If Disney builds a new rollercoaster using Didi’s stock chart from the last four weeks, it will surely be one of its most head-spinning, vomit-inducing rides yet. With so much volatility around all Chinese stocks, but Didi’s in particular, it is impossible to take a pause from the moving ticker and think through what Didi is really worth as a business.

An ever-moving stock price can be the biggest distraction to a company, especially one that does not quite have all its shit together – that’s Didi. But taking such a company private so it can focus on its business operations and comply with regulators can be a profitable opportunity for bold investors and a blessing for the company – that’s also Didi.

Let’s lay out the case for why taking Didi private may not be such a bad idea.

Don't Air Your Dirty Laundry in Public

Didi’s core problem is that by going public in the US, it violated one of the oldest Chinese sayings: “家丑不可外扬” (English adaptation: “Don't Air Your Dirty Laundry in Public”). By storing extremely sensitive data (personal transportation histories and patterns of hundreds of millions of people) and having very poor data security practices (not acceptable, but quite common in many high-growth consumer tech companies), Didi has many people’s “dirty laundry”. Didi also has its own “dirty laundry”, most notably a terrible track record of rider safety, resulting in death and sexual harassment of female users.

Whether it is other people’s “dirty laundry” or your own, airing and cleaning them in the public eye almost never works well. But with a stock ticker on the NYSE for all to see, that is what Didi is going through right now. In all fairness to Didi, listing on the NYSE was not much of a choice. The Hong Kong Stock Exchange was off-limits because it was not a profitable business (and still off-limits because it has not met the data security requirements of Chinese regulators). Raising more private capital was also not an option because its pre-IPO valuation was already high and existing large investors like Softbank and Uber likely needed a liquidity event.

Speaking of Uber, it also had a similar issue with its own “dirty laundry” – sexual harassment and discrimination in the workplace; “greyballing” local law enforcement officials from Philadelphia to Australia; getting sued for stealing self-driving technology secrets; and using its “God view” mode to track reporters who write negative stories about the company.

Even though these issues were all heavily reported by the media, Uber got lucky in one respect – it wasn’t a public company yet and had no stock ticker to reflect all the negative headlines on a day-to-day basis. While still a private company, Uber managed to fire its founding CEO and many senior execs, hired a new CEO, cleaned house somewhat, formed an independent committee to keep itself in check, and settled its self-driving lawsuit, before eventually going public in May 2019. Since then, Uber has had a relatively drama-free tenure as a public company.

Being drama-free and without the distraction of daily stock pricing may just be what Didi needs to air all its “dirty laundry” privately. Didi’s issues – fixing data security, making amends with regulators, improving user safety, while still growing the business – are all difficult but not impossible challenges. But the company needs leadership focus and the ability to attract and retain capable operators to do the fixing, which is quite impossible when your stock price swings wildly on every news headline that mentions your company’s name.

With its share price now down around 80% from its IPO price, Didi is no longer too expensive for private capital. The question becomes: is Didi still a good enough business to attract private capital to catalyze and profit from a turnaround?

The answer is definitely a “yes”.

Still A Pretty Good (Global) Business

I’d argue that Didi’s price is cheap enough now that if taken private, the probability of making a healthy return on the investment is better than 50%. Why? Because Didi’s product is still sticky in China, and its international market share outside of China is growing, especially in the fast-growing Latin American markets.

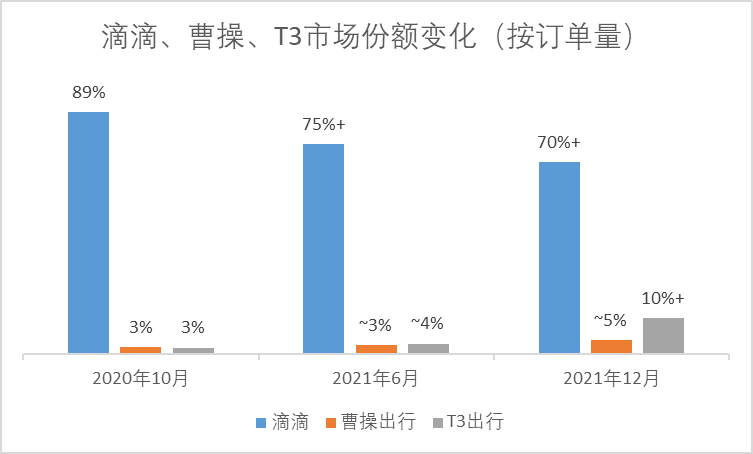

In China, Didi was ubiquitous until regulators forced its app off of all app stores last June to address its data security issues. Before June 2021, its market share was 90%. After June 2021, it has been losing ground to domestic competitors, like CaoCao and T3, but still commands around 70%. For comparison, Uber and Lyft split the US market 70% to 30%, respectively.

