I’ve been struggling to come up with an elegant analogy to explain China’s regulatory crackdown on its tech industry. After observing this year’s Singles Day, I think I finally found it.

Everything that’s been happening in China Tech this year can be understood and analogized to a common practice that occurs periodically inside every successful tech company: removing startup debt.

How Does “Removing Startup Debt” Work?

Every startup accumulates a lot of “debt” during the initial years of its creation and growth. The original engineering team may have chosen the wrong stack or programming language to scale the product. The company might’ve selected the wrong HR and benefits provider that did not offer good enough health benefits to retain employees over time. The founding CEO may have hired the wrong early exec to build its go-to-market team. These are all real examples of “startup debt”, which can be technical, administrative, or organizational. They should all sound familiar to anyone who has started a tech company or worked in one.

Startups create these “debts” repeatedly, not because they are dumb, but because trying to do every aspect of company-building perfectly the first time is the wrong priority, when you don’t even know if your startup idea will work yet. Thus, moving fast, shipping features, testing out hypotheses, and running experiments is the right approach when starting something new, even though accumulating “debt” is the inevitable consequence and tradeoff.

It usually takes a tech startup 8-10 years to reach a stage of maturity where “removing startup debt” is even warranted. Most startups don't survive for that long; it’s a somewhat rarefied state to be in. When a startup gets to this stage, more experienced leaders usually get brought in, code review becomes more stringent, more investment is spent on improving infrastructure and testing capabilities, and more compliance measures get implemented across all functions. Basically, more of all the boring but essential things to “grow up”.

The most high-profile startup debt removal is Facebook (or Meta)’s transition from the controversial “Move Fast and Break Things” ethos to the decidedly more boring “Move Fast with Stable Infra”. This transition happened in 2014, exactly 10 years after Facebook's founding.

What does “removing startup debt” have to do with China’s tech crackdown? Everything!

Removing 40 Years of “Startup Debt”

When “opening and reform” began in 1978, that moment marked the beginning of China, the startup. The subsequent years of experimentation -- attracting foreign direct investment, trying out capitalism in a fishing village called Shenzhen -- was not unlike the initial years of any Silicon Valley tech startup. Deng Xiaoping was effectively a startup founder, searching for the elusive product market fit. Except the prototype was a poor country with close to 1 billion people at the time in a world market that did not understand it (and some would argue still don’t).

Fast forward 43 years later, it’s safe to say that China found its product market fit, has grown by leaps and bounds, but also accumulated a ton of “startup debt”.

