In Part I of our multi-part series on e-CNY, China’s digital currency, we presented an overview of the key players that are driving this project. One of those key players is the Digital Currency Research Institute, a dedicated R&D lab housed under the People’s Bank of China (PBOC). (See Part III on Strategic Value and Implications and Part IV on product experience, if you'd like to jump ahead.)

This Institute’s patent filings will be the focus of this Part II on Technology. Even though many other private and public organizations have been filing blockchain patents too, the e-CNY’s is a top-down, centralized finance (CeFi) project. Thus, the technology and patents that really matter are the ones developed by the Digital Currency Research Institute.

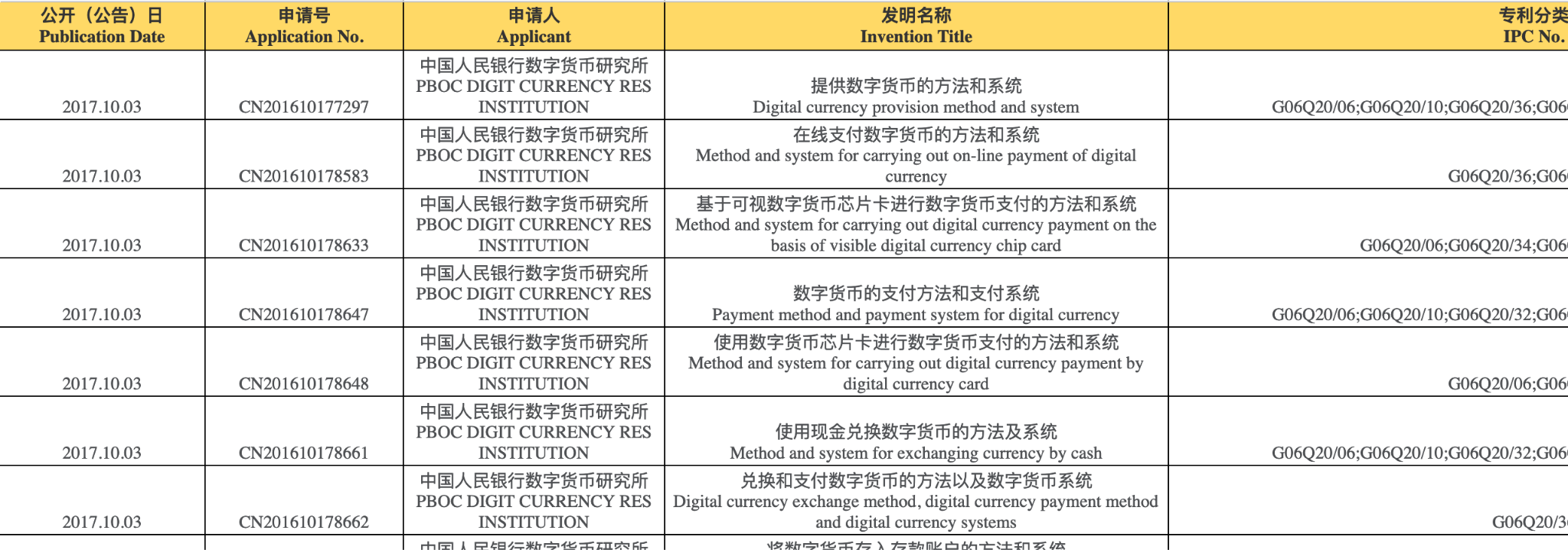

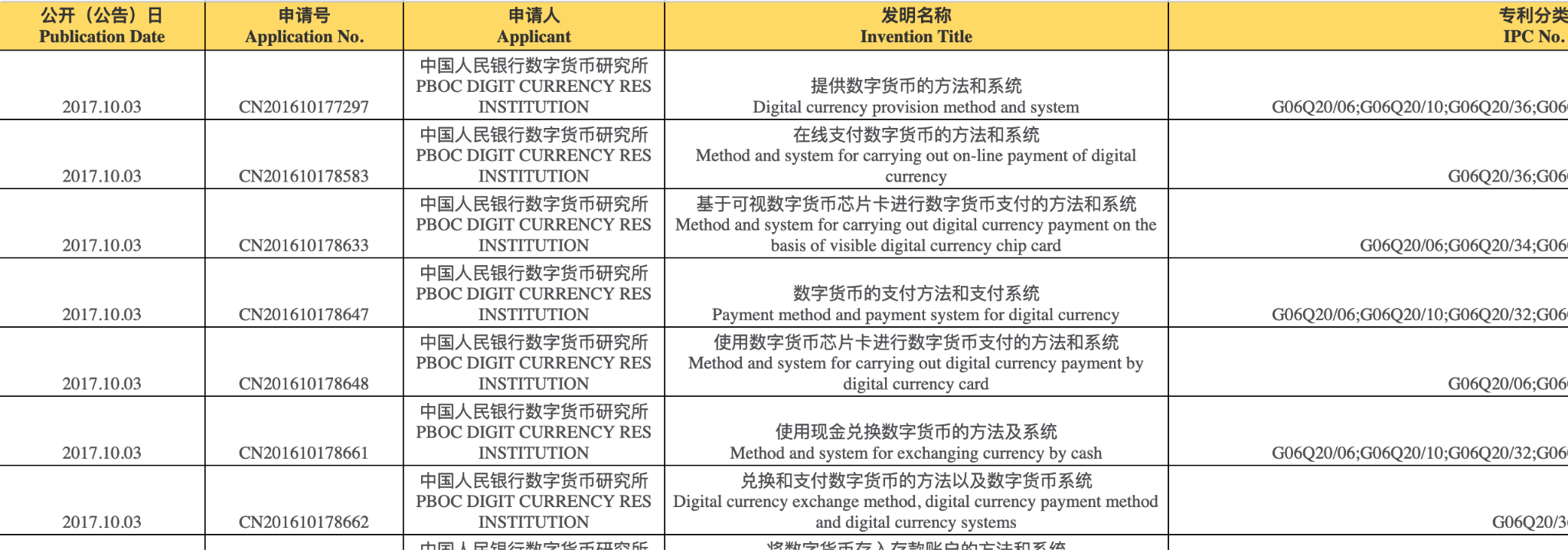

The Interconnected research team compiled all of the Institute’s patents since its inception -- 123 of them so far -- into a publicly viewable Google Sheet. We plan to update this list periodically. I won’t discuss every patent in detail, but will instead identify three categories that, in my view, are the most important and interesting from a long-term perspective.

User Experience: Payment, Wallet, Fiat

The Digital Currency Research Institute’s largest category of patents is related to payment, wallet, and interaction with fiat RMB. This is especially true during the first two years of the Institute’s existence (2017-2018). This focus is not entirely surprising, because to make any Central Bank Digital Currency (CBDC) work, the consumer adoption rate has to be meaningful. To accomplish that, the consumers have to trust this new way of interacting with their money, thus the user experience has to be meaningfully better than the alternative, which is dirty fiat cash or credit card.

