Welcome to Interconnected Capital’s Q1 2026 performance update letter.

To new and old readers alike, a friendly reminder: I run a global technology long-only fund focused on investing in both the hardware and software “picks and shovels” of the interconnected global digital AI economy. I draw on my technology business operator’s experience and geopolitical antennas to bring an edge to how I assess a tech company’s rhythm and prospects in a constantly changing world. [1]

As always, first the numbers, then the reflections.

[1] My past experiences include: senior leadership position at GitHub (the world’s largest developer and open source technology platform, now owned by Microsoft), a unicorn database startup, early stage VC, and the White House and Department of Commerce during the Obama administration. I studied law and computer science at Stanford; international relations at Brown.

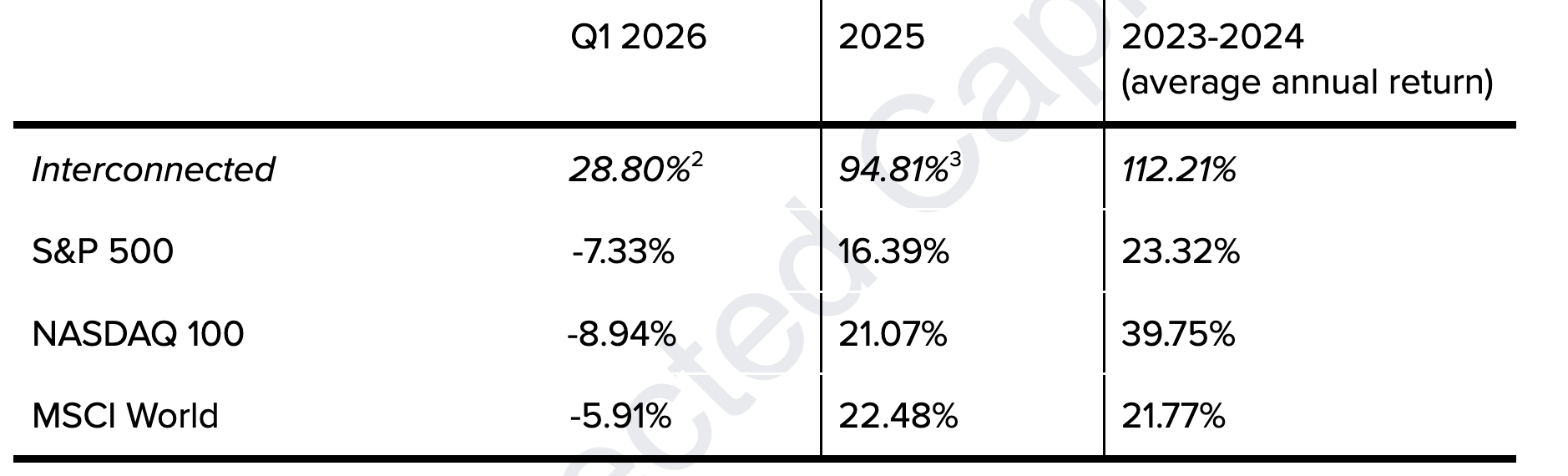

[2] Includes January 1 - March 31, 2026. Gross returns. Unaudited.

[3] Includes January 1 - December 31, 2025. Gross returns. Audit in progress.

Portfolio positions in random order (as of March 31, 2026):

- CIENA CORP

- NEBIUS GROUP NV

- APPLIED MATERIALS INC

- OUSTER INC

- WERIDE INC ADR

- ARM HOLDINGS PLC-ADR

- INTEL CORP

So What Happened in Q1?

While the number more or less speaks for itself as I materially outperformed a down market, let’s talk honestly about what worked and what didn’t work.

A big part of what worked was the set up I had going into this new year. As I shared in the 2025 annual letter, heading into 2026 a good chunk of our portfolio was made up of three companies – Nebius, Intel, Ciena. Our sizing at that time reflected my high conviction level of these companies’ growing prospects, which are being reflected in their share prices in meaningful ways. We did the work on these companies at various points in 2025 and 2024, so the fact that the “big three” carried the portfolio during Q1 was not due to anything I did during that quarter. Such is the dynamic and rhythm of long-only and long-term investing.

