This week marks the 4th anniversary of Jack Ma’s infamous Bund Finance Summit in Shanghai that, among other things, led to the cancellation of Ant Group’s IPO. The IPO was geared up to be the largest ever – 34.5 billion USD. It was also supposed to be a rare, joint listing in both Hong Kong and Shanghai, which would’ve put the home of the Oriental Pearl on the map as a destination where premium tech companies could go public. The Shanghai portion of the IPO was oversubscribed by 872 times!

None of that happened, of course. For the next four years, Ant was in the “regulatory doghouse”. To comply and show good attitude, Ant broke itself up into several independently-run businesses. It did a share buyback program and issued three rounds of dividends to the likes of Carlyle and Temasek, who were major overseas shareholders and got screwed out of a big payday. It paid 7.1 billion yuan ($994 million) in fines to financial regulators. Jack Ma reduced his stake in Ant and controlling power.

Meanwhile, Alibaba was going through its own version of the “regulatory doghouse” – a three year journey that included a 18.2 billion yuan ($2.8 billion) fine for practicing the anti-competitive “pick one from two” scheme. This clean up did not officially wrap up until a month or so ago, when the State Administration for Market Regulations (SAMR) issued a statement declaring Alibaba properly “rectified”.

So is it time to rekindle Ant’s IPO dream?

I think so, though not just because the company probably deserves to be put back on track after four years of regulatory torture, but because China, at this critical juncture of its economic development, needs a blockbuster domestic IPO more than ever.

The IPO “Wealth Drain”

Most people are familiar with the concept of “brain drain” – talented people from one country leaving to study, work, and flourish in another country. There is an analogous version of this concept in the global capital market – an IPO “wealth drain”, if you will – where companies built on the talent and economic growth of one country goes public in another country, while retail investors from the home country can’t easy invest and access the wealth such an IPO may create.

Alibaba is the poster child of this phenomenon. After a subdued listing of its Alibaba.com subsidiary in 2007 in Hong Kong – an event few people remember – Alibaba Group executed the largest IPO at the time in September 2014 on the New York Stock Exchange (NYSE). It was all rainbow and roses for Softbank, other sophisticated institutional shareholders, and employees who had equity, but for an average investor in China whose online shopping budget contributed to Taobao’s top and bottom line, it was a deal of the decade that they could not participate in. And being locked out of the wealth created by Alibaba shares appreciation lasted for a decade, until just a few weeks ago, when the company finally completed a primary listing on the Hong Kong Stock Exchange. This listing status now lets Mainland Chinese retail investors to buy its shares easily through the Stock Connect Program, which as I wrote before may be too little too late for wealth creation.

Today, shares of leading tech companies like Pinduoduo and Baidu still do not have primary listing status in Hong Kong, and thus are difficult to access for the same reasons that Alibaba shares used to be. And for ambitious, up-and-coming tech companies in China, an IPO in Shanghai would still be considered a “minor failure”, a Hong Kong listing would be a decent outcome, and an IPO on Wall Street is still the crown jewel, even in the face of all the geopolitical headwinds and extra regulatory hoops to jump through.

Pony AI is the latest example of this “wealth drain”. Arguably the best robotaxi company in China from a technology perspective, Pony filed for a NASDAQ IPO last week. Its deployment is almost entirely in China, having secured licenses in all the tier-1 cities – Beijing, Shanghai, Guangzhou, Shenzhen – yet for its riders, its shares would be more difficult to grab than its robotaxis.

Zeekr, an EV brand owned by Geely, also went public on the NYSE, not Hong Kong or Shanghai. Even though it has almost no business prospects in the US thanks to tariffs and other restrictions for being a Chinese-made connected vehicle, and its “innovation”, the latest of which is a hotpot table in its luxury minivan, is hardly relatable outside of China, Wall Street money was still the preferred choice. While its share price has been mostly flat, Zeekr’s oversubscribed IPO raised a solid $441 million dollars.

Had the Ant IPO gone through in 2020, or even in 2022 as it was speculated at the time, would Pony or Zeekr have considered a domestic listing as more viable to fetch the valuation and raise the amount of capital it was hoping to? We will never know. But we do know that until a marquee tech company successfully lists in Shanghai – a path Ant was happy to pursue four years ago – the “wealth drain” will continue.

