Back in January, I published our first Interconnected Annual Letter to share the Interconnected public market portfolio performance in 2022 and my learning along the way. Even though I don’t manage anyone else’s money but my own, writing the letter was a useful mental exercise to qualitatively make sense of the previous year, while quantitatively measuring myself against industry benchmarks.

Writing is one of the surest ways to improve one’s thinking abilities. It is also, as the designer and author Edwin Schlossberg like to say, a skill that can “create a context in which other people can think.” So to the extent that these personal, investing-focused, and reflection-oriented letters can also help our readers think, going forward, I plan to write a quarterly letter to share performance numbers and lessons learned, to be published within two weeks of a quarter’s end. Today’s letter is for Q1 2023.

(Evidently, this letter is already published behind schedule because I contracted Covid this month and am still dealing with symptoms. Sorry about that! Let’s hope this endemic won’t set me back again in the future.)

Q1 2023 performance and benchmarks comparison (as of March 31):

- Interconnected Portfolio: +80.65%

- S&P 500: +7.03%

- DJIA: +0.38%

- NASDAQ 100: +20.49%

- Russell 2000: +2.34%

- MSCI World: +7.88%

- Wilshire 5000: +7.26%

As an operator, I can speak from experience that a single quarter is rarely meaningful. Of course, on Wall Street quarterly earnings get over-analyzed and over-interpreted up the wazoo. Thus, I won’t extrapolate much from my performance (usual disclaimer applies: past performance is not indicative of future results). I also won’t share any industry, market, technology, or company prognostications in this quarterly update, again, because the time period is too short to be meaningful. Instead, I’ll share some key psychological learning in navigating the mental volatility of investing – something every investor feels on a daily basis – and how I wrestled with them, during an especially volatile Q1.

Circle of Competence Breeds “Gumption and Patience”

I put “gumption and patience” in quotes because this phrasing came from this Charlie Munger axiom:

“Successful investing requires this crazy combination of gumption and patience, and then being ready to pounce when the opportunity presents itself, because in this world opportunities just don’t last very long.”

The level of gumption that Munger is used to is in the millions of shares; the level of patience is waiting for years for an opportunity and then holding for decades. I am, of course, nowhere near that level, though I’m working to reach that level someday.

On a much smaller scale, I’ve been investing with both gumption and patience in mind, which presented a lot of new psychological challenges during Q1. Thinking back, these were just some of the (many) moments that caused internal psychological volatility for me: collapsing banks in the US and EU, Fed interest rate uncertainty, implications of China’s newly-formed government, TikTok hearing and the RESTRICT Act, GPT-4’s release, massive friendshoring in Mexico from Asia.

This list is in some ways just a reflection of what I pay attention to; you may have a different list. But what I realized was that whenever something triggers a high level of internal psychological volatility, the size of my gumption and the degree of my patience were tested. This effect went both ways. On some days, this psychological volatility made me double down the investments I’ve made. On other days, it tempted me to look at opportunities way beyond what I truly know. (Let’s be honest, who was not tempted to short the banking sector for at least a day or two last quarter?)

My saving grace is sticking with my self-defined circle of competence:

- DevOps

- Cloud infrastructure

- Open source (software and hardware)

- A subset of China tech that overlaps with the three areas above

- Technologies that have a strong influence on or by geopolitics and US domestic politics

By and large, I invest strictly within this circle, which is admittedly small, tight, and not conventionally defined. This “smallness” has the side effect of not making too many transactions. (I executed less than 20 orders total last quarter; I probably could have done even less and had similar or better results.) However, the same “smallness” also gives me anxiety sometimes. Am I missing opportunities? Should I start learning things I have relatively little advantage or expertise in, just to cover more bases?