In China, the user experience bar of a payment product is higher than most countries, because it has one of the more advanced and mature digital payment ecosystems. In other words, even though the PBOC has the authority to decree usage of e-CNY the currency, e-CNY the product can’t suck.

So far, the adoption rate of e-CNY is low. Based on the PBOC’s latest whitepaper, as of June 30, there are 20.8 million active individual wallets and the entire system has processed 70 million transactions -- less than 4 transactions per wallet. The e-CNY is, of course, still in trial use and has a long way to go to reach product maturity. Thus, the Institute’s investment in fundamental technology to make sure the user experience is up to par is table stakes. That means a stable wallet, easy payment via QR code, and smooth interface with fiat RMB, so consumers can trust this blockchain way of interacting with the money they have.

e-CNY’s big stress test will be the Beijing Winter Olympics, which is a mere 5 months away. It will be rolled out more broadly within China. It will also be introduced to all the athletes, which is a natural, if not "sneaky", way for the e-CNY to internationalize the RMB.

The e-CNY-Olympics nexus will not only be a test of narrative, but also a test of product and technology. We can assume that there will be coverage of the potentially sinister, “big brotherly” intent of the e-CNY. There will surely be a handful of athletes from the West who will refuse to use it due to a litany of valid privacy or security reasons, and garner most of the attention. But there will also be athletes from countries which either aren't concerned about China as much, or aren’t advanced enough, so accessing the technology is more valuable than the possible abuse of said technology. Privacy, by and large, is a first-world problem.

So the technology and product questions that e-CNY must be able to answer when the Winter Olympic rolls around are:

- Can e-CNY perform well and scale with the huge spike in transactions during the Olympics?

