Will “AI in a box” become a thing? Huawei Cloud is certainly trying to make it so.

By packaging GPUs, networking, server racks, other hardware, and AI models all together, Huawei Cloud is pushing the adoption of AI infrastructure by putting everything an enterprise or government agency could possibly need to build its own AI in its own private cloud environment.

This is a notable departure from Huawei’s other peers in the China cloud landscape – Alibaba, Baidu, Tencent – as well as its American cloud counterparts – AWS, Azure, Google Cloud Platform – all of which are favoring AI adoption via their respective public cloud. Huawei’s on-prem, private cloud AI strategy may seem strange relative to the rest of the market, but there are good reasons to believe that this approach has its business logic, is playing to Huawei’s historical strengths, and may even be ahead of the curve in where the global AI adoption trend is going, not just in China.

As Jensen Huang said a couple of days ago at the Dell World Conference, “On-prem is cool again.”

Huawei Cloud: First Mover, Late Bloomer

To understand the merits of Huawei’s “AI in a box” approach, it is worth taking a brief history tour of where Huawei Cloud came from.

Huawei began as a networking hardware company, competing with the likes of Cisco. Its cloud division was actually formed very early, in 2005. For context, AWS launched in 2006 with S3 and EC2. In a sense, you could say Huawei Cloud was born before AWS and was the first cloud in China.

As its hardware business grew and its products were installed in server rooms and data centers in China and elsewhere, Huawei probably saw early that “the cloud” (or renting out hardware at scale) could be a thing. However, this was also during a time when Huawei started its consumer electronics division, chip design division (HiSilicon), and other offshoots, all to expand beyond its core business. Huawei Cloud was just one of its many options to find future growth. During the mid-2000s, when the tech industry globally was still reeling from the pains of the bursted bubble a few years ago, cloud computing in China was seen as either a fleeting fad or a distant reality. So, likely suffering from a combo case of the Innovator's Dilemma and groupthink, Huawei Cloud was under-invested, not prioritized, and went nowhere for the next 10 years.

The only Chinese tech company that took cloud computing seriously and invested heavily was Alibaba. As the Chinese Internet sector raced ahead during its go-go decade of the 2010s, so did Alibaba Cloud, which for a period had a bigger market share than all of its domestic competitors combined. And many competitors did enter the fray, from cloud divisions of large tech firms like Tencent, Baidu, and Kingsoft, to new independent upstarts, like UCloud, Qiniu, DaoCloud, and CaiCloud (later acquired by ByteDance to form its own cloud division). Yet, Huawei Cloud remained on the sideline, unwilling to deviate too far from its core hardware competency into the unknown of cloud software, until 2017, when “moving to the cloud” was no longer a fad and more a consensus.

In March 2017, Huawei Cloud officially became a top-level business unit, not just another division. An executive vowed to take over Alibaba Cloud’s market share and become a top 5 global cloud provider in three years. The way Huawei Cloud went about achieving this lofty goal initially was off the mark, pulled down by its DNA, and foreshadowed what it is doing today with AI. One of its first growth initiatives was going after governments, specifically selling a private cloud solution to 660 city governments in China – a classically on-prem, “all in a box” offering for every single city. While this strategy fit within Huawei’s comfort zone as a hardware and services seller, it went against the grain of where China’s tech environment was heading, when the country’s public cloud segment was growing 2-3x faster than private cloud. Huawei Cloud was behind the curve.

The setback was painful and instructive for Huawei Cloud, which had to quickly transition from focusing on hardware and private cloud to software and public cloud. Through investments in containers, open source software, and distributed database solutions, like GaussDB (databases and data warehouses were, and still are, the big moneymaker for cloud platforms), Huawei Cloud began to make a dent.

