Last December, I wrote a rather provocative post called “Let the ‘Great Delisting’ Begin”. That was when the SEC released its final specifications to implement the accounting compliance requirements outlined in the Holding Foreign Companies Accountable Act (HFCAA). Back then, and right on cue, every Chinese company’s stock price dropped like dead flies, whether they were listed in the US, Hong Kong, or both.

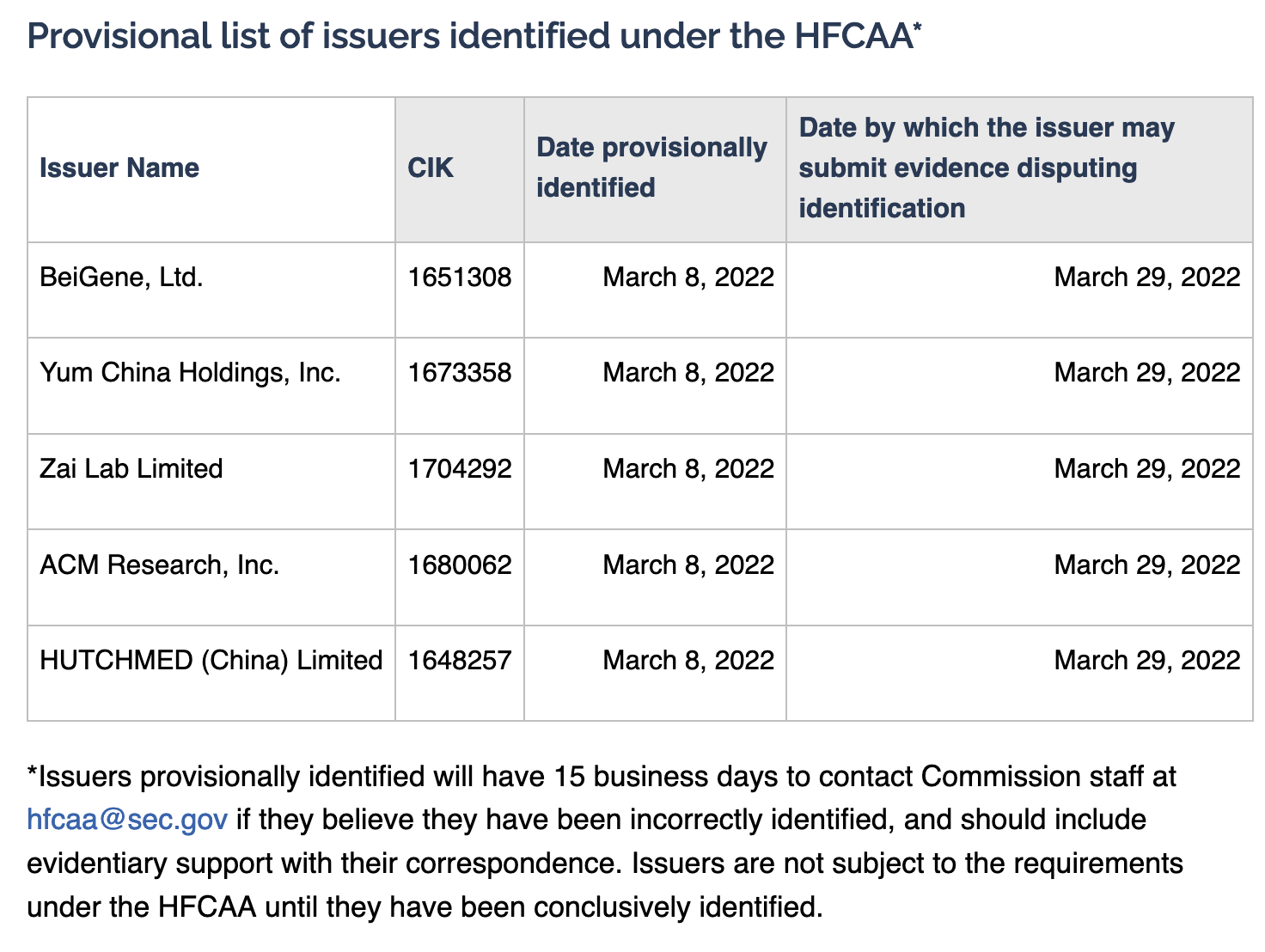

