When we introduced Interconnected 2.0 in October, one of the new elements was a monthly post sharing our observations on the market and any interesting investment research work we undertook in the previous month. Today’s post is the first installment of this kind, covering November 2023.

For readers unfamiliar with our investment operation, we run a long/short equity portfolio focused on the “picks and shovels” of the interconnected global digital AI economy. I draw on my technology business operator's experience and geopolitical antennae to bring an edge to how we assess a tech company’s rhythm and prospects. Internally, we like to say, “we can’t time the market, but we can time companies.”

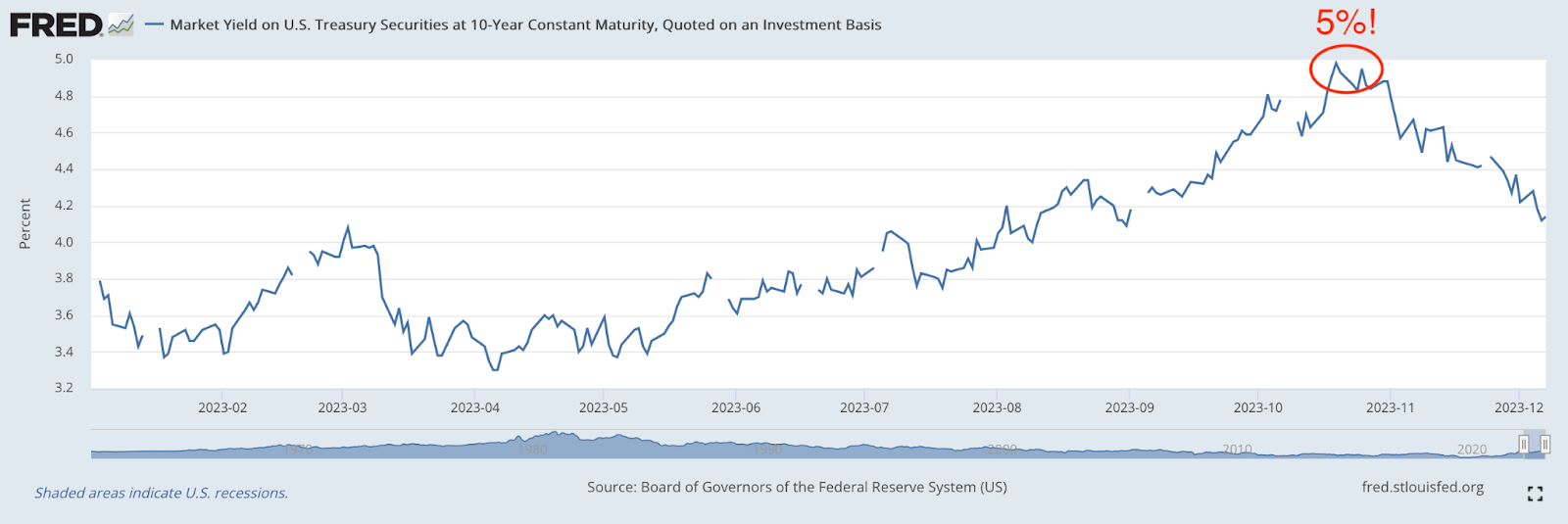

Timing the market is impossible. Timing a good entry point to a company is extremely hard or nearly impossible. What has made this exercise especially hard but also rewarding in November is how the confluence of the 10-year yield of US Treasury reaching 5% in October, the Federal Reserve’s subtle reaction to this financial condition, and how the interplay of these two factors affected share prices in the universe of companies we focus on, creating investment opportunities.

To be successful, an investor must combine knowledge of the micro – business fundamentals, company specific knowledge, and (especially in our case) technical and product expertise with the macro – interest rates, geopolitical movements, and signals from the Fed. We did a lot of this in November.

Micro Plus Macro

The last time the 10-year yield reached 5% was 16 years ago in 2007. The extended low interest rate environment since that point until early 2022 is now known, almost pejoratively, as ZIRP (zero interest rate policy).

The era of ZIRP happens to be when most of the companies we focus on were founded. A good shorthand of our investment universe or “circle of competence” is the Cloud Infrastructure Software Index that the venture firm, Redpoint, introduced earlier this year. This index includes about 70% of our current focus.

Rightly or wrongly, this index is quite sensitive to interest rates. And among the indexed companies, only seven were founded before 2007 (Atlassian, Palo Alto Networks, Dynatrace, UiPath, Tenable, Akamai, Jamf).

Thus, when the 10-year yield hit its 16-year high in October, all these companies started tanking, even ones that were already trading at very depressed multiples, i.e. between 2x to 3x EV (enterprise value) to NTM (next twelve months) sales. Just as quickly, the Fed’s FOMC (Federal Open Market Committee) meeting that took place on October 31 - November 1 paid a subtle but important nod to this rising yield in its press release with the phrase “Tighter financial and credit conditions for households and businesses…” (The same phrase from the September FOMC meeting press release did not have the word “financial” in it.)

