Most of the CHIPS Act subsidies have (finally) been (preliminarily) allocated.

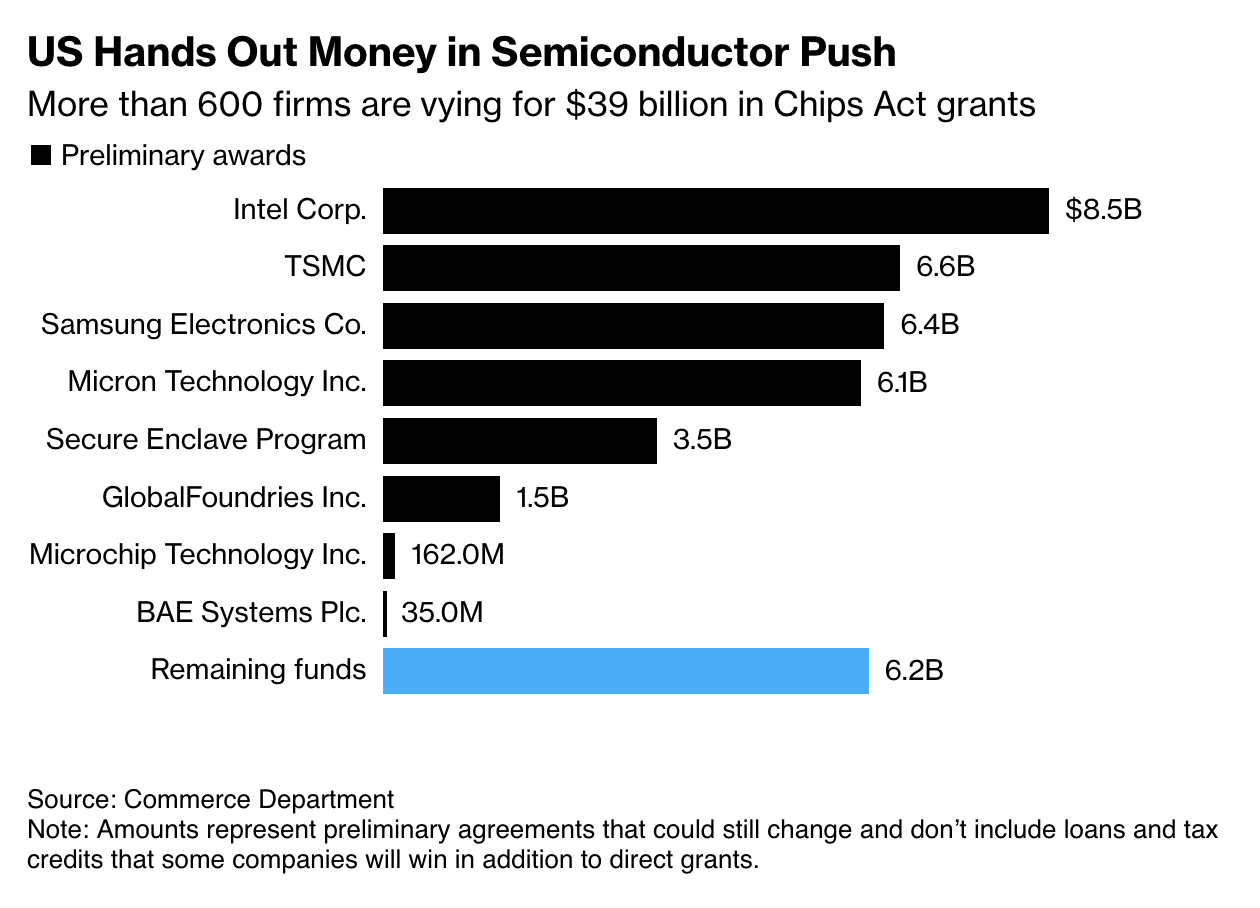

Out of the pot, and out of the companies’ whose fabs and capabilities actually matter in the industry, Intel got $8.5 billion, TSMC got $6.6 billion, Samsung got $6.4 billion, and Micron got $6.1 billion. That is 70% of the total pie of $39 billion that’s made available by the CHIPS Act. There is $6.2 billion left in the pot, and I expect remaining American companies, like Texas Instruments, to receive some of what’s left.

The allocation of these subsidies alone took a surprisingly herculean effort by the Commerce Department, which had to stand up a CHIPS program office from scratch and hire hundreds of staffers to receive, vet, and decide on all the applications. As America’s first go at a major industry policy in a long while, reaching this milestone deserves some celebration and relief.