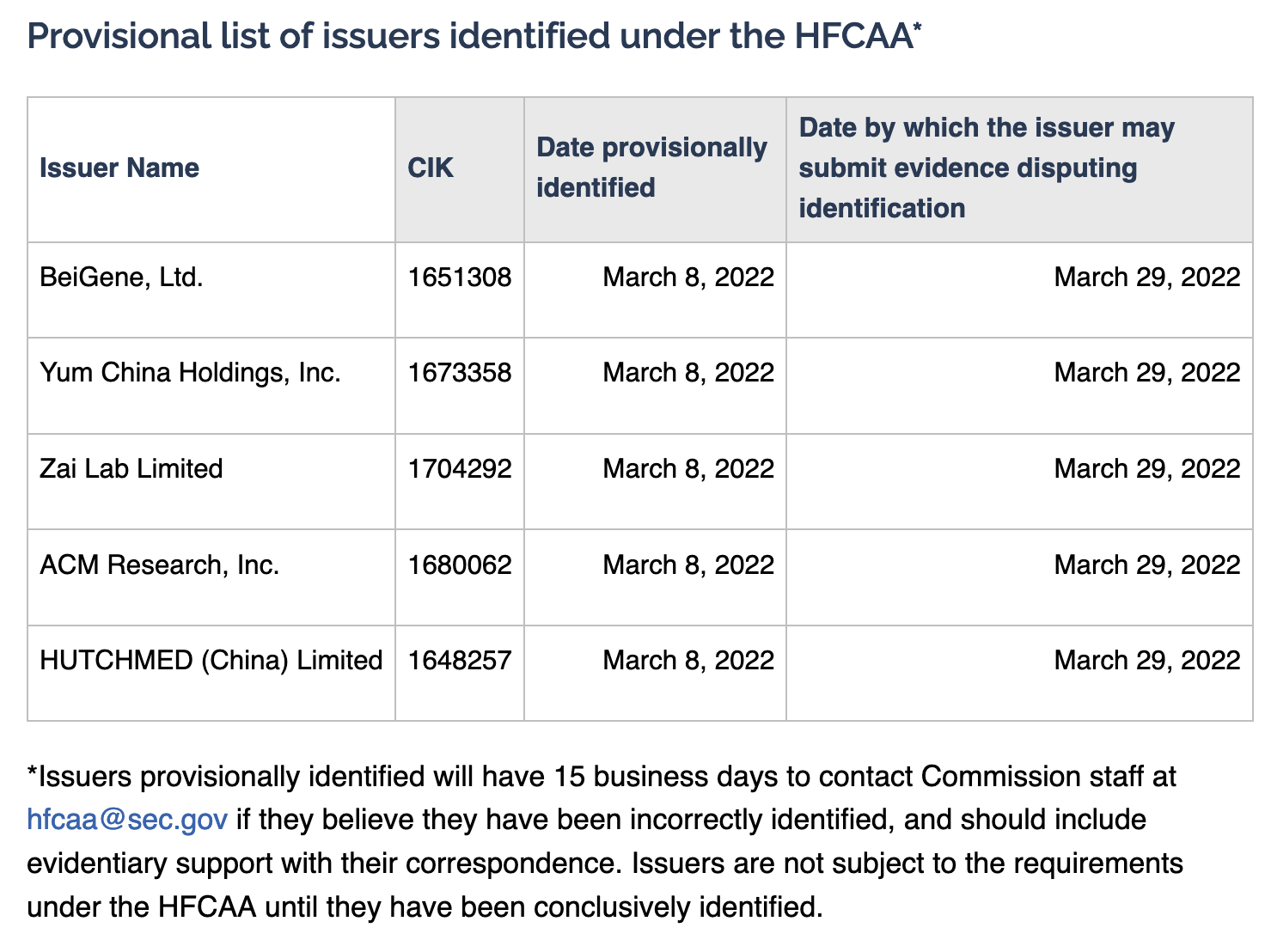

Last week, the SEC announced the first five companies it deemed questionable on the provisional list of its so-called “Commission-Identified Issuers” – what I call the “naughty list”. It is provisional because these companies – BeiGene, Yum China, Zai Lab, ACM Research, HUTCHMED (China) – have 15 business days (so until March 29) to push back on the SEC’s “public shaming”.