Let this sink in. Didi has so far been able to maintain a 70% market share in China, while no one was allowed to install its app for nine months and counting. Anecdotally, many users in China have avoided getting new phones, so they can keep using their Didi app. The competitors’ gain is also not because they have a different superior ridesharing model to Didi – it’s all the same – nor that they have better data security practices. They are simply too small for regulators to care. When (not if) the Cyberspace Administration of China and Didi come to terms, CaoCao, T3, and other copycat services will simply fall in line.

Furthermore, Didi’s stickiness and dominance are more apparent in 7th and 8th-tier cities in China where the only competitors are illegal, black taxis. These are places that most 1st or 2nd-tier city dwellers won’t even visit, let alone foreigners, so information about them is scant. This article, which articulates a rare and balanced view of Didi, cites an anecdote of a salesperson, who travels to one of these 7th/8th-tier cities often for work, and he swears by his Didi app because it addresses a huge pain point of finding trustworthy drivers to give him rides. The alternative would have been rolling the dice on a black taxi and crossing his fingers that he won’t get robbed (or worse).

Having been the dominant ridesharing player in China for so long, Didi’s mapping, routing, optimization, and recommendation algorithms powered by data collected from cities of all tiers are extremely difficult to replicate by a competitor. The same data, seen as “dirty laundry” by regulators, is also Didi’s moat.

Internationally, Didi has been investing in markets outside of China since it took out Uber China in 2016. Most of these overseas market expansions are money-burning machines, where the sole purpose is to gain market share at all cost. Didi’s most successful expansion region so far has been Latin America, which began in 2018 with the acquisition of Brazilian ridesharing app, 99. Late last year, Didi’s president, Jean Liu, revealed that Didi’s market share in top-tier Latin American markets (think Mexico City) is close to 50%.

When I traveled to Mexico early last year, I witnessed Didi’s activities first-hand, where local drivers formed long lines outside its office to drive for Didi and take advantage of its bonuses and discounts.

Didi now covers most Latin American countries and also operates in Japan, Egypt, South Africa, Australia, New Zealand, and even Russia (Didi announced an exit out of Russia due to its invasion of Ukraine, only to backtrack five days later).

To be clear, Didi’s international business, while growing, is nowhere near profitability; neither is its China business. Its service is usually in 2nd or 3rd place in overseas markets. But at the end of the day, Didi is still a sizable business with a sticky core market and growing global reach, not a worthless penny stock, as its price often suggests.

What is a Fair Price?

Even with the rosiest of glasses, Didi is in a tough spot and the company knows this. It is cutting 20% of its staff and reducing investment in many of its non-core businesses, like community group buying, to get lean for the tough years ahead (Didi still plans to make its own car though). Instituting more operational discipline and better product focus is never a bad thing, even though the process is always painful and real people’s lives (and livelihood) are impacted.

If you are a Blackstone, KKR, Vista, or TPG, taking Didi private at this moment and giving it 2-3 years to clean up, then taking it public again, could be a career-defining, fund-returning investment (Softbank would have been the most obvious source of more capital, but the failed Nvidia-Arm acquisition makes its ability to fund another huge investment murky).

But what would a fair price be for Didi?

Here’s my back of the envelope math, using Uber and Lyft as comps (Please take my calculation with a giant grain of salt as my investment focus is mostly in cloud, SaaS, infrastructure software, and DevOps, not in ridesharing consumer tech companies).

As of Friday, March 25, 2022, these are the market caps and share prices of Uber, Didi, and Lyft, respectively:

- Uber – market cap: $66.6 billion; share price: $34.06

- Didi – market cap: $15.8 billion; share price: $3.27

- Lyft – market cap: $13.1 billion; share price: $37.51

Didi should be worth less than Uber, but much more than Lyft (Lyft has no service outside of the US and a few cities in Canada). A fair market value for Didi should be around the midpoint between Uber and Lyft. Based on last Friday’s price, this heuristic would give Didi a $42.7 billion market cap and a share price of $8.83.

If a hypothetical group of investors takes Didi private at $4.90, paying a healthy 50% premium above its current price, and can exit the position at $8.83 in 2-3 years, this investment would net an 80% return. It’s likely that the “Taking Didi Private” price could be lower, making the investment return more attractive.