Sadly, this celebration can’t last long because it is the easy part of onshoring advanced semiconductor manufacturing onto US soil. As Morris Chang likes to say, this is just the “end of the beginning.” Among all the companies that have received subsidies, only TSMC really matters, if we focus on the “advanced” part of advanced semiconductor manufacturing. When Commerce Secretary Gina Raimondo boasted about how the US has the “most sophisticated semiconductors in the world” on 60 Minutes, and Lesley Stahl pushed her by retorting “you mean Taiwan,” the Biden cabinet member begrudgingly responded, “Fair...”

Even with these subsidies, there is a common assumption that TSMC’s fabs outside of Taiwan will be less profitable due to the various foreseen and unforeseen costs of building “geopolitical redundancies.” Yet, TSMC has maintained and reiterated its longstanding financial goal of delivering 53% gross margin or higher. So the only way it could do so, amidst the obvious specter of higher cost, is raising prices.

With this first stage of CHIPS Act implementation behind us, we finally got some clues from TSMC’s most recent earnings call on the “where and how” of its plans to raise prices.

Where and How to Raise Prices

During the opening remarks of TSMC Q1 2024 earnings call, its CEO, CC Wei, offered this insight on cost, after sharing updates on its overseas fabs progress in Phoenix, Kumamoto, and Dresden:

“In today's fragmented globalization environment, cost will be higher of everyone, including TSMC, our customers, our competitors and the entire semiconductor industry. We plan to manage and minimize the overseas cost gap by, first, pricing strategically to reflect the value of geographic flexibility; second, working closely with government to secure their support; and third, leveraging our fundamental advantage of manufacturing technology leadership and our large-scale manufacturing base, which no other manufacturer in this industry can match.” (Bold emphasis mine)

In short, Wei and his TSMC leadership team have three levers to pull to maintain its gross margin profitability:

- Higher price

- Government help

- Economies of scale

When pushed by an analyst for more specifics on the possible price hikes, Wei offered this answer:

“[L]et me expand a little bit, we do encounter some kind of higher cost in the overseas or even recently, the inflation and the electricity [cost in Taiwan]. We expect our customers to share some of the higher cost with us, and we already started our discussion with our customers.

And as I said, for the overseas fab, we want to share our value, which also includes the flexibility of [ geopolitical ] location or something like that. If my customer requests to be in some certain area, then definitely, TSMC and the customer had to share the incremental cost.” (Bold emphasis mine)

As convoluted and diplomatic of an answer this may be, which is to be expected, Wei divulged that the topic of raising prices is already happening between TSMC and its many customers. And whether there will be a price hike or not depends entirely on if a customer needs its semiconductor source to come from a fab outside of Taiwan or not. If outside of Taiwan, more expensive, if in Taiwan, cheaper.

Then what types of companies or products would have such a need?

We also have some clues from the different strategic investors and partners that came together to build TSMC’s overseas capacities. In Japan, Toyota, Sony, and Denso are major investors. Thus, a good number of automotives, especially ones that may have security implications (e.g. government cars), may be required to source their chips from the joint venture with TSMC in Kumamoto – JASM (Japan Advanced Semiconductor Manufacturing). In Germany, Bosch, Infineon, and NXP are strategic investors and partners. Thus, a good number of automotives there would need to source their chips locally for the same reason. Additionally, communication equipment that are deployed in 5G base stations or have surveillance use cases, like CCTV cameras, would also likely require local sourcing (Bosch makes CCTV cameras). Of course, any military applications would fall squarely within this realm.

The tricky part is that, as the definitional venn diagram between semiconductor use cases and national security needs become bigger, the cost will become higher for a whole range of mostly consumer products. And this venn diagram is undoubtedly getting bigger by the day, especially in America.

From TSMC’s perspective, because it has the most leverage and largest economies of scale of any fab company – a well-earned one built over three decades of institutional knowledge and industry neutrality – it is confident in its ability to convince customers to share the burden. The wildcard is the size and efficacy of support that the respective governments can deliver to lower that cost, thus reducing or removing any price hikes for its own homegrown companies who are TSMC customers.

Interestingly, this is a competition among allies to see who can make TSMC’s local presence profitable and sustainable, not against China.

On the European side, it’s too early to tell since the European Chips Act is less further along.

In Japan, the government has been most generous and efficient so far, having already issued $8 billion USD worth of subsidies to JASM, more than the US government has allocated.