Money Come Home

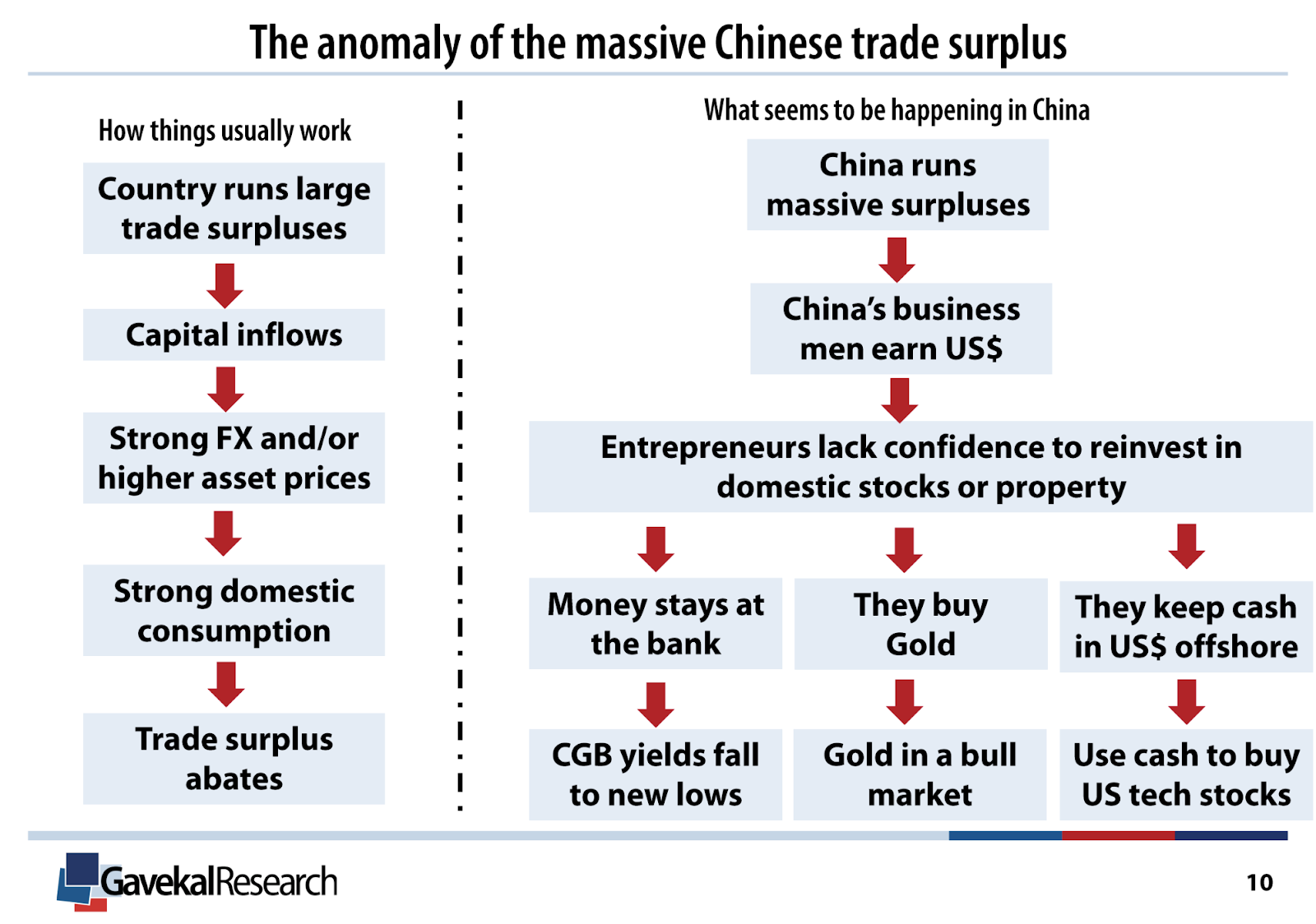

The IPO “wealth drain” is a symptom of large structural problems. These problems, all complex in their own right, can be summed up as such: Chinese money prefers to stay abroad than come home.