Not bad if you ask me. Fortune favors the bold.

将滴滴私有化

如果迪士尼用滴滴过去四周的股价图表建个新的过山车,那它肯定会是最令人头晕目眩、忍不住呕吐的游乐项目之一。最近所有中国公司的股价波动都如此之大,尤其是滴滴,让我们无法在动荡中按下暂停键,静静的思考一下滴滴作为一个企业的真正价值。

随时波动的股价是最让一家公司分心的困扰了,尤其是对内部秩序还不健全的公司而言,这就是滴滴。但是,将这样的公司私有化,使其能够专注于业务运营并遵守监管机构的规定,对于大胆的投资者来说是个有利可图的机会,对于公司来说也是个福音——这同样也是滴滴。

那就让我们看看,为什么将滴滴私有化可能并不是个坏主意。

家丑不可外扬

因为在美国上市了,滴滴的核心问题就是它违背一句老话:“家丑不可外扬”。通过存储极其敏感的个人数据(数以亿计的个人的出行历史和规律),以及极不健全的数据安全保护秩序(这种问题不可接受,但对这类高速增长的toC科技公司来说又很常见),滴滴存了许多人的“家丑”。滴滴也有自己的“家丑”,最“丑”的就是乘客安全问题,导致女性用户致死和遭到性骚扰。

无论是别人的还是自己的“家丑”,如果在大众面前“外扬”了几乎从来没有好结果。但因为有了NYSE的股票代码,所有人都能看到,“家丑外扬” 就是滴滴的现状。平心而论,滴滴在纽交所上市也是被逼的:当时没法上港交所,因为滴滴还没有盈利(至今还是上不了,因为滴滴在数据安全方面还没有满足要求,无法合规);筹集更多的二级市场私有资本也行不通,因为其上市前的估值已经很高,而且像软银、Uber这些大股东急需把钱拿出来。

说到Uber,它也有类似“家丑”的问题 —— 工作场合的性骚扰与员工歧视;使用“灰球”软件,在从费城到澳大利亚的一系列地区,躲避当地警方的钓鱼执法;因窃取自动驾驶科技机密而被起诉;以及利用其“God View”模式,追踪负面报道公司的记者。

尽管这些问题都被媒体大量曝光,但Uber在一个方面很走运——它当时还没上市,没有股票代码来反映每天不断的负面头条。在仍是一家没有上市的公司的时候,Uber炒了其创始CEO和许多高管,雇了新CEO,在一定程度上清理了内部秩序,成立了一个独立委员会来监督自己,并花钱平息了有关自动驾驶技术盗窃的诉讼。最终,Uber于2019年5月上市。从那时起,Uber作为一家上市公司也就没那么多丑闻了。

没有丑闻,没有每天股价波动的干扰,可能正是滴滴最需要的,私下清理各种“家丑”,而不要继续“外扬”。滴滴的问题——解决数据安全漏洞,与监管机构和解,改善用户安全,同时发展业务——都是艰难但并非不可能克服的挑战。但是,滴滴需要领导层集中精力,需要吸引和留住有能力的人才来执行修整。这种境界在每次公司名字上了头条股价就疯狂波动状态下,无法能做到。

滴滴的股价比其IPO价格已跌了80%多,对于私有资本来说,滴滴已不那么贵了。更需要问的问题是:滴滴作为一家公司它的业务还足够好,如果投入资本私有化会从中获利吗?

答案肯定是 "yes"。

仍然是个相当好的(全球)业务

我认为,滴滴现在的价格已经足够便宜了,便宜到如果被私有化,获得丰厚回报的概率超过50%。为什么呢?因为滴滴的产品在中国仍然具有粘性,而且它在各大海外市场份额正在扩大,特别是在增长迅猛的拉美市场。

在中国,滴滴是无处不在的,直到去年6月监管机构为解决其数据安全问题而迫使其下架。2021年6月之前,滴滴市场份额为90%。2021年6月之后,一直在流失市场份额给国内的竞争对手,如曹操和T3,但占有率仍在70%左右。那美国市场最对比,Uber和Lyft在美国的份额分别为70%和30%。

