Cloud computing is hot. All cloud stocks are hot. Cloud was already growing everywhere and now accelerated by COVID, with massive adoption trends like remote work, e-commerce, digital health, and who knows what else. What used to be an outlandish approach to enterprise IT consumption is now becoming more mainstream. The TAM (total addressable market) is as big and far as the eyes can see.

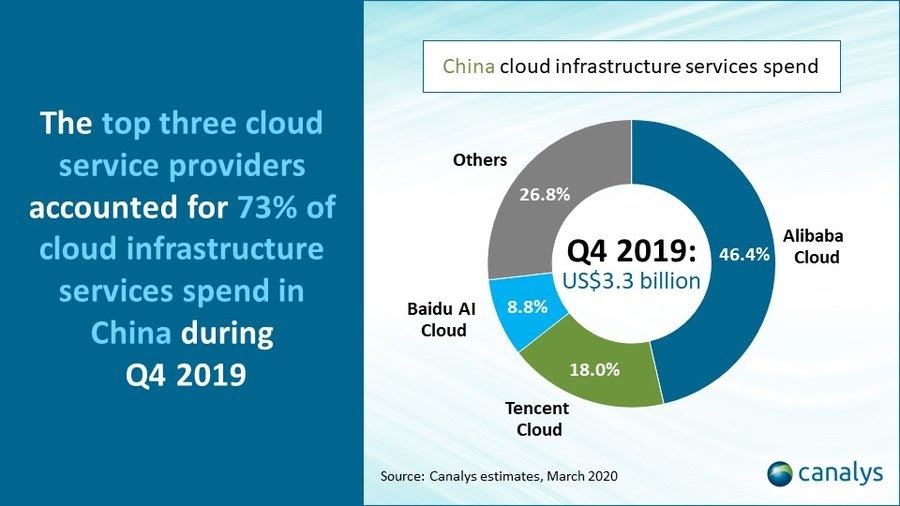

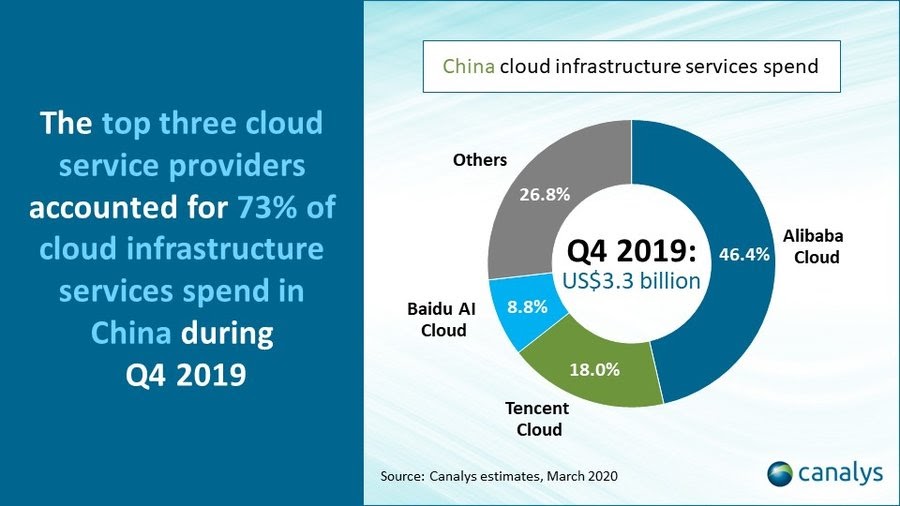

China’s own domestic cloud market is also growing rapidly. According to the research firm Canalys, China’s cloud infrastructure spending grew by 66.9% in Q4 of 2019 and by 63.7% for the entire year to exceed $10.7 billion USD, making it the second-largest cloud market in the world.

So will cloud in China just grow and grow with no end in sight, like the rest of the world?

As it turns out, there are a few factors that could put a lower ceiling on this market, especially public cloud adoption. One part of that ceiling is regulatory, thus artificial. Other parts -- namely labor cost and product maturity -- may sort themselves out eventually by natural market competition, but will take many years to play out.