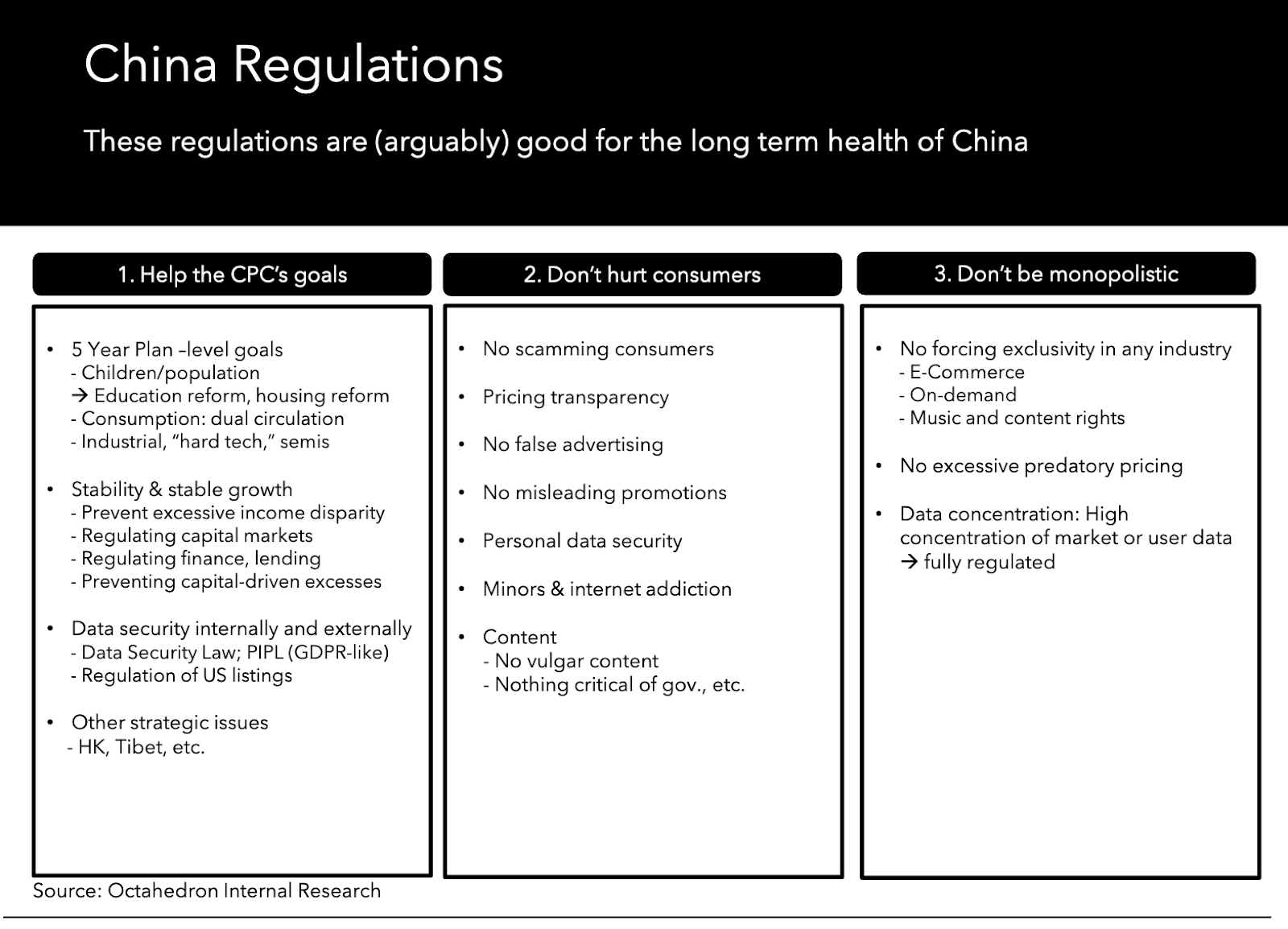

Some of this debt is literally just debt (like Evergrande). Some of this debt is technical debt (like the new data governance, data privacy, and various cybersecurity rules). Some of this debt is regulatory debt (like antitrust, fintech reform, and possible change to corporate structures like VIE). Some of this debt is cultural debt (like outlawing for-profit after-school tutoring and limiting minors’ videogame playing time). Similar to a 10-year-old startup, these are all the boring but essential things to “grow up”, just implemented in the largest economy in the world (at least in GDP PPP terms).

All of these debts need to be cleaned up sooner or later, so the fact that this cleaning happened earlier this year should not be surprising. What is more surprise-worthy is the speed in which they all happened in a short period of time, under the new CEO of China Inc., Xi Jinping, who is more powerful than Deng was. (Deng had to govern mostly by consensus during his tenure and his title within the Party was never higher than “Vice Chairman”.)

There are two tricky things about removing startup debt, whether it’s a company or a country.

First, it always takes longer than you think it does. Using Facebook as our example, it’s been seven years since “Move Fast with Stable Infra”, and Instagram was down just earlier this month.

Second, while removing your startup debt, growth can’t stop! You can’t stop shipping features and improving your products or your competition will surpass you. You just have to ship a little slower than before with more code review, more testing, and more compliance. While cleaning up its infra debt (and many other forms of societal debt), Facebook is still reinventing itself by becoming Meta.