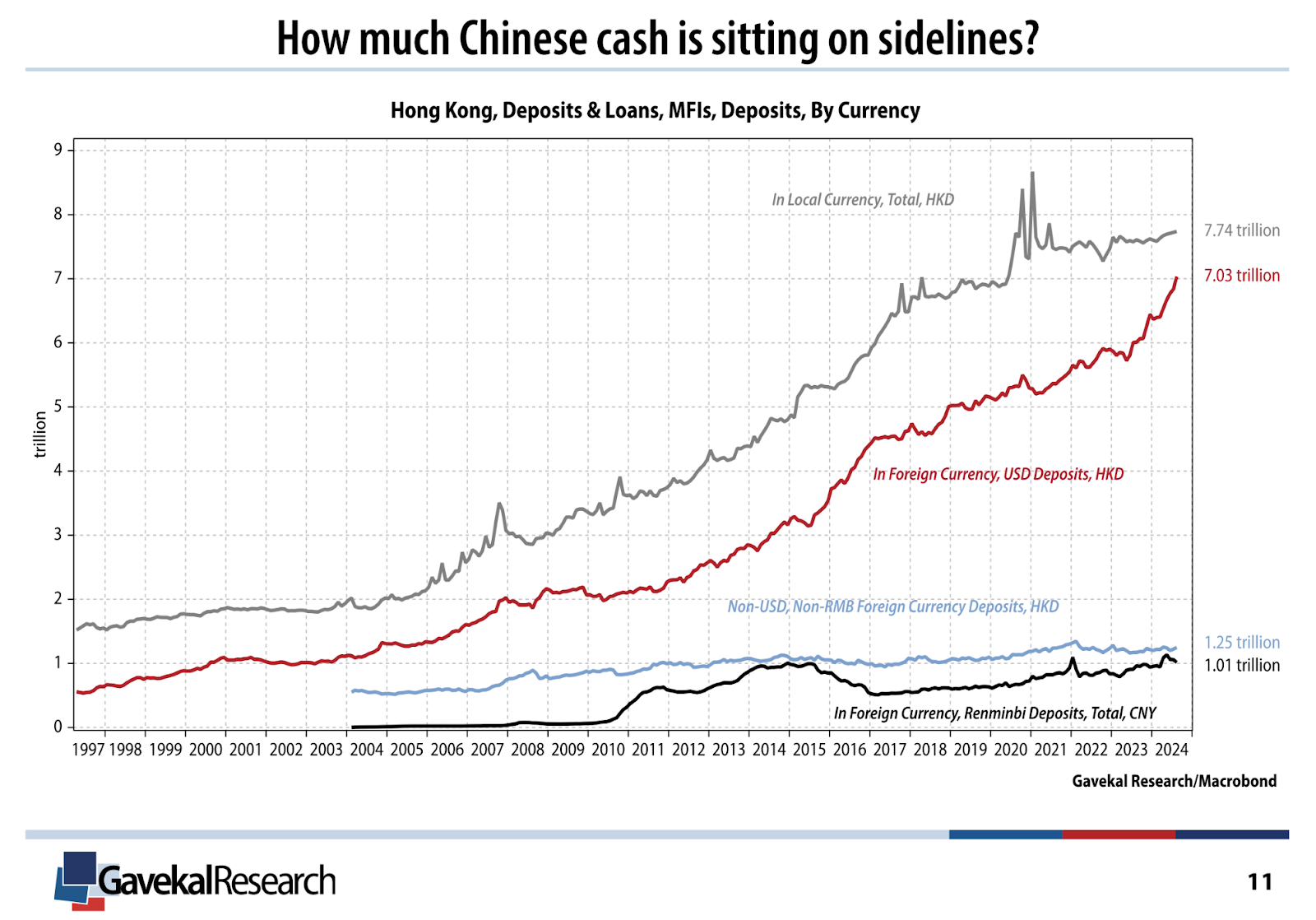

Gavekal Research illustrated this phenomenon on the macro-level in its China Quandray deck. Even though the Chinese economy has been uninspiring this year with missing its “around 5%” GDP target a real possibility, exports continue to do well.

How well? $80 billion dollars in surplus per month!

A combination of recovering demand overseas and unrelenting capacity (or overcapacity?) building at home to produce cheaper and better goods to be sold continues to power China as an export-led economy, tariffs and geopolitics be damned. But where is the money made from export sitting?

Abroad not at home.

How much is sitting abroad?

7 trillion, and counting.

And what is this 7 trillion doing abroad?

Apparently buying gold, sitting in banks, or accumulating US tech stocks.

