAV points for Softbank’s organizational structure (à la Moneyball), just less dramatically. As someone who also owns his hometown baseball team, the Fukuoka SoftBank Hawks, Masa knows how this works better than most.

In an uncertain and volatile world – war, climate change, higher interest rate, geopolitical hotspots, supply chain, domestic polarization, the list goes on – Masa’s outlook and action appears perfectly pragmatic and rational, for him, not for me, or you.

理解孙正义的理性思考

(本篇中文版文章是读者 Ben Yu 做的编译,我做了一些修改后发表。非常感谢Ben的贡献!)

去年圣诞节的时候,我阅读了一本有关孙正义的传记《Aiming High: Masayoshi Son, SoftBank, and Disrupting Silicon Valley》,作者是井上笃夫。相对来说,孙正义的传记没有那么多本可以选择。我阅读的版本是日文原版的英译本,也许是翻译原因,这本书并不是我读过最好的传记,而且整本书都在极力夸奖孙正义的职业生涯和成就。当然,这也不妨碍这本书让我们能够更了解孙正义的一些思考方式。

几周前的一则头条新闻:软银遭遇公司历史上最大的季度亏损——高达 245 亿美元。当我看到这则新闻后,我立即读了软银的全部财报,也重新阅读了《Aiming High》里的部分内容。这些年来孙正义对外表露的形象和观点惊人地一致:一种极端谦逊和极端夸大的混合。这让理解他的想法变得很困难。但如果我们去看孙正义过去说过的话,以及软银的业务运作模式,这一切又都相当理性。

我们能听到很多外界的声音,一些科技行业或者商业媒体的各色人士很喜欢对孙正义的亏损幸灾乐祸,也写过很多诸如《The SoftBank Experiment Has Failed》这种标题的报道。包括很多人会认为孙正义正在做的事(也是一直做了很长时间的事)是极度疯狂和缺乏理性的。但这些声音很少通过孙正义自己的视角来看事情,去评价理性。

