NVIDIA notched yet another record this week. This time it is its single day 9.5% drop on September 3 that amounted to a $278.9 billion evaporation in market cap – the equivalent of more than three Intel’s.

It is probably not the kind of record you want to tell your grandma about. And adding more salt to its wound, Bloomberg broke the news that the Department of Justice issued a subpoena to the company in an escalation of the agency’s antitrust investigation – a subpoena which NVIDIA has since denied. This probe presents a massive overhang that no doubt contributed to NVIDIA’s single day rout and potentially continued weakness in the coming weeks. In these moments of legal uncertainty and regulatory volatility, it is helpful to find legal precedents or prior arts to put the risk in context. Lucky for NVIDIA, we do have some examples to examine. They are not in the United States, but across the Pacific pond in China.

The core thread of the DOJ's investigation is that NVIDIA is allegedly making customers harder to switch to other vendors and punishes those who don’t use its products exclusively. Well, sounds like a case of “pick one from two” (aka 二选一) to me!

The anti-competitive practice of “pick one from two” was outlined by China’s State Administration for Market Regulations (SAMR) in late 2020 that led to a series of lawsuits and investigations into large tech platforms like Alibaba and Meituan that ultimately resulted in multi-billion dollar fines. It was the beginning of Alibaba being thrown into the “regulatory doghouse” for more than three years, which it didn’t get out of until last Friday.

A thorough understanding of what is “pick one from two” and how it got resolved in China holds useful clues. If you are holding a big “NVIDIA bag”, it may put you more at ease.

What is “Pick One From Two”?

The story of “pick one from two” is essentially mega tech players trying to achieve some “platform lock-in” against competitors, albeit with some Chinese characteristics.

Prior to the 2020 SAMR investigations, Alibaba, the then dominant but threatened e-commerce juggernaut, forced online merchants to sell their products only on Taobao or Tmall and not on competing platforms, like JD.com. Alibaba induced this exclusivity with both carrots – discounted commissions, extra subsidies, more search traffic – and sticks – hiding storefronts, lowering traffic, downgrading search placement. JD.com wasn’t happy, of course, so it sued Alibaba and complained to the regulators. Meanwhile, Meituan, the restaurant review turned food delivery turned all things online to offline services platform, was doing the same thing to Ele.me, a similar service that was/is owned by Alibaba. (Interestingly, Alibaba was both a perpetrator and victim of “pick one from two.”)

How China’s SAMR went about describing and tackling this anti-competitive practice broke some new ground in the world of antitrust regulation in the Internet age. The level of dominance by “big tech” in both the US and China only came about in the 2010s, when the platform shift to mobile went from new and cool to de facto. To fight for the ever-shorter attention span of consumers and the limited real estate on their smartphones, sellers of goods and services have less bargaining power and need to obey the rules set by the biggest tech platforms, who control access to these consumers, in order to survive.

However, the antitrust framework in the US was/is still rooted in the Sherman Antitrust Act of 1890, when the target was Big Oil and the victims were the everyday consumers. But in the mobile Internet era, consumers were benefiting handsomely from better deals and more convenience, so the “Sherman framework” was woefully outdated. SAMR was the first regulatory body that I’m aware of that codified the dynamics of a “platform economy” (平台经济), described in grueling details the various adverse incentives and shenanigans, and did something about it.

Now that we are upon yet another platform shift called generative AI, sub out “platform lock-in” with “GPU lock-in”, sub out Alibaba for NVIDIA, sub out JD.com for AMD, and you have a legit antitrust case. (I would add Intel into this equation too, if only it’s worthy of even being discriminated against in a “pick one from two” scheme.)

Of course, e-commerce and online food delivery couldn’t be more different of an industry from GPU accelerators and cloud computing. But the competitive dynamic (or lack thereof) couldn't be more similar, where a single dominant vendor is capable of throwing its weight around to ensure future dominance. One notable difference is that, while the victims in China’s “choose one from two” case is mostly smaller merchants who couldn't’ afford to be forced into either Alibaba or JD.com, the NVIDIA customers who are complaining may be other mega tech companies like Microsoft, who is rumored to be NVIDIA’s single largest customer and is as well-versed in anti-competitive practices as any tech company in history.

If NVIDIA did in fact carry out its own version of “choose one from two”, how much will this hurt the AI juggernaut?

What Will Punishment Look Like?

The short answer is: not much, if what happened to Alibaba and Meituan were good indicators.

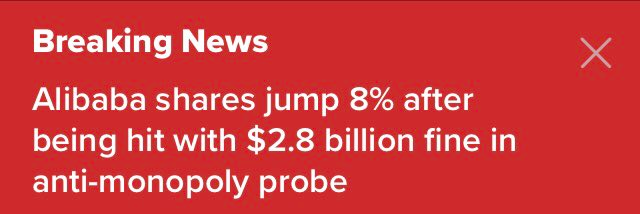

After both Alibaba and Meituan were found guilty, each were fined $2.8 billion and $533 million, respectively. While the raw numbers sound like a lot of money, the $2.8 billion amounted to 4% of Alibaba’s previous year revenue and the $533 million amounted to 3% of Meituan’s previous year revenue, when the fines were levied. A percentage of previous year’s revenue has been the standard in which antitrust fines of this type have been levied in not just China, but Europe and the United States as well. So far, none of the antitrust fines have exceeded 5%.

Hypothetically, if the DOJ finds NVIDIA guilty this year and applies this 5% “cap” as a worst case scenario, then 5% of NVIDIA’s 2023 revenue comes out to be about a $1.4 billion fine – less than what SAMR slapped on Alibaba three years ago! (Since NVIDIA is now making more revenue per quarter this year than it was doing for all of 2023, for the sake of the DOJ's reputation and America’s mounting debt, I would delay any guilty verdict and fine until next year.)

Furthermore, both Alibaba and Meituan’s stock prices jumped when their respective punishments were announced. After all, the market always rewards certainty, even if the cost is billions of dollars. So if you are worried about your “NVIDIA bag”, a guilty verdict is not a bad outcome. A lingering investigation is.

The 5% “cap” is an unwritten standard and by no means a black and white rule. And there is no indication that the United States DOJ would use what China’s SAMR has done on “choose one from two” as prior art (if it’s even aware of what “choose one from two” is at all). But it does exist and has referential value; there is no need to recreate the regulatory wheel from scratch. Regardless, as long as a monetary fine is how this probe gets resolved no matter the percentage or formula, this will be a slap on the wrist of the 800-pound AI gorilla.

The more worrying, long-term question of a potential guilty antitrust verdict is why would NVIDIA need to resolve to a “choose one from two” type scheme at all, if it is winning customers purely on the merit of its product? Perhaps its moat is not nearly as wide as the consensus hive mind believes.