Additionally, one of the opportunities I spelled out in my annual letter – growing demand for CPUs due to growing agentic workloads – materialized rather quickly. What started out as an under the radar topic at the start of the year has become the fodder of daily chatter, as more and more investors recognize that CPUs are cool again. During the early part of last quarter, I acted decisively to seize this opportunity, by both adding to Intel, whose x86 server CPU franchise still has a sizable market share, and starting a position in Arm, who is wading aggressively into selling chips directly with its newly introduced Arm AGI CPU.

I have always been fond of Arm, as a rare semiconductor IP powerhouse with an enviable developer audience (I always start with the developers). I have been monitoring and writing about the company for many years (here is a fun piece from four years ago). According to the company, there are over 22 million Arm developers worldwide. If true, that would be close to half of all developers total. (My own research and experience suggest that the global developer population is around 50 million.) If the ownership by Softbank isn’t so tight – roughly 90% of the company is owned by Masa and not part of its publicly-traded float – and thus so volatile, Arm would have been an easier name to own. But the CPU tailwind is strong and few benefits from it more directly than the Japanese-owned British champion.

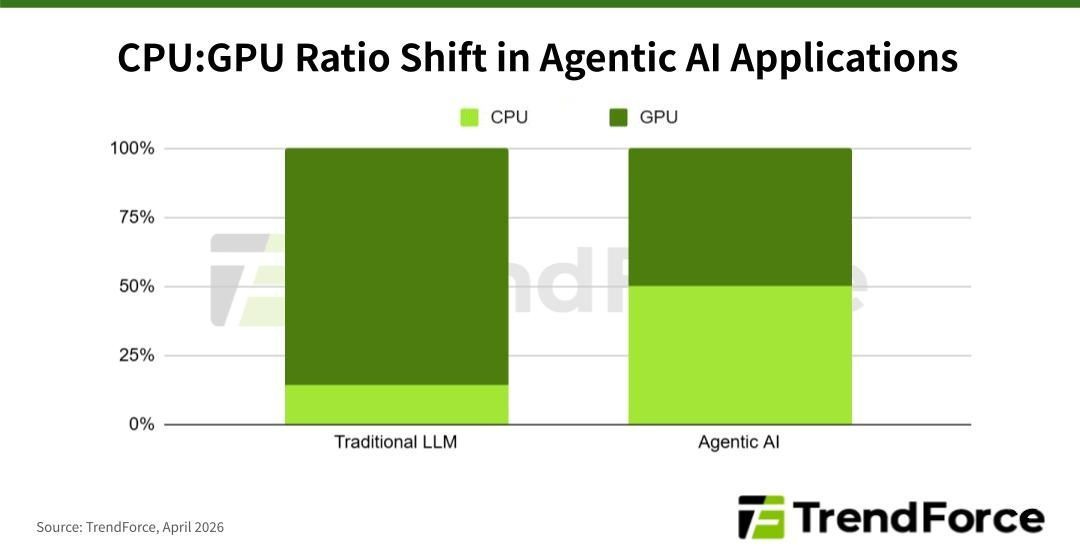

While the CPU story is a hot topic, there is still a long way to go for the chips to be fabbed, shipped, and running agentic workloads. As this TrendForce chart projects, the CPU:GPU ratio is approaching half and half for agents, from a 10:90 split for training and running LLMs as chatbots. This tailwind should blow for a while longer.

Now let’s turn to what did not work!

One risk management tactic I mentioned in my annual letter was using put options periodically and opportunistically to protect the long-term potential of our best ideas, while moderating the short-term gyration of the whims and tickles of the public market, of which we had a lot in Q1. I applied this tactic to our “big three” positions. After the quarter ended, I did a tally of how all these hedges collectively performed and the result was basically flat. These hedges were never designed to make big money, few hedges are. Given how much the three names have risen, having these hedges come out effectively a wash is a tolerable outcome, though by no means a perfect one. I will continue to perfect this tactic for the purpose of risk management as time goes on.

I also ventured into the collapse of the SaaS market to express my view on the other opportunity I see – the need for deterministic guardrails to govern probabilistic AI agents. This foray turned out to be more painful. After doing all the tally, my foray in the SaaSpolcalypse resulted in -2.45%. As you can see in our portfolio positions, I have closed all software exposure and don’t plan to start any for a while. I will continue to actively monitor the sector as I wait for more market clarity.