As if the Mag 7 trade isn’t crowded enough, let’s add another source of price insensitive capital to the flow – Chinese trade surplus.

While the option to invest money abroad is available to large, sophisticated exporters or rich elites with accounts everywhere, that optionality is a pipe dream for your ordinary uncles and aunties, looking to grow or preserve some hard-earned wealth. The net benefits for ordinary consumers of the “wealth effect” from stock market appreciation has been well documented in the US context. A comparable case study hardly exists in the China context because its domestic stock market doesn’t even have its best companies. There are only so many shares of Moutai (or bottles of Moutai) one should buy with one’s life savings. (Kweichow Moutai, the maker of luxury brand Chinese liquor, has the largest market cap on the Shanghai Stock Exchange.)

Will an Ant Group IPO change things overnight? No, but it will be a step in the right direction. Even with all the regulatory overhang, the company did not stop growing and innovating. At home, AliPay continues to be a dominant interface for all things fintech and digital living. It is forging partnerships with the likes of Mastercard to help foreign travelers ease into the digital-first lifestyle of modern China and expand abroad. It is launching a suite of LLM-powered chatbots in personal assistant, wealth management, and health – outpacing its US counterparts like PayPal and Block. And it continues to invest in the less sexy but equally important IT infrastructure layer with its home-grown database solution, Oceanbase, one of its most prominent spinouts during its last four years of “reform”.

To “celebrate” this four-year anniversary of the Jack Ma speech (a weird thing to celebrate, I know), I re-listened to it in its original form. (You can too here, if you can understand or tolerate his Hangzhou accent, or read my translation of it.) Thinking back on everything that happened since, his tone was clearly too aggressive for his own good, but the substance of his central message was sincere and warranted – China needs regulations designed from first principles, not blindly copying the West, so its best tech companies want to stay and create wealth at home.

Time to dust off those prospectus and let Ant IPO. Otherwise, Chinese wealth, and Chinese innovation, may never come home.

该让蚂蚁上市了!

这周是马云“著名”的上海外滩金融峰会演讲的四周年。众所周知,讲完后蚂蚁集团的上市计划就被取消了。蚂蚁的IPO原本会是史上最大规模的IPO,融资额高达345亿美元。它同时还是一次罕见的香港-上海双重上市,能让上海从一个传统金融中心的角色变成顶尖科技公司上市的目的地。IPO在上交所那一块的认购超额了872倍!

然而,所有这些都没有发生。在接下来的四年里,蚂蚁陷入了“监管困境”。为了合规并示意出良好态度,蚂蚁集团将自己拆分为几个独立运营的业务。它还启动了股票回购计划,并向凯雷(Carlyle)和淡马锡 (Temasek) 等大头海外股东分红三轮,来减低因IPO被取消而造成的巨额损失。蚂蚁还被金融监管机构罚了71亿元人民币(9.94亿美元)。马云减少了他在蚂蚁集团的持股比例和控制权。

与此同时,阿里巴巴也经历了自己的“监管困境”,一场持续三年的旅程,包括因“二选一”的行为而被罚款182亿元人民币(28亿美元)。直到一个月前左右,国家市场监管总局才正式宣布,阿里已“整改到位”。

那么,蚂蚁的IPO梦是否该重新点燃了?

我认为是的,不仅因为蚂蚁在经历了四年的监管折磨后,确实“改邪归正”了,应得重归正规,还因为中国在当前经济发展的关键时刻,比以往更需要一笔重磅的国内IPO。

IPO “财富流失”

大多人应该都熟悉“人才流失”这个概念 —— 即一个国家的优秀人才出国移民,去另一个国家学习、工作,安居乐业,取得成功。在资本市场上也存在类似的现象,可以称之为IPO“财富流失”。即一个国家依靠本土人才和经济增长培养出来的优秀公司,却在另一个国家上市,而本国的投资人,尤其是散户,却难以买到其股票并从IPO所可能带来的财富收益。