要有更多的本垒打

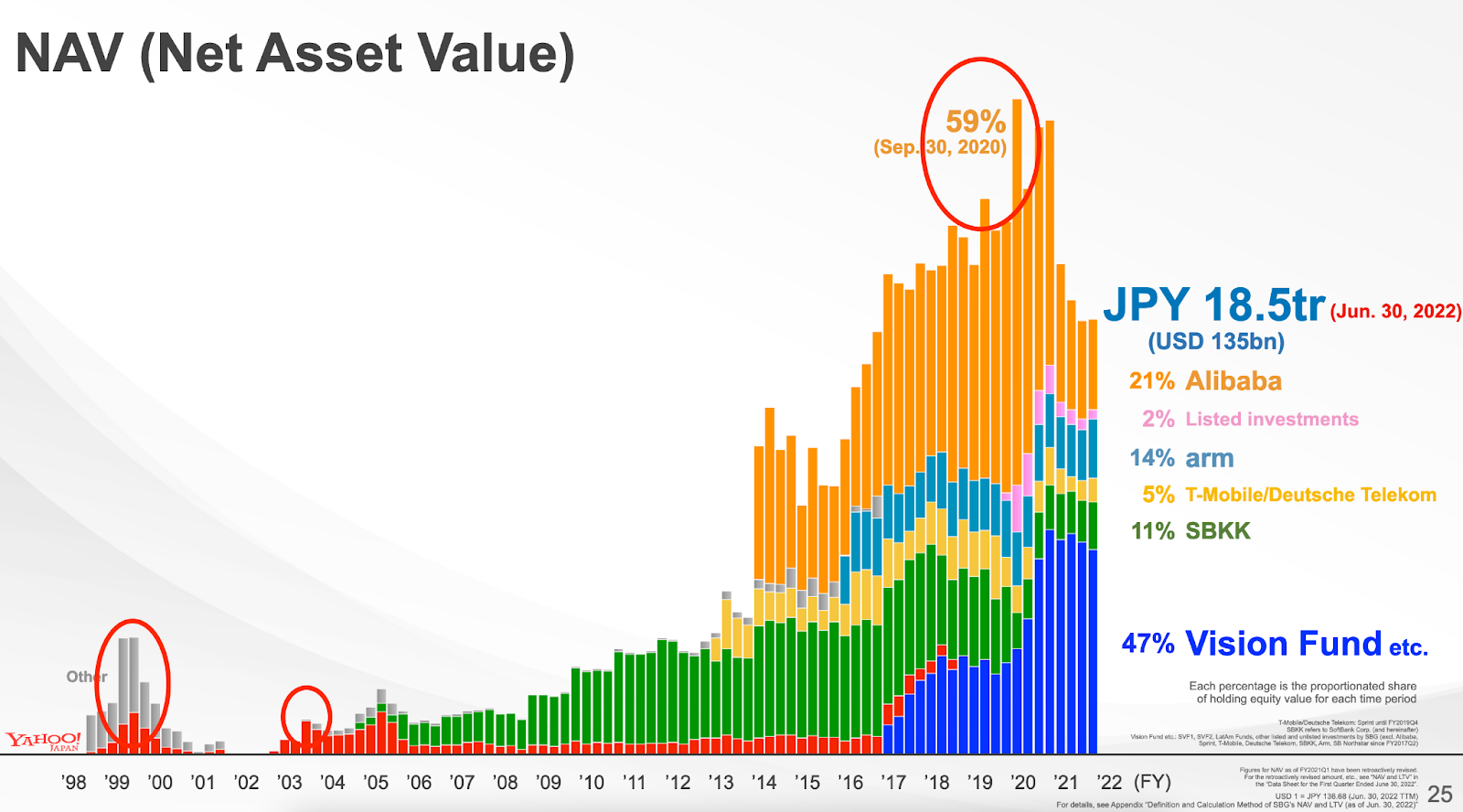

下面这张反应软银近几十年资产变化的图表最能说明孙正义理性的思维过程:

软银在大部分时间里都有一个至关重要的,类似于“全垒打”的关键业务。但它和典型的风险投资不太一样。

我用红色的圈标注出了三个最能说明问题的关键时刻。图表中最高的那个区间,对应阿里巴巴的估值在 2020 年 9 月达到顶峰,当时它占软银总资产净值(NAV)的 59% 。另外两个不那么明显的圈子则都与雅虎有关。在 2000 年前的互联网泡沫时期,雅虎占据了软银资产净值的近一半。在2002-2004 年互联网泡沫崩盘后的时期,雅虎几乎占据了软银全部的 NAV。

这些关键业务在软银的 NAV 中所占比例如此大,说明了一个非常重要的问题,风险投资的大部分回报来自于少数几个投对的公司,整个行业符合幂律分布的发展。然而,对于软银的资产负债表来说,这些关键的全垒打投资发挥着独特的作用,为软银渡过好或坏的市场状况都提供了资金支持。因此,软银在财务上会尽可能长久地持有这些本垒打投资(这一点和传统风投不太一样) ,因为它的成功和生存都依赖于这些投资作为缓冲。

在互联网泡沫前后,软银对雅虎的投资扮演了这个关键投资的角色。现在,随着孙正义正在经历另一个艰难时期,阿里正在扮演这个角色,通过一种名为“预付远期合约”(prepaid forward contracts)的复杂金融工具筹集 220 亿美元现金,以度过这场风暴。

能够在早期就投中阿里,对于大部分投资人来说都是值得回顾一生的成就。但孙正义的理性揭示了软银独特的组织结构和企业增长战略的一个弱点 —— 需要更多的“本垒打”投资。然而,软银并没有一个好的方法找到更多的这种机会。

正如孙正义在《Aiming High》中说的:

在中国和亚洲其他地区,我们比任何人都更早地找到了马云,尽管——如果你想知道我的看法——这充其量只是半成功,我们本来可以做得更好。

这种所谓的“半成功”在塞巴斯蒂安·马拉比(Sebastian Mallaby)关于风险投资行业的新书《The Power Law》中得到了证实。在书中马拉比写到,孙正义发现马云的故事几乎纯粹是偶然,当时高盛临阵退缩,希望能找到一个投资人接手高盛在中国投资的七家初创科技公司。孙正义最后投资了这其中的几家,其中就包括给阿里巴巴的 2000 万美元,而其中,只有马云是唯一成功的“全垒打”。

在多次尝试全垒打的过程中,孙正义更被自己的疏忽所困扰,尤其是他错过了亚马逊。在 2020 年的一次采访中,他尴尬地笑了,坦诚地分享了自己是如何在亚马逊 IPO 前试图投资 1 亿美元的:

鉴于他在雅虎 IPO 前一个月成功投资了 1 亿美元,孙正义有充分的理由相信,在亚马逊 IPO 之前再投资 1 亿美元,将会给他带来另一个“全垒打”,以保持软银的 NAV 的增长。

问题是软银没钱了。

在《Aiming High》中,孙正义谈及筹集Vision Fund I 的理由时,反省到:

“永远看向未来,不要有任何借口。我已经意识到我们的一个问题,到现在为止我们没有足够的钱……我们一直在偿还贷款。我和你讲一个我和贝佐斯的故事,在亚马逊上市之前,我们两个私下见面,我告诉他我想要投他的公司——我们最后来回谈判了大约 4 个小时,但最后软银在资金方面差了那么一点点,没有投成。”

所以,为了避免以后再犯错误,为了总能在下一个亚马逊上下注,最理性的做法当然就是募资一个 1000 亿美元的基金咯。

资金量 = 全垒打

尽管 Vision Fund 对外的宣传是专注投资人工智能领域,但它首要的目的是确保孙正义不会再缺钱了。Vision Fund I 经常被贴上风险投资基金的标签,但它的结构更像是一个传统的私募股权基金。该基金的投资期限为 5 年,基金成熟期限为 12 年。

除了软银自己的 280 亿美元,Vision Fund I 其余的资金来自:

- 沙特主权财富基金:450 亿美元

- 阿布扎比主权财富基金:150 亿美元

- 苹果:10 亿美元

- 其余 110 亿美元来自:高通,富士康科技,夏普(富士康所有),Larry Ellison的家族办公室

从 2017 年算起,Vision Fund I 已经成立了 5 年多,孙正义从中学习到了什么呢?下面是他在软银财报发布会的问答环节中的发言:

“对于Vision Fund I,我们有大幅度的波动,Uber、 滴滴、 WeWork... 我们做了很多事情,但没能挥出关键一击... 因为我对某些公司的情绪过于强烈...这是我学到的东西。”

事实证明,即便你有全世界所有的钱来承受剧烈的市场波动,也无法弥补错误的判断。孙正义非常坦诚,承认了很多自己的误判,这些并未表现在他对外的分享中,而是表现在他现在经营Vision Fund II的方式上。他意识到他不一定需要“全垒打”来保持软银的 NAV 增长,或让他的投资人满意。