Regulatory Limitations

At the moment, no banks can run their core workload on a public cloud platform in China. Similarly, no securities exchange type workloads, e.g. a stock trading platform, are allowed either. Thus, a Robinhood on AWS situation would not be currently possible. The banks are regulated by the China Banking Regulatory Commission, while securities are regulated by the China Securities Regulatory Commission.

To my knowledge, the regulation as it stands today does not contain explicit rules against public clouds, but has a series of requirements that public clouds currently don’t meet. In order for core banking or securities workloads to get on the “cloud train”, either the vendors will have to make changes to their solutions or the regulators will have to update their rules. Most of these rules were enshrined before the public cloud was a thing.

This regulatory limitation presents two market hurdles. One is obvious: without banks being allowed to fully adopt the cloud, the whole market’s growth has a ceiling. Banks, and financial services in general, tend to spend a lot of money on technology.

The other is more subtle, but has a larger long-term implication: it’ll slow down Chinese domestic cloud players’ pace of product evolution to meet the stringent technical requirements of core banking or securities exchange workloads. This implication may impact the domestic cloud leaders -- Alibaba, Tencent, Baidu, Huawei, JD, etc. -- and their competitiveness vis-a-vis their American counterparts -- AWS, Azure, GCP, Oracle Cloud, IBM Cloud -- especially when fighting for businesses elsewhere. To be sure, Chinese tech giants have had plenty of experiences running financial products on a large scale, especially Alibaba’s AliPay and Tencent’s WeChat Pay, so the technical foundation is there. But operating another bank, and ideally multiple banks at the same time to benefit from the economy-of-scale of the public cloud, is quite another matter.

Running core banking workload (think of it as the transactions in your own bank account that must be kept in-sync and accurate at all times) is oftentimes the ultimate proof of strength and reliability of any IT infrastructure stack. That realm includes everything from hardware (processors and storage) to networking to multitudes of software services, e.g. databases, big data analytics tools, fraud detection models based on machine learning, etc. Sadly, it looks like Chinese public cloud providers won’t get the chance to prove themselves any time soon, nor make the big bucks while doing so.

Labor Cost

The conventional wisdom of China’s labor cost (and arbitrage opportunity) is that it’s still cheap, but getting more expensive. That’s generally true for tech talent as well, but there are important nuances to parse in order to understand the “ceiling effect” on the cloud market.

As I have written elsewhere, the competition for talent in high-end areas of technology -- distributed systems, large-scale infrastructure engineering, machine learning -- is fierce worldwide. Thus, the top of the talent pool in these areas command just as much compensation in China as they do in Silicon Valley; very little room for arbitrage is left unexploited. These types of talent are also who you’d need to build a robust, reliable, and performant public cloud.

With that said, other lower-end parts of the backend IT labor force are still materially cheaper in China, for example, database administrators, system administrators, network administrators, and DevOps. This isn’t to say their skills are inherently not valuable, but they aren’t currently rewarded in the market. Thus, when a large enterprise in China weighs the choice between using a cloud solution and hiring five more people to do the same work internally, hiring can still be a more attractive option. Even if the cloud solution is technically more performant and elegant, commanding more humans when the humans are cheap enough has its appeals, not to mention the ego-stroking that managers get from a larger headcount.

It’s difficult for me to precisely gauge how much cheaper these backend technical workers are. For front end developers and designers (another relatively lower skilled strata of the tech workforce), the ones in China tend to cost about one-third as their counterparts in Silicon Valley, controlling for skill and experience level. Since backend, infrastructure-level operations engineers tend to be higher on the value chain and more senior overall, I’d venture to say the salary gap is about one-half to two-thirds, which would be quite material.

A public cloud’s core value is to be a more cost-effective and flexible way to use IT resources and the people who operationalize them. The typical go-to-market pitch of any public cloud platform, or third-party solutions built on top of these platforms, is three-fold:

- Technology (our technology is better than what you can build internally, so you should rent ours versus build it yourself)

- Total Cost of Ownership (TCO or the total cost of resources, both hardware and software, you’d have to buy and maintain over time versus renting the same resources from a cloud)

- Labor Cost (the number of people you’d have to hire to build/maintain these services, say 2-3 experienced DevOps, versus outsourcing the same work to a cloud vendor.)

While the technology and TCO pitch still work and will fuel the cloud market growth in China to a certain level, the labor cost argument tends to fall flat, which puts a ceiling on more public cloud adoption.