This nod, along with probably the new liquidity that typically becomes available via mutual funds, which end their fiscal year in October and thus have additional cash to deploy starting in November, catapulted these companies’ share prices higher.

Our portfolio took advantage of the downswing in October followed by the upswing in November by putting more dollars in a couple of names we have already done a lot of fundamental analysis (or micro work) on. We would have invested more but, as a small fund, we are always capital constrained. Although the macro was what created the opportunities, going through October and November in real time was not easy and not for the faint of heart (or stomach). It was our deep understanding of the micro that allowed us to sleep soundly.

Macro analysis, for us, goes beyond just identifying price entry (or exit) opportunities. As the whole world exits ZIRP, thinking hard about how the cost of money and the price of time affect how much and how often companies spend their technology budget is critically important to the success or failure of the companies we closely track.

That's why, last month, we spent a lot of time studying Roblox.

The Roblox Story

To be clear, Roblox is not in our investment universe, and we normally don’t track it. However, Roblox is a big buyer, consumer, and “lighthouse” logo for other cloud infrastructure outfits, so what the company is doing on the infrastructure side matters a great deal.

Roblox came on our radar because Confluent, a company we do track closely, had one of its worst quarterly earnings reactions in November. The stock dropped more than 40% after releasing its Q3 earnings. A primary reason behind this reaction was two major customer churns. One was New Relic, which is being taken private by private equity and understandably reducing its software spending. The other, as we learned through the grapevines of our scuttlebutts in the industry, was Roblox.

So what is Roblox doing to its infrastructure? As it turns out, a lot!

The company has been undergoing a multi-year project to re-architect its entire cloud backend to be fully under its own control, and get rid of third party cloud providers and services. It has been building a new core data center in Ashburn, Virginia since at least Q2 2022 and has largely completed in Q3 2023. It has renegotiated a new, presumably much cheaper, 3-year deal with its main public cloud provider, likely AWS. It has hired top-notch infrastructure engineers from the likes of Apple – the kind of engineer who likes to recreate wheels and manage complex systems – to its ranks. Confluent became a victim of this undertaking.

Roblox chose to build, not buy. It spent $700 million on this infrastructure rebuild, according to its CFO. What resulted is its own “Roblox Cloud”, with two core data centers and more than 30 edge data centers around the world – something it was very proud to showcase during its Investor Day event in mid-November.

As most of the enterprise IT world still zigs towards adopting the public cloud to accelerate digital transformation, Roblox is zagging by opting to build and manage everything in house. The big question, especially for companies like Confluent, is this a start of a trend or an idiosyncratic event?

Based on our research so far, it appears to be idiosyncratic. That's good news for Confluent. And its stock price has indeed recovered some since that horrific 40+% drop. Roblox has a uniquely strong engineering culture that emanates from its founder and CEO, David Baszucki. Just listen to his podcast, which is full of nerdy technical topics like active-active data storage and Luau, a programming language. Roblox has the leadership will from the top and the reputation to attract technical talent to pull off building a private cloud in ways that few companies can. And by being able to manage its infrastructure cost in ways that predictably match its growth trajectory, Roblox can become sustainably profitable in ways few companies can.

Idiosyncrasies aside, what Roblox is doing does have larger implications.

One topic we have been wrestling with is how will an elevated interest rate environment impact how large and how quickly the budget allocated for AI investments will be spent in 2024. We touched on this with our learnings gleaned from Zoom and Snowflake’s recent earnings report. The preliminary conclusion is that CFOs of large enterprises will continue to judiciously manage the pace of money leaving their corporate treasury to take advantage of interest incomes on cash, which may mean AI software vendors will have to settle for shorter, more frequent payment terms, while managing their own coffers in the same way, assuming they are profitable and have healthy cash flow.

Roblox has serious AI ambitions and will spend big to realize those ambitions. However, very few of those dollars will flow to other software vendors, given its hardcore, “build not buy” culture. Its investment will go more into hiring talent, acquiring more data centers, and rolling up its own AI solutions using open source building blocks. If more enterprises emulate Roblox even partially, coupled with a tight budget purse due to high interest rate, the 2024 AI budget may not be as flush as many people are hoping for.

Of course, none of this may matter if the Fed plans to cut interest rates sooner rather than later. A trial balloon from the Wall Street Journal has already been floated to push out a “rate cut” narrative in advance of the FOMC meeting later this week, the last one of the year.

Although the consensus is that Chair Powell will hold the Fed Funds Rate unchanged, it will be his tone and narrative about next year that everyone will be watching and the market will be reacting to. It's folly to waste energy predicting the unpredictable. All we plan to do is keep building our knowledge on the micro, while keeping a watchful eye on the macro.