让我们好好想想这数据意味着什么。9个月以来,虽然没人允许下载滴滴的app,它还能够在中国保持70%的市场份额!许多用户甚至为了能继续用滴滴,避免购买新手机。同时,竞争对手的收益并不是因为它们与滴滴有多大的差异、其实共享乘车模式都是一样的,也不是因为它们有更好的数据安全管制。它们能成长是因为规模还太小,监管机构根本无暇顾及。当有一天(而不是如果)滴滴合规与国家互联网信息办公室的要求时,曹操、T3和其他山寨服务都将同样归顺。

此外,滴滴的粘性和主导地位在中国七、八线城市更为明显,那里唯一的竞争对手是非法的黑车。这些地方是大多数一线或二线城市居民都不会去的,更不用说外国人了,所以关于这些地方的信息很少。这篇文章阐述了对滴滴少有的平衡观点,并引用了一位销售人员的轶事:他经常去这些七八线城市出差,对滴滴的依赖性很高,因为滴滴解决了一个巨大的痛点,就是能随地找到可信的司机来载他。要不然,唯一的选择就是搭黑车,向老天爷祈祷不会被抢劫(或更糟的下场)。

滴滴长期以来一直是中国共享出行领域的主导者,滴滴的地图、路线、优化和推荐算法由从各层级城市收集的数据驱动,这些优势竞争对手极难复制。这些数据虽然被监管机构视为“家丑”,却也是滴滴的护城河。

在海外,滴滴自2016年击败并收购优步中国以来,一直在投资中国以外的市场。这些海外市场的扩张大多是烧钱增长,唯一的目的就是不惜一切代价获得市场份额。迄今为止,滴滴最成功的扩张地区是拉美,在2018年收购巴西共享汽车服务99时打响了第一炮。 去年年底,滴滴总裁柳青透露,滴滴在拉美一线市场(比如墨西哥城)的市场份额已接近50%。

去年年初我去墨西哥旅行时,亲眼目睹了滴滴当地的景象,当地司机在滴滴办公室外排起了长队,都想为滴滴开车,享受其奖金和折扣。

滴滴现在覆盖了大多数拉美国家,还在日本、埃及、南非、澳大利亚、新西兰,甚至俄罗斯都开展了业务(由于俄罗斯入侵乌克兰,滴滴宣布退出俄罗斯,但五天后又反悔了)。

说白了,滴滴的国际业务虽然在增长,但离盈利还有很长的路要走;其中国业务也是如此。其服务在海外市场通常处于第二或第三的位置。但是到头来,滴滴仍拥有一个粘性很高的国内核心市场和不断增长的海外业务,而不是像其股价暗示的那样,是一个毫无价值的仙股。

什么价格合理呢?

即使戴着最玫瑰色的眼镜来看,滴滴仍处于一个艰难的境地,公司也知道自己的处境。从裁员约20%,到减少许多非核心业务的投入,如社区团购,已经开始为未来艰难的岁月做准备(尽管如此,滴滴仍然计划自己造车)。业务运营更专注,提高对核心产品的关注,从来都不是一件坏事,尽管这个过程总是痛苦的,会影响到许多员工的生活(和生计)。

如果你是Blackstone、KKR、Vista或TPG,此刻投入滴滴将其私有化,给它2-3年的时间整顿,然后再上市,可能是笔能决定职业生涯走向,让资金回报翻倍的投资。(软银本来是最合适的资本来源,但在Nvidia-Arm并购失败后,其投资能力变得模糊。)

那对滴滴而言,什么价格合理呢?

以下是我个人的草草计算结果,以Uber和Lyft做参照(我的计算仅供参考,请不要照单全收,我的投资重点主要在云计算、SaaS、基础设施软件和DevOps方面,并不是共享出行这种toC公司)。

截至2022年3月25日周五,以下是Uber、滴滴和Lyft的市值和股价:

- Uber – 市值:666亿美元;股价:34.06美元

- 滴滴 – 市值:158亿美元;股价:3.27美元

- Lyft – 市值:131亿美元;股价:37.51美元

滴滴的市值应该低于Uber,但该比Lyft高得多(Lyft除了美国和加拿大的几个城市之外没有任何业务)。滴滴的合理市值应该大概是Uber和Lyft之间的中间点。根据上周五的价格,滴滴的市值应该大约427亿美元左右,股价应为8.83美元。

假如一帮投资人以4.9美元的价格将滴滴私有化,支付比其当前价格高出50%的溢价,并能在2-3年内以8.83美元的价格退出,这笔投资将获得80%的回报。实际上,私有化滴滴的价格可能会更低些,投资回报也更具吸引力。

如果你问我这笔投资值不值,我觉得还真挺值的。财富眷顾勇者。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周一篇新文章送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!