Cloud-Native Product Maturity

This last limitation is a second-order effect that stems from both the regulatory and labor-related hurdles we just discussed.

With banking and securities customers being off limit, Chinese cloud vendors won’t have the chance to build cloud-native products for two of the most demanding use cases in the industry. With labor cost being materially lower, the same cloud vendors also won’t have the chance to design products for demanding users, because these users know if they don’t like the cloud solution, they can afford to throw bodies at the problem.

When these end users have both low expectations and low willingness to spend on cloud products, these products will be of less quality and less cloud-native, if only because the market they are serving doesn't need them to be. Consequently, the cloud ecosystem tolerates less quality products and produces less talented people with good product sense, which conditions the market to always expect less of these products, eroding their pace of evolution and pricing power -- a subtle downward cycle. If stuck in this cycle, Chinese public cloud providers will not only grow into a smaller domestic market than it could have been, they will also be less competitive globally.

Of course, this isn’t to say all the products in the US, the largest cloud market by far, are all that great. In his recent analysis “The Developer Experience Gap”, Stephen O’Grady of RedMonk, lamented the huge gap in developer experience that has yet to be solved, while developers toil in a growing but confusing technology market that seems to offer everything except an easy way to use all those things. As he noted:

The same market that offers developers any infrastructure primitive they could possibly want is simultaneously telling them that piecing them together is a developer’s problem.

The technology landscape today is a Scrooge McDuck-level embarrassment of riches.

Even (or especially?) the public cloud leader, AWS, is not doing a great job of offering top-notch, developer-friendly product experiences.

The data warehouse and analytics company, Snowflake, pushed the cloud hype to a whole new level with its eye-popping IPO. An important part of its success is due to its product experience being easy to use, deploy, scale, and pay for on a subscription basis -- the quintessentially cloud-native way of consuming technology. (The company’s fun billboards might’ve helped too.)

This cloud-first way of building data analytics products was anything but obvious, when Snowflake first started in 2012, during the much earlier days of public cloud adoption. With its glitzy IPO now behind us, China's tech sector is now searching for its own Snowflake. PingWest published an article recently on exactly this question, by talking to executives from PingCAP and Kyligence -- two startups with the best chance of becoming Snowflake. While the article explored the two companies’ early decision to build cloud-native products as evidence of that potential, another more important angle that was not discussed is their aggressive expansion into the more mature and demanding US cloud market, in order to hone their product maturity.

Despite both being relatively young, series C stage startups, PingCAP and Kyligence’s willingness to expose its offerings to American users and build them on American public cloud platforms, will do wonders to accelerate their products’ evolution and make them leaders in China. While the short-term revenue may not be meaningful (and the geopolitical headwind isn’t helping), the long-term benefit of expanding and serving customers’ with more demanding expectations is definitely worth the trouble.

Had they stayed comfortably within China to let that market guide their product development, their potential would have a lower ceiling just like China’s own cloud market. The same willingness to expand early beyond the domestic comfort zone will be necessary for younger Chinese startups, looking to compete and stand out in the global cloud ecosystem.

All in all, cloud computing in China will still grow rapidly, if only because the country is huge and the base is small, so wherever the ceiling is, it won’t be touched for the foreseeable future. But the ceiling may not be as high as you think, and China’s cloud market will evolve, as many things in China do, with its own “Chinese characteristics”.

Full disclosure: I’ve worked with both PingCAP and Kyligence in the past in a management and operator role. I don’t hold shares in either company.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

中国的云市场天花板

云计算很火,所有云端企业的股票都很火。云计算一直在全球各地快速发展,现在因为新冠的影响加速了发展,包括远程办公、电商、数字化医疗和其他我们可能还没有看到的大趋势。云过去是个看似荒谬的企业IT消费方式,现在却越来越主流。TAM(Total Addressable Market)看起来能有多大就有多大。

中国国内的云市场也在飞速增长。根据研究机构Canalys的数据,2019年第四季度中国云基础设施支出增长66.9%,全年增长63.7%,超过107亿美元,成为全球第二大云市场。

那国内的云市场会不会像世界其他地方一样一直增长,没有尽头呢?

