Welcome to our first-ever quarterly investment performance deep dive letter. To new and old readers alike, a friendly reminder of who we are: at Interconnected, we run a long/short equity portfolio that is laser-focused on investing in the “picks and shovels” of the interconnected global digital AI economy. I draw on my technology business operator's experience and geopolitical antennas to bring an edge to how we assess a tech company’s rhythm and prospects in a constantly changing world.1 Internally, we like to say, “we can’t time the market, but we can time companies.”

Here is our Q3 2023 and cumulative 2023 performance, and comparisons to three relevant benchmarks.

1 My past experiences include: senior leadership position at GitHub (the world’s largest developer and open source technology platform, now owned by Microsoft), a unicorn database startup, early stage VC, and the White House and Department of Commerce during the Obama administration. I studied law and computer science at Stanford; international relations at Brown.

2 Through September 30, 2023. Returns are net of an assumed management fee of 0.5% and performance fees of 15% calculated on a proforma basis. The 3rd-party auditor’s statement of investment performance statistics document is available upon request.

Top holdings in alphabetical order (as of September 30, 2023):

- ALIBABA GROUP HOLDING ADR

- GITLAB INC

- TWILIO INC (Call Options)

- ZOOM VIDEO COMMUNICATIONS

We have a long bias, because the digital AI economy is in its early days, and it will take a long time to reach full potential. We only short names opportunistically, when the market gets out of whack and gets ahead of reality, which tends to happen from time to time. We look for long-term investment opportunities, where we prefer to hold for a minimum of three years. Thus, the list of top holdings will not change much in future letters and will look quite boring. We like boring.

Performance and Portfolio Review

The overall market condition was tough in Q3, continuing a sideways pattern punctuated by a clarity of “higher for longer” interest rate regime, a year-plus long hot war in Ukraine, more cold war behaviors between the US and China, and now even more geopolitical uncertainty with another hot war simmering in Gaza. By staying disciplined and focused on only things we understand well within our circle of competence, we managed to come out ahead. However, it is hard to celebrate this inconsequential accomplishment in the face of consequential, world-changing events, like the Hamas terrorist attack on Israel, an impending larger-scale conflict in the Middle East, and the extraordinary human sufferings and losses from war that still vex humankind.

As nothing more than an investor and newsletter-writer, there is not much I can do to alter the course of history. That being said, I always believe in doing what I can with what I have to support what ought to be supported. To that end, we have donated some of our Q3 profit to two non-profit organizations, United Hatzalah and The Jewish Agency for Israel, that are providing emergency medical and other humanitarian services to victims and their families in Israel.

Turning to our performance and portfolio, I’d like to highlight two portfolio activities that either had “move the needle” impact or were emblematic of what we do.

Shorting overvalued AI stocks in the era of “higher for longer”

We shorted two names during Q3 – MongoDB ($MDB) and Cloudflare ($NET). Because both positions worked out much faster than we expected, they were opened and closed within the same quarter. While we have no obligation to disclose such activities – in fact, much larger funds who have 13F duties mostly don’t disclose these intra-quarter moves – we believe being transparent, especially when doing so creates an opportunity to inform readers why we think the way we do with real “skin the game” examples, is always worthwhile.

The logic of our shorts is as follows: in this extended higher interest rate macro backdrop, very (very) few companies deserve or can sustain a valuation that is more than 15x enterprise value over sales multiples (EV/sales), especially ones whose free cash flow generation is still small and/or inconsistent. However, the AI hype in the first half of 2023 has pumped up a group of companies, whose technology offerings may indeed play a critical role in the global digital AI economy, but whose business model and product nature make it hard to justify lofty valuations. MongoDB and Cloudflare, two companies that have been trading with high EV/sales multiples while still displaying negative free cash flow margins, exemplified the combination of these characteristics.

Both companies do offer technology products – Mongo’s Atlas, Cloudflare’s Worker plus its robust worldwide network – that lend themselves to the long-term growth of generative AI. Both companies are also releasing features quickly to cater to that future; Mongo introduced vector search in June and Cloudflare did the same in September (which also indicates that vector search itself is not much of a technology moat; a topic we will address with more detail in the future). Yet, both companies operate a usage or consumption-based business model that does not lend itself well to upcharging for new features (as opposed to a seat-based model). In a way, that is what makes consumption a more customer-friendly model and, oftentimes, a leading indicator of broader economic activities. I am a fan of usage-based models in general. However, on a specific level, this model also sets up any short-term valuation bump induced by immediate revenue expectation from AI for guaranteed disappointment, a dynamic we have written about previously. And the casualties of that disappointment are overvalued AI stocks that structurally cannot easily charge more.