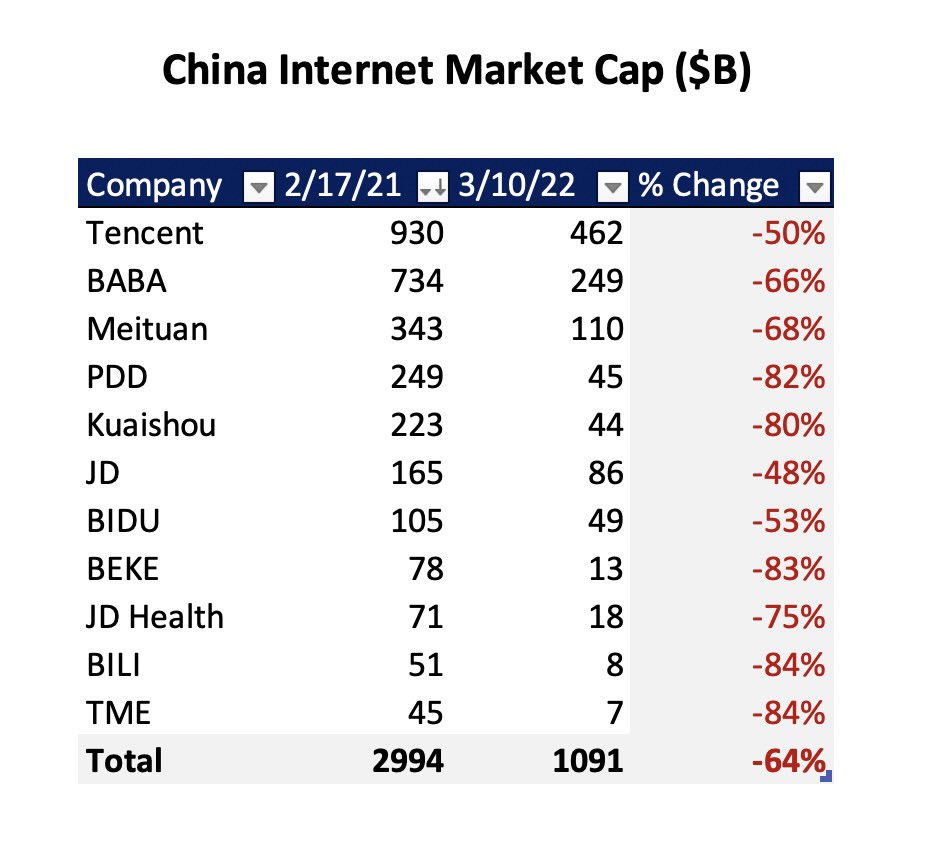

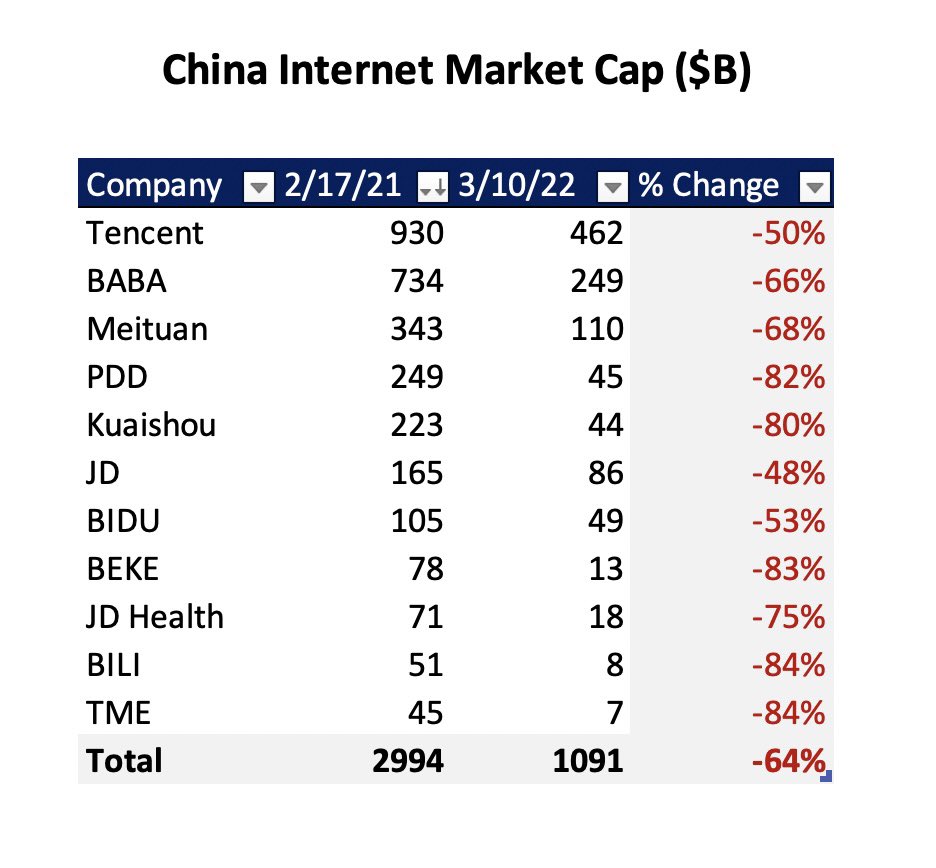

Again, right on cue, every Chinese company under the sun collapsed further, like a melting avalanche, even though these five companies are relatively insignificant as far as market caps or influence is considered (except for maybe Yum China; KFC’s and Pizza Huts are still a big deal in China). In particular, the Internet sector saw the largest drawdown – this vomit-inducing picture says it all.