有些因素很可能会降低这个市场的天花板,尤其在公有云应用这一块。一部分是监管制度造成的,所以是人为原因。其他的阻力 -- 即劳动力成本和产品成熟度 -- 可能最终会通过市场竞争来解决,但需要多年的演变。

监管限制

目前,在中国,没有任何银行可以用公有云运行其核心系统的负载。证券交易类的负载也不可以,比如股票交易平台。因此像Robinhood搭在AWS上的这种构架目前是不可行的。银行是由银监会监管,而证券业务则是由证监会监管。

据我所了解,目前的监管制度并没有直接限制公有云的规定,但有一系列的要求,公有云厂商目前无法满足。如果银行或证券的核心负载要搭上 "云列车",要么厂商得改变其解决方案去满足监管的要求,要么监管部门得更新自己的规则。这些规定大多是在公有云还没成气候之前制定的。

目前的监管限制带来了两个市场障碍,一个是显而易见的:如果不允许银行全面采用云,整个市场的增长就有了天花板。银行以及整个金融服务行业,往往在技术上花很多钱。

另一个障碍更微妙,但有更长远的影响:监管限制会放慢中国国内云厂商的产品迭代步伐,因为它们没有机会去满足银行与证券交易核心系统的严格技术要求。这会影响到国内云计算的领军企业 -- 阿里、腾讯、百度、华为、JD等 -- 与它们的美国同行 -- AWS、Azure、GCP、Oracle云、IBM云 -- 的竞争力,尤其是在其他国家抢生意的时候。值得一提的是,国内的科技巨头们已经有很多运营大规模金融产品的经验,尤其是阿里的支付宝和腾讯的微信支付,所以技术基础是有的。但运营另一家银行,而且最好是同时运营多家银行,以从公有云的规模经济中获益,则是另一回事。

运维管理银行核心负载(可以想像成我们自己银行账户中的各种必须始终保持同步和准确的交易)通常是一款IT基础设施堆栈的实力和可靠性的终极证明。这包括了硬件(处理器和存储)、网络和众多的软件服务,例如数据库、大数据分析、基于机器学习的欺诈检测模型等。遗憾的是,中国的公有云厂商似乎不会有机会在短时间内在这方面证明自己的实力,也没法在证明的同时赚大钱。

人力成本

关于中国劳动力成本(和套利机遇)的主流思维是,整体劳动力仍然便宜,但越来越贵。对于技术人才来说,总体也是如此,但要理解它对云市场的 "天花板效应",还需要解析一些重要的差别。

正如我以前所写到的,在高端技术领域里,比如分布式系统、大规模基础设施工程、机器学习等的人才竞争在全球都非常激烈。因此,这些领域的顶尖人才不管在中国还是在硅谷,薪酬都差不多高,已经没有什么可以套利的空间了。这种人才也是一个想构建强大、可靠、高性能的公有云的公司所需要的。

话虽如此,但某些较低端的后端IT劳动力在中国还是比较便宜的,比如数据库管理员、系统管理员、网络管理员和DevOps。这并不是说他们的技能本身不值钱,但目前的劳动市场还没有奖励这种人才。因此,当某家国内大企业在选择“上云”还是再雇5个人自己干的情况下,雇人仍然是个更普遍的选择。即使云的解决方案在技术上性能更好,设计更优雅,在人力足够便宜的情况下,“砸人”还是有它的吸引力的,更不用说经理们能从团队人头增长中获得的“权力炫耀”了。

我很难准确估算这些后端技术人员的便宜程度。对于前端开发和设计人员来说(在科技劳动力中另一个技术含量相对较低的阶层),在控制技能和经验水平的情况下,中国劳动力的成本差不多是硅谷同行的三分之一。由于后端以及基础架构的运营工程师往往在价值链上处于相对较高的位置,总体经验也比较多,我觉得工资差距与硅谷比大约在二分之一到三分之二的范围。这个差距还是相当可观的。

公有云的核心价值就是以更低的成本,更灵活的方式运用IT资源和相关人员。所有公有云,以及搭建在公有云上的第三方解决方案,其经典的市场宣传都包括这三个方面:

- 技术(云的技术比企业内部的更好,所以应该租用云技术,而不要自己“造轮子”)

- 总拥有成本(Total Cost of Ownership, TCO或资源的总成本,包括硬件和软件;公司必须自己购买和长期维护这些东西,不如就从云端租用相同的资源)