But TSMC Arizona is planned to have the most advanced technology of the three overseas expansions. The third planned fab in northern Phoenix is supposed to sport 2nm technology or better.

So in addition to the $6.6 billion from Uncle Sam, where else (if anywhere) can the US government play a role to help reduce the inevitable rise in cost, especially since the venn diagram between chips and national security (real or perceived) is by far the largest in America?

Where Can the Government Help?

Structurally, there are many challenges facing TSMC, or any fab company, when it comes to manufacturing semiconductors in the US. Many of these challenges are well-known, and there is very little the government can do about them.

For one, human capital costs more, much more. As I wrote in my deep dive on the advantages of building fabs in Kumamoto, one of them is that the entry-level engineering salary cost around $23,000 USD, similar to the level in Taiwan, but more than 60% less than in the US (around $60,000 USD). There are also immense and vexing cultural differences between the working style and expectations inside the TSMC fabs in Taiwan versus the typical expectations in the US. These differences, which have some irreconcilable cultural and even racial dimensions, are creating ongoing management and execution difficulties in Arizona and already causing employee attrition when the fabs are barely getting started. These human challenges are depicted in excruciatingly colorful but also useful details in this Rest of World article.

However, there are things the governments at all levels can still do to help move the ball forward. Here are three I can think of:

Clarify the semiconductor-national-security nexus: on the federal level, there is a lack of clarity as to what types of semiconductor applications warrant national security scrutiny. In the meantime, under the “small yard, high fence” doctrine, the yard keeps getting bigger and the fence keeps getting higher. While this loosely-doosey policy approach may help win turf wars in DC, it makes things impossible to anticipate for companies. TSMC Arizona will be the most costly producer of chips among all the locations. Thus, giving clarity on the semiconductor-national-security nexus, so companies know exactly what products have to source from the US fabs, while other products can be sourced from the most economical location, would be wise policymaking.

Unleash the community colleges: a hidden super power that the US has not tapped fully to support the dearth of semiconductor talent is mobilizing local community colleges to quickly recruit and train new workers. Yes, the salary will still be higher than in Japan, not to mention healthcare and other non-salary costs, but at least the pipeline of human capital will be larger, which will reduce the recruiting, training, and attribution cost that TSMC (and Intel and Samsung) must shoulder to fill up the empty fabs.

This piece would fall more on the state and local government, and some community college initiatives have been in motion. Maricopa County, where metropolitan Phoenix is situated, has tapped its community colleges to design a 10-day “Semiconductor Technician Quick Start” program to train local people. However, the program is currently on pause due to a slowing of hiring. This slowing most likely has to do with the slow pace in which the CHIPS Act allocated its subsidies to give clarity to the receiving companies on where things stand. Now that the allocation phase is mostly over, hopefully hiring will pick up again, and more of these community college programs will pop up to meet the talent gap.

No more social engineering: if there is one thing that shows the amateurism and arrogance of American industrial policy implementation, it is the practice that government subsidies have “social strings” attached to them. These strings come in the form of mandating the hiring of union workers, providing onsite day care, and meeting diversity hiring quotas (without using the word “quota” of course, because that would be unconstitutional).

To be clear, none of the aims of these requirements are bad or wrong per se. But mandating them in the form of social policy via industrial policy unnecessarily distorts the cost model further against the companies, when they are perfectly capable of making those choices on their own based on market dynamics. A company that needs more talent or wants to retain more employees who have young families will do its own cost-benefit analysis and decide to build onsite day care or expand its recruiting efforts to more diverse sources. The government should stay out of the way.

In the same 60 Minutes interview, Raimondo was also questioned by Stahl on this point. Raimondo pushed back saying that these requirements are not mandated, though they are written down as part of the conditions of receiving federal subsidies. Raimondo also contorted, rather confusingly and disingenuously, that this social policy is good because it’s “math” – as in the math of attracting talent.

It is not “math”, at least not the same math that’s used over and over again to model out cost, in order to make a fab sustainably profitable. Yet, sustainably profitable is what must happen for Raimondo’s own vision of increasing advanced chip manufacturing in the US from 0% to 20% by 2030 to not be just a pipe dream (or a campaign slogan).

Either way though, TSMC will find ways – through price hikes, government help from around the world, or its economies of scale – to keep its gross margin at 53%. Whether America contributes to that gross margin, or diminishes it, will depend on whether we genuinely and humbly want advanced chips on our shores for years to come, or only doing so begrudgingly, like this giant Arizona cactus, shaped like a big middle finger, flipping off the looming TSMC fabs.