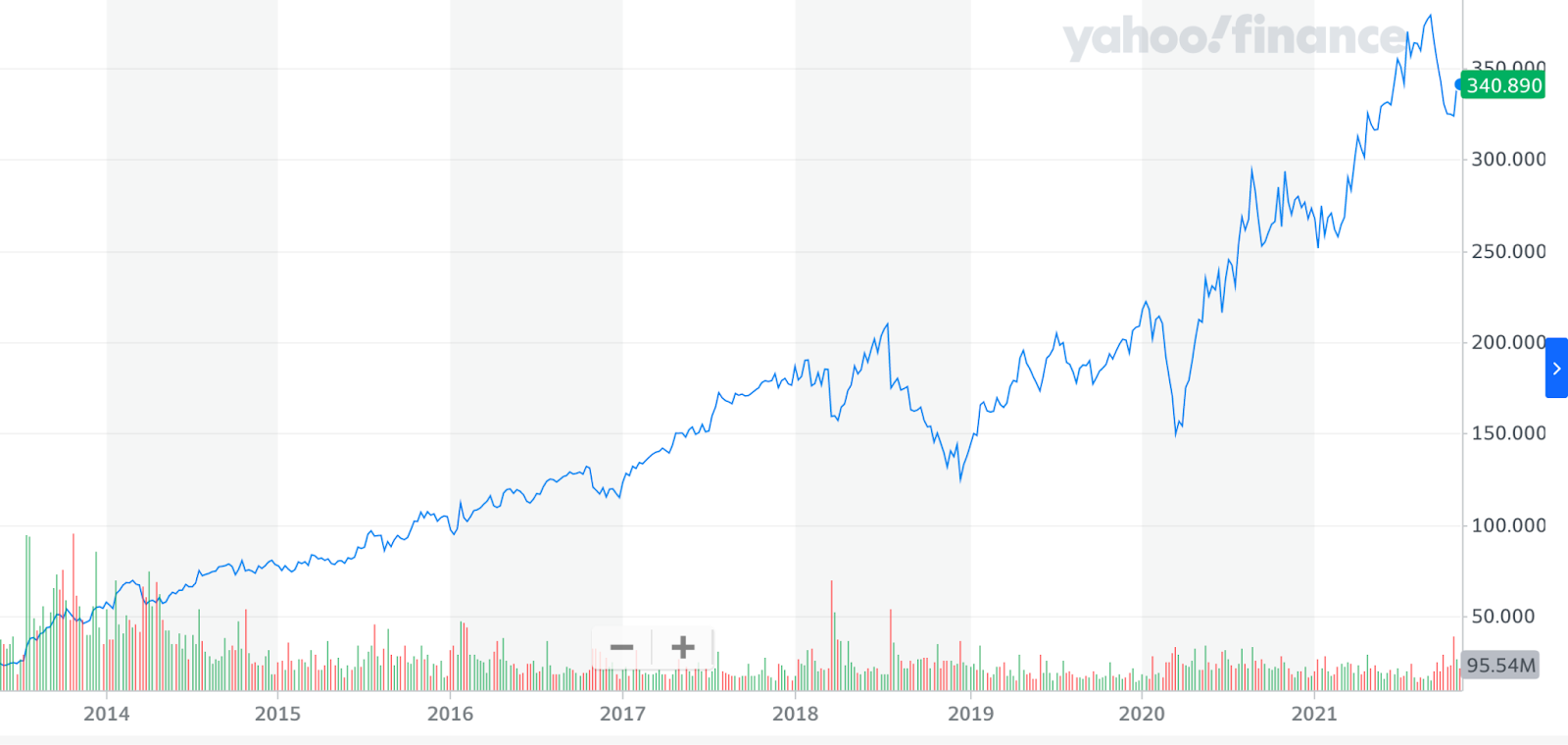

While it’s impossible (and intellectually irresponsible) to analogize Facebook to China, we can map a few concepts and experiences. Facebook is seven years into its debt removal journey and counting. We can safely assume that China, a 40-plus-year-old startup and a more complex organism, will take much longer to clean up its own startup debts. Since 2014, Facebook’s valuation and stock price has also grown at a healthy clip -- almost 6x. So we can also safely assume that China will keep growing for decades to come. Achieving this balance between removing debt and continuing growth is now the difficult terrain that China is about to face.

And that brings us to this year’s Singles Day and Alibaba.

New Singles Day, New China

The prevailing Western narrative of this year’s Singles Day is that it was a subdued, almost sad, affair. Nevertheless, the event generated an all-time high in GMV of $84.5 billion USD for Alibaba -- a 8.5% growth from last year.