There are pros and cons to every approach. So far, I’ve stuck with the pros of having a small circle of competence and decided to let the cons play out. I take comfort in the secular trend that the industries within my circle will all continue to grow for a long time – effectively making my circle “bigger” over time. One massive trend that reinforces this point is Generative AI. Although no one at this point can say who the winner/losers will be in the application layer of AI, it is quite clear that all the winners (and all the losers who will die trying) will pay a hefty sum to the cloud infrastructure providers, the makers of chips and networking equipments that power the training and running of models, and the ever-evolving AI models themselves, most of which are open source software. (For a thoughtful perspective on AI’s future growth through the lens and history of cloud computing, this post by Mitchell Hashimoto, who co-founded Hashicorp, is a worthwhile read.)

Having confidence in the future of my own circle of competence helped me in navigating the psychological volatility of last quarter to maintain some “gumption and patience.”

Concentration Moves the Needle

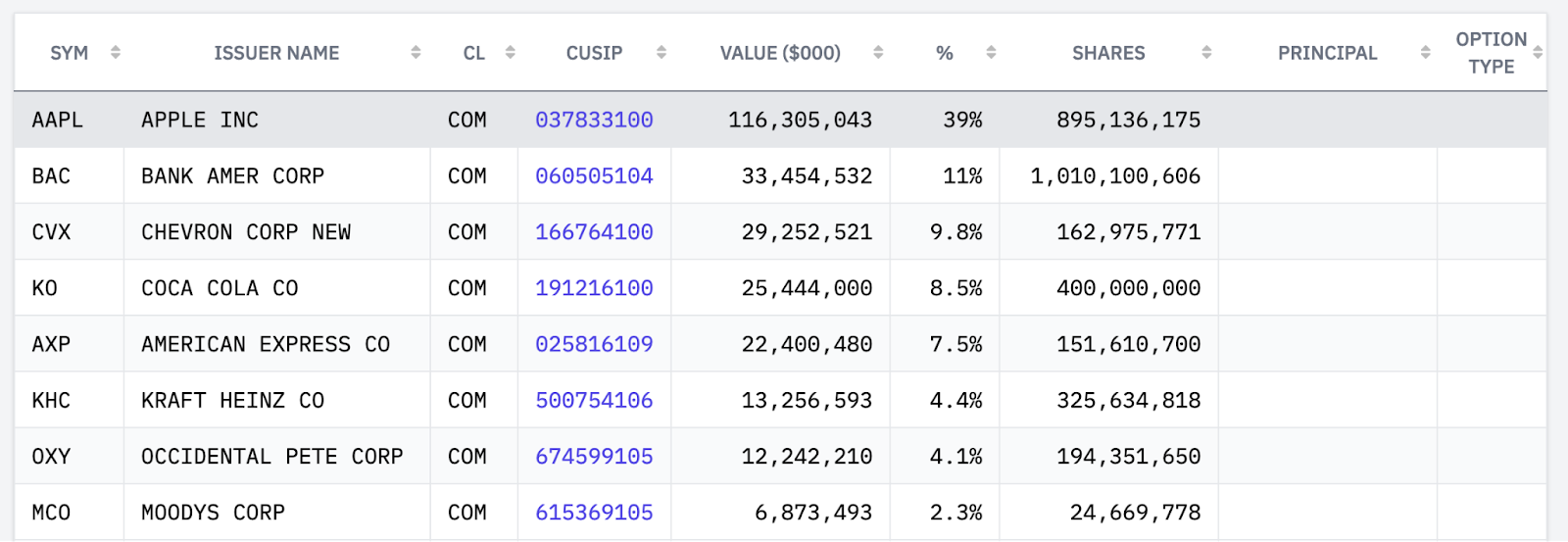

This learning is related to how I use my own circle of competence to balance my psychology when investing. Most students of investing are well aware of the lesson that concentration, not diversification, is how you achieve above average returns and move the needle of a portfolio’s performance. So this lesson is nothing new. Historical examples and current portfolios continue to reinforce this point. Stan Druckenmiller’s British Pound trade in 1992 is the classic, often-studied example. Berkshire Hathaway’s portfolio, with close to 40% concentrated in Apple, continue to be the living case study where concentration trumps diversification.