- Will the user experience and interface be intuitive enough where people from outside of China can adopt it easily?

- Can the settlement layer between different banks (aka inter-bank), both Chinese banks and non-Chinese banks, be executed accurately and consistently?

Inter-Bank Transactions

Whether the e-CNY can be an effective inter-bank transaction interface will determine how influential this digital currency can really be on the global stage. In late 2017, one year after the Digital Currency Research Institute’s founding, there was a flurry of patents filed that are focused specifically on inter-bank transactions.

This “inter-bank” piece should be assessed in two lenses. The first lens is the inter-banking system inside China. Even though the PBOC is the omnipotent central bank, there are many provincial and municipal level commercial banks in China, competing for consumers’ business and deposits, just like how Citizens Bank (a regional bank in New England I used when I went to Brown University) and Bank of America compete. The e-CNY’s first to-do will be to build a technical foundation that can facilitate transactions between banks inside China.

The second layer is the “internationalization” of the RMB. The ambition to “internationalize” is a stated PBOC goal since at least 2015 with the Cross-Border Inter-Bank Payments System (CIPS). As I noted in Part I of this series, the PBOC’s official exploration into the blockchain came on the heels of the lackluster launch of the CIPS.

Although the CIPS is still chugging along, with 53 direct participants and 1137 so-called indirect participants according to its website (most of whom are in the APAC region), blockchain-based digital currency is likely the future of inter-bank transactions. One of Ark Invest’s bull case arguments for Bitcoin is its potential to replace the traditional SWIFT money transfer system someday.

The PBOC sees this potential future as well, but the mechanism has to be something it controls, so it can’t be Bitcoin. The batch of patents on inter-bank transactions by Digital Currency Research Institute reflects that view.

Cryptocurrency Trading

The last category of patents that I’ll mention briefly is related to cryptocurrency trading. To be honest, calling it a “category” is premature. There is only one filing so far, but its timing is interesting.

This patent, blandly called “A digital currency trading method and system”, is the newest patent filed by the Institute on August 24. This is one month before the Chinese government announced its massive crackdown on all forms of cryptocurrency trading, which sent Bitcoin price into a tailspin.

If you only read the media headlines, you’d think that there will never be any cryptocurrency trading in China. But the patent filing suggests a different story. More trading-related patents will likely be filed and in due time, so crypto trading will resume in China, but the stablecoin interface will be e-CNY and e-CNY only.

Forbidding trading is like forbidding human nature. That won’t fly, even in China. The PBOC just wants to make sure it is being done via its own centralized blockchain.

I hope this Part II of our multipart series on e-CNY gave you a sense of its core technology and, in my view, the most interesting categories of patents being filed so far. In Part III, we discuss e-CNY’s strategic value and implications.

If you like what you've read, please SUBSCRIBE to the Interconnected email list. To read all previous posts, please check out the Archive section. New content will be delivered to your inbox once a week. Follow and interact with me on: Twitter, LinkedIn, Clubhouse (@kevinsxu).

e-CNY: 技术

数字人民币“多部曲系列”的第一篇中,我们介绍了推动这个项目的关键玩家。其中一个是央行的数字货币研究所,也就是央行的内部研发部门。(本系列第三篇关于e-CNY战略价值和影响,第四篇关于产品体验,两篇都已经发布。)

该研究所的专利申请将是本篇关于e-CNY技术的重点。尽管许多其他私有和公有组织都在积极申请区块链专利,但e-CNY的是一个自上而下的集中式金融(CeFi)项目。因此,真正重要的技术和专利都是由数字货币研究所开发的。

《互联》的研究团队已将该研究所自成立以来的所有专利 -- 到目前为止123项 -- 编入了一个可公开查看的谷歌表格,我们团队也计划定期更新这个列表。我不会在本篇文章详细讨论每一项专利,而是挑出了三个从长期角度来看最重要,也是最有趣的专利类别。

用户体验:支付、钱包、法币

数字货币研究所最大的一组专利是与支付、钱包以及与法币人民币兑换有关的,大部分都是在研究所成立的前两年(2017-2018)申请的。对这类专利的关注并不令人惊讶,因为要使任何中央银行数字货币(Central Bank Digital Currency,CBDC)发挥作用,消费者的采用率必须达到一定程度。要做到这一点,消费者就必须信任这种与他们的个人钱财互动兑换的新方式,因此用户体验必须比旧方式(即脏脏的纸钱或信用卡)要好很多。