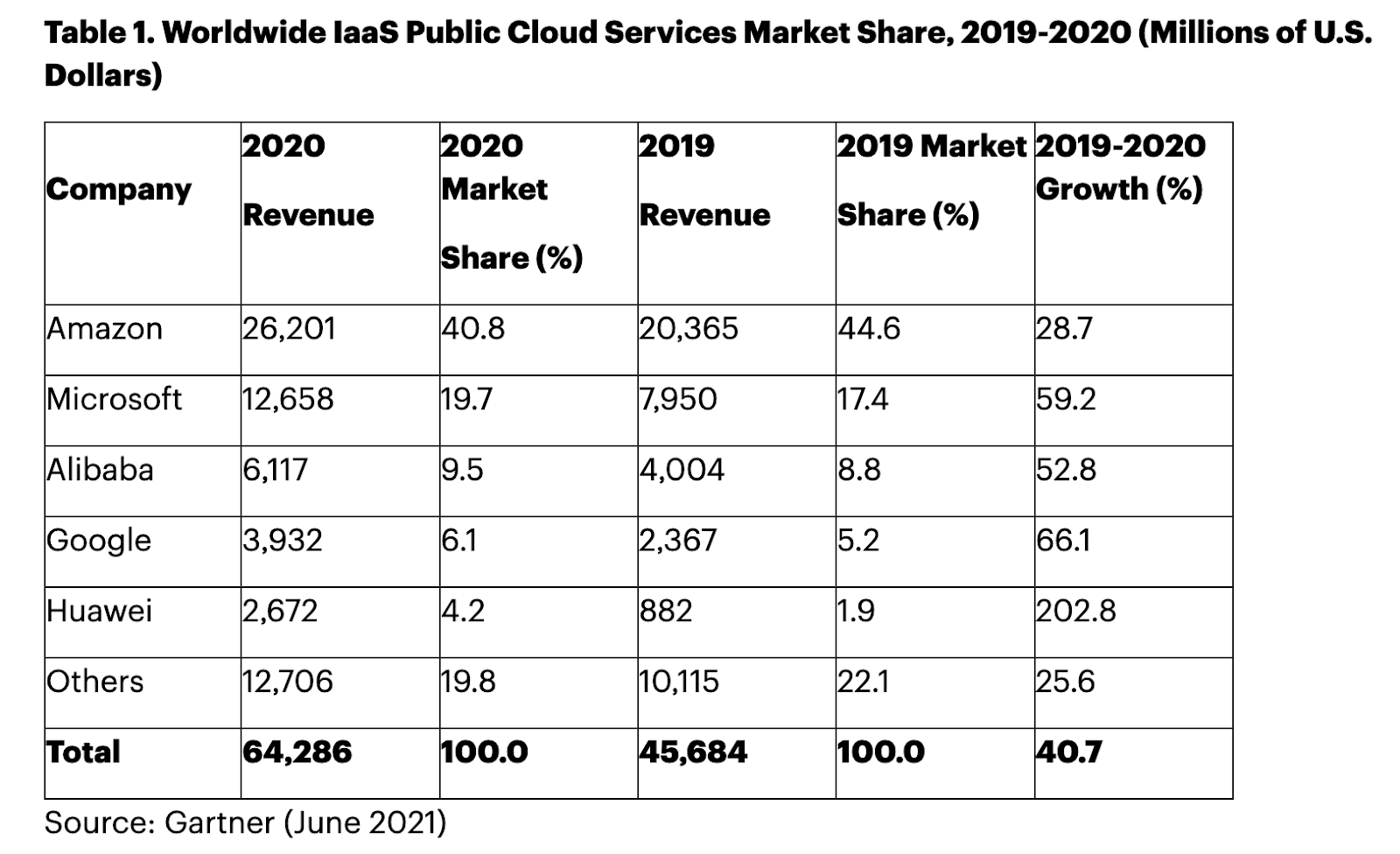

By 2020, according to industry analyst firm Gartner, Huawei Cloud became the fifth largest cloud provider globally in revenue and market share (at least at the infrastructure-as-a-service layer) replacing Tencent Cloud. It has held that number 5 position ever since – achieving and maintaining one of the two goals it set out to accomplish in 2017.

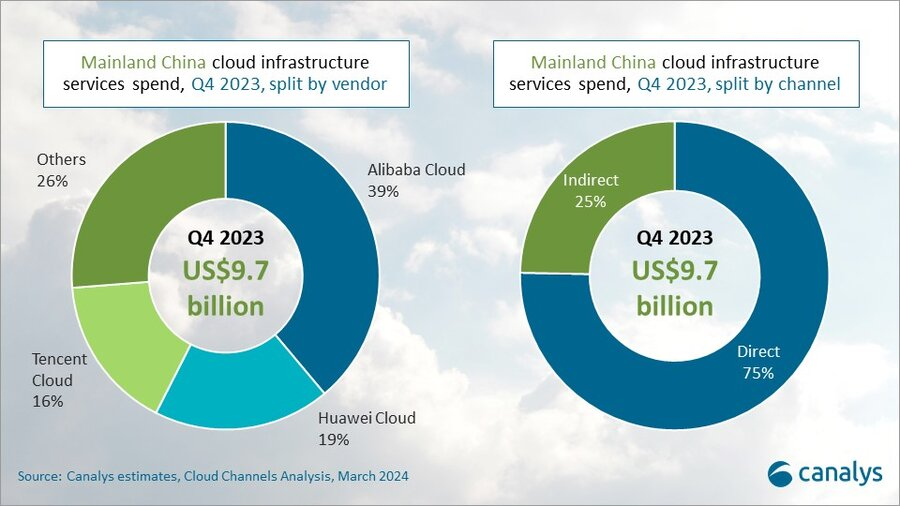

Domestically, however, it is still catching up to Alibaba Cloud, but has decidedly established itself as the #2 player. Based on the latest report from Canalys (another industry research firm), as of Q4 2023, Alibaba Cloud’s market share is 39%, Huawei Cloud’s is 19%, Tencent Cloud is 16%, with the rest of the 26% being divvied up by other cloud platforms.