阿里巴巴就是这种现象的经典案例。早在2007年,阿里集团旗下的跨境B2B网站Alibaba.com曾在香港低调上市 —— 这事现在已经很少有人记得了。之后,阿里于2014年9月在纽约证券交易所(NYSE)做盘了当时全球最大规模的IPO。对于软银、其他专业机构股东和持有股权的员工来说,这是一场前所未有的payday,但对于那些天天网购,腰包里的钱直接兑现成淘宝的收入的老百姓散户们来说,这则是他们十年一遇但又无法参与的大好机会。随后阿里股价一直涨,而国内普通投资者却无法参与,一点没赚到,状况持续了长达十年,直到几周前,阿里才在港交所完成了主板上市,意味着内地的散户终于可以通过 “沪港通” 计划较容易的买到阿里股票了。然而,正如我之前所写的,“致富”的机遇可能早就过去了,完全错过了黄金时期。

目前,像拼多多和百度这样的大科技公司仍未在香港做主板上市,因此对散户来说它们的股票仍然难以买到,就像阿里以前的情况一样。对于那些雄心勃勃的新兴科技公司来说,在上海上市仍被视为“欠佳”,在香港上市仍是个不错的结果,而即便面临各种地缘政治逆风和额外的监管障碍,能去美国上市仍是所有科技公司的“IPO梦”。

小马智行(Pony AI)是这种“财富流失”的最新例子。从技术角度看,它无疑是中国最领先的无人驾驶出租车公司。上周,小马向纳斯达克提交了IPO申请。尽管其业务几乎完全在国内,并且已经在北京、上海、广州和深圳等一线城市获得了运营牌照,但对于乘客来说,小马的股票要比小马的出租车难要的多。

吉利旗下的电动车品牌极氪(Zeekr)今年上旬也选择了在纽约证券交易所上市,而不是香港或上海。由于美国关税和其他针对中国制造的智能车的管制,极氪在美国几乎没有什么商机。其各种“创新”,比如豪华minivan内新设的火锅桌,估计在中国以外也不会产生多少共鸣,但它还是最想要华尔街的钱。尽管上市后其股价一直波动不大,极氪超额认购的IPO还是成功筹集了4.41亿美元。

如果蚂蚁集团的IPO在2020年成功走通,或者在2022年重起(当时有传言),小马或极氪是否会更认真考虑在国内上市,来获取它们所期望的估值和资本呢?这个不好说。但可以肯定的是,直到有一家标杆级别的科技公司在上海成功上市 —— 也是蚂蚁四年前的远景 —— “财富流失” 将继续存在。