With so many reasons to feel jittery about the market, it’s worth taking a step back to see if there is any quality information we can dissect to see through the fog and not let fear and confusion take over our brains.

Luckily, there is.

Dissecting the PCAOB Database

The SEC said last December it had identified a total of 273 companies that could be on the “naughty list”, but did not disclose any names back then. Simply go to this database on the PCAOB’s website and you will find them all!

The PCAOB (Public Companies Accounting Oversight Board) is the central regulatory actor within the SEC that determines who is “naughty” and who is “nice”. It is the auditor of all auditors. This responsibility was enshrined in the Sarbanes-Oxley Act of 2002, long before the HFCAA was even a thing.

Because of the political subtext of the HFCAA, there has been a common misconception that the PCAOB is after all Chinese companies. Not true. It is after public companies where their accounting and financial auditing practices occur in places where the PCAOB are not allowed to do inspections, regardless of whether you hire one of the Big Four accounting firms or a boutique. That’s why this database is described (rather verbosely) as a “database of PCAOB-registered firms located where non-U.S. authorities impede the PCAOB’s ability to conduct oversight activities.”

Even if a company was born in the US, thus an “American” company, if its accounting is done in a non-US region where the PCAOB is not allowed to conduct its inspection – like Mainland China or Hong Kong – then it could end up on the “naughty list”. In fact, as Liqian Ren of Wisdom Tree ETFs pointed out, ACM Research, a semiconductor packaging company that started in California and one of the five companies named, is such an example.

Clarify: CRITERIA SEC uses is whether the company's audit firm is on the PCAOB's list that it could not audit, which are mostly based in China mainland and HK.

— Liqian Ren (@liqian_ren) March 11, 2022

So ACMR, founded in US or not, will still appear on the list.

Link to PCAOB.https://t.co/eBmHCiYvRI pic.twitter.com/O5XFp7Yavz

Thus, it’s not about the “national origin” of the companies themselves nor the prestige or expertise of the accounting firms they hire. It’s all about the jurisdiction of the places where the accounting happens and whether these jurisdictions like each other or not.

That’s how you end up in this PCAOB database, and in effect, the “naughty list”.

It’s All About Nation-States

When the provisional list was first unveiled, sending shockwaves throughout the market, my initial reaction was there are two doors a company on the list can walk through to get itself off of it:

1. Change to a more reputable auditor;

2. Make auditing happen in a jurisdiction where the PCAOB is allowed to inspect.

Upon further thinking, only door 2 is viable. Door 1 is irrelevant. Despite how interconnected our world is, with the pervasiveness of the internet, global trade, and the international financial system, the question of whether a company gets delisted or not in 2022 comes down to a concept born out of the Treaty of Westphalia in 1648: nation-states.

What matters now is how two particular nation-states, People’s Republic of China (plus Hong Kong in this matter) and the United States of America, decide to deal with this matter, among all the other matters they need to worry about. The two relevant regulators are the China Securities Regulatory Commission (CSRC) and the SEC’s PCAOB. Everything else – no matter how large your market cap is, how cutting edge your product or technology is, how much AUM you have in your fund – is irrelevant.

While this picture may look gloomy, regulators can be reasonable problem solvers. There are signs that reasonableness and compromise may win the day between the CSRC and PCAOB, as current discussions between the two sides are described as “proceeding smoothly”.

Where these discussions could fall apart is if the CSRC views this matter as more of a national security issue, while the PCAOB views it as simply a financial one. That outcome would lead to a long-term impasse, inaction, and the “Great Delisting”.

If this worst-case scenario becomes reality, do we have a Plan B? If we dig into the PCAOB database, there are clues suggesting that a third nation-state (well, more of the city-state) may step up to save the day.