Intellectually understanding the benefits of concentration is one thing. Feeling the effects of concentration was quite another. Withstanding the ups and downs of a concentrated portfolio requires a strong stomach. As I put the theoretical wisdom of concentration in practice, the one thing that gave me a source of stability was, again, the comfort of my circle of competence.

I ultimately benefited from concentrating only within my circle of competence and not “dabbling” outside too much, which significantly moved the needle, as the Q1 results have shown. That being said, if one’s knowledge, confidence, and conviction in an investment rise, the concentration should only get bigger, which also makes staying psychologically stable tougher.

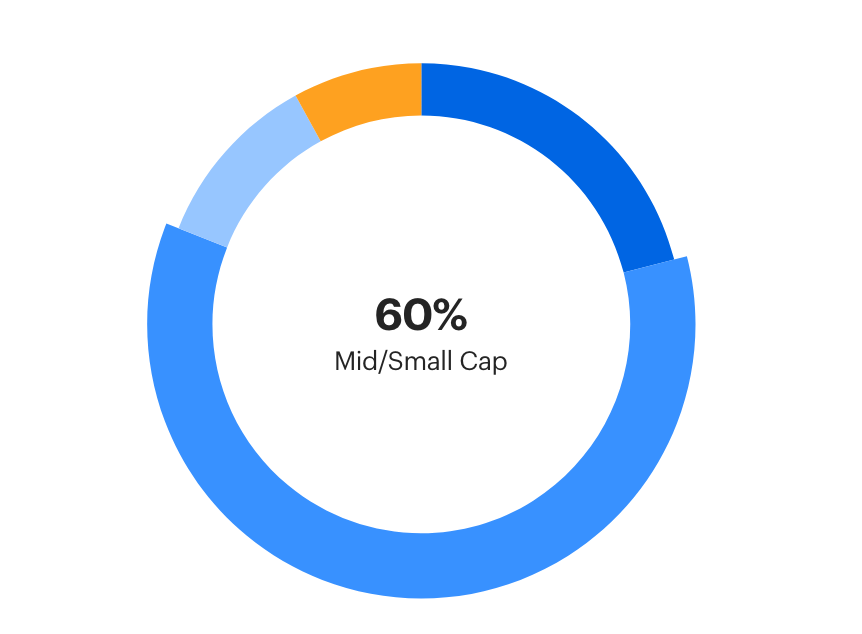

My portfolio (and my stomach) will be put to the test soon, as I have concentrated roughly 60% into one investment (see screenshot below). It is an opportunity that sits squarely within my circle of competence and is going against the market trend (thus somewhat contrarian).

Regardless of whether this one concentrated investment succeeds or fails, I will learn a ton from the experience, and I look forward to sharing those lessons. It is the psychological crucible that I want to put my temperament through. As Warren Buffett likes to say:

“The most important quality for an investor is temperament, not intellect.”

Deglobalization and Uncorrelated Portfolio (A Half-Baked Idea)

One half-baked idea that has occupied a lot of my mental space last quarter (and continues to) is in what ways will deglobalization influence portfolio construction.

Deglobalization is a macro-trend that is here to stay for the rest of this decade, if not longer. It is also becoming a hot topic in the zeitgeist. I might’ve contributed to it in some way with my own writing on semiconductor friendshoring.

With deglobalization comes two subtrends: redundancy building and market defragmentation. More “wheels” will need to be recreated to satisfy the geopolitical desires of deglobalization. These recreated wheels will also have access to certain markets that are not purely competitive, because other similar wheels (sometimes better wheels) aren’t allowed to enter these markets because they are made by geopolitically undesirable creators. More interchangeable products will have their own, not-so competitive markets to swim in – almost in a parallel universe.

Theoretically, you can then construct a portfolio of companies that offer similar products but serve different geopolitical needs, thus they will have less correlation with each other thanks to deglobalization. It’s not hard to see how such a portfolio would be attractive from a hedging perspective.