吸引钱回家

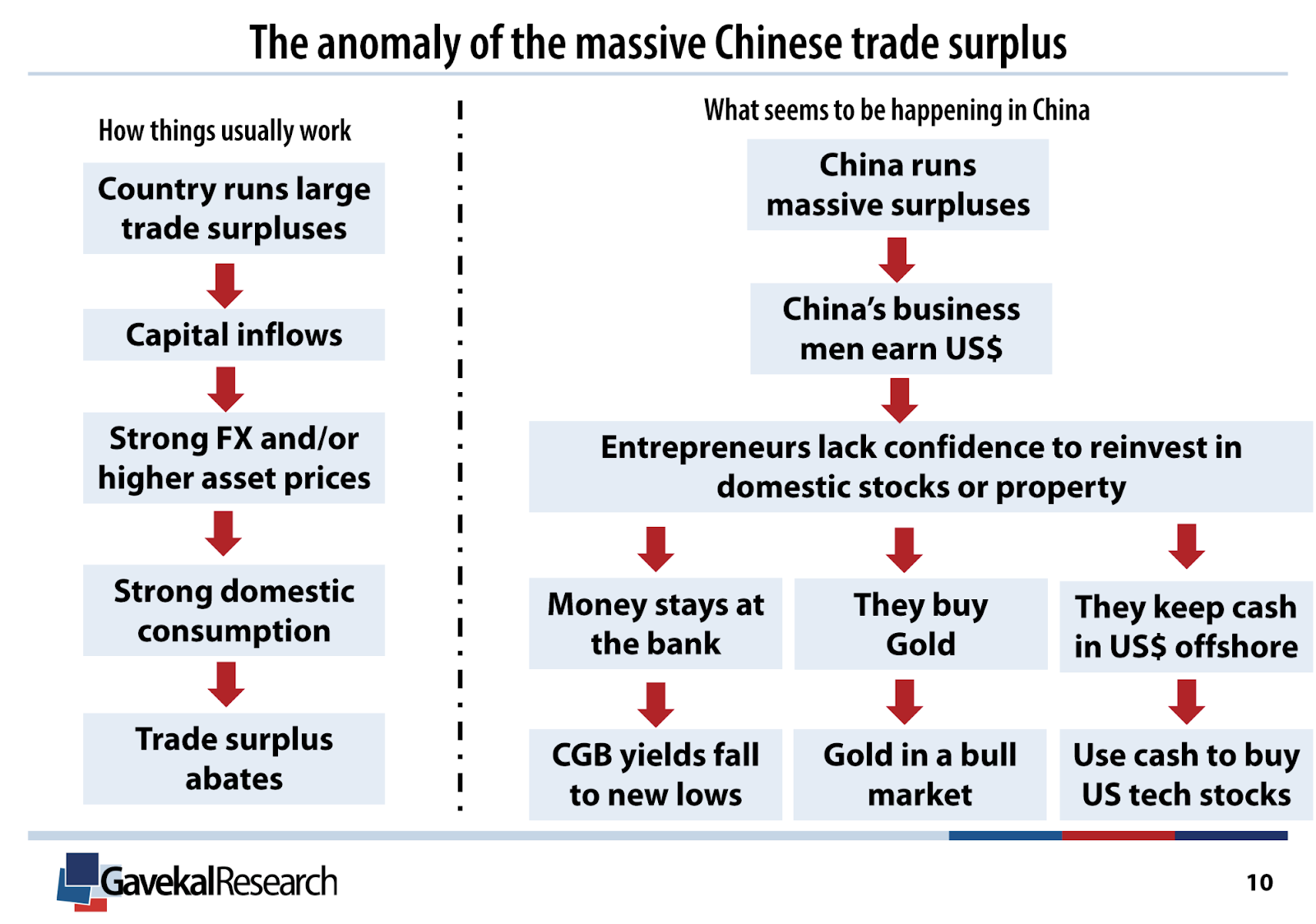

IPO“财富流失”只是整体经济结构性问题的一个症状。这些问题每一点都很复杂,但也可以概括为:中国的钱更愿意留在国外,而不愿意回家。

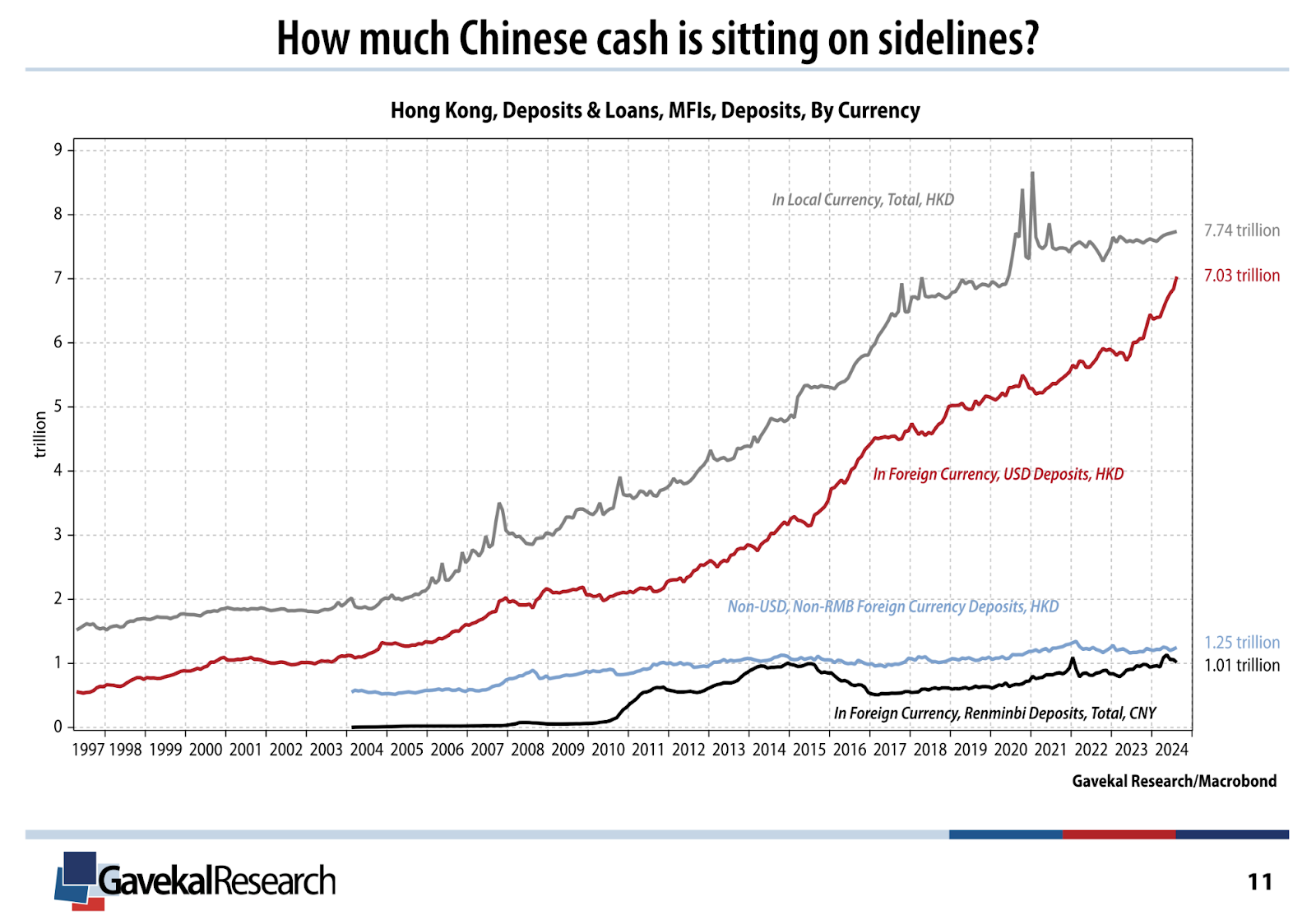

Gavekal Research 在其《中国困局》报告中,从宏观层面描述了这一现象。尽管中国经济今年表现还不够好,要达到GDP目标可能会很吃力,但出口这一块表现一直强劲。

有多强劲?每月顺差达到800亿美元!

海外需求的复苏和国内持续不断对新生产能力(或许是过剩生产能力?)的投资建设,制造出更便宜、更好的产品去出口,继续推动了以出口为主导的经济前行,尽管关税和地缘政治因素依然存在。那出口赚来的钱都在哪儿?

在国外,而不是在国内。

有多少钱在国外?

7万亿,而且还在日益增长。

那么,这7万亿在国外都在做什么?

买黄金、存在银行里,买美国科技股。

仿佛买 “MAG 7”(指美国七大科技股)投资方向还不够挤,现在又加上一个对价格不敏感的资金来源 —— 中国的贸易顺差。

对于大型精通全球市场的出口商或在全球各地都拥有账户的有钱精英来说,把钱留在国外并不难。但对于那些普通的叔叔阿姨们来说,他们辛苦积攒的财富要想通过这种渠道增值或保值,只能是个幻想。