Welcome to Interconnected Capital’s Q3 2024 investment performance letter, which I write on a quarterly basis. (You can find my most recent H1 letter here.)

To new and old readers alike, a friendly reminder: I run a global technology long-only fund focused on investing in the “picks and shovels” of the interconnected global digital AI economy. I draw on my technology business operator's experience and geopolitical antennas to bring an edge to how I assess a tech company’s rhythm and prospects in a constantly changing world.[1]

This quarter’s update is a little different. Over the last couple of months, I successfully raised a small round – a “friends and family of Interconnected” round. The clock for this “new” fund’s performance started on October 1, thus, the “clock starts anew” title. Future letters will reflect the performance of this new fund. As for this letter, the numbers reflect performance up until the end of Q3, prior to the start of the new fund. (If you are an accredited investor, who is interested in getting our 3rd-party examined 2023 performance report or learning more about Interconnected Capital, you can email me at: xu.kevin@interconnectedcapital.com.)

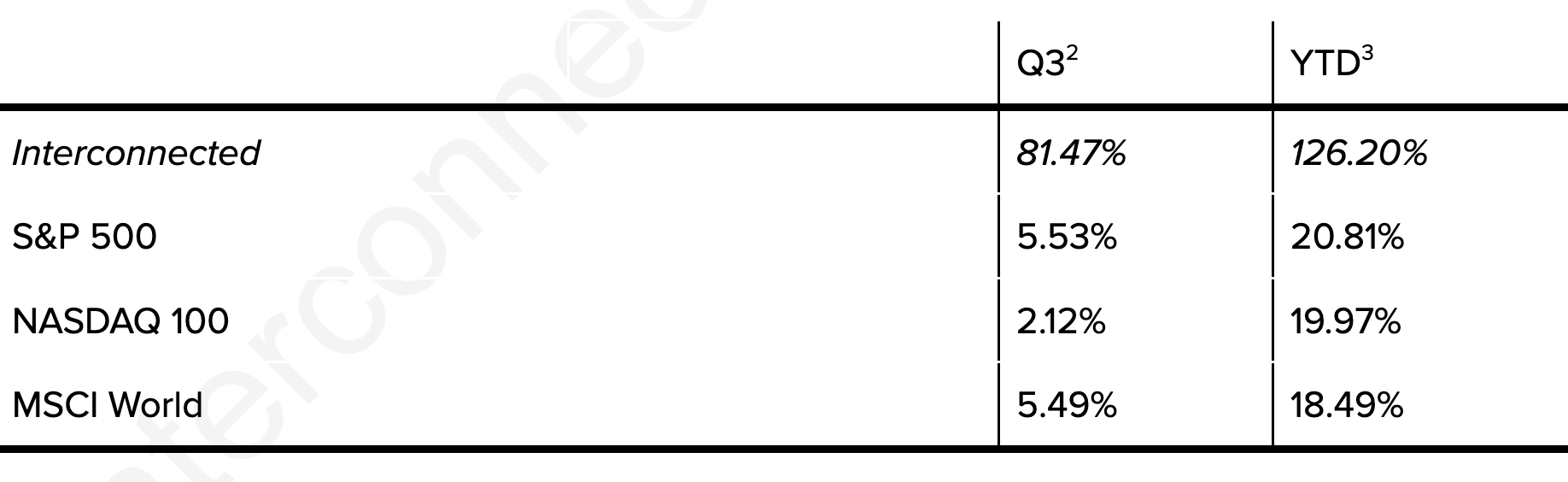

Without further adieu, here is my Q3 and YTD cumulative 2024 performance (ending on and inclusive of September 30), as well as comparisons to three relevant benchmarks – NASDAQ 100, S&P 500, MSCI World.

1 My past experiences include: senior leadership position at GitHub (the world’s largest developer and open source technology platform, now owned by Microsoft), a unicorn database startup, early stage VC, and the White House and Department of Commerce during the Obama administration. I studied law and computer science at Stanford; international relations at Brown.

2 Between July 1 - September 30, 2024. Unaudited.

3 Between January 1 - September 30, 2024. Unaudited.

Although the fund starts anew in a sense, the approach and strategy remains the same. I invest within a tight circle of competence – cloud computing infrastructure, DevOps, developer tools, open source, semiconductors. My process is value-oriented and bottoms-up, starting from the technology, then the business model, then the people and management, and ultimately the price – marrying technology fundamentals with financial fundamentals.

Starting Anew at an Interesting Time

Looking back, choosing to start fresh and reshuffling the deck in the September-October time frame landed on interesting timing. To properly and compliantly contribute my own money to the new fund (the GP commit), I had to liquidate all my positions first, which is why this letter does not contain a list of my positions (though you can refer to previous letters for what I have invested in before).

While I juggle the various operational, legal, and compliance tasks of bringing on new limited partners, most US indices hovered around all time highs. The Fed cut rates by 50 basis points. China also experienced its own policy-rumor-led euphoria and reached a temporary, local maximum. Psychologically, it was a mildly frustrating few weeks to watch on the sidelines, waiting for wires to clear. Then again, I have stated publicly in my Inner Scorecard letter that my goal is to generate 30% average annual return for 30 years or 30 for 30. Year 1 was 2023. So the mild frustration I went through was exactly that: mild.