Many Westerners are still discovering Singles Day. It is often used by foreign investors and analysts as a barometer to China’s consumer confidence. But it is really old news in China at this point; it’s been around as an online shopping holiday since 2009. Last year, Alibaba reframed the topline GMV number from a one-day sale to an 11-day shopping period starting from November 1st to 11th -- a clever PR trick. GMV itself is a notorious noisy and somewhat useless metric, when you account for return rate, margins after discount, etc. Singles Day has basically outlived its usefulness as a barometer.

But it can still be useful when viewed in the context of Alibaba as a whole, as Jack Ma’s creation navigates a “New China” focused on removing the country’s “startup debt” -- a lot of it was created by Alibaba under a permissive environment previously sanctioned by the government.

In startup terms, Alibaba still shipped “2021 Singles Day”, the product, and did decently well despite the circumstances. And that’s not the only thing $BABA is shipping. Alibaba Cloud shipped a custom-designed, custom-built chip as part of its proprietary server offering called Panjiu in October. The cloud unit also open sourced a bunch of software tools based on RISC-V, the open source chip design architecture, to bolster the RISC-V ecosystem. RISC-V is critically important to accelerating semiconductor design and development worldwide, but it’s boring. (Please see more of our writings on RISC-V and its strategic implications.)

China’s Big Tech like Alibaba will continue to build and ship products in this “New China” to fuel growth, they will just be more of the boring kind.

For a tech company, “removing startup debt” may slow down product improvement in the short-term, but generally creates a more sustainable foundation to grow for the long term. I see a similar possible future for China, but on a much longer time horizon. Short-term pain aside, investors who know China well, like Octahedron Capital, also believe that all these new regulations to remove China’s “startup debt” is a good thing for long-term growth.

No pain, no gain.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox once a week. Follow and interact with me on: Twitter, LinkedIn, Clubhouse (@kevinsxu).

清除中国的"创业债"

我最近一直在努力想出一个“优雅”的比喻来解释国内对其科技行业的监管打击。在观察了今年的双十一之后,我终于想出来了。

今年在中国科技界发生的一切可以从“清除创业债”来理解,这也是每家成功的科技公司会定期采取的一种常见做法。

怎么“清除创业债”?

每家创业公司在起家和发展的最初几年都会积累大量的 "债"。最初的工程团队可能选择了错误的堆栈或编程语言,导致支持产品扩容很困难;公司可能选错了人力资源和福利供应商,因此没有提供足够好的健康福利来长期保留员工;创始CEO可能聘错了来搭建市场团队的早期高管。这些都是 "创业债" 的真实例子,它可以是技术性的,也可以是行政性或是组织性的。对于任何创办过科技创业公司或在其中工作过的人来说,这些例子听起来应该很熟悉。

创业公司反复产出这些 "债",并不是因为他们愚蠢,而是因为当你还不知道创业想法是否可行时,试图一开始就把公司建设的每个方面做得完美是错误的优先级。因此,在创新时,快速迭代、ship新功能、测试各种假设和实验才是正确的做法,积累"债" 是不可避免的后果和代价。

一家科技创业公司通常需要8-10年的时间才能达到一个足够成熟的阶段,到时候才值得考虑 "清除创业债"。大多数初创企业都活不了那么久,能达到那个境界已经很罕见了。当一个创业公司步入这个阶段时,通常会有更多有经验的领导加入,代码审查变得更严,更多的资源被用于改善基础设施和测试能力,以及在各个部门都会开始实施更多的合规措施。换句话说,为了 "长大" ,就要做更多无聊但必要的事情。

最高调的 “创业债” 清除就是Facebook(或Meta)从有争议的 "Move Fast and Break Things" 调调转型到明显更无聊的 "Move Fast with Stable Infra"。这一转型发生在2014年,正好是Facebook成立10年之后。

“清除创业债”与当今中国科技界有啥关系?关系可大了!