- 人力成本 (公司需要雇人去构建及维护某些服务,比如要添加2-3个有经验的DevOps,不如把同样的工作外包给云厂商。)

虽然技术和TCO这两个角度仍然有效,也会在一定程度上一直推动中国云市场的增长,但人力成本这个说法往往会落空,也就给公有云的应用加了个天花板。

云原生产品的成熟度

这最后一个限制是个二阶效应,源于我们刚刚讨论到的监管和人力成本障碍。

在无法拿下银行和证券客户的情况下,国内的云厂商将没有机会为行业中两个最苛刻的用例打造云原生产品。在人力成本较低的情况下,同样的云厂商也不会有机会为高要求的用户设计产品,因为这些用户知道,如果不喜欢云,“砸人”解决问题就可以了。

在终端用户对云产品的期望值和消费意愿都比较低的状况下,相应产品的质量就会降低,云原生性也会降低,原因就是它们所服务的市场不需要那么好的产品。因此,整个国内云生态对低质量产品的容忍度更高,能培养出具有良好产品意识的人才也会更少,这就决定了市场对云产品的期望值总是会偏低,侵蚀了云厂商整体进化的速度和定价能力 -- 这是个微妙的下行循环。如果陷入这种循环,公有云厂商不仅会成长在一个更小的国内市场中,而且在全球的竞争力也会下降。

当然,这并不是说在美国这个目前最大的云市场里,所有的产品都那么优秀。RedMonk的Stephen O'Grady在最近的一篇分析《开发者体验差距》中,感叹开发者体验的巨大差距尚未解决,而开发者在一个不断变大但又混乱的技术市场中苦苦挣扎,似乎什么解决方案都有,就是没有一个简单应用这些方案的方法。正如他所指出的:

一个为开发者提供了他们可能想象和想要的任何基础架构方案的市场,也同时在告诉他们,将各种技术拼凑起来的挑战是开发者自己的事儿。

今天的技术格局是一个Scrooge McDuck级别的财富尴尬。

甚至(或尤其是?)公有云的领头羊,AWS,在提供顶级的、开发者友好的产品体验方面都做得不好。

大数据仓库和分析公司Snowflake以其令人瞠目结舌的IPO将云的“热度”推向了一个全新的高度,其成功背后的一个重要原因就是它产品体验的易用,包括部署、扩容和以订阅为方式的付费制度。这是典型的云原生产品的消费方式。(当然,该公司搞笑的广告牌可能也有帮助。)

在2012年Snowflake刚起步时,那还是公有云被接受的早期阶段,没有达到行业共识,当时“以云为先”的这种数据分析产品构建方式风险很大。随着其闪亮的IPO变成往事,国内科技界正在寻找中国自己的Snowflake。品玩最近发表了一篇文章,就是针对这个问题,采访了PingCAP和Kyligence,两家最有可能成为Snowflake的创业公司的高管。文章探讨到这两家公司很早就决定打造云原生产品,以此来证明它们的潜力,但另一个更重要的角度却被忽略了,那就是它们积极往更成熟、要求更高的美国云市场扩张,以打磨自己的产品成熟度。

尽管都是相对年轻的C轮阶段公司,但PingCAP和Kyligence愿意将产品暴露给美国用户,并将其搭建在美国的公有云平台上,这将加速其产品的迭代,也会使其成为中国市场的领先者。虽然短期收入可能不会太多(中美关系的逆风也不帮忙),但拓展和服务于有更高要求的客户的长期利益绝对是值得的。

如果这两家公司安稳地呆在中国,让国内市场来引导它们的产品开发,公司的潜力就会像中国自己的云市场一样,有一个较低的天花板。对于更年轻的一批国内创业公司来说,同样需要早期走出国内的“舒适环境”,有去海外扩张的意愿,要不然在全球云行业的生态中很难脱颖而出。

总而言之,中国的云计算市场仍将会快速发展,即使只是因为国家大,基数小。无论天花板在哪里,在可预见的未来都不会触到,但这个天花板可能没有大家想象的那么高。中国的云市场也会像中国的许多其他东西一样,以有"中国特色"的方式去发展。

声明:我曾与这两家公司合作过,担任其管理及运维的角色。我不持这两家公司的股份。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,和我交流互动!