As all the big tech earnings rolled in earlier this week, I am increasingly optimistic about a multi-year recovery and reacceleration of the cloud world. The Big Three hyperscalers – AWS, Azure, GCP – all reported impressive growth rates, even more impressive if you think about the large base the growth was based on, somehow escaping the constraints of the “law of large numbers”. GCP grew by more than 35%. Azure grew at 34% and is expected to continue growing above 30% for the foreseeable future, while the AI portion will reach a $10 billion run rate by next quarter (as in Q4 CY24 or now). AWS grew at 19% (looks small), but its RPO (remaining performance obligation aka backlog) accelerated to 23% on a business that has reached a $100 billion run rate!

Some of the smaller cloud players that are well within my investing circle of competence – Confluent, Twilio, Atlassian – also did well. The market’s post-earnings reactions to each of these companies speak for themselves. Yet, many of their peer companies are still trading well below their IPO price from just a few years ago!

AI no doubt has something to do with this (all of generative AI so far is built and deployed in the cloud). The long-waited normalization of cloud IT spend, reversing from the whiplash caused by Covid, is another major factor. To each of us, the pandemic may feel like a distant memory. But for the slow-moving rhythm of budgeting and spending for the Global 2000 companies, it has continued to be a relevant though finally fading factor. The market’s misplaced expectations and mispricings of this rhythm is one of the most consistent inefficiencies I have observed. It is an inefficiency I intend to take advantage of continuously.

Election Day “Playbook”

Looking ahead, many things on the near horizon will keep the market busy and volatile. Election Day in the US is around the corner. In the same week, the Fed also meets and another rate cut is expected. While Americans pick our next president, China’s National People’s Congress will deliberate on how much financial stimulus to pass and in what form to boost its economy. Lots of room for volatility, lots of room for opportunity, and I will stay vigilant on both fronts.

However, I don’t have an Election Day trade idea for you (or myself). As a long-term investor, as a matter of principle, I don’t trade around obvious events of volatility, whether it is something as big as an election or as small as quarterly earnings. But since the US election is such a looming, anxiety-inducing topic, I want to close by sharing some personal stories that may offer a “playbook” of sorts that offer some calm.

The first election I viscerally experienced was in 2008, when I worked as a staffer for the Obama campaign in Charlotte, North Carolina. On Election Day, I sent out waves of volunteers to get-out-the-vote in my territory, but was otherwise bored out of my mind. After working 100-hour weeks for months fueled by only adrenaline and little sleep, every hour and every minute on the big day felt like an eternity. Thinking back, it was what “leaving everything on the field” literally felt like. The Election Day boredom ended up being as reliable of a pattern as any. In 2012, when I was a White House staffer, I spent the day chit chatting with my West Wing colleagues and ate pizza in the Roosevelt Room to watch the results. In 2016, when I was doing voter protection work in Raleigh, North Carolina, I spent the day in the so-called “boiler room” playing card games online, while waiting for poll watchers to call us with voting irregularities. In 2020, when I was doing field work in Reno, Nevada, I spent the day passing out PPEs to volunteers (it was the height of Covid), booked a flight to Hawaii for the following week (it snowed in Reno that year), then drove to a deserted Black Rock City, where Burning Man is hosted, at night to stargaze.

If pattern matching is a basic skill of any good investor, then my pattern matching suggests this upcoming Election Day will be another “boring” one, though this one will be a different kind of “boring” from past elections. My current base case is we won’t know who the next president will be when Election Day is over, because the credibility of US media and the electoral institutions have been so thoroughly assaulted that any result will be challenged immediately by the losing side. We already got a preview of that in 2020, when the election was not called until the Saturday of election week and has been constantly challenged since, for some to this day.

In short, find your serenity and stick with your routines on Election Day – it is usually a boring day.

To think that billions of dollars have been burned on this election, yet it’s likely we won’t even know the result immediately, or trust the result even if we get one, is comically disappointing to me. It reminds me of one of Charlie Munger’s lesser-known zingers and a recent favorite of mine, which he uttered at the end of the 2016 Berkshire Hathaway annual meeting when asked about how he maintained his sense of humor over the years:

“If you see the world accurately, it’s bound to be humorous, because it’s ridiculous.”

I hope this quote brings you some levity, no matter what happens in the coming weeks and months.

Until next quarter (and year). Sincerely,

Kevin S. Xu

Date: November 2, 2024

(You can access the original letter in a view-only Google Doc link HERE.)

LEGAL INFORMATION AND DISCLOSURE

This letter expresses the views of the author as of the date indicated and such views are subject to change without notice. Interconnected Capital, LLC (“Interconnected”) has no duty or obligation to update the information contained herein.

Further, Interconnected makes no representation, and it should not be assumed that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This letter is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

Interconnected believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

All figures are unaudited. Interconnected does not undertake to update any information contained herein as a result of audit adjustments or other corrections. Past performance is not indicative of future results.

This letter, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Interconnected.