Pay Attention to Singapore

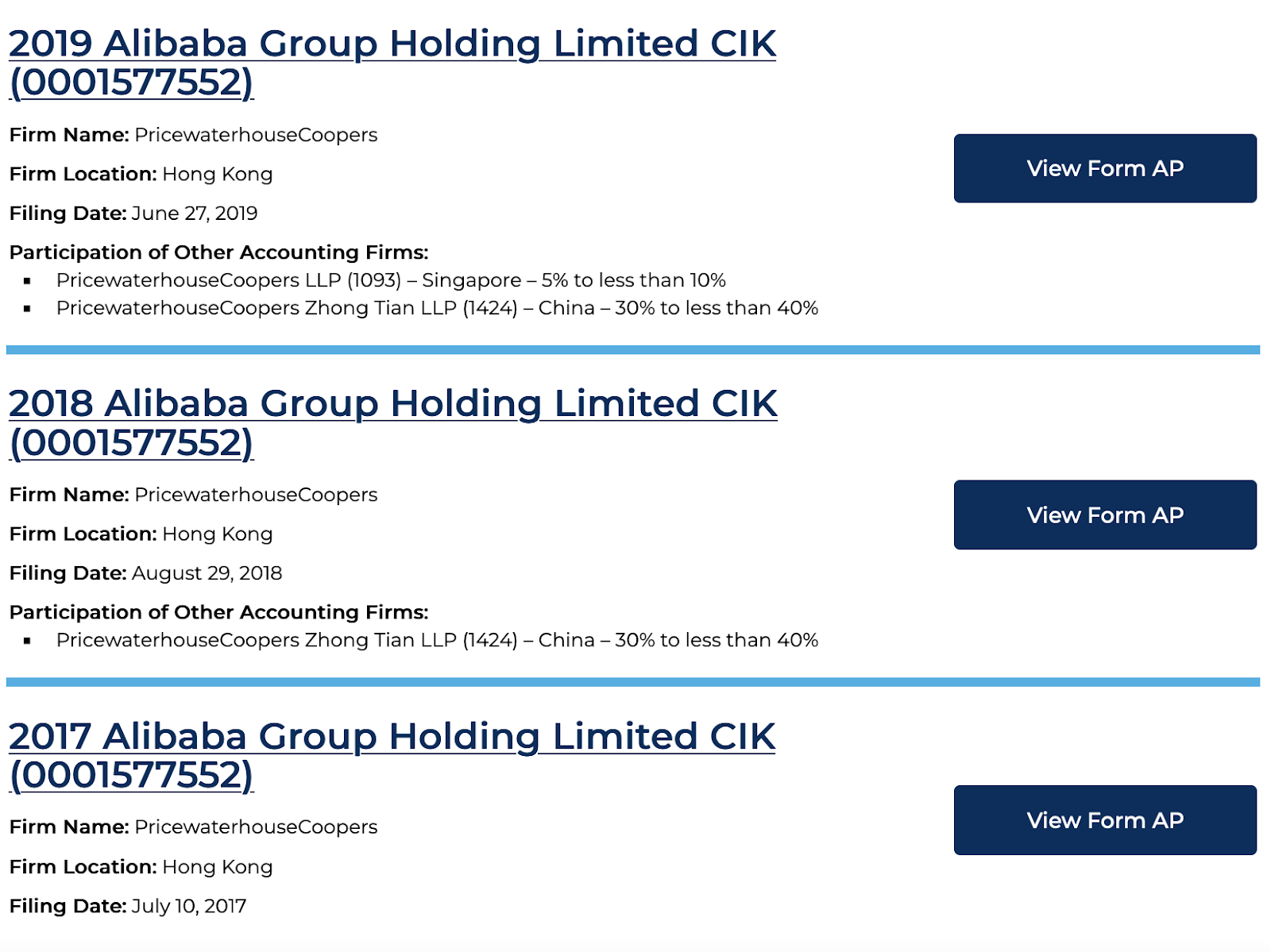

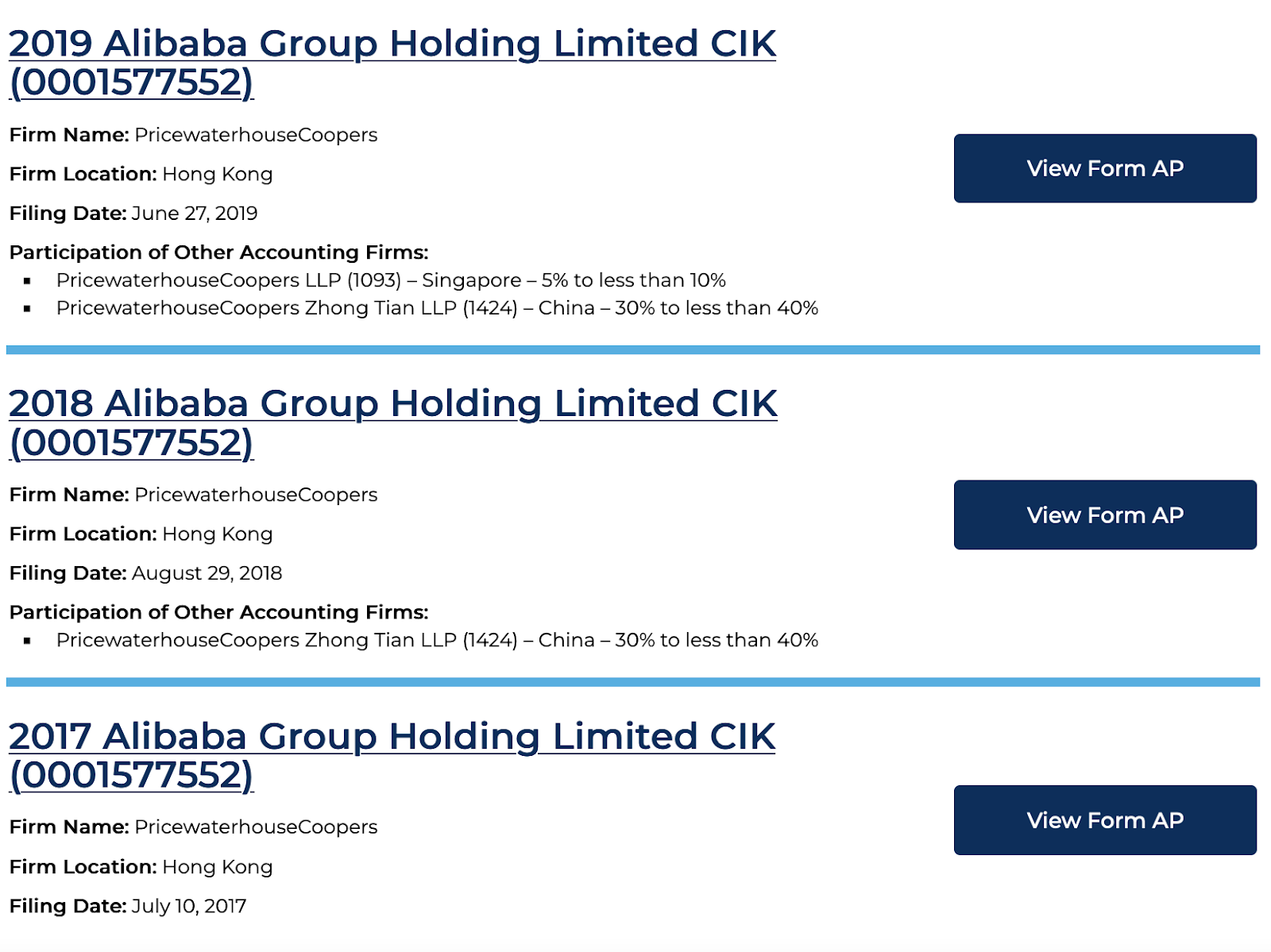

If you type in “Alibaba” into the PCAOB database, this is what you see:

As early as 2017, when the PCAOB first started requiring registered auditors to file the so-called Form AP to indicate which of their branches that are off-limits to the PCAOB are working for a US-listed public company, Alibaba’s auditor, PwC, started filing right away. These Form AP’s are what populate this database.

As you can see, over the last 4-5 years, Alibaba began diversifying its auditing location from being 100% in Hong Kong to Mainland China, but more interestingly, also to Singapore. In its latest 2021 filing, its auditing location distribution is 30%-40% in Mainland China, 5%-10% in Singapore, and the rest presumably still in Hong Kong.

The diversification to Singapore may be partly to serve real business expansion needs. All of Alibaba’s main product lines – e-commerce, fintech, cloud computing – are growing in Southeast Asia. But being the largest Chinese tech company listed in the US, it has always drawn the most attention and had the biggest “delisting” target on its back. It also has the most resources to hire the most creative lawyers and accountants to come up with a Plan B.

Will Singapore become this “compromise location” between the PCAOB and CSRC – a strategic position of neutrality it often serves in so many thorny geopolitical matters? (Remember, the meeting between Trump and Kim Jung-Un in 2018? That was dubbed the “Singapore Summit.” It does not get thornier than that.)