This decrease in correlation should show up in a stock’s beta. In the US-China technology deglobalization context, there are signs of this trend showing up. Alibaba’s two-year beta is 0.90, one-year beta is 0.46. JD’s two-year beta is 0.68, one-year beta is: 0.01. Pinduoduo’s two-year beta is 0.69, one-year beta is: -0.01. If more negative betas start showing up among US-listed China tech companies, you can construct a portfolio of comparable American and Chinese tech stocks in very interesting ways...theoretically.

Like I said, this is very much a half-baked idea. And I welcome your thoughts, feedback, and rebuttal of this potentially foolish thought.

Help! Help!

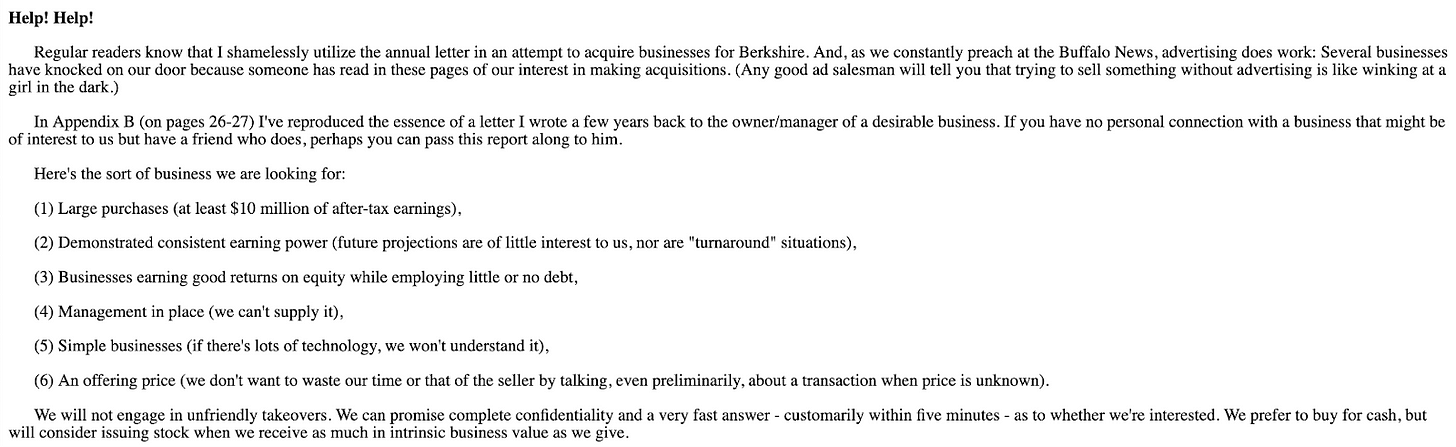

One of the “superpowers” of Buffett’s success is his ability as a consummate but tasteful marketer, using his annual letters as a vehicle to advertise Berkshire in order to acquire more businesses. He was a pioneer in the “newsletter as a distribution channel” tactic, long before any of us. Here is a screenshot from his 1990 annual letter:

In a naked act of mimicry of the Berkshire annual letter “advertisements”, I’m once again including a “Help! Help!” section to wrap up this quarterly update, as I did in my 2022 annual letter. I’m looking for help connecting with and learning from family offices that are ideally:

- Managing $100 million or more in assets (can be a single family or multi-family office)

- Regularly evaluate and hire outside managers to manage capital

- Ideally located outside the US (or have non-US perspectives, as these are the views I’m more curious about and have more blindspots in)

During 2022, I got to know a few family offices who reached out to me because of my writing. I learned a great deal about how they operate, what they care about, and how they see the world. It was a set of fresh perspectives I did not have before, and I would like to scale that learning more this year. If you have connections to this type of family office (or are part of one yourself), I would be grateful for an introduction to have a 45-minute to 1-hour Zoom call to get to know each other. I don’t have anything to sell, except my curiosity. I will have many prepared questions to ask, and I’m also happy to share my unvarnished points of view on deglobalization, investing, or any industry topic that resides within my circle of competence.

Thank you for reading and look forward to sharing my Q2 performance update and psychological learning in due time.