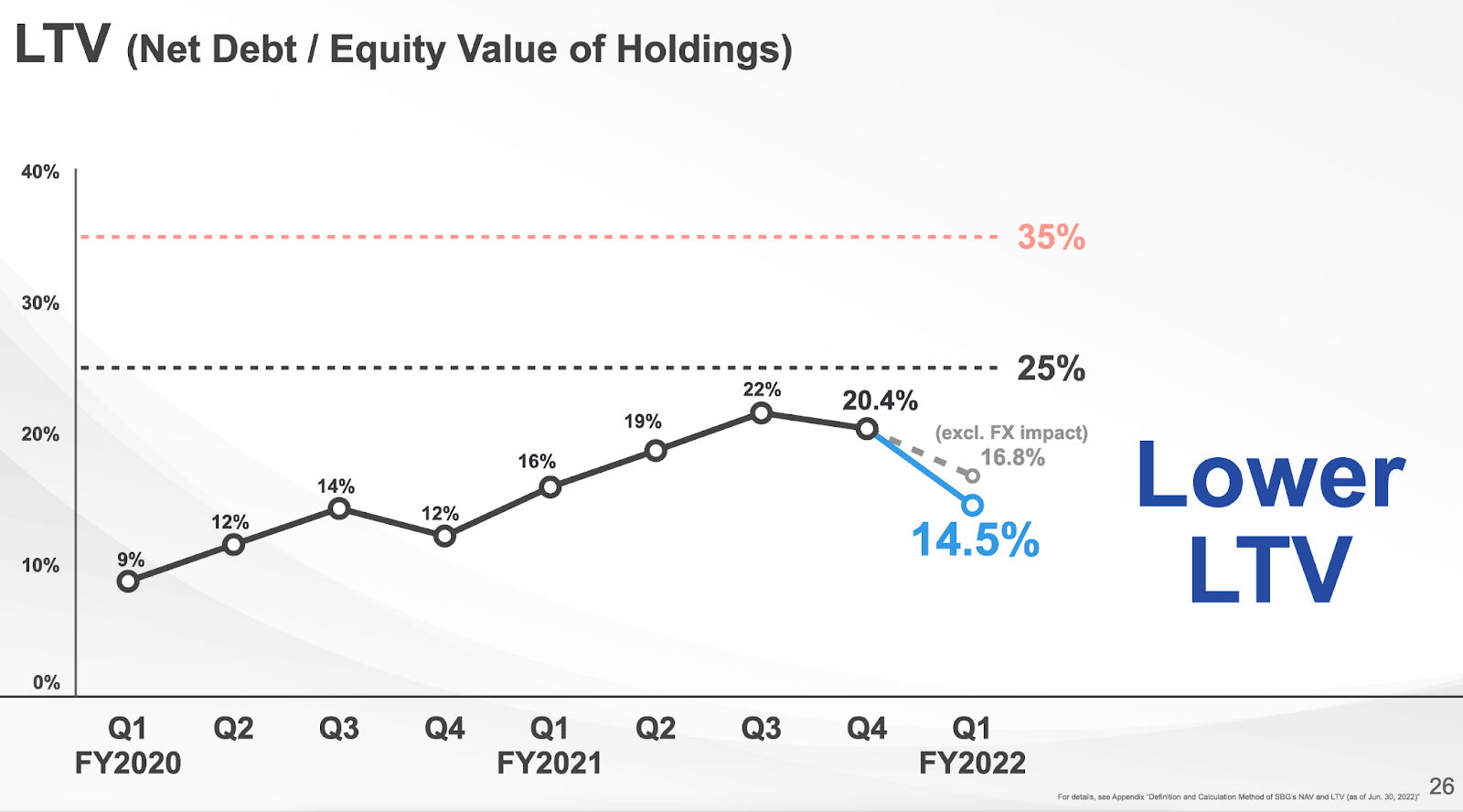

考虑到 Vision Fund I 的外部投资人、所有主权财富基金或大型企业(Ellison除外)的规模和性质,他们并不期待高水平的回报(以“全垒打”)。就像典型的捐赠基金期望从典型的风险投资公司获得的那样,只要愿景基金能够让软银的 NAV 长期保持增长,并保持公司的贷款与价值(LTV)比率低于 25%——对于孙正义这种这么喜欢大波大浪的风险承担者来说,这是一个相当保守的财务门槛——软银总能活到下一天。

三只 Vision Fund 加起来现在占软银 NAV 总额的 47% ,这是软银 NAV 中的最大类别,部分原因是阿里的价值急剧下跌。通过将其在阿里的部分股份转换为现金,孙正义管理软银的 LTV 从最近的高点 22% 降至 14.5%,以采用一种防御手段。

从 Vision Fund I 中吸取了一些惨痛的教训,在采用防御手段时,现在最理性的做法是什么?

用孙正义自己的话来说是:

“我们的目标不是全垒打,而是一垒安打或二垒安打,确保我们有好的安打...”

从全垒打到安打

与Vision Fund I不同,Vision Fund II 的唯一资金来源是软银本身。它本质上是一家企业风险投资机构,而非风险投资或私人股本基金。孙正义还将全面控制 Vision Fund II,要么是因为他不再信任管理 Vision Fund I 的拉杰夫·米斯拉(Rajeev Misra),要么是因为他想修正自己的错判。

但是,面对这些价值数十亿美元的大起大落,孙正义到底想建造什么呢?同样,在《Aiming High》一书中,他分享了这样的思考:

“‘孙正义发明了什么?未来子孙后代问这个问题时,我希望答案是:我发明了一种组织结构,300 多年来一直在增长...... 我们必须采取一种‘聚类数’的战略。”

像雅虎和阿里这样的 “全垒打” 投资案例曾经在软银的组织结构中发挥重要作用。因此,孙正义想要继续打出更多的“全垒打”是很理性地选择。在这个过程中失败并损失了数十亿美元之后,他正在调整自己的打发,争取更多的安打。如果你打出足够多的安打,最终的效果加起来可能和全垒打差不多,还是可以为软银的组织结构产生同样多的净资产收益率点(就像魔球理论一样),只是过程没那么大起大落而已。实际上孙正义拥有自己家乡的棒球队——福冈软银鹰队,他比大多数人更了解这一点。

在一个充满不确定性和动荡的世界中——战争、气候变化、更高的利率、地缘政治、供应链、两极分化……孙正义的视角和行动其实还蛮务实和理性的,只是不是你我的视角所轻易能看出来的理性。