We will know the answer to this question soon enough. In fact, we may have gotten a hint of it already from one of the best investors alive and Alibaba’s newest fan: Charlie Munger.

It’s old news at this point that Alibaba is now the 3rd largest holding of the Munger-controlled Daily Journal. With $BABA stock price now lower than its 2014 IPO opening day price, Poor Charlie may be adding to his position this quarter, if he lives by his partner Warren Buffett’s investing creed: “be fearful when others are greedy, and greedy when others are fearful.”

Last month, when asked about the risk of owning Alibaba ADRs during the Daily Journal shareholders meeting, his response was:

“Assuming there is a reasonable honor among civilized nations, that risk doesn't seem all that big to me.”

I might be over-dissecting his response here, but the language he used was extremely precise – “a reasonable honor among civilized nations”, not between the US and China. The word “among” implies more than two.

He may be relying on Singapore to save the day (and his Alibaba holding) too.

剖析 "大退市"

去年12月,我写了一篇颇具煽动性的文章,名为《让“大退市”开始吧》。写那篇文章的契机是,美国证券交易委员会(SEC)发布了《外国公司问责法案》(HFCAA)中所述的会计合规要求的最终规范。当时,所有中国公司的股票价格都像死苍蝇一样下跌,无论它们是在美国、香港还是这两个地方都上市。

上周,美国证券交易委员会公布了所谓“Commission-Identified Issuers”的临时名单,上面有首批的五家公司——我称其为“淘气名单”。之所以说是临时的,是因为这些公司——百济神州、百胜中国、再鼎医药、盛美半导体、以及和黄医药(中国)——有15个工作日(所以直到3月29日)来反驳证监会的“公开羞辱”。

同样的,就在这个时候,天下所有中国公司的股票价格都进一步崩溃,就像一场融化的雪崩,尽管就市值或影响力而言,这五家公司相对来说并不重要(也许除了百胜中国,毕竟肯德基和必胜客在中国还是挺多人吃的)。其中,互联网行业的跌幅尤其大——这张让人作呕的图片说明了一切。

面对这么多让我们对市场感到不安的理由,值得退一步看看是否有任何高质量的信息,帮助我们通过剖析看穿迷雾,以防止恐惧和混乱占据了大脑。

面对这么多让我们对市场感到不安的理由,值得退一步看看是否有任何高质量的信息,帮助我们通过剖析看穿迷雾,以防止恐惧和混乱占据了大脑。

幸运的是,有这样的高质量信息。

剖析PCAOB数据库

美国证券交易委员会去年12月说,它总共确定了273家可能被列入“淘气名单”的公司,但当时没有披露任何名字。只要进入这个PCAOB官网上的数据库,你就能找到完整的公司名单!

PCAOB(Public Companies Accounting Oversight Board,即上市公司会计监督委员会)是美国证券交易委员会内,决定谁“淘气”、谁又是“好孩子”的核心监管部门。它是所有审计师的审计师。这一职责被写入了2002年的《萨班斯法案》,远早于《外国公司问责法案》(HFCAA)的出现。

由于HFCAA的政治潜台词,人们普遍误认为PCAOB的目标是所有中国公司。事实并非如此。它的目标是那些会计和财务审计行为发生在PCAOB不被允许进行检查的地方的上市公司,无论你雇用的是四大会计师事务所之一还是精品事务所。这就是为什么这个数据库被(相当冗长地)描述为,“位于有非美国当局阻碍PCAOB开展监督活动之处的PCAOB注册公司的数据库”。

即使一家公司诞生于美国,因此是一家“美国”公司,如果它的会计工作是在PCAOB不被允许进行检查的非美国地区进行的——比如中国大陆或香港——那么它最终也可能被列入“淘气名单”。事实上,正如智慧树投资的Ren Liqian所指出的,盛美半导体就是这样一个例子:一家始于加州的半导体封装公司,也是被点名的五家公司之一。

Clarify: CRITERIA SEC uses is whether the company's audit firm is on the PCAOB's list that it could not audit, which are mostly based in China mainland and HK.

— Liqian Ren (@liqian_ren) March 11, 2022

So ACMR, founded in US or not, will still appear on the list.

