Huawei started a little-known corporate VC division in 2019 called Habo Investment. Since then, it has made 22 investments and five of them have either IPO’ed or are in the process of doing so on the Shanghai STAR market.

Although these IPO’s are not huge by market cap standards, from an investment-to-liquidity perspective, 5 out of 22 within two years is an incredibly high ratio. It would make Habo one of the best-performing VCs.

Habo’s very existence breaks Huawei’s own tradition. Its founder and CEO, Ren Zhengfei, has made it a rule to never do corporate venture investments, especially in current or potential partners, in order to maintain objectivity in choosing the best companies to work with.

So what has changed that gave birth to Habo and led to its success so far as an investment firm?

IPO Bonanza

The pace of Habo’s investments has been aggressive, and its fund size has ballooned quickly as well. It began as a 700 million RMB (~104 million USD) fund in April 2019, which increased to 1.4 billion RMB (~200 million USD) in January 2020, and increased again to 2.7 billion RMB (~400 million USD) in October 2020. Basically, its size almost quadrupled in less than two years.

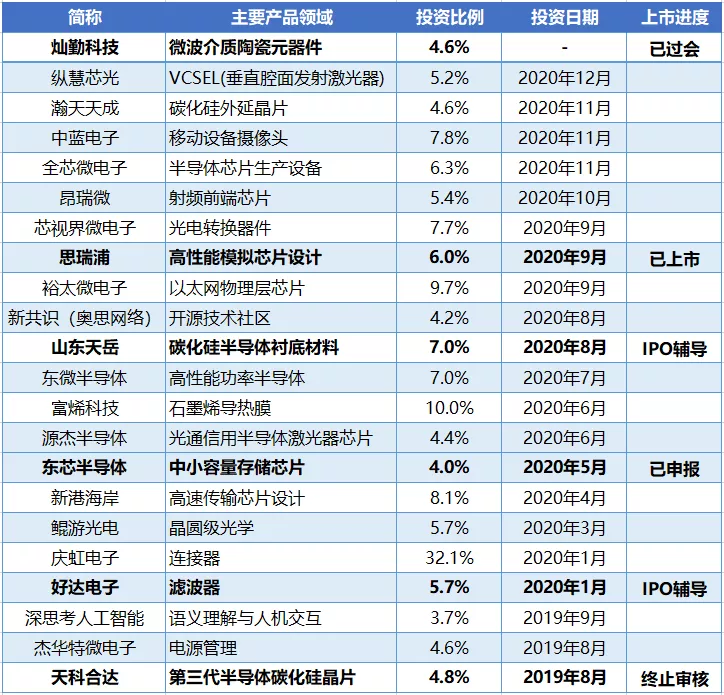

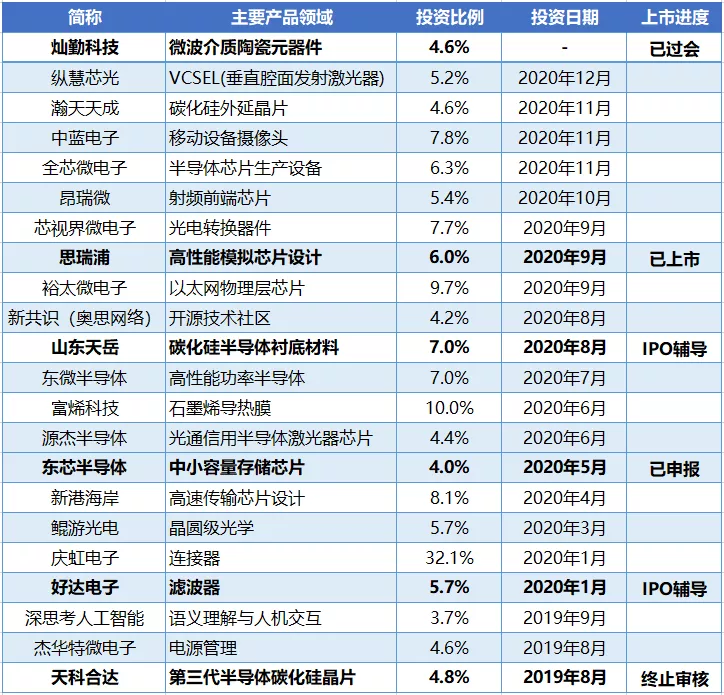

All things considered, Habo’s fund size is still a drop in the bucket for Huawei, whose cash and cash equivalents at the end of 2019 is a whopping 171 billion RMB (~25 billion USD). Here’s a table that lists Habo's current portfolio, plus where they are in the STAR Market’s IPO review process.

(For my non-Chinese readers, the 3rd column denotes the fund’s ownership percentage. The last column notes the stage where some of the companies are currently in to prepare for their Shanghai STAR market IPOs. The bolded companies are all in the IPO pipeline, except for the last one, which canceled its application.)

One notable Habo investment we’ve discussed before in “300 Years: Huawei's Open Source Strategy” and “Can You ‘Nationalize’ Open Source?” is OSChina, an open-source tech community organization and the parent organization of Gitee, China’s GitHub alternative.

There are two ingredients that make Habo-invested companies primed for public listings:

- A Habo investment and a stack of Huawei purchase orders typically come together

- Habo’s investment areas are strategically important sectors that are encouraged by the government to go public and grow

From Investor to Customer

There have already been a few examples where a Habo investment plus Huawei purchases revived companies that were struggling to survive.

One is C&Q (灿勤科技), a manufacturer of antenna filters -- a key component of 5G base stations. The company was founded in 2004 and its business was struggling until 2019, when its revenue increased 11-fold, almost all of which are from Huawei. C&Q has now finished its IPO review process and is poised to trade on the STAR market.

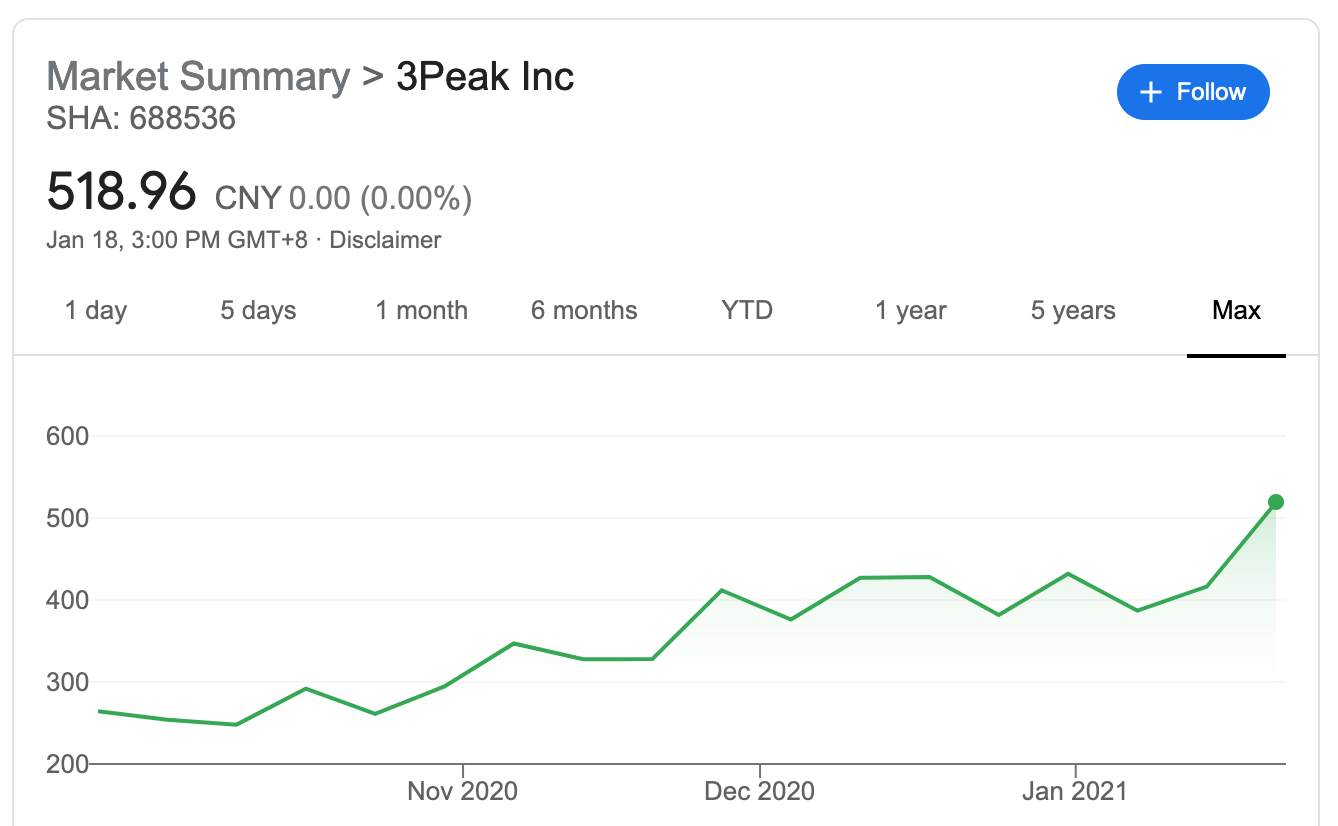

Another one is 3Peak (思瑞浦), which makes signal chain simulation chips -- another key component of 5G base stations. This company was on life support until its revenue grew 167% from 2018 to 2019 on the back of orders from Huawei and investment from Habo. It’s now listed on the STAR market; its share price has doubled since the IPO.

Thus, a Habo investment is a trifecta of:

- Fresh new capital

- Huawei’s business and vote of confidence

- Positive signal for more investment from both public and private markets

The last bullet point on “positive signal” deserves some explanation. Because Habo is a corporate venture division of a company that has plenty of cash, it does not need to make a quick return on capital and will hold shares for a long time. Thus, private market investors like VCs, who do need liquidity and look to bet on reliably growing businesses, like to ride Habo’s coattail. One recent example is VisionICs (芯视界微电子), which received an investment from Habo in September 2020 and was soon followed by another one from Sequoia China in December.

This “positive signal” carries over into the public market if the invested companies IPO, because Habo is a long-term shareholder and only invests in sectors that Huawei needs, which by extension are what China needs. Thus, the “Habo team” tends to align well with China’s overall development and planning objectives, making them good bets in the Chinese stock market, even though some of them effectively become single-customer companies, like C&Q.

With that in mind, let’s look at which areas Habo has been investing in.

Investment Areas

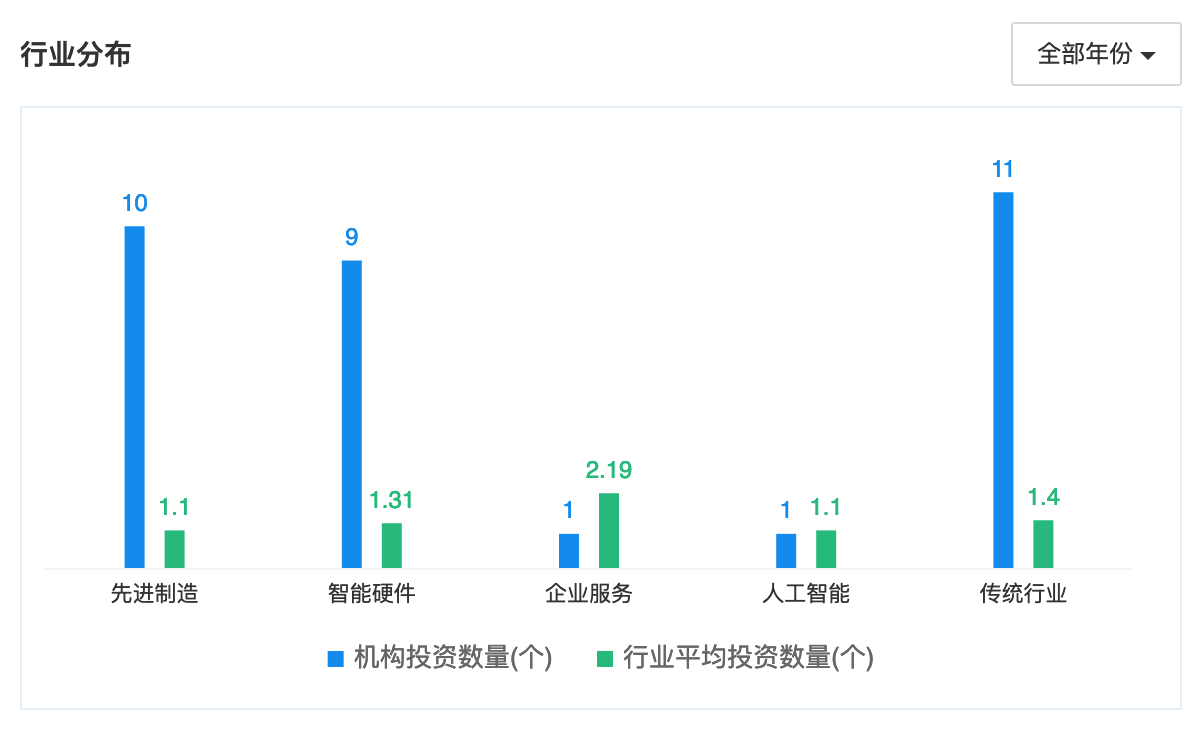

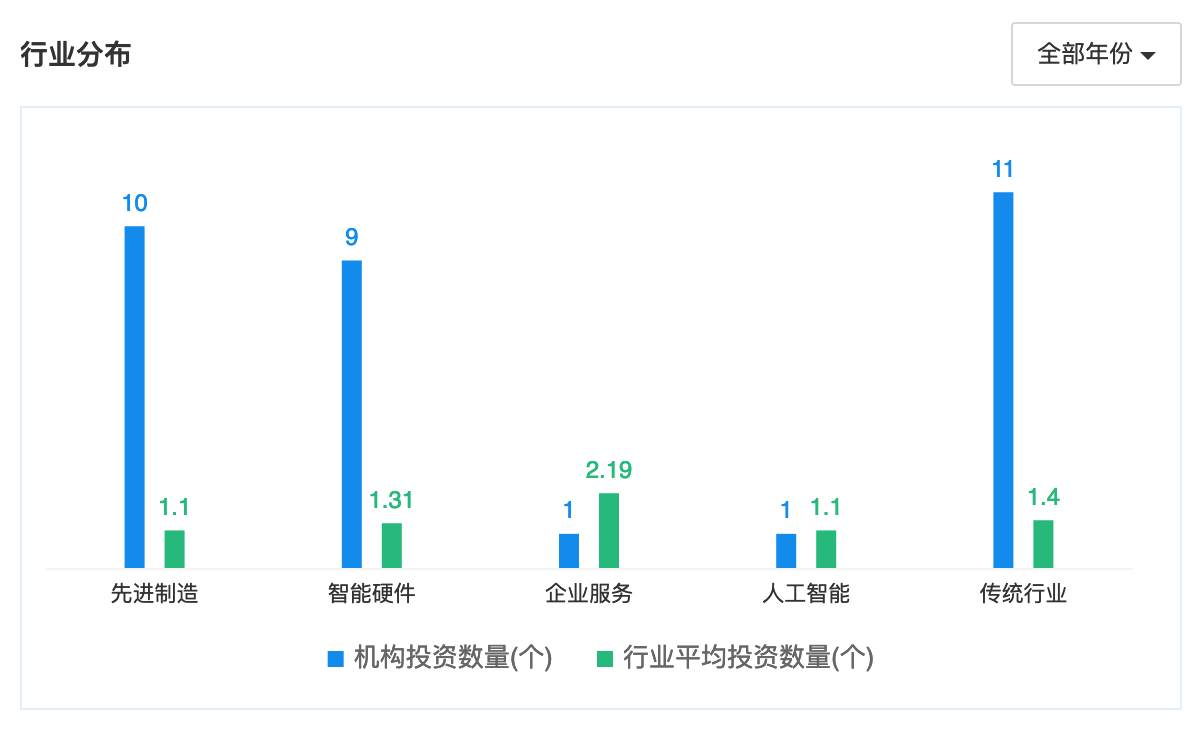

As the chart below provided by Qcc.com indicates, Habo’s five sectors of focus so far are advanced manufacturing, smart hardware, enterprise technology, artificial intelligence, and traditional industries, listed from left to right. It’s worth clarifying that the “traditional industries” category includes companies that do integrated-circuit design and semiconductor materials R&D, while “smart hardware” includes companies that actually develop, produce, and test semiconductors.

The blue bars indicate Habo’s investments. The green bars indicate the industry average number of investments in the same sector. (I assume the averaging is done per investment funds, but it’s not totally clear.)

What’s evident from this chart is that Habo doesn’t invest in necessarily the hottest areas in the market. (It would be unthinkable, even comical, for Habo to try betting on the next Pinduoduo, Kuaishou, or community group buying service.) Habo invests in what Huawei needs, which ends up being more hardcore tech that requires a longer time horizon to mature. The only sector where industry outpaces Habo is “enterprise technology”, because B2B SaaS is becoming trendy in China’s VC circle.

Breaking Tradition

So why did Huawei give birth to Habo against the principle laid out by its founder? It was a way to adapt to sanctions and geopolitical realities.

Ren Zhengfei’s “no partnership favoritism” rule worked well in a no-sanction world. Huawei sourced the best-of-class technology and suppliers from around the globe and gave no special treatment to domestic partners -- until it couldn’t anymore.

Habo is a way to find and invest in the best companies in China who can be suppliers and partners, and groom them to be world-class quality. That's why Huawei gives them its business -- there’s no better training than serving a real (and big) customer. Huawei would even send engineering teams to be embedded in some of these companies to help them “level up.”

In many ways, Habo’s investment performance as a fund is beside the point. Its purpose is another, less discussed way to speed up the journey to achieving technological self-reliance.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox (twice per week). Follow and interact with me on: Twitter, LinkedIn.

华为是家一线VC吗?

华为在2019年成立了一个鲜为人知的企业VC部门,叫哈勃投资。成立以后已经投了22家公司,其中有5个要不已经在上海科创板上市,要不正在审核过程中。

虽然从市值上来看,这些IPO的规模并不算大,但从投资到上市这个角度来看,哈勃应该算是一线VC了。两年内,22笔投资中5个上市,这个比例还是非常高的。

哈勃的存在也打破了华为自身的传统。任正非为了在选择最佳合作伙伴时能保持客观性,规定绝不做投资,尤其是对现有或潜在的合作伙伴。

那么,是什么变化催生了哈勃?它作为一家投资机构的成功又缘由何在呢?

上市狂欢

哈勃的投资步伐一直很激进,其基金规模也在迅速膨胀。从2019年4月开始是一个7亿人民币(约1.04亿美元)的基金,到2020年1月增加到14亿元人民币(约2亿美元),到2020年10月再次增加到27亿元人民币(约4亿美元)。在不到两年里,其规模几乎翻了四番。

综合来看,哈勃的基金规模对于华为来说只是个小case。截至2019年底,华为的现金和类似现金价物高达1710亿人民币(约250亿美元)。以下这张表格,列出了哈勃目前投的所有项目,以及它们在科创板IPO审核过程中的进度。

我们之前在《能把开源“国有化”吗?》和《300年:华为的开源战略》这两篇文章中讨论过一笔值得关注的哈勃投资,就是新共识(奥思网络),这是一个开源技术社区组织,也是GitHub在中国的替代品Gitee的母公司。

哈勃旗下的公司有两个要素可以加速它们的上市步伐:

- 哈勃的投资和华为的订单通常绑在一起

- 哈勃投资的领域是政府极其鼓励发展的重要战略行业

从投资到客户

目前已经有几个例子证明,哈勃的投资加上华为的订单会让一些垂死挣扎的公司重获新生。

其中一个是灿勤科技,一家介质波导滤波器制造商,产品是5G基站的关键部件之一。该公司成立于2004年,其业务成绩一直很平凡,直到2019年,突然收入涨了11倍,几乎全部来自华为。目前,灿勤已经完成了IPO审核过程,准备在科创板上开始交易。

另一家是思瑞浦,它生产信号链模拟芯片,也是5G基站的另一个关键部件。这家公司在2018年至2019年的营收增长167%之前,也一直处在挣扎状态。因为有了华为的订单和哈勃的投资,它现在已经在科创板上市了。自IPO以来,股价也已经翻了一番。

因此,一笔哈博的投资其实是个“三部曲”:

- 注入新资本

- 拿到华为的订单和信任

- 给公私募市场两方投资机构发出正面信号

"正面信号" 这一点可能需要更细致的解释。因为哈勃是家现金充足的企业战略投资部门,不需要短期的资本回报,而会长期持股,所以像类似风投这样的私募市场投资人,喜欢搭“哈勃火箭” —— 既有可靠的增长(华为订单)又有可盼的资本流动和回报(上市)。最近的一个例子是芯视界微电子,该公司在2020年9月获得了哈勃的投资,很快在12月就获得了红杉中国的投资。

这种 "正面信号" 也能延续到公募市场,是因为哈勃作为一家长期股东,只投资华为需要的领域,也就是国家需要的领域。哈勃的公司往往与中国的整体发展和规划目标保持一致,所以在中国股市里押“哈勃队”是不错的选择,尽管有些公司基本上只给一家客户(华为)服务,比如灿勤。

考虑到这一点,我们来看看哈勃到底在投哪些领域。

投资领域

如企查查提供的数据图(下)所示,到目前为止,哈勃的五大行业重点分别是:先进制造、智能硬件、企业服务、人工智能和传统产业。值得说明的是,"传统产业" 里包括做集成电路设计和半导体材料研发的公司,而 "智能硬件" 则包括研发、生产半导体,以及做测试的公司。

蓝色统计条代表哈勃的投资,绿色统计条代表同行业里的平均投资数量(我默认这是按投资基金做出的平均数,但统计表并没有明确地说明)。

从这张图里可以看到,哈勃投的不一定是市场上最火的领域(如果哈勃押下一个拼多多、快手、或社区团购服务,那也是挺荒谬滑稽的)。哈勃只投华为需要的东西,所以基本都是很硬核的技术,需要长时间的成熟过程。唯一一个行业平均量超过哈勃的领域就是 "企业服务",因为B2B SaaS最近在中国的创投圈里很火。

打破传统

那么华为为什么要打破其创始人制定的原则和传统,允许哈勃的诞生呢?因为这是不得不适应制裁和国际关系新现状的被迫手法。

任正非之前设定的“不投供应商”原则,在没有制裁的大环境下效果很好。华为从全球各地采购最好的技术,与最好供应商合作,对国内的供应商不给予特殊待遇。但是,现在这种做法行不通了。

在当下,哈勃就是要找到并投资于中国企业,让它们成为供应商和合作伙伴,培养它们达到世界级的品质。这也是为什么华为给它们订单的原因 —— 没有什么历练比服务真正的(大)客户效果更好的了。华为甚至会派自己的工程团队,嵌入自己投资了的公司,以帮它们提高水平和质量。

所以从宏观角度来看,讨论哈勃的投资业绩其实有点跑题。它的真正目的是以一种鲜有人讨论的方式,来加快华为以及国家实现技术自立的步伐。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周两次,新的文章将会直接送达您的邮箱。请在Twitter、LinkedIn上给个follow,和我交流互动!