To be crystal clear, I don’t think generative AI is a fad. I also don’t think MongoDB and Cloudflare are bad companies. Both will play a meaningful part in AI going forward. I greatly admire both companies’ speed of execution, shipping cadence, innovative culture, and management competence. At the right price, we would love to own their shares, and a lot of them. But to claim competence over categories like DevOps, databases, and cloud infrastructure, which we do confidently, it is important to know what is cheap and what is expensive, and act accordingly.

We can be short-term pessimists. But we are always long-term optimists.

Our journey with $BABA

Speaking of being long-term optimists, I would like to pull back the curtain slightly on how we think about Alibaba, as a chunk of our shares reach their one-year anniversary (and we have no intention of selling them).

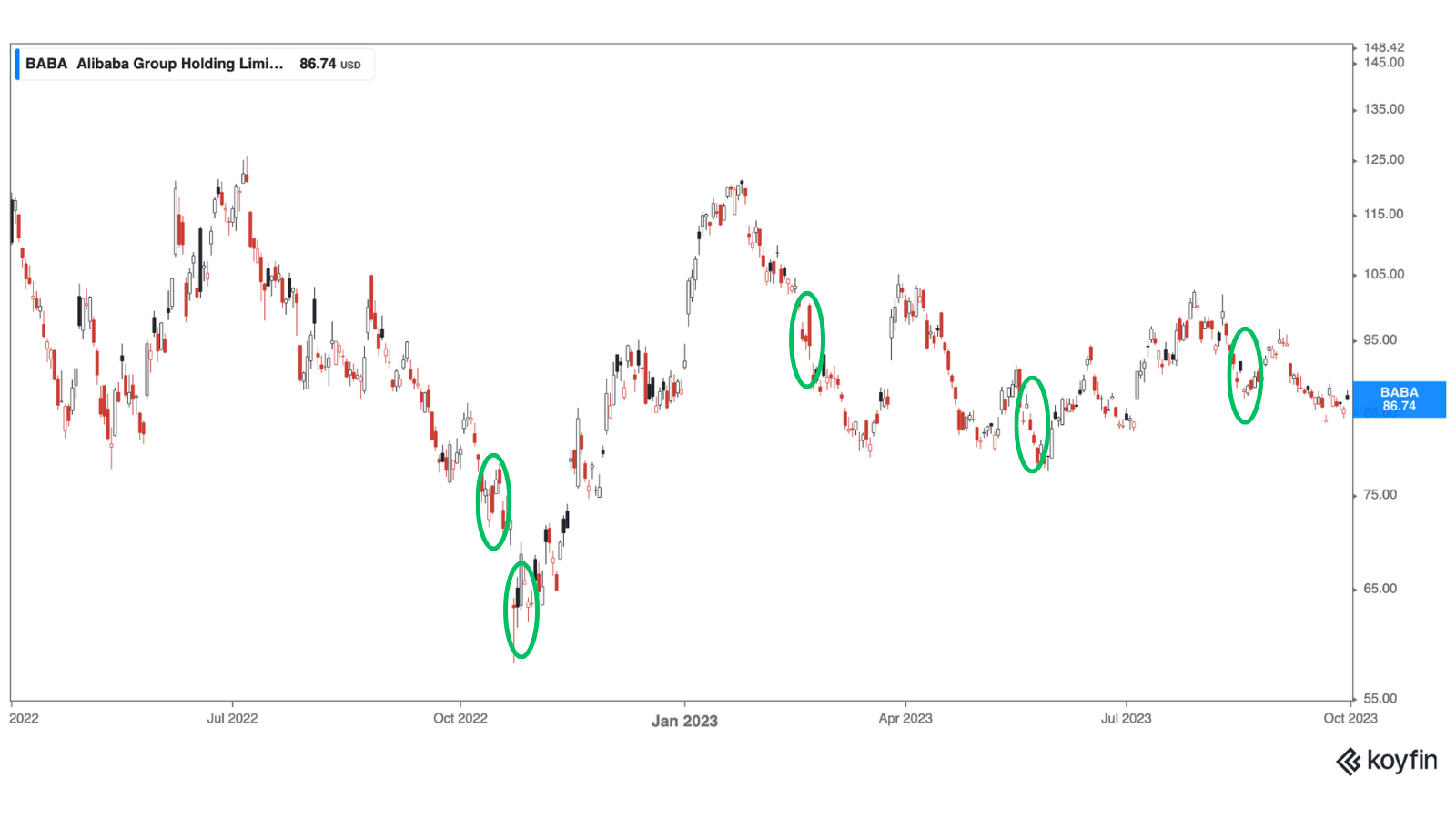

Below is a chart of Alibaba’s stock price from April 1, 2022 to October 1, 2023. The green circles demarcate moments when we bought shares.