在中国,支付产品的用户体验标准要比大多数国家高,因为中国科技生态在这方面是比较先进和成熟的。换句话说,即使央行有权下令强迫使用e-CNY这个新数字货币,e-CNY这个新的科技产品还是不能太差。

到目前为止,e-CNY的采用率还很低。根据央行最新的白皮书,截至6月30日,有2080万个活跃的个人钱包,整个系统仅处理了7000万笔交易 -- 每个钱包平均不到4笔交易。当然,数字人民币仍处于试用阶段,要达到产品成熟度还有很长的路要走。因此,研究所在基础技术方面的投资,以确保用户体验达到标准是必要的。要有一个稳定的钱包,通过二维码轻松支付,以及与法定人民币的顺利兑换,让消费者可以信任这种新颖、用区块链驱动的花钱方式。

e-CNY最重要的“压测”将是北京冬奥会,距离现在仅有5个月的时间了。冬奥会期间,e-CNY将在中国境内更广泛地推广。它也将被介绍给所有来自世界各地的运动员,这是e-CNY偷偷 "国际化" 的一个自然渠道。

e-CNY与冬奥会的结合不仅是对媒体舆论的考验,也是对产品和技术的考验。可以默认西方媒体会对数字人民币的潜在威胁做出报道,也会有少数西方国家的运动员由于一些合理的隐私或安全原因而拒绝使用e-CNY,并获得媒体关注。但也会有一些国家的运动员,要么对中国不那么在意,要么本国不够先进,所以获取技术比担心该技术的可能滥用方式更重要。隐私,总的来说,是一个第一世界的问题。

所以从技术和产品角度来说,在冬奥会开始之前,e-CNY必须能够回答的问题是:

- e-CNY能否在奥运会期间扩容并扛住巨大的交易高峰?

- 用户体验和界面是否够易用,让外国人也能够轻易采用?

- 不同银行(也就是银行间)之间的结算层,包括国内银行和非国内银行,能否准确和一致地结算?

银行间交易

e-CNY能否成为一款有效的银行间交易接口,将决定它在全球舞台上最终会有多大影响力。2017年底,在数字货币研究所成立一年后,就有一批专利专门针对银行间交易这一层技术。

"银行间交易" 这一块可以从两个角度来看。第一个角度是中国境内的银行间系统。尽管央行是大佬,但中国还有许多省市级的商业银行,都在做生意,争用户。数字人民币的第一项用处将是建立一个可靠的技术基础,以促进中国境内银行之间的交易。

第二个角度是人民币的 "国际化"。至少自2015年以来,央行就把人民币 "国际化" 作为一个大目标,当时创建了“跨境银行间支付清算系统”(CIPS)。但正如我在本系列第一篇文章中所指出的那样,该系统被推出后效果不佳,随后央行就开始认真地探索区块链了。

尽管CIPS还活着,根据其官网,有53个直接参与者和1137个所谓的间接参与者(其中大部分在亚太地区),但基于区块链的数字货币可能是银行间交易的未来。Ark Invest对比特币看好的一个论点就是它有可能在某一天取代传统的SWIFT汇款系统。

央行也看到了这个未来,但使用的机制必须是它能控制的,因此不能是比特币。数字货币研究所的这一批银行间交易的专利就反映了这个观点。

加密币交易

我将简要提及的最后一类专利与加密币交易有关。说实话,称其为 "类别" 为时尚早。到目前为止,只有一项申请与这方面有关,但其时机值得讨论一下。

这项专利被低调地称为 "一种数字货币交易方法和系统",是该所8月24日提交的最新专利,正好在中国政府宣布禁止所有形式的加密币交易的一个月前,当时比特币价格大跌。

如果您只看媒体头条,会认为在中国永远不会再有任何加密币交易了,但这项专利申请证明这种看法是不准确的。更多与交易有关的专利会在适当的时候不断出炉,中国应该也会恢复加密币交易,但可以用的“稳定币”界面只能是e-CNY。

禁止交易就像禁止人性一样,就算在中国,这也是行不通的。央行只想确保所有交易在自己能控制的中心化区块链上进行。

希望这篇文章帮您了解了数字人民币的核心技术,以及在我看来,所有专利中最值得注意的几个类别。在本系列第三篇中,我们将讨论e-CNY的战略价值和影响。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周一篇新文章送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!