What are some lessons I learned from this experience?

First, from my deep dive research into this “guardrails” opportunity, I learned that even the largest of the enterprises (think a Fortune 500 bank) are tolerating the risks of probabilistic AI agents and rolling them out en masse without all the guardrails I had expected to be in place first. The pressure from the board level and the C-suite to use more AI is strong, the use case specific risks can be managed, so agents are being deployed, while companies wait for guardrails to catch up.

Second, it is more likely that the best, most AI-native guardrails will be built by new startups, not publicly listed companies in the same domain, which are by definition older and tend to be less innovative. There is already a fast-growing and crowded landscape of cybersecurity startups tackling various dimensions of agent security, identity, and governance. The guardrails could also be built by the AI labs themselves, who are the ones building the most capable agents anyways. There is no reason why Anthropic couldn’t build the best Claude agent and the Claude guardrails to keep the agents in check, if the customers trust them to do both (still a big if).

Third, speaking of Anthropic, the market is operating on a “sell software every time Anthropic releases a feature” mode that makes rational investing difficult to execute. I don’t think the market is entirely wrong here. The market is never entirely wrong, or right. The future for all software companies is muddied by AI. This muddiness will continue, I suspect, until Anthropic and OpenAI execute their respective IPOs. That will finally open up the vault and disclose metrics and financials to allow for a more apples-to-apples comparison. Until then, price actions will be volatile and triggered by vibes and fears, not fundamentals and rationality. Thus, I plan to stay out of the chaos until the IPOs. Luckily, we won’t have to wait too long; both are expected to happen in 2026.

“Roughing It” in the AI Age

From my research into the guardrails thesis, plus other data points gathered on the fast pace of agent adoption at large especially in software engineering, it is clear that we are kind of winging it and roughing it head first into the AI age. Not to mention that the entire world order is entering into a new phase of “roughing it”, with two literal regime changes in Venezuela and Iran already.