Link to PCAOB.https://t.co/eBmHCiYvRI pic.twitter.com/O5XFp7Yavz

因此,这与公司本身的“民族血统”无关,也与它们雇用的会计师事务所的声望和专业知识无关。一切都是关于会计发生之处的管辖权,以及这些管辖权是否喜欢对方。

这就是一家公司如何出现在这个PCAOB数据库中的原因,也就是实际上的“淘气名单”。

一切都围绕“民族国家”

当临时名单首次公布、给整个市场带来冲击时,我的第一反应是,名单上的公司可以通过两道门来把自己从名单上除名:

1. 换一个更有信誉的审计事所;

2. 在允许PCAOB检查的管辖区进行审计。

经过进一步思考,只有第二扇门是可行的,第一扇门是无关的。尽管我们的世界是如此的相互联结,互联网、全球贸易和国际金融体系无处不在,但一家公司在2022年是否会被退市,归根结底取决于1648年《威斯特伐利亚和约》中诞生的一个概念:民族国家。

现在最关键的是两个民族国家——中华人民共和国(加上香港)和美利坚合众国——在它们需要担心的所有事情中,如何决定处理这个问题。两个相关的监管机构是中国证券监督管理委员会(中国证监会,或CSRC)和美国证券交易委员会(SEC)的PCAOB。其他一切——无论你的市值有多大,产品或技术有多先进,基金有多少资产管理规模——都无关紧要。

虽然这幅画面看起来有点阴沉,但监管机构们可以是合理的问题解决者。有迹象表明,合理性和妥协可能会在中国证监会和PCAOB之间获胜,因为目前双方的讨论被描述为“进展顺利”。

如果中国证监会将此事视为国家安全问题,而PCAOB将其视为简单的金融问题,那么这些讨论就可能会破裂。这种结果将导致长期的僵局、不作为和“大退市”。

如果这种最坏的情况成为现实,我们是否有一个B计划?如果我们深挖PCAOB的数据库,里面其实有线索表明,第三个民族国家(好吧,它更像是个城市国家)可能会站出来拯救现实。

关注新加坡

如果你在PCAOB的数据库中输入“阿里巴巴”,你会看到以下的结果:

早在2017年,当PCAOB首次开始要求注册审计师提交所谓的AP表,以表明他们有哪些不受PCAOB管制的分支机构在为在美国上市的上市公司工作时,阿里巴巴的审计师——普华永道——就立即开始提交表格了。这些AP表就是这个数据库的内容。

正如你所看到的,在过去4-5年里,阿里巴巴开始将其审计地点多样化:从100%在香港,到分一些去中国大陆;更有趣的是,部分审计地点被改到了新加坡。在最新的2021年文件中,阿里巴巴审计地点的分布是30%-40%在中国大陆,5%-10%在新加坡,其余的可能仍然在香港。

走向新加坡的审计地点多样化发展,可能部分是服务于实际的业务扩张需要。阿里巴巴的所有主要产品线——电商、金融科技、云计算——在东南亚都在增长。但作为在美国上市的最大的中国科技公司,它一直吸引着最多的关注,并有着最大的“退市”目标在身。它也拥有最多的资源,可以聘请最有创意的律师和会计师,来想出B计划。

新加坡会成为PCAOB和中国证监会之间的“妥协地点”吗——一个诸多棘手的地缘政治事务中,它经常担任的中立战略地位?(还记得特朗普和金正恩在2018年的会晤吗?那被称为“新加坡峰会”,世上没有比这更棘手的事情了。)

我们很快就会知道这个问题的答案。事实上,我们可能已经从最好的投资者之一、阿里巴巴的最新粉丝查理·芒格那里,得到了一个提示。

现在,阿里巴巴是芒格控制的Daily Journal的第三大持股公司已是旧闻。当下$BABA的股价低于其2014年IPO开盘价,“穷查理”如果遵循他的合伙人巴菲特的投资信条:“在别人贪婪的时候要恐惧,在别人恐惧的时候要贪婪”,就可能会在本季度加仓。

上个月,在Daily Journal的股东大会上,查理·芒格被问及拥有阿里巴巴美国存托凭证的风险,他的回答是:

“假设文明国家们之间有合理的信誉,这个风险在我看来并不大。”

我在这里可能过度剖析了他的回应,但是他使用的语言极其精确——“a reasonable honor among civilized nations(文明国家们之间的合理信誉)”,而不是仅指美国和中国之间。“among”这个词意味着不止两个国家。

他可能是想靠新加坡来拯救世界(以及他持有的阿里巴巴股票)。

如果您喜欢所读的内容,请用email订阅加入“互联”。要想读以前的文章,请查阅《互联档案》。每周一篇新文章送达您的邮箱。请在Twitter、LinkedIn、Clubhouse(@kevinsxu)上给个follow,和我交流互动!