My interest in Alibaba has always been AliCloud, its massive public cloud platform. I have little interest or expertise in Alibaba’s e-commerce, delivery, entertainment, and other verticals, except to the degree in which they all use AliCloud as their digital backend and serve as internal customers to battletest its cloud services.

Before China's tech crackdown, AliCloud’s global market share has been strong, sometimes ranked as the world’s number 3 before Alphabet’s GCP, depending on which analysts report you read. As the crackdown subsides, AliCloud still has the most market share in China’s domestic market by a wide margin, while its overseas data center investments buildout hasn’t stopped. However, being still a relatively small albeit fast growing part of Alibaba’s sprawling empire, it was not a pure play, so the price had to be very attractive and offer a large margin of safety to justify buying.

Price indeed became attractive leading up to the 20th National Congress of the Chinese Communist Party last October, when Alibaba shares dropped to the 60s, momentarily touching a low of $58.01 a share, when the world was disappointed that Zero Covid was not lifted. To put this price in context, when Alibaba IPO’ed on the NYSE in September 2014, the offering price was $68 and first day of trading closed at $93.89. Famed investor Stanley Druckenmiller likes to use stock prices as measurements of expectations of real economic activities in the next 6-12 months. If we apply Druckenmiller’s lens through the prism of Alibaba, then the market had a lower expectation of Alibaba’s future and China’s economy by October 2023 (12 months after the 20th Party Congress, or now), and a higher expectation of the same asset almost a decade earlier by September 2015 (12 months after Alibaba’s IPO). That level of pessimism, based on our assessment, was overdone, so we started buying.

With the delisting risk removed last December, Zero Covid later gone (though the collective PTSD this policy triggered is still sagging China’s economy), and, most importantly, Alibaba’s own corporate reorg, we continued building our position. The corporate reorg is the most material change for me, because it presented a clear path to own AliCloud outright when it completes its independent listing, which would make it the largest pure play public cloud investment option on the market. (To be exposed to AWS, you still have to buy Amazon shares and put up with the razor-thin margins of a retail business.) AliCloud’s overseas data center footprint and the global nature of providing cloud services also means AliCloud is not completely, though still mostly, dependent on China alone – a small hedge against a stagnant China.

However, Alibaba’s ongoing corporate reshuffling in the last few months, especially regarding AliCloud’s leadership (Daniel Zhang is CEO, Daniel Zhang is not CEO, Eddie Wu is CEO but only on an interim basis?) is giving us pause. No technology business can live up to its full potential without a consistently competent leadership. Thus, we will unlikely be building our position further until the dust of leadership change settles for good.

Our journey with $BABA will be bumpy, but it will continue.

Looking Ahead

Navigating the near future (defined in my mind as one to two quarters) will be very difficult when the things we know will happen for sure are as such: an ongoing hot war in between Ukraine and Russia, an escalating hot war in the Middle East, and a federal funds rate hovering somewhere between 5-6%. After all, there is an inextricable link between the price of war and the price of money.

Philip Fisher touched on this link in his classic investment book, "Common Stocks and Uncommon Profits", where he wrote:

“Modern war always causes governments to spend far more than they can possibly collect from their taxpayers while the war is being waged. This causes a vast increase in the amount of money, so that each individual unit of money, such as a dollar, becomes worth less than it was before. It takes lots more dollars to buy the same number of shares of stock…In other words, war is always bearish on money.”

Keep in mind, Fisher published these words in 1958. Since then, war has only gotten more modern, a unit of money like the dollar is worth a whole lot less, and the future is no more certain or less dangerous.

Nevertheless, there are many constructive things to do. We are working on investment ideas, researching companies, and assessing technological trends everyday, some of which we will share in our monthly market observation letter going forward.

One geopolitical event we will also be paying much closer attention to is the Taiwanese election – election day is January 13, 2024. I have not spent much time thinking about this event because, as a former political campaign staffer who has worked multiple cycles in the US, I know not to pay attention too early because it is usually a waste of time. November 24 is the deadline for candidates to register with the Taiwanese Election Commission; only by then will we know who will actually be on the ballot for voters to choose from. The end of the beginning is near, so we will begin watching intently.

I look forward to writing to you again in this fashion after Q4 ends, and when I will have the entirety of 2023 to look back on. Until then, thank you for reading.

Kevin S. Xu

Date: October 18, 2023

(You can access the original letter in a view-only Google Doc link HERE.)

LEGAL INFORMATION AND DISCLOSURE

This letter expresses the views of the author as of the date indicated and such views are subject to change without notice. Interconnected Capital, LLC (“Interconnected”) has no duty or obligation to update the information contained herein.

Further, Interconnected makes no representation, and it should not be assumed that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This letter is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources.

Interconnected believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

All figures are unaudited. Interconnected does not undertake to update any information contained herein as a result of audit adjustments or other corrections. Past performance is not indicative of future results.

This letter, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Interconnected.