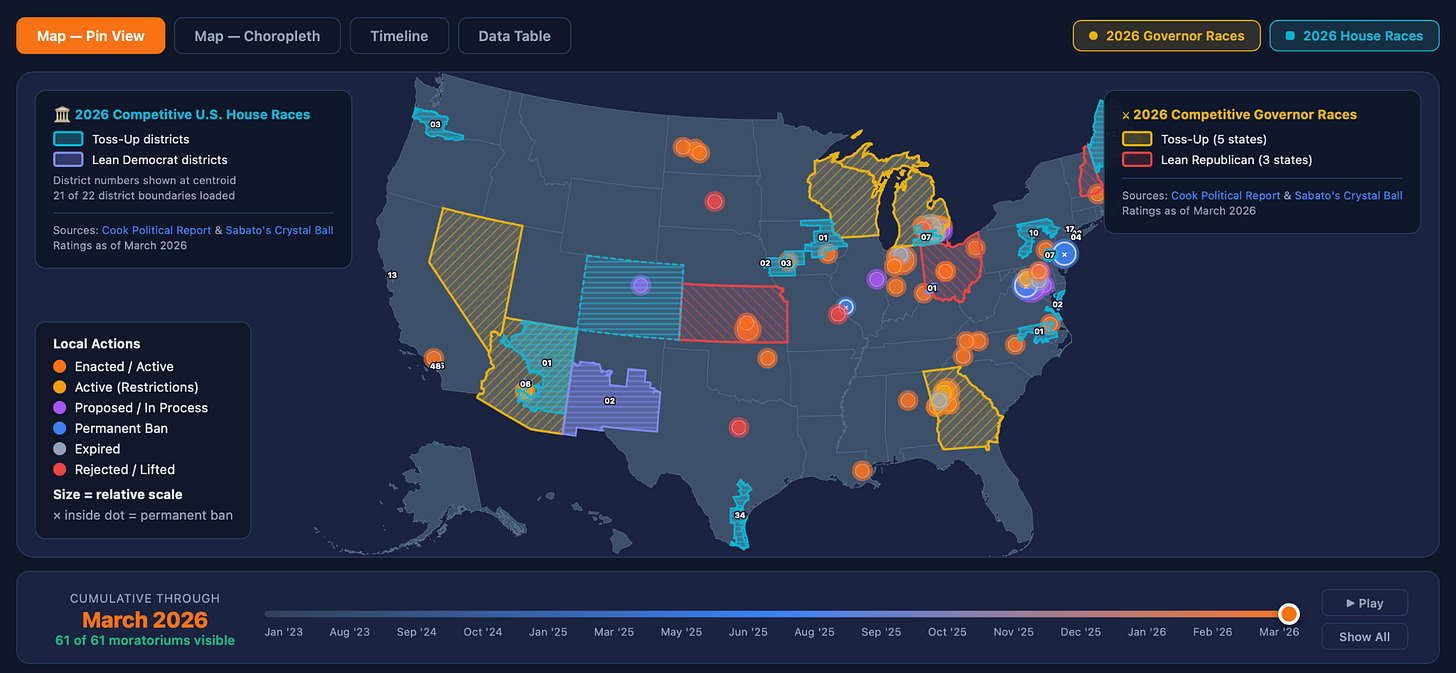

To wrap some data, metrics, and clarity around the chaos, I built a dashboard (with the help of AI, of course) tracking all the data center moratoriums popping up across the United States. As you may recall, data center construction becoming a bipartisan punching bag and hot button local political issue was a major risk I cited going into this year. The dashboard is now published in the “research” section of Interconnected Capital’s website and will be updated every two weeks.

The tl;dr of the findings is that this risk is materializing faster than I had anticipated, with moratoriums of different sizes and lengths popping up with increasing frequency starting in Q4 of last year and intensifying as this year progresses. The risk is also squarely bipartisan, even though the news coverage you might have read on this issue often casts it as a liberal or progressive one. Out of the 44 counties that have active bans, 26 voted for Trump, 17 voted for Harris. (You can press the “play” button on the dashboard to visualize this evolution from January 2023 to now.)

As I prepare to face the rest of a rough 2026, the word that keeps popping back into my head is “equanimity”. I reflected on this word last year around the same time in the letter I wrote to you then, titled “Equanimity Investing”. It was the quarter when Liberation Day happened, when maintaining an equal, leveled mind came in handy. Looks like this mental state will be useful again.

One trick I often use to inject some equanimity into my life is to take my baby boy on a long walk in the neighborhood. While he points at trees and airplanes, I slip on an audiobook that has nothing to do with tech or investing or geopolitics. (There is only so much of those podcasts a mind can handle.)

One recent discovery was a memoir by Mark Twain, fittingly also titled “Roughing It”. It was published in 1872, several years before the iconic American author wrote his household classics, The Adventures of Tom Sawyer and The Adventures of Huckleberry Finn. This memoir was about his own adventures, traveling on stagecoach before the railroads were built into the western frontiers of America in the 1860s with his older brother, who was appointed the Secretary of the Nevada Territory, a high-ranking political office of the yet to be ordained Silver State.

It is a long book and I’m only a third of the way through. But listening to it has been a fun and calming teleportation into a different era of rampant get-rich-quick schemes, where Twain recounted tales of his younger self diving head first into silver mining and speculation in places like Humboldt County. He failed in his pursuit of getting rich off of silver, so he resorted to journalism and later writing. If he hadn’t failed, we might have never had the pleasure of reading the books he wrote and laugh at the jokes he crafted. And putting it all in perspective, that era of gold rush and silver rush was when the notion of investing in the “picks and shovels” of a wave first came from.

Whether it is investing in the “picks and shovels” of shiny metals or shiny AI agents, every wave begets its fair share of scammers and speculators (a shoe company pivoting into AI compute?), but also transformative changes and immeasurable societal benefits. They all exist together simultaneously, always have, always will.

As crazy and disorienting as things might feel right now, I still very much prefer roughing it in 2026 than roughing it in the 1860s, like Twain did. I hope you feel the same way.

Kevin S. Xu

April 17, 2026

(You can access the original letter in a view-only Google Doc link HERE.)

LEGAL INFORMATION AND DISCLOSURE

This letter expresses the views of the author as of the date indicated and such views are subject to change without notice. Interconnected Capital, LLC (“Interconnected”) has no duty or obligation to update the information contained herein.

Further, Interconnected makes no representation, and it should not be assumed that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This letter is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

Interconnected believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

All figures are unaudited. Interconnected does not undertake to update any information contained herein as a result of audit adjustments or other corrections. Past performance is not indicative of future results.

This letter, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Interconnected.