清除40多年的"创业债"

当改革开放于1978年开始时,那一刻标志了中国这家创业公司的起点。随后几年的实验——吸引外资,在一个叫深圳的渔村尝试资本主义——与任何硅谷创业公司的最初几年并无不同。邓小平实际上是个创始人,当时就在寻找product market fit。只不过当时的“产品原型”是一个拥有近10亿人口的贫国,而整个世界市场并不了解它(直到今天仍然有很多方面的不了解)。

快进43年后,可以说中国找到了自己的product market fit,实现了飞跃式增长,但也积累了大量的 "创业债"。

这些“债”中的一部分真的就是债(如恒大),有些是“技术债”(如新出炉的数据治理、数据隐私和各种网络安全规则),有些是“监管债”(如反垄断、金融科技行业改革和可能发生的公司结构监管,如VIE),有些则是“文化债”(如取缔营利性的课外辅导和限制未成年人玩游戏的时间)。类似于一个10岁左右的创业科技公司,这些都是为了 "长大" 而做的无聊但必要的事情,只是用在了世界最大的经济体上(至少以GDP购买力来算)。

所有这些“债”迟早需要被清除,所以今年中国监管界内外发生的事情不应该令人惊讶。值得惊讶的也许是,在中国这个创业公司新任CEO习近平的领导下,清除“创业债”在极短的时间内就发生了。

清除“创业债”通常有两个特征, 无论是用在公司上,还是国家上,都是成立的。

首先,整个过程总是比你想象的要长。以Facebook为例,自 "Move Fast with Stable Infra" 以来已过七年,而Instagram在本月初还是down了。

第二,在清除“创业债”的同时,增长不能停!不能停止打造新功能,不能停止改进产品,公司不能停止发展,否则竞争对手会超过你。和以前不一样的是,步伐要放慢点,代码审查步骤要多点,测试也要更完善点,总体做法要更合规点。在清除其基础设施的“创业债”(以及其他形式的“社会债”)的同时,Facebook仍通过Meta来重塑自己。

虽然将Facebook与中国进行类比是不合理的(也是不负责的),但我们可以映射一些类似的概念和经验。Facebook的清债之旅已经走了七年,还在继续。可以有把握地假设,中国这个累计了40多年“债”的“创业公司”将需要更长的时间。自2014年以来,Facebook的估值和股价也以健康的速度增长 -- 近6倍。因此,也可以有把握地假设,未来几十年的中国将会保持增长。在清除“创业债”和持续增长之间的平衡,则是现在中国要面临的挑战。

到聊聊阿里和双十一的时候了。

新的双十一,新的中国

西方媒体对今年双十一的普遍评论是,近年比以往低调,甚至有点惨。然而,整个活动仍为阿里创造了845亿美元的历史最高GMV——比去年增长8.5%。

许多西方人仍是第一次听说双十一。外国投资机构和分析师也经常把它作为中国消费能力的“指南针”。但在国内,双十一这个东西已经不新鲜了,从2009年就开始有了。去年,阿里把双十一GMV的公布从一天的数字改为从11月1日到11日长达11天的购物期的总和——玩了个巧妙的公关把戏。如果考虑到退货率、折扣后的利润率等因素,GMV作为一个指标其实没什么价值。因此双十一作为一个“指南针” 已经失效了。

但如果把它放在阿里的整体大情况下来看,还是有点用的,因为马云创建的阿里正在一个认真清除“创业债”的“新中国”中摸索——其中的“债” 很多是阿里在政府允许的宽松环境下创造出来的。

从一家创业公司的角度来看,阿里仍把 "2021年双十一" 这个产品release出去了,在这种大环境下看成绩还算不错。它也并不是阿里推出的唯一产品:阿里云在10月份发货了一款自定制设计的芯片,作为其专有服务器产品 "盘古" 的一部分。该云计算部门还开放了一系列基于RISC-V(开源芯片设计架构)的软件工具,以支持RISC-V生态。在全球,RISC-V对加速半导体设计和开发至关重要,但它很无聊。(请看《互联》关于RISC-V及其战略意义的文章。)

像阿里这种中国科技巨头,一定会继续在这个 "新中国" 迭代和推出新产品,以促进增长。只是新产品会更多是无聊的、不抢头条的那种。

对于一家科技公司来说,"清除创业债" 可能会在短期内减缓产品的更新迭代,但通常会搭建出一个更可持续的基础,以利于长期发展。我认为中国也有可能会有类似的未来,但时间线要长得多。撇开短期痛苦不谈,像Octahedron Capital这样熟悉中国的投资基金也认为,所有这些旨在清除中国 "创业债" 的新规定和政策对长期增长来说是件好事。

没有付出,就没有收获。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周一篇新文章送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!