在美国,股市上涨所带来的 “财富效应” 给普通消费者带来的收益已有很多成熟的研究。而在中国,由于国内股市连自己最棒的公司都没有,“财富效应” 对老百姓的消费能力影响很难做类比的分析。毕竟,一辈子的积蓄又能买多少茅台的股票(或茅台酒)呢?

蚂蚁如果上市会立刻扭转这种现象吗?当然不会,但会是朝正确方向迈出的重要一步。即便在监管压力下,蚂蚁仍在继续创新和扩大业务。在国内,支付宝仍然是金融科技和数字生活的核心平台之一。它与万事达卡(Mastercard)等海外公司建立了合作伙伴关系,帮助外国游客更容易的适应现代中国的数字化生活方式,并逐步向海外扩展。此外,蚂蚁还推出了一系列基于大语言模型(LLM)的聊天机器人,覆盖个人助理、财富管理和健康领域,发展速度超过了美国同行,如PayPal和Block。同时,它继续投资于不那么引人注目但非常重要的IT基础设施层面,比如自研的数据库,Oceanbase,也是其过去四年“整顿”中最为突出的分拆业务之一。

为了“纪念”马云演讲四周年,我又重新听了一遍他当时的发言。回顾之后发生的一切,他当时的语气确实有点“过火”,但他想表达的核心看法还是诚挚且合理的 —— 中国需要从根本原则出发设计自己的监管体系,而不应盲目效仿西方的模式,这样中国本土的顶尖科技公司才会愿意留在国内创造财富。

所以该让蚂蚁上市了。否则,中国的创新和财富,会继续流失于海外。