Huawei Cloud is a rare example of being a first mover, but a late bloomer.

As Alibaba Cloud struggles to grow even at single-digit percentages, Huawei Cloud’s 2023 annual growth rate clocked in at 21.9%, making it the company’s 3rd largest revenue driver after “ICT Infrastructure” (aka core networking products) and “Consumer” (aka smartphones, laptops, etc.). For context, in 2023, AWS grew at 13%, Azure at 30%, GCP at 26%, and Alibaba Cloud at 4%.

Interestingly, Alibaba has vowed to return its cloud unit to double-digit growth primarily by abandoning most of its private cloud projects, which it deems costly and low-margin, and focus solely on the public cloud – its bread and butter (or porridge and pickled veggie?). Meanwhile, Huawei Cloud’s natural strengths in (and preference for) on-prem, private cloud never left its bloodstream.

“On-Prem Is Cool Again”

In comes generative AI, which every cloud platform is banking on to re-accelerate growth, after a massive industry-wide slowdown following a period of unnatural hypergrowth during Covid.

The business logic between AI and cloud is simple enough. So much of AI depends on training, fine-tuning, and drawing inferences from large (and increasingly small) models, all of which requires a lot of compute and networking resources to deploy, more AI must mean more cloud usage. However, there seems to be a subtle but profound shift in infrastructure preference from public cloud to private cloud. And this is not unique to either Huawei or China.

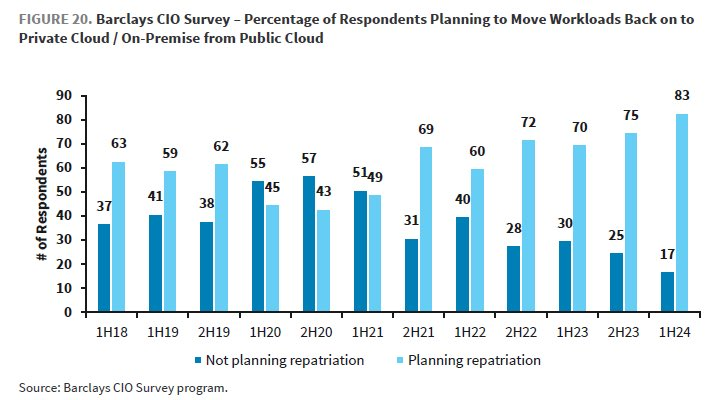

In April, Barclays released its regular survey of 100 CIOs (Chief Information Officers), where 83 of them said they plan to move workloads from public cloud back to on-prem, private cloud environments because of AI. This is a marked increase from the same survey conducted in the first half of 2022, before ChatGPT, where 60 CIOs said they plan to shift workloads from public to private.

This noticeable shift in cloud posture follows the fast realization that when it comes to generative AI, your company’s or department’s (or even country’s) data is more valuable than ever. It is no doubt reinforced by Jensen Huang, Michael Dell and others, who have been harping on the notion that data equals intelligence, so owning your data is the key to success in the AI era. Unsurprisingly, Nvidia, Dell, and other AI infrastructure builders are also well-incentivized and highly-compensated for making this narrative stick, because private cloud is in many ways a form of “overcapacity”, while public cloud is more about efficient use of resources and economies of scale. Sovereign AI is but another manifestation of this narrative.

Data as a valuable resource is not a new idea. Before AI, public cloud vendors spent years convincing large companies that it was safe to store their data elsewhere off their premises to reduce operational cost, make IT backends more efficient, while still being able to derive value from that data through various cloud big data tools (Snowflake, Databricks, Redshift, BigQuery, Fabric, to name just a few). But with AI, companies and governments are becoming more possessive of that data and less willing to trade off the operational efficiency of the public cloud against the risks of “leaking” its own “intelligence” in someone else’s data center. AI has made the inefficiency of private cloud worth it.

Private cloud as an important business vector is also not new for public clouds. To branch into the on-prem environment, AWS announced its private cloud offering, Outposts, five years ago. GCP announced its own spin on private cloud, called Anthos, a few months after AWS released Outposts. It will be interesting to see if these private offerings from public cloud platforms become more prominent as generative AI gets adopted more widely.

For Huawei, which will always be more adept at installing 5G base stations and building hardwares, this shift back to on-prem is both playing to its strengths and allowing it to be ahead of, rather than behind, the curve this time. Of course, there is a clear, geopolitical ring fence around western countries, where any Huawei solution is off limits. But that reality is irrelevant to simply understanding why “AI in a Box” may, in fact, be the right strategy and meeting the moment.

If Jensen is even half right about on-prem’s return to the cool kids table, then what Huawei Cloud is doing